Panuwat Dangsungnoen/iStock through Getty Photos

Final yr presently, this blog thought that 2023 would be a better year, with a prediction of constructive returns for each shares and bonds.

To be frank with readers, to know that Ed Yardeni and Tom Lee are each optimistic about 2024 inventory and bond returns makes it simple for a long-only advisor to stay optimistic about ahead inventory and bond returns. Additionally, Carson Group’s Ryan Detrick and Sonu Varghese, Carson’s World Strategist, previewed their 2024 outlook final week and anticipated the S&P 500 to return 11-13% subsequent yr.

Right here’s what would make me nervous about 2024 and enhance the chance of unfavourable returns subsequent yr:

1.) The S&P 500 trades as much as its outdated excessive close to 4,795-4,800 and begins to say no materially. When the S&P 500 ran again to its March 2000 excessive in October 2007, it ran via the outdated excessive close to 1,550, traded increased a couple of %, after which began to say no and saved going. The present S&P 500 hasn’t made a brand new excessive in – effectively – will probably be 24 months, subsequent week on January 2nd ’24, so I’d wish to see that outdated excessive at 4,795-4,800 taken out by the top of Q1 ’24. The S&P 500 has made a brand new all-time-high on a complete return foundation, however it wants to interrupt out decisively;

2.) Excessive-yield and company credit score continues to commerce effectively, with high-yield credit score (junk bonds) up 10-11% in 2023 to date. Company unfold widening normally happens in tandem with recessions. In 2022, the HYG or iShares iBoxx $ Excessive Yield Company Bond ETF declined -10.99%. It’s now “round-tripped” the final 24 months, similar to the S&P 500 fairness benchmark. Company defaults appear very well-contained, however company credit score spreads are your “early warning” indicator for a deeper recession.

3.) The “downside trade” within the final 2 years concerned increased rates of interest (i.e. 10-year Treasury yield), a stronger greenback, increased crude oil, all leading to decrease inventory costs within the final 24 months. Watch that sample.

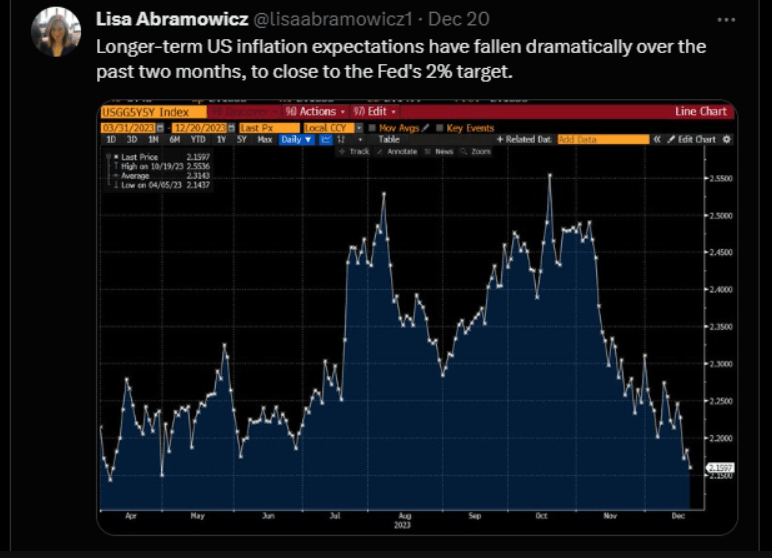

4.) Inflation would reignite and start transferring increased once more, however Friday, December twenty third, 2023’s November PCE knowledge got here in under expectations once more. Right here’s the implication of falling inflation, courtesy of a Bloomberg reporter’s chart:

The fixed “nattering nabobs” which might be mainstream monetary media discuss continually about inflation, however the cash & banking, and economics texts clarify that it’s “inflation expectations” that drive inflation and finally bond costs, though modifications within the precise inflation charge do decide inflation expectations, so I’ve all the time felt that’s considerably of a round argument.

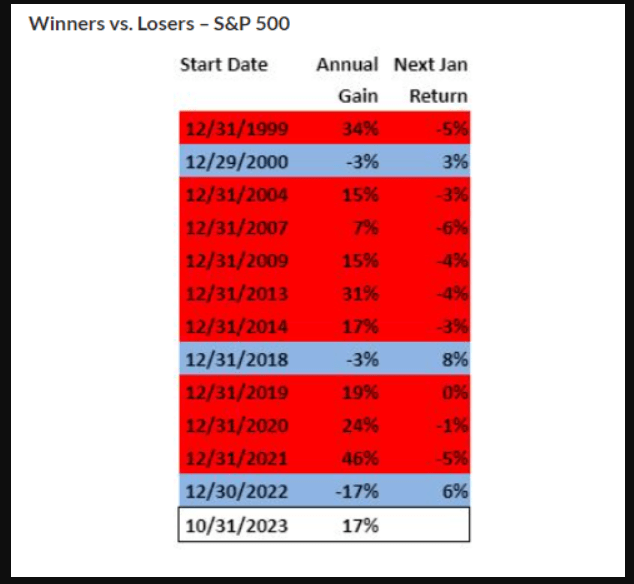

5.) Right here’s an enchanting desk from Lawrence McDonald, the “Bear Traps Report” blogger and the writer of the guide on the Lehman collapse in 2008, “A Colossal Failure of Common Sense.” (Right here’s all the weblog put up from late November ’23: a great read from Lawrence McDonald.)

January ’24 could possibly be fascinating. It is perhaps sufficient to shake out all of this renewed optimistic sentiment that we’ve seen within the inventory market since November ’23.

6.) 2024 may simply see bonds outperform shares, and but each have a superb yr. The final “round-trip” for financial coverage was from late 2016 to late 2018, when Janet Yellen began elevating the Fed funds charge off the ZIRP (zero rate of interest coverage) goal, and Jay Powell virtually received us to three% on Fed funds earlier than the financial knowledge began to sluggish sharply and Powell began to scale back the Fed funds charge. In 2019, Barclay’s Mixture (AGG), or the bond market equal of the S&P 500, returned 8% and alter, whereas the TLT or iShares 20+ 12 months Treasury ETF returned +14% in 2019. Excessive-yield credit score returned 14-15% in 2019.

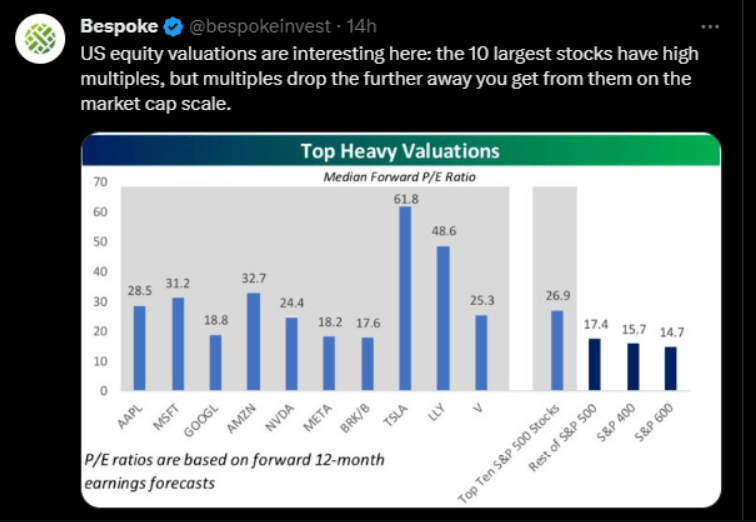

7.) The Magnificent 7 vs. small and mid-caps, rising markets, and worldwide investing: look ahead to rotation from the mega-caps to the small and mid-caps in addition to worldwide investing:

This Bespoke bar chart reveals the assorted P/Es throughout US market capitalizations.

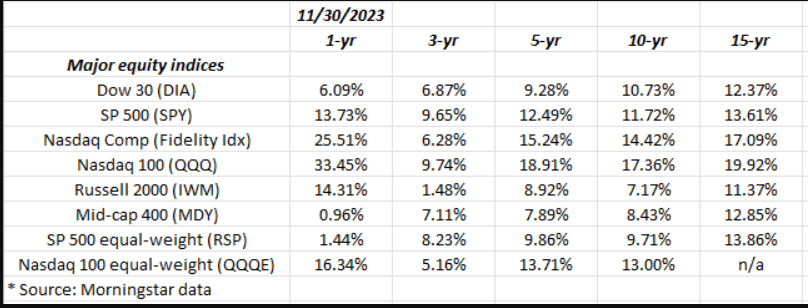

The above desk is the foremost US fairness benchmarks, with annual returns. The small- and mid-caps look affordable from 3-year to 10-year returns, and between the 2 of these, mid-caps truly look just a little higher from a return perspective.

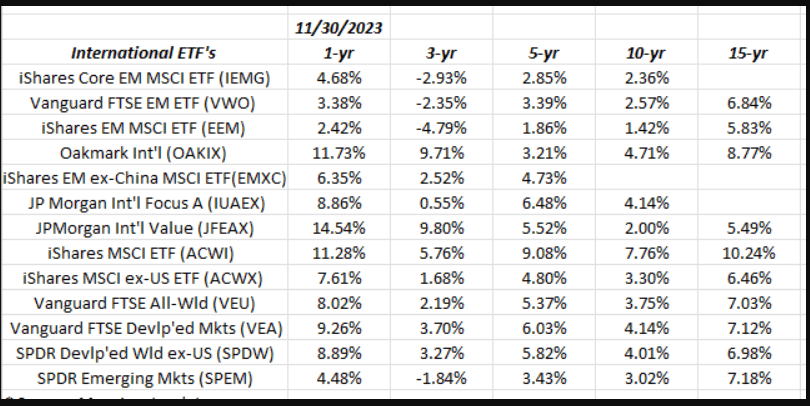

Taking a look at rising market (EM) and worldwide returns, they continue to be common to under common all the time frames. The rising markets peaked in 2007, which (I believe) means the final of the “hot” years for worldwide and EM investing resulted in 2007, so I think these years drop off the 15-year return knowledge, and people 15-year returns will decline after January 1 ’24.

Each portfolio supervisor I discuss to although, says the identical factor: they all the time find yourself having a dialog with the consumer about worldwide and EM publicity within the portfolio, and the truth that it’s usually a drag on portfolio returns. Portfolio managers have to carry worldwide and EM for “uncorrelated” returns.

A Bespoke chart on relative energy: US vs Worldwide benchmarks.

Abstract/conclusion:

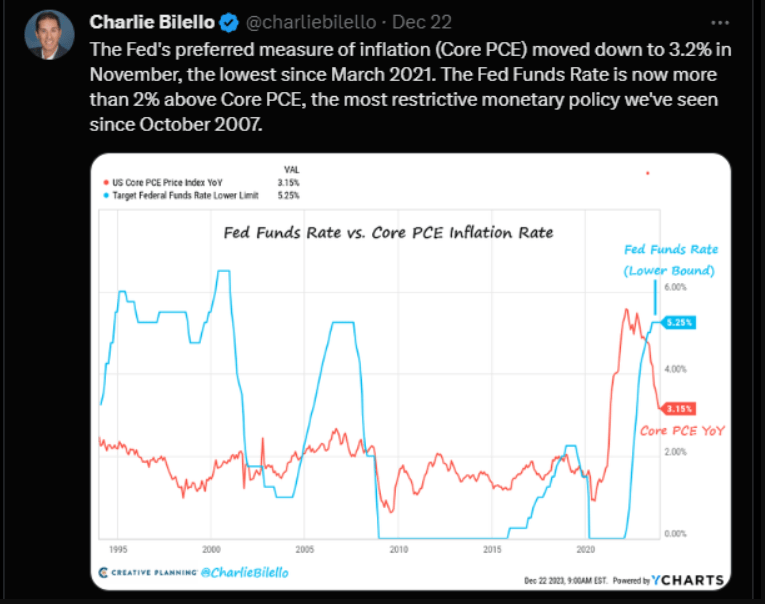

In the end, I do suppose 2024 can be concerning the Fed and Jay Powell, and whether or not the FOMC reduces the Fed funds charge. Proper now, financial coverage may be very restrictive:

This chart reveals the Fed funds charge remaining meaningfully above the Fed funds charge, which implies that – effectively – financial coverage stays very tight, regardless of the FOMC having paused Fed funds charge hikes since July ’23.

Fed liquidity trumps virtually all the things, and if the Fed reduces the Fed funds charge in ’24, it’s going to go an extended technique to making certain constructive returns for each bonds and shares.

Listed below are three latest posts from the final month – here, here, and here – discussing this secular bull market within the S&P 500 and the way a lot time is perhaps left. If the Fed/FOMC cuts charges and shares decline (learn Half III or the third hyperlink above), that normally denotes systemic issues inside the US economic system and it probably means US shares are headed a lot decrease, i.e. in 2001-2002, and 2008.

Readers ought to ignore all predictions, each right here and notably in monetary media. Nobody has a fool-proof system to precisely predict the longer term, even more often than not. Simply take into consideration COVID, the Russian invasion of Ukraine, and October seventh, i.e. three occasions of the final three years which have materially altered the financial and monetary panorama and have or will pressure world economies to regulate to the present atmosphere.

None of it is a prediction, suggestion, or recommendation. Previous efficiency is not any assure of future outcomes. All S&P 500 EPS and income knowledge is sourced largely from IBES knowledge by Refinitiv, however often from FactSet. All spelling errors and errors are 100% my very own. Any prediction that’s correct might be another person’s. Capital markets change rapidly for each the nice and unhealthy. If readers are uncomfortable with their very own portfolio volatility, then modify your portfolio accordingly.

Thanks for studying. Have a wholesome and affluent 2024.

Editor’s Word: The abstract bullets for this text have been chosen by Looking for Alpha editors.