Henrik5000

I have been bearish on the economy for several quarters now, arguing the most likely economic scenarios by the end of 2024 are either recession or a significant bout of Stagflation. Obviously, neither of those scenarios unfolding would be good for stocks.

I base those views on several factors. The most important of which is the Federal Reserve embarked on its most aggressive monetary stance since the days of Paul Volcker in March 2022. This monetary tightening phase was triggered by the highest inflation levels since the late ’70s/early ’80s. A succession of hikes took the Fed Funds rate from basically zero to 5.25% to 5.5% in a relatively short amount of time. To think the central bank is going to pull off a “soft landing,” something they have managed to do successfully once in my almost 58 years on this planet (1995), always seemed more like Hopium than a likely scenario.

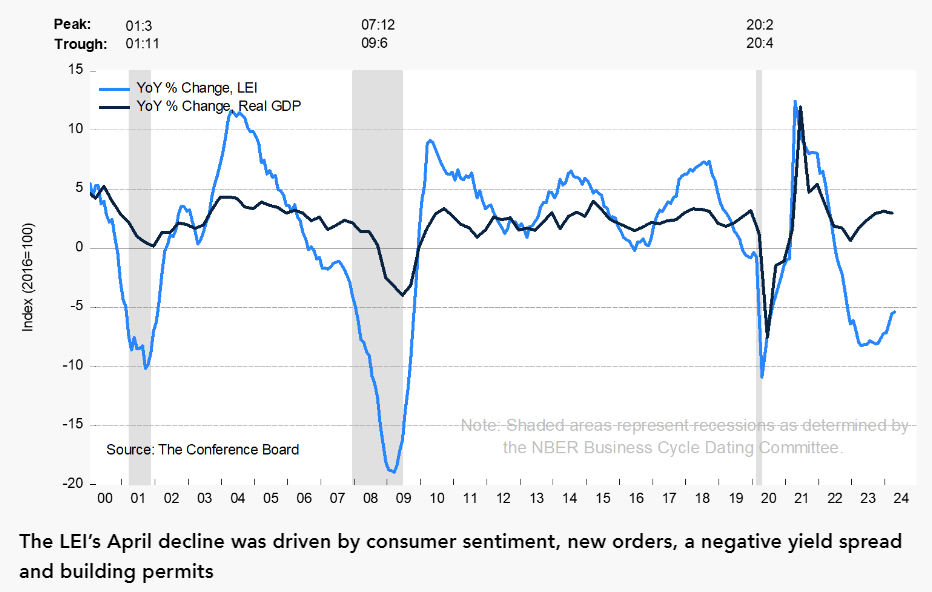

Conference Board

In addition, indicators that have had a good long-term track record of predicting recessions have been flashing yellow for some time now. The monthly Leading Economic Indicators reading has been positive for just one month (February 2024) for over just over two years now. The yield curve also went inverted midway through 2022 and has stayed that way ever since.

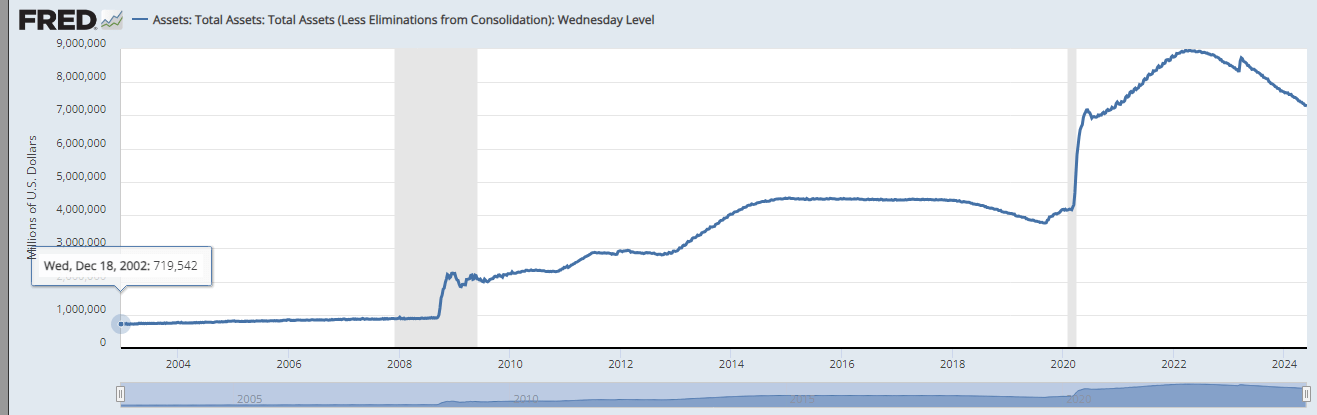

Now, some have argued these indicators are either no longer useful or are just wrong this time around. However, I would posit that there were some massive excesses of cash flowing throughout the economy that needed time to be burned off before traditional indicators were predictive again. First, the Federal Reserve expanded the money supply by some 40% in response to the pandemic. The central bank also boosted their balance from roughly $5 trillion before the pandemic to a peak of a bit over $9 trillion, which they have been slowly reducing since.

Federal Reserve Balance Sheet (Federal Reserve Bank Of St. Louis)

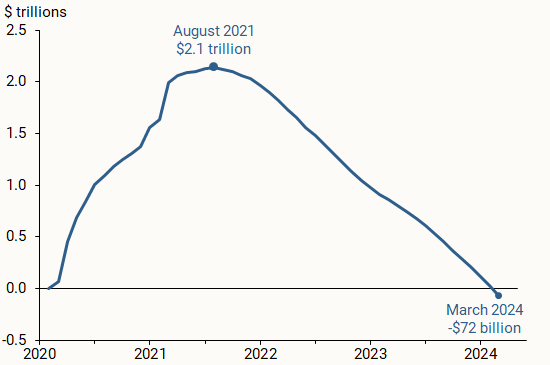

In addition, thanks to massive congressional largess and Covid related stimulus payments, excess personal savings peaked at $2.1 trillion in August 2021. Those excess funds have been burned through and personal savings rates are now near historical low levels and less than half what they were pre-pandemic.

U.S. excess personal savings (Bureau of Economic Analysis)

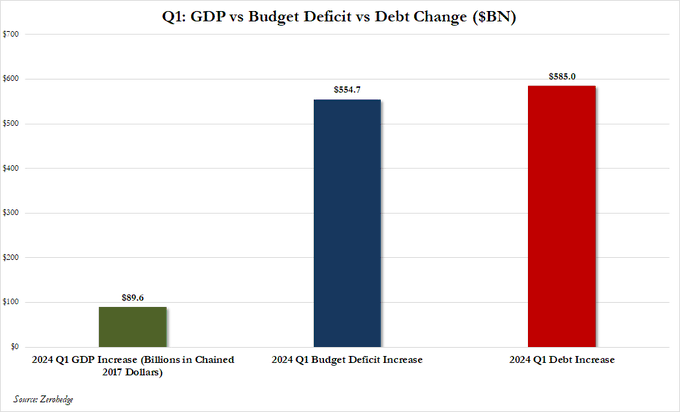

Finally, we have the Federal government engaged is huge deficit spending totaling roughly six to seven percent of annual GDP despite the country being in an economic expansion. Unfortunately, the U.S. economy is getting less and less “bang for the buck” for all of this largess as the national debt continues to accelerate higher.

ZeroHedge

However, it appears some of the chickens are finally coming home to roost and there are many signs the economy is cooling in 2024, perhaps significantly. Here are 10 recent signs of reduced economic activity investors should be aware of. In no particular order chronologically.

1. The second estimate of first quarter GDP growth was revised down from a preliminary 1.6% to 1.3% last week. This continues a decelerating trend line, with GDP rising 4.9% in the third quarter of last year and 3.4% in the fourth quarter.

2. Goldman Sachs took down its projection for second quarter GDP growth from 3.2% to 2.8%. The Atlanta Fed lowered its Q2 GDP forecast from 2.7% to 1.8% late last week as well. The main driver of both 1st and 2nd quarter GDP estimates was weakening consumer spending. I recently covered the growing challenges most consumers face in this article.

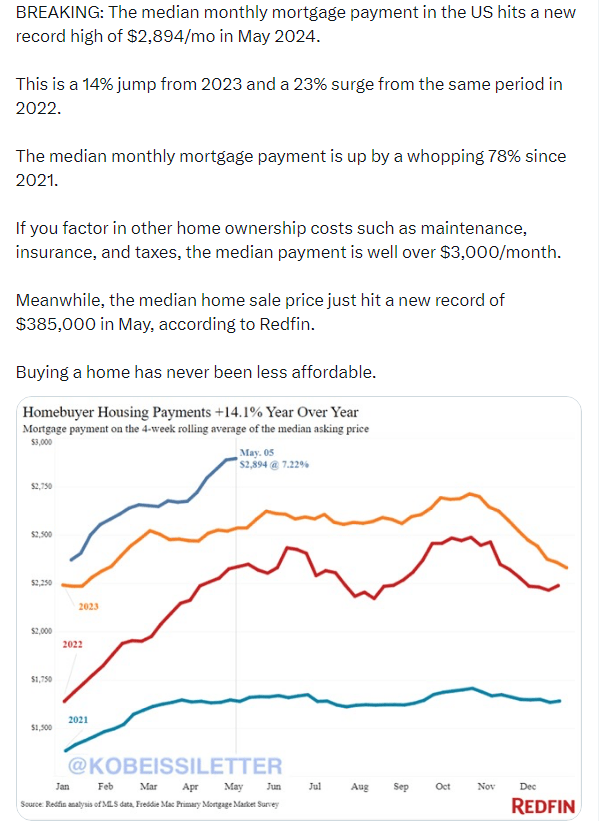

3. Pending home sales in April plunged 7.7%, far more than the 1.1% decline expected. This was the lowest level of monthly pending sales since April 2020 when most of the country was in lockdown mode. 2023 saw the lowest number of existing home sales since 1995, thanks largely to high mortgage rates. Housing related activity constitutes approximately 15% of overall economic growth, it should be noted.

4. The housing sector is also unlikely to get better in the months ahead and will likely remain weak given horrid housing affordability levels, which is nicely captured below.

Kobeissiletter

5. Manufacturing activity has been in contractionary territory for most of the past two years, while Services have seen expansionary levels over that time. Last week, the May Chicago PMI fell to 35.4 from the 40.8 level expected. Any signal under 50 signals contraction. The May ISM Manufacturing PMI report also slipped into recession for the second month in a row.

6. Any company supplying the AI revolution like Nvidia Corporation (NVDA) is minting money right now. However, most corporations appear to be struggling to maintain profit margins. Corporate profits unexpectedly fell 1.7% in the first quarter of this year. The consensus was expecting a rise of 3.9%. A significant miss and not what one would expect during an economic expansion.

7. The April BLS Jobs report showed just 175,000 positions created in April, the lowest level in six months and below expectations. The unemployment rate also ticked up to 3.9% from 3.8% previously. Investors will be looking at the May BLS Jobs report closely when it comes out before the bell on Friday to see if the jobs market is weakening or April’s reading was a one-off.

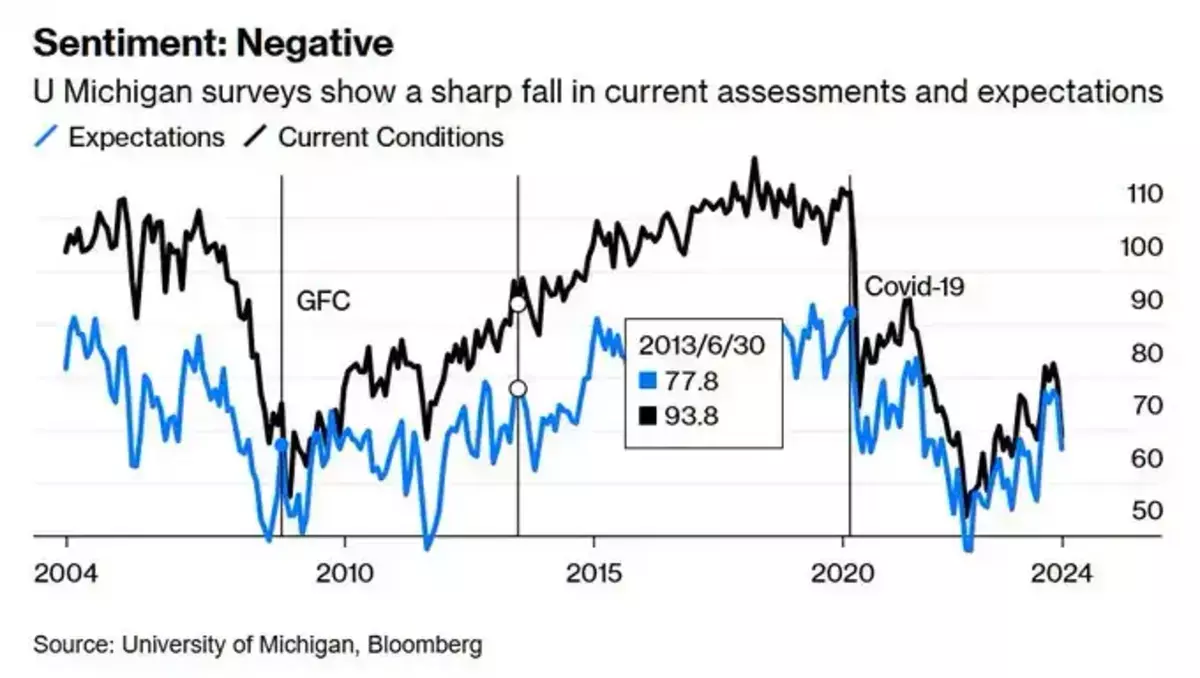

8. Consumer sentiment is far below pre-pandemic levels and appears to be weakening. Consumer spending makes up nearly 70% of U.S. economic activity, it should be noted.

University of Michigan, Bloomberg

9. Demand for commodities appears to be ebbing, with the price of Brent falling below $80 a barrel for the first time since February and the Goldman Sachs Commodities Index just suffering through its worse four-day stretch so far in 2024.

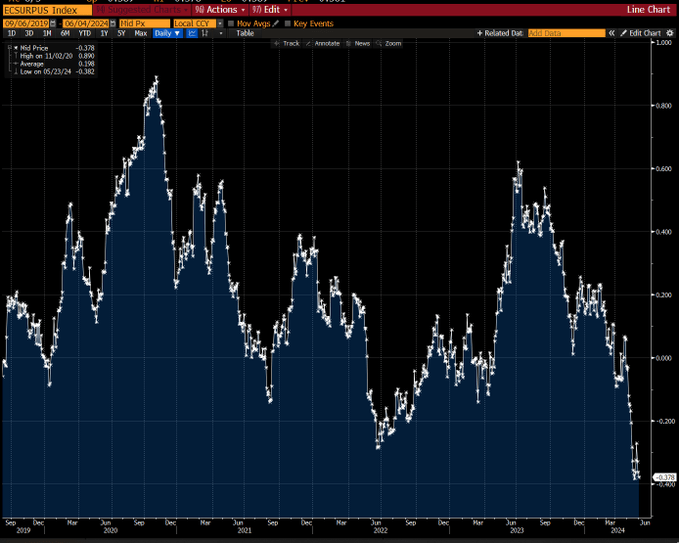

10. The Bloomberg Economic Surprise Index is currently as negative as it has been since 2019, just before the Covid outbreak came to our shores.

Bloomberg

Given the economy seems to be clearly slowing and likely heading to either recession or Stagflation, with the S&P 500 (SP500) priced at just over 21 times forward earnings; my portfolio continues to be very cautiously positioned. Roughly half is in short-term treasuries, yielding nearly 5.4%. The rest is largely within covered call holdings around the relatively few equities that sport reasonable valuations in an overbought market. This portfolio allocation is providing decent returns while I await significantly lower entry points to be more aggressive, deploying funds into equities. If the economy is indeed slowing substantially, we should get a significant pullback in the market at some point in the second half of this year.