franckreporter

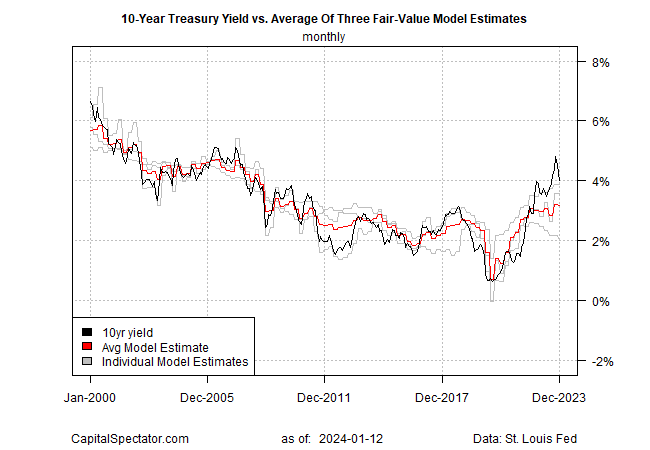

The US 10-year Treasury yield continues to fall, which is narrowing the hole between the upper market fee and a lesser “fair-value” estimate, based mostly on the average of three models run by CapitalSpectator.com.

As latest updates remind (see this November 2023 review, as an illustration), the benchmark 10-year fee has traded considerably above the typical fair-value estimate for an prolonged time period. As anticipated, the unusually widespread is lastly narrowing. Nonetheless, the market fee nonetheless trades properly above the typical fair-value estimate, which suggests a bias in favor of additional narrowing within the months forward. The query for the way it narrows is one in all mechanics: Will the hole fade attributable to a declining market fee, a rising estimate by way of the modeling, or each?

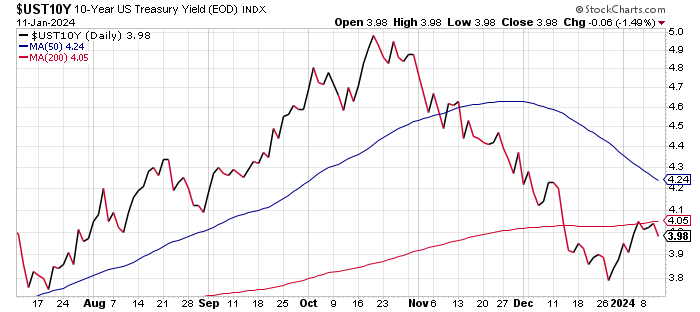

For some perspective, let’s begin with a chart of latest historical past for the 10-year yield. On the shut of buying and selling on Thursday, Jan. 11, the benchmark fee eased to three.98%. The draw back pattern in latest months leaves the 10-year yield greater than a full proportion level under its earlier 5% peak in October.

The December fair-value estimate for the 10-year fee is 3.16% (crimson line in chart under), which is 82 foundation factors under the present market fee. The extensive hole nonetheless means that the market fee will fall and/or the fair-value estimate (based mostly on month-to-month information) will rise, or some mixture of the 2.

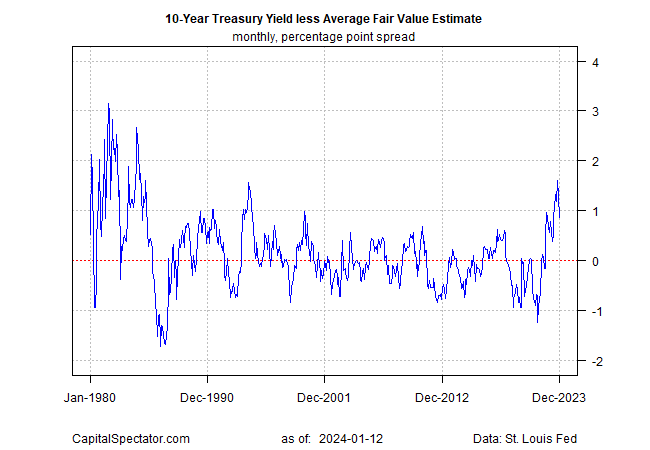

The following chart under exhibits the unfold between the market fee and common mannequin fee. The primary takeaway: the hole continues to reverse after spiking to an unusually excessive stage that was pushed by a pointy rise out there yield.

Regardless of the narrowing hole, the unfold stays comparatively extensive. The tendency for reversion to the imply to prevail, finally, means that this extreme situation will proceed to normalize within the close to time period. As The Capital Spectator observed in November, “history suggests such an extreme level doesn’t last long.” At this time’s replace offers a recent motive to imagine no much less.

One caveat to remember: Honest-value modeling isn’t helpful for timing market adjustments within the quick time period, but it surely does supply context for marking extremes and managing expectations, and, maybe, creating methods for longer-run funding choices. Accordingly, the modeling continues to foretell that the extensive hole out there yield vs. the typical fair-value estimate has peaked and so extra narrowing lies forward.

Editor’s Observe: The abstract bullets for this text had been chosen by Looking for Alpha editors.