SDI Productions

On this 2023 year-end sector assessment, half 1, we take a look at how firms carried out throughout 2023 within the communications providers, client discretionary, client staples, vitality, and monetary providers sectors.

Communication Providers

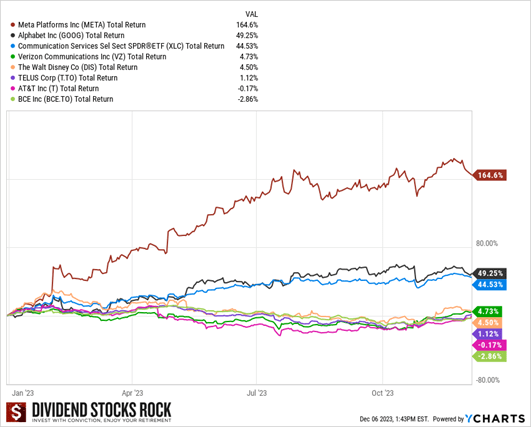

Communication providers normally recall to mind huge telecom firms like AT&T (T), Verizon (VZ), BCE (BCE), or Telus (TU). Nevertheless, this sector has modified, now providing shares from some expertise corporations. The sector is now fueled by firms like Alphabet (GOOG) (GOOGL), Meta (META) and Netflix (NFLX). Communication providers now ship development by way of tech shares and dividends by way of telecoms.

As depicted beneath, telco dividend shares aren’t doing that nicely. Streaming providers went from being darlings to rubbish because the market realized it prices greater than anticipated to provide entertaining content material. After a troublesome yr in 2022, most tech-focused firms got here again robust. Notably, Meta utterly modified the market’s thoughts about its enterprise mannequin. Disney (DIS) simply reinstated a small dividend, however nonetheless struggles to generate revenue from its streaming providers. It’ll be a protracted restoration.

In Canada, we noticed BCE and Telus proceed the downtrend began in 2022. They’re working out of time to show their narrative – that investing massively over a decade to generate increased money circulation is well worth the debt load. For 2024, my eyes can be mounted on their money circulation state of affairs: money from operations, capital expenditure and free money circulation. The aim is to cowl dividend funds with free money circulation, i.e., the money left over after investments in initiatives and community upkeep.

Client Discretionary

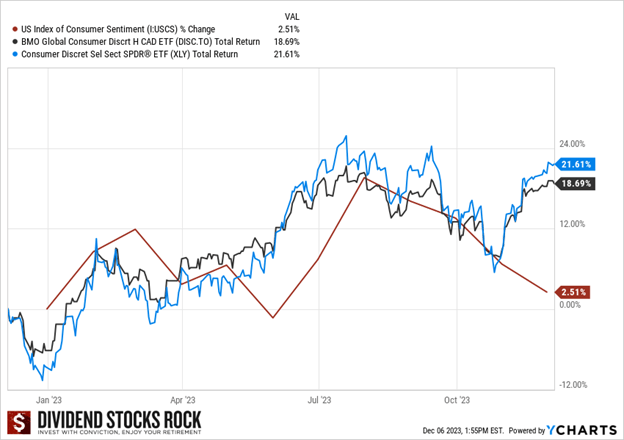

After a nasty yr in 2022, the patron discretionary sector surged in 2023. Surprisingly, the patron confidence index is a bit of increased than final yr. Nevertheless, we see that this confidence is fragile, fluctuating month by month, an indication that the typical client isn’t positive about something. Confidence and client spending can erode rapidly.

Will we see an enormous bump in 2024 if we hear about rate of interest cuts? Presumably. Nonetheless, I’m not satisfied we’ll have an financial delicate touchdown and I proceed to anticipate a recession. Will probably be exhausting to handle inflation and excessive rates of interest for the Joneses.

Once more, the U.S. ETF is dominated by Tesla and Amazon. I’m undecided I might give a lot significance to the sector uptrend at this level. Many retailers advised us customers are tightening their belts and going for important spending method earlier than rewarding themselves with treats.

Excluding these “big tech” firms, most client discretionary shares have underperformed the index in 2023. It’s positively time to pick out your favourite inventory on this sector. Take your time and go for absolute winners, i.e., these with robust dividend triangles and several other development vectors.

Within the latter a part of 2023, we noticed indicators that increased rates of interest are lastly slowing down the economic system. We’ll proceed to really feel their affect for a few years. Unemployment charges stay low, however have a bit going up a bit these days on each side of the border. Add inflation to the combo, which is slowing down however nonetheless including stress, and we may be in for a bumpy trip.

Client Staples

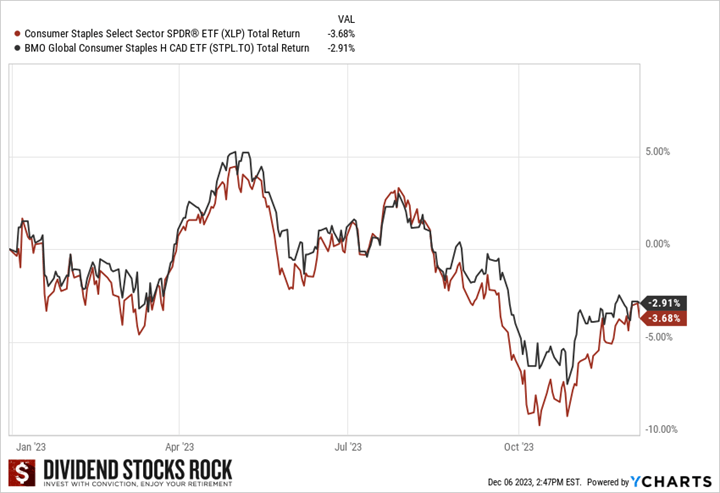

After a comparatively flat yr in 2022, client staples firms did a bit of worse in 2023. Inflation is hurting meals producers, notably meat product producers, on account of their margins contracting. Family & Private merchandise firms like Colgate-Palmolive (CL) and Procter & Gamble (PG) confirmed pricing energy and a few resiliency. Snacks and beverage are underneath stress from weigh loss capsules like Ozempic utilized by customers to scale back their urge for food and anticipated decrease Doritos, Reese’s, and Coca-Cola consumption. Will that drop be everlasting? I doubt it. It’s most likely shopping for alternative, although.

Boring is a dividend development investor’s finest good friend. Within the client staples sector, you may have the possibility to seek out firms that march ahead slowly, however absolutely. Inflation must be much less of a priority for this sector, as customers are keen to pay a better worth for primary items. On the similar time, don’t anticipate to beat the market with these shares. I’d be cautious about excessive yielders on this class. Tobacco shares appear engaging, however their enterprise mannequin isn’t going wherever.

Power

In case you’ve adopted me for some time, I’m not a fan of the vitality sector. My motive is straightforward: vitality firms become profitable when commodity costs are up. They lose cash when costs are down. They haven’t any actual management over costs. This makes them marginal dividend growers.

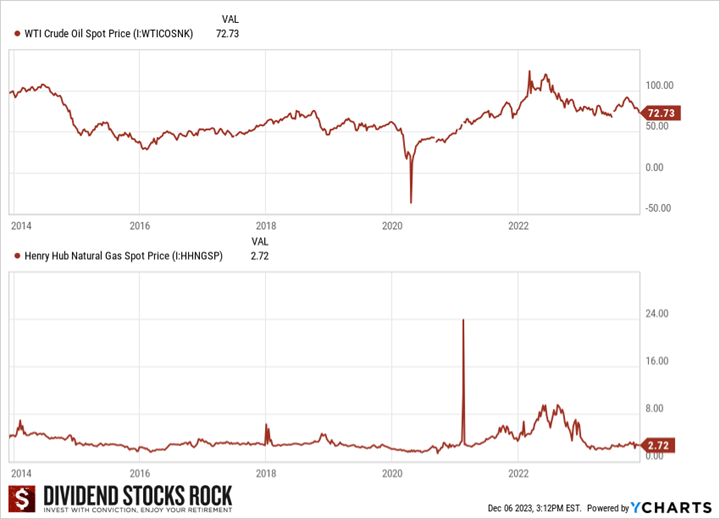

Nevertheless, it’s exhausting to disregard the spectacular bull trip most vitality shares have been on in 2021-22. As you possibly can see with the WTI crude oil spot worth, the rise in worth has been phenomenal.

Many firms reported robust earnings, loads of money circulation, and decrease debt ranges. Does this modification my opinion about this sector? Not likely. I’ve seen this film a number of instances and I understand how it ends. On the time of writing (December 2023), it was again between $70 and $75 per barrel. That’s a steep decline in a short while. The market stays assured as oil shares nonetheless present nice promise.

Will the narrative change if we see the value stabilizing underneath $80? We already noticed some firms get hit by inflation (price of exploration, labor, and so on.). Whereas the vitality sector is a superb protect in opposition to inflation, it additionally has to take care of the elevated prices of their operations.

As for pure gasoline, we noticed an vital improve fueled by the Covid-hype after which by the warfare between Russia and Ukraine. The pure gasoline spot worth is now again to 2019 ranges. Ethical of this story: the world adapts faster than we expect.

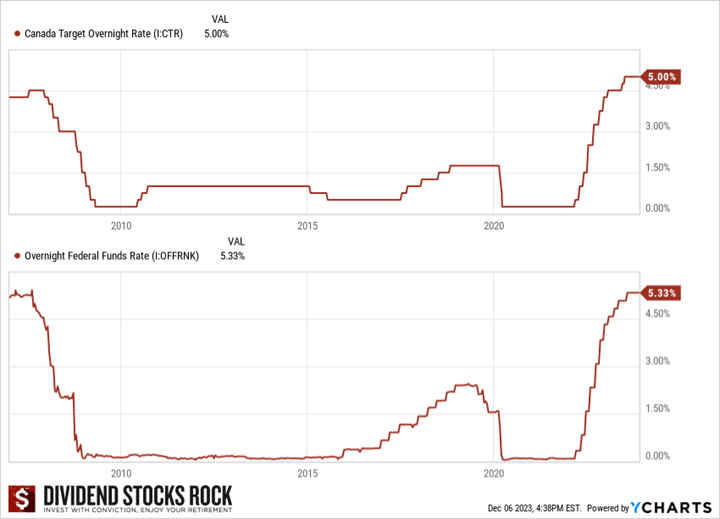

Monetary Providers

I alerted you that 2023 could be a yr of upper and better (and better) rates of interest. The Central Financial institution of Canada and the Fed are in it “for the kill” and the inflation won’t survive (or our economic system will perish). They reasonably amputate an arm to avoid wasting the physique. Happily for us, it appears we’re lastly over the speed hikes.

Not way back, we noticed the primary indicators that the Client Value Index (CPI) was underneath management and that the economic system was cooling off. The market obtained fairly joyful, and all the things grew in November. Don’t suppose we’re finished but. Will central banks attain their unachievable aim of a easy touchdown? It’s clear that price will increase have a lagging impact on all financial metrics. Many owners and indebted firms haven’t renewed their mortgages or most of their debenture but. We haven’t seen the worst of the story but. I anticipate extra ache to return in 2024 as we are going to really feel the total penalties of the quite a few price hikes.

Keep tuned for half 2 of this sector assessment, the place we’ll take a look at the healthcare, industrials, info expertise, supplies, REITs, and utilities sectors. Till then, keep invested!

Editor’s Word: The abstract bullets for this text have been chosen by Looking for Alpha editors.