ATU Photos/The Picture Financial institution through Getty Photos

Co-produced by Austin Rogers

The US financial system as a complete may not be in recession, however it’s definitely experiencing a “rolling recession” affecting particular industries.

One of the vital apparent sectors of the financial system that’s struggling its personal mini-recession is the housing market.

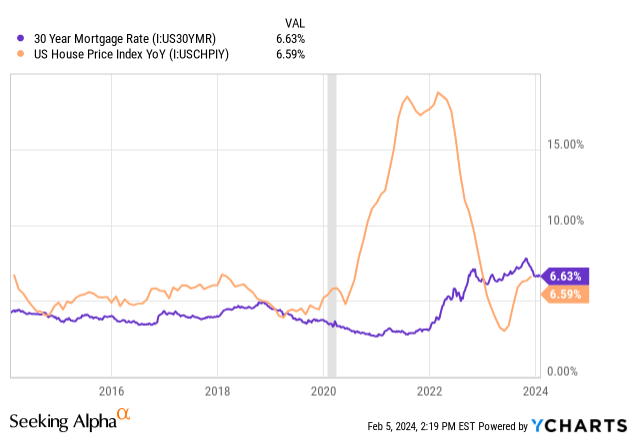

The ultra-low mortgage charges of 2020-2021 fueled a homebuying frenzy, particularly amongst Millennials who’re coming into their prime single-family house years. Dwelling costs soared, cooling solely briefly as mortgage charge spiked to a 25-year excessive in 2023.

At this time, house costs proceed to rise as stock of properties in the marketplace is low and mortgage charges have receded a bit. No current house owner is keen to surrender their present mortgage charge of 3-4% to maneuver to a different home that may have a 6.5%+ mortgage charge.

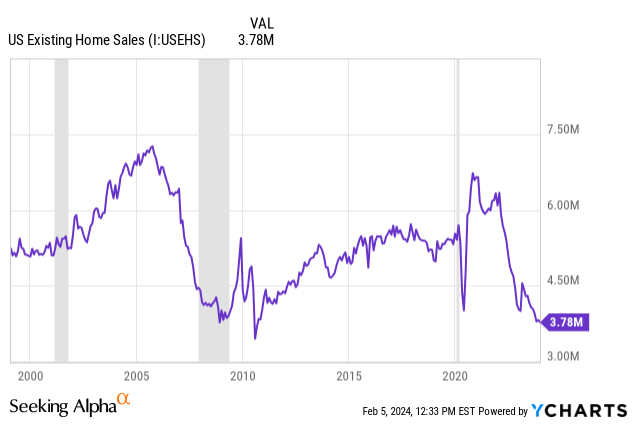

Therefore we discover that gross sales of current properties (by far the biggest a part of the house gross sales market) has plunged to Nice Monetary Disaster-era lows.

It might not be an excessive amount of of an exaggeration to name the US housing market “frozen.”

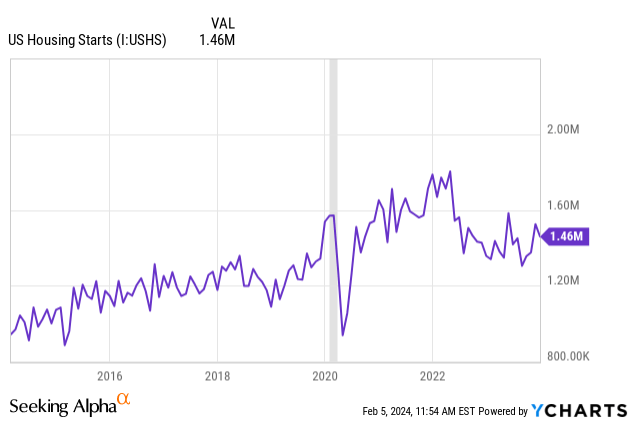

On the identical time, US housing begins, which incorporates each single-family and multi-family housing, have dropped from their elevated post-pandemic ranges and now hover under their pre-COVID trendline.

Thus, whereas house costs proceed to carry up, the assorted industries that serve the housing market and thrive on house gross sales and development are struggling their very own mini-recession.

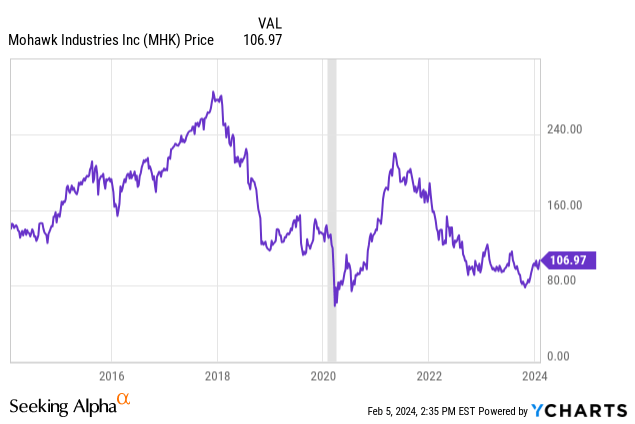

Take, for instance, Mohawk Industries (MHK), a producer of assorted sorts of flooring, primarily for residential use. After its inventory value surged in the course of the go-go days of homebuying in 2021, it has since slumped again to COVID-era ranges.

However Mohawk is not one of many cyclical shares we’re masking on this article.

As an alternative, we wish to try two different, at present high-yielding cyclical corporations which are being punished proper now from the housing market recession. These two corporations have wonderful long-term observe data of efficiency, boast main market shares of their respective product traces, and luxuriate in lengthy histories of paying dividends with out cuts.

These two corporations are Whirlpool (WHR) and Leggett & Platt (LEG).

Are the spectacular dividend data of WHR and LEG vulnerable to coming to an finish in the course of the present housing market mini-recession?

Let’s discover.

Two Cyclical Blue-Chips Tied To The Housing Market

WHR is a number one American producer of family home equipment, each giant and small. They make fridges, oven/stoves, dishwashers, microwaves, laundry machines, and sure smaller home equipment by way of their KitchenAid and InSinkErator manufacturers.

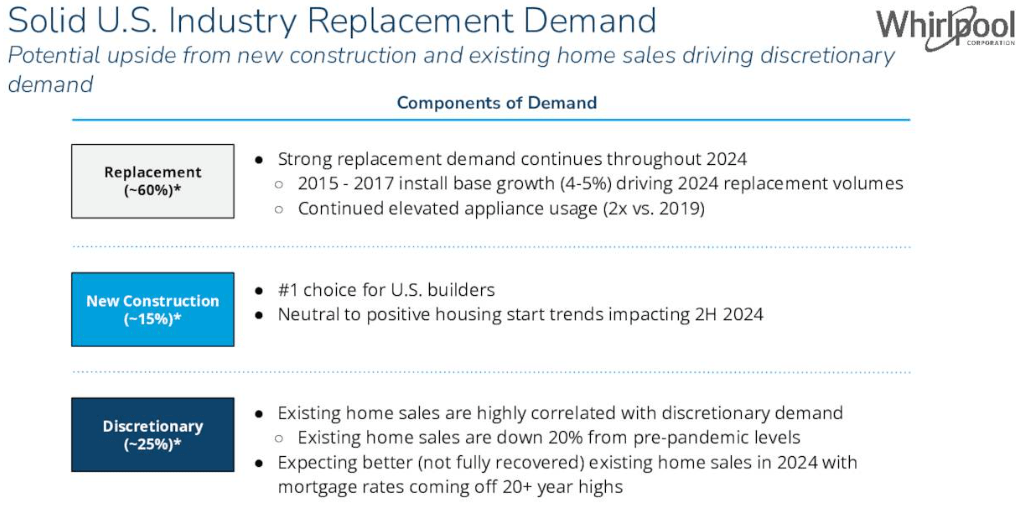

Traditionally, about half of WHR’s gross sales are tied to house gross sales, with the opposite half being replacements. WHR boasts the #1 market place in home equipment for brand new construct properties, which clearly means extra new house development is sweet for WHR’s enterprise.

At present, nonetheless, replacements account for round 60% of gross sales due to the drop in house gross sales.

WHR This autumn 2023 Presentation

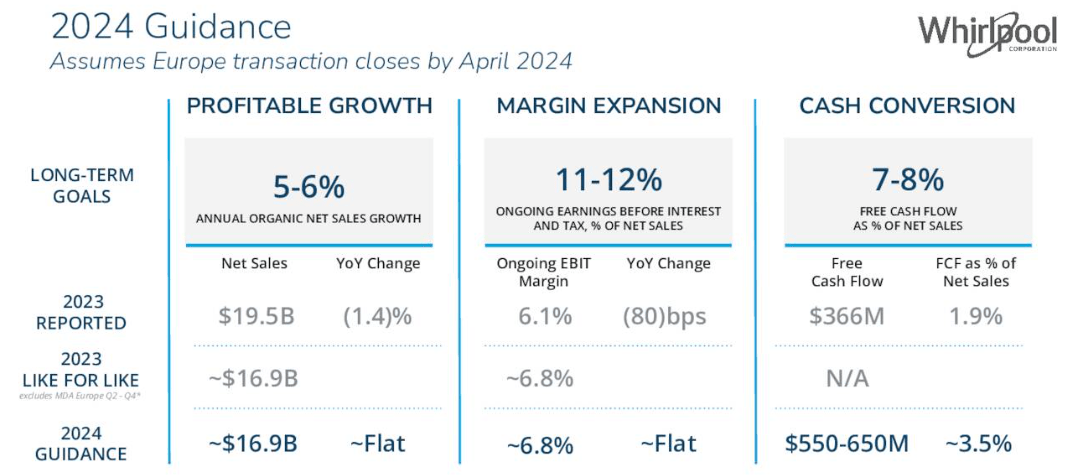

In 2023, gross sales got here in roughly flat YoY, and whereas margins improved, free money circulation and FCF conversion dropped. In comparison with WHR’s long-term FCF conversion goal of 7-8%, WHR generated a mere 1.9% FCF conversion in 2023, and 2024’s metric is anticipated to enhance solely to ~3.5%.

In comparison with 2023’s $366 million in FCF, WHR has guided for a rebound in FCF in 2024 to $550-650 million in opposition to flat gross sales. This must be pushed nearly fully by value cuts — $300-400 million value of value cuts, to be precise.

WHR This autumn 2023 Presentation

This is a crucial metric to look at, as a result of in 2023, WHR’s ~$400 million dividend was not lined by FCF. Hopefully FCF will bounce again in 2024 to a ample diploma to cowl the dividend, deleverage, and maybe additionally fund some share buybacks.

WHR’s efficiency and dividend security this yr relies upon rather a lot on the route of the housing market. If house gross sales quantity makes a comeback this yr and there’s a rise in new properties getting constructed, then WHR ought to take pleasure in a pleasant rebound. If the housing market continues to languish with minimal house gross sales for a lot of the yr, WHR’s efficiency would doubtless proceed to languish with it.

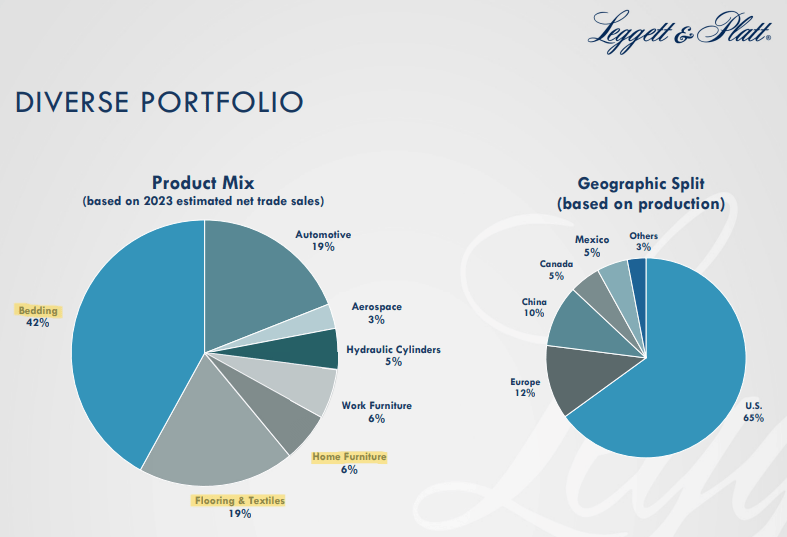

In the meantime, LEG is a business-to-business industrial firm that’s not customer-facing. They produce intermediate parts of bedding, flooring, furnishings, and sure automotive and aerospace merchandise. Roughly 2/3rds of LEG’s merchandise are instantly or not directly tied to the housing market and residential gross sales.

LEG November Presentation

The largest catalyst for getting new mattresses or furnishings, in any case, is shifting into a brand new house. With fewer house gross sales, fewer individuals are shifting into new properties.

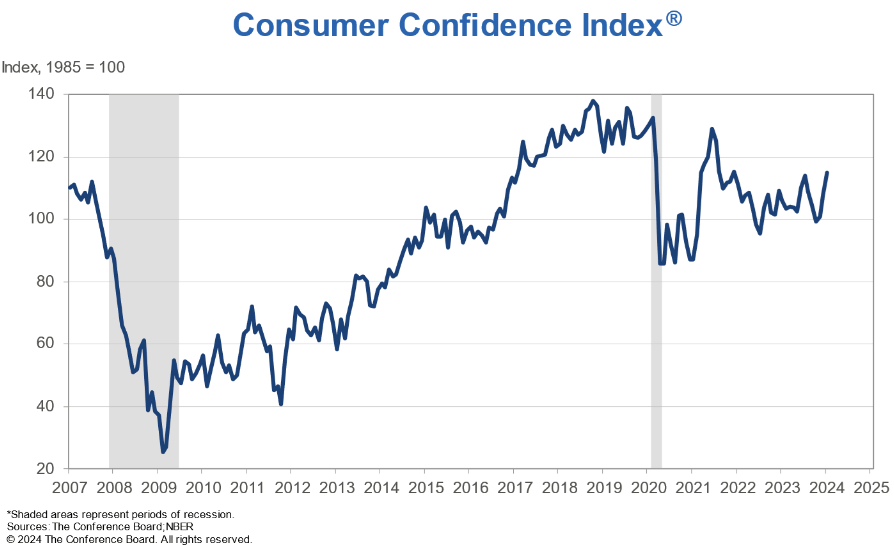

In fact, client confidence performs an enormous position in LEG’s gross sales as nicely, as a result of many if not most mattress and furnishings gross sales are to interchange current merchandise. Whereas client confidence took a bit hit in the course of the pandemic after which once more in the course of the inflationary surge, confidence rebounded considerably in January.

The Convention Board

On the finish of the day, bedding, furnishings, and to some extent flooring are discretionary merchandise that may be deferred for an indefinite interval till shoppers really feel able to spend cash on them.

LEG has suffered lately not solely from a downturn in house turnover but additionally from receding client want to have interaction in these big-ticket discretionary product purchases.

Whereas we don’t have This autumn 2023’s earnings report but as of this writing, LEG did need to decrease steerage for 2023 gross sales and earnings in its Q3 earnings report due to weaker than anticipated gross sales quantity.

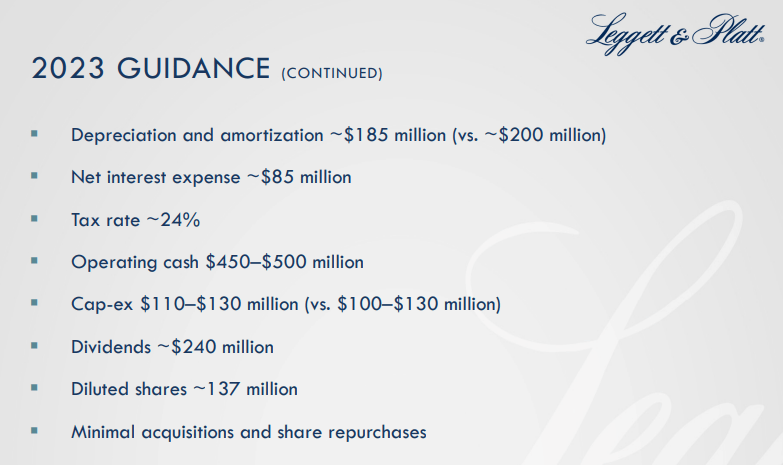

Even so, on the time, LEG nonetheless anticipated to generate free money circulation of $320-390 million, which might be greater than ample to cowl the ~$240 million annual dividend.

LEG November Presentation

Might LEG’s efficiency outlook have eroded much more since then?

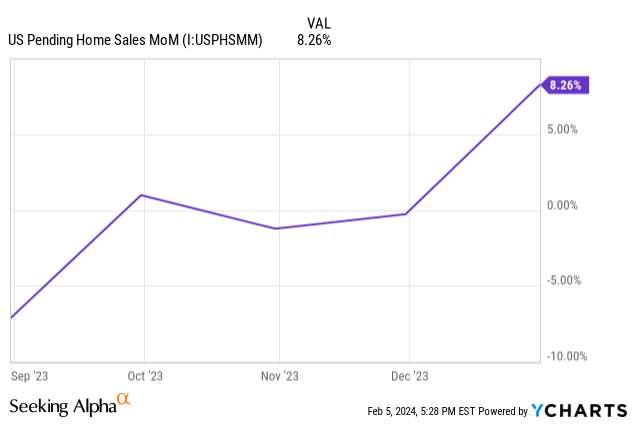

It is attainable, however we doubt it. In spite of everything, as beforehand said, client confidence has ticked up since then, and pending house gross sales have likewise risen during the last 3- and 6-month durations.

If this pattern of extra house gross sales continues into 2024, then LEG must be on the trail to restoration this yr similar to WHR.

Helping on this restoration path is a not too long ago announced “restructuring”/cost-cutting plan that ought to see LEG generate a further $40-50 million annualized by consolidating each its actual property footprint and its workforce.

The analysts’ estimate of income and earnings rebounds for bedding and furnishings corporations like Tempur Sealy (TPX) and Haverty Furnishings (HVT) in 2024 is encouraging, even when preliminary presently.

Are The Dividends Protected?

There’s all the time uncertainty within the markets, however in terms of these two cyclical shares leveraged to the housing market, this yr brings with it an elevated stage of uncertainty. So much depends upon what occurs with the housing market and client confidence.

That mentioned, there are some causes to imagine it’s unlikely that both WHR or LEG will lower their dividends this yr.

First, each have very spectacular dividend data.

Whereas WHR isn’t a dividend aristocrat as a result of it has needed to pause its dividend development for a number of durations of time (together with the previous few years), the corporate has additionally paid uninterrupted, regular or rising dividends yearly for the final 68 years.

On the Q4 conference call, WHR’s administration made clear their intention to pay the identical dividend in 2024 as they did in 2023.

In the meantime, LEG is a dividend king, having raised its dividend during the last 50+ consecutive years. Administration have indicated their intention to protect and lengthen that report.

Second, each corporations have sturdy money technology skills even within the midst of the presently troublesome atmosphere. WHR expects to generate greater than sufficient FCF to cowl its dividend in 2024, and LEG anticipated to take action for 2023 as of the final report.

Third, each corporations have some liquidity offering the pliability wanted to maintain the dividend for 1 / 4 or two if and when FCF would not cowl it utterly.

WHR ended 2024 with $1.6 billion in money, whereas LEG ended Q3 2023 with about $274 million in money together with a $1.2 billion credit score revolver with little drawn on it.

Backside Line

This yr will undoubtedly be a troublesome one for industries that depend on a easily functioning housing market. Uncertainty concerning the efficiency of WHR and LEG is increased than regular in 2024.

That mentioned, the Federal Reserve has nonetheless forecast the chance of slicing charges someday this yr. This could assist push mortgage charges down, which in flip ought to fortify house gross sales quantity. WHR and LEG ought to not directly profit from that.

We’re cautiously optimistic concerning the prospects of each these blue-chip cyclical names. Though we acknowledge the potential of dividend cuts this yr, we expect it’s extra doubtless that we are going to see a restoration this yr for each corporations and that their dividends will stay intact.

For many who wish to personal both or each of those cyclical dividend payers, we expect proper now could also be the most effective time within the cycle to purchase.