BBuilder

Introduction

Asset costs are a random walk, i.e., the inventory market is unpredictable. I do not know, you do not know, and no one else is aware of the place the market goes subsequent. Nonetheless, guesstimating a 12-month worth goal for the market – through the SPDR® S&P 500 ETF Belief (NYSEARCA:SPY) – is a helpful thought experiment for buyers seeking to arrange a strong portfolio technique for the 12 months forward.

Reviewing Our Market Outlook For 2023

At my investing group, we went into 2023 with an financial thesis of “Inflation collapses along with consumer demand,” which meant defensive positioning throughout all of our core portfolio methods. This is what I wrote in my 2023 outlook be aware for our subscribers:

As you could have observed, I’ve been positioning our core portfolios for 2023 with nice warning. My meant allocation (by the tip of 2023) is 100% fairness, however after this newest re-balancing, we’re at ~45-55% equities, ~30-40% money (short-term treasury payments are making 4.3-4.7%), and ~15% in option-based hedges throughout our core portfolios. The plan is to encash (promote) our tactical hedges within the second half of 2023 (hopefully, at massive good points) to purchase extra shares in our high-conviction inventory concepts (hopefully, at huge reductions).

Fairness Money Hedges TQI’s GARP Portfolio $51.87K (~53.9% of portfolio) $29.2K (~30.3% of portfolio) $15.2K (~15.8% of portfolio) TQI’s Buyback-Dividend Portfolio $52.9K (~53.5% of portfolio) $30.2K (~31% of portfolio) $15.2K (~15.5% of portfolio) TQI’s Moonshot Development Portfolio $43.0K (~44.5% of portfolio) $38.2K (~39.5% of portfolio) $15.2K (~15.8% of portfolio)

With the Fed tightening aggressively right into a deeply inverted yield curve, a richly valued fairness market faces the double whammy of a a number of contraction and an earnings recession in 2023. Whereas we will not predict rates of interest and Fed’s coverage choices, we are able to management our funding portfolios.

This is my outlook for this hostile market:

- An asset’s PE (price-to-earnings) ratio is straight ruled by the risk-free fee out there. So if the Fed strikes risk-free fee to say 5%+ [terminal rate] and holds it there for some time, the market may find yourself demanding an earnings yield of 7-9% from equities (threat premium of 2-3%). Invert that and we get a PE ratio of ~11.11-14.28x.

- Traditionally, bear markets have bottomed with S&P500 (SPX) hitting the ~10-15x PE vary. For 2022, S&P500 EPS is projected to come back in at $225 primarily based on consensus analyst estimates. In a typical recession, EPS tends to go down by 15-20%, and so, 2023 S&P500 EPS may land at $180 to $191.25.

- Assigning a 10-15x PE ratio, we’re taking a look at a possible backside for the continued bear market within the S&P500 to be within the vary of 1,800 to 2,868, which factors to a decline of ~25-50% from present ranges (SPX is at 3,839).

- In late 2023, SPX’s chart flashed a bearish technical crossover (MA-50 falling beneath MA-100 on the weekly chart) that has beforehand preceded ~50% declines in broad market indices in the course of the Nice Monetary Disaster and the Dot Com Bubble bust. If the S&P 500 plunges 35-50% from right here, we get a spread of 1,885 to 2,450.

The elemental and technical views on a possible backside for the S&P 500 are in alignment, and whereas this may increasingly sound scary, it’s definitely a attainable end result of this bear market.

Supply: Should Learn – Unique: Bi-Weekly Portfolio & Market Replace – November 4th, 2022

With the Fed pulling liquidity out of the market and main financial indicators flashing indicators of an impending recession (a view supported by the bond market – an inverted treasury yield curve), we should be defensively positioned. Such an setting is ripe for a monetary accident, and we’ve put tactical option-based hedges in place to protect towards a possible 25-50% decline in fairness markets.

That stated, fairness markets not often have back-to-back destructive return years. Inflation is collapsing, and the Fed could have wriggle room to loosen its financial coverage in 2023. If client demand stays resilient, we might even see an epic rebound within the inventory market. Because of this our positioning is kind of balanced.

We personal high-beta names throughout our core portfolios, and I imagine that even a 50% fairness publicity needs to be sufficient to generate our goal returns. On the flip aspect, we’ve tons of money and tactical hedges to defend our portfolios towards a continuation of the continued bear market.

With our balanced positioning, I really feel assured that we’re well-positioned to take care of regardless of the market throws at us over the following few quarters.

Supply: Bi-Weekly Portfolio & Market Replace – December thirtieth, 2022.

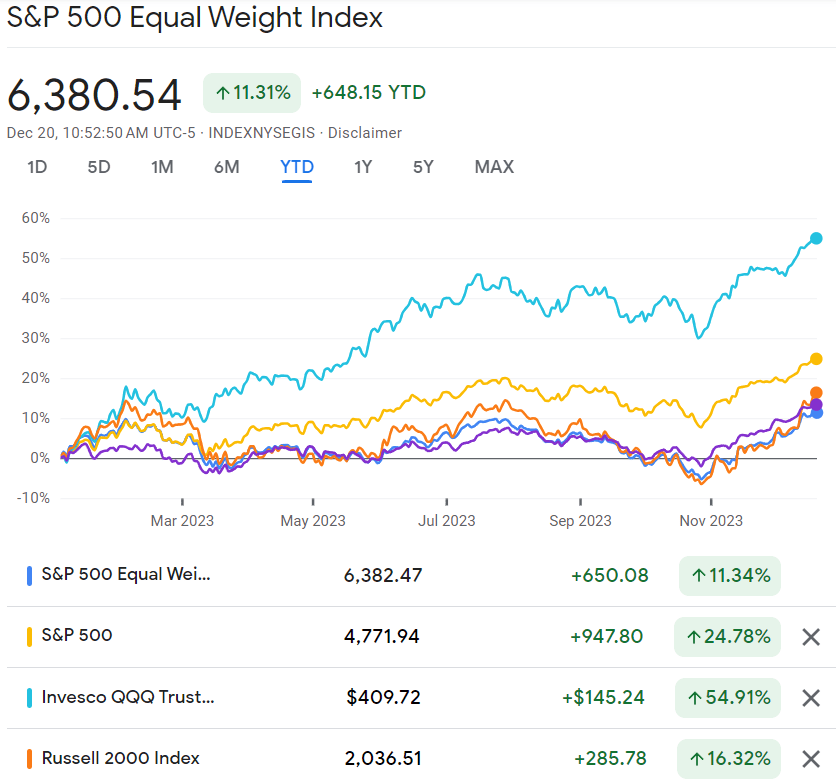

With inflation moderating quickly and client spending (labor market) holding up all through 2023, fairness markets have skilled an epic rebound this 12 months, with the S&P 500 (SP500) up almost 25% YTD on twentieth December. Whereas giant/mega-cap tech firms have led the cost larger (powered by a pink sizzling gen AI theme), the fairness rally has been broadening out in latest weeks, with the equal-weighted S&P 500 (RSP) up a good 11% YTD.

Google Finance

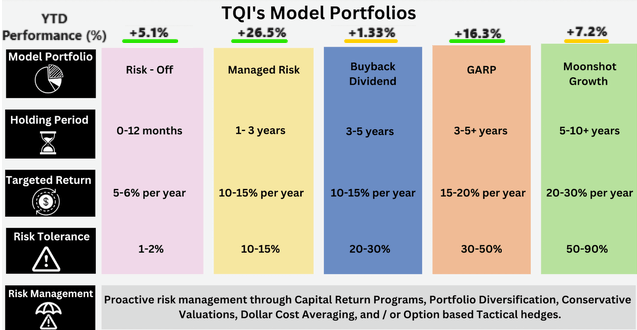

At TQI, not dropping cash is our #1 precedence. And, regardless of being unsuitable in regards to the overarching macroeconomic thesis [“inflation will collapse along with consumer demand” has failed to play out (so far)], all of our managed portfolio methods are within the inexperienced for 2023:

The Quantamental Investor

Whereas relative underperformance to broad market indices such because the S&P 500 is definitely disappointing, I’m glad with the YTD end result of our core portfolio methods given how the 12 months has unfolded to date.

Now, self-introspection is a vital a part of investing, and I at all times like to check my thesis towards real-world outcomes.

So, what went unsuitable for us in 2023?

As we foresaw, inflation collapsed (first a part of our financial thesis) in 2023; nonetheless, client demand held up sturdy amid a persistently tight labor market (unemployment fee <4%). Along with the labor market (considerable jobs and wholesome wage progress), extra financial savings from the pandemic and super quantities of fiscal deficit spending ($2T per 12 months) have enabled client spending (and the labor market) to stay resilient on this cycle.

A recession (exhausting touchdown) didn’t materialize this 12 months, which allowed S&P 500 earnings to carry up. And, given the dearth of financial weak spot [plus lots of AI hopium], buying and selling multiples for the S&P 500 have expanded considerably (with AI shares getting probably the most love from buyers).

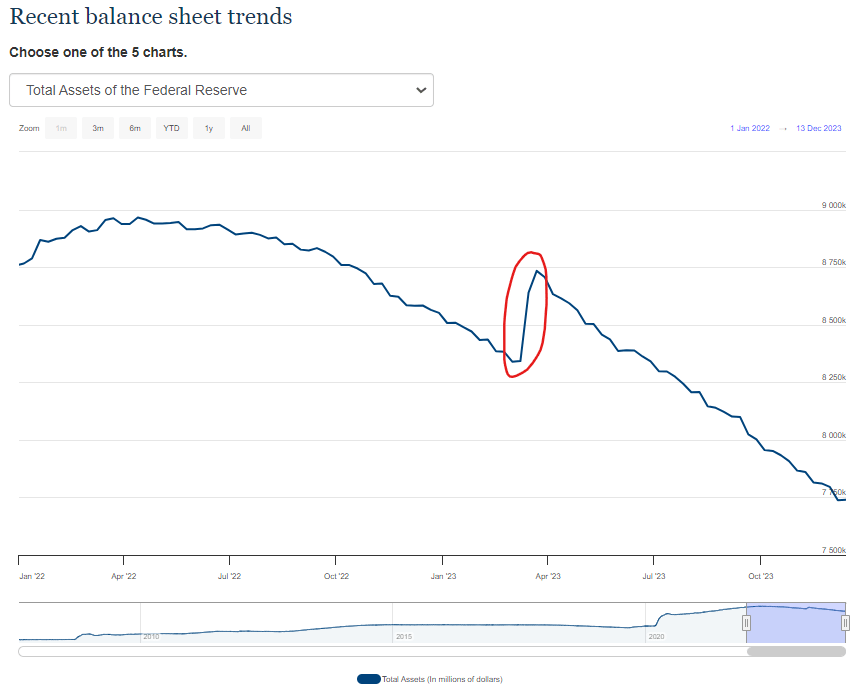

The one massive shock that I did not see occurring this 12 months was Fed’s backdoor QE [quantitative easing]. On the again of a number of financial institution failures (monetary accidents) in March 2023, the Fed shortly pumped $400B of further liquidity into the system (backdoor QE) to avert a banking disaster.

Federal Reserve

For my part, market individuals considered this depositor bailout (for poorly run banks like Silicon Valley Financial institution and First Republic Financial institution) as an indication of the “Fed Put” being lively. That is most likely an enormous a part of Mr. Market’s willingness to pay a a lot larger a number of for S&P 500 earnings.

Please be aware: S&P 500 earnings are anticipated to shut flat(ish) y/y for 2023. Therefore, the complete YTD inventory market rally relies on buying and selling a number of growth [with S&P 500 forward P/E rising from ~16x to ~20x in 2023] and never basic earnings progress.

Now, I’ll share my market outlook for 2024, after which current a year-end worth goal for the S&P 500.

TQI’s Market Outlook for 2024

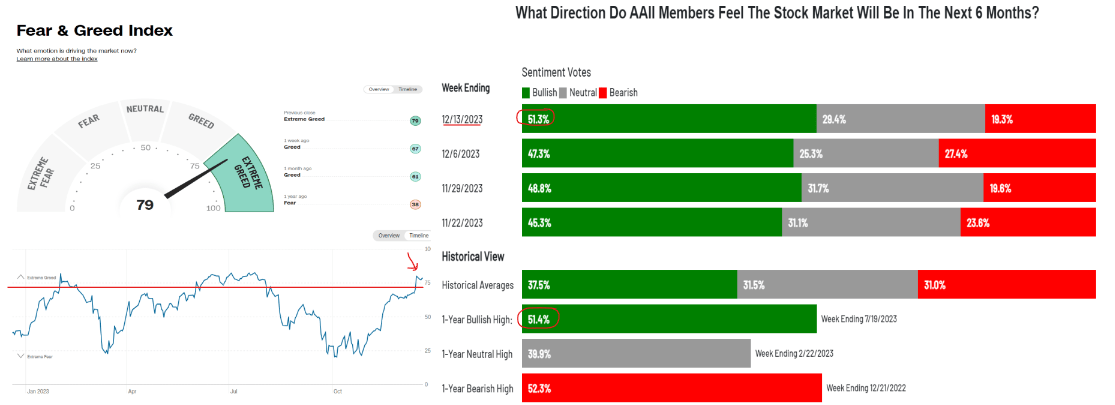

Primarily based on latest “Goldilocks” financial knowledge (quickly moderating inflation charges, ultra-low unemployment charges <4%, resilient client spending progress) and inventory market rally, the “soft” touchdown narrative has develop into the consensus view within the investing world. Heading into 2024, broad U.S. fairness indices have hit or are near hitting new all-time highs (not inflation-adjusted), and bullish investor sentiment is thru the roof proper now:

Creator, CNN, AAII

With everybody on one aspect of the boat, I believe the market can spring a shock within the different route, which is basically what occurred this 12 months. Going into 2023, investor sentiment was extraordinarily bearish, and we all know how issues turned out (S&P 500 is up 25% YTD).

Whereas our financial thesis “inflation will collapse along with consumer demand” failed miserably in 2023 (as a result of causes I shared within the earlier part), I imagine the lag results of Fed’s aggressive financial coverage tightening actions (federal funds fee hiked from 0% to five.25-5.5% over the past 18 months and ongoing QT [quantitative tightening] of $95B monthly) are set to adversely influence the financial system (and company earnings) within the subsequent 6-12 months.

Sure, the Fed lately guided for 3 fee cuts (financial coverage easing) in 2024 within the latest dot plot, which is being celebrated as a “pivot” within the fairness markets. Nonetheless, with inflation nonetheless operating forward of Fed’s goal fee of two%, the cuts are unlikely to come back till the second half of subsequent 12 months. And by then, I believe the financial injury would have already been inflicted. The Fed is at all times late, and will probably be late once more!

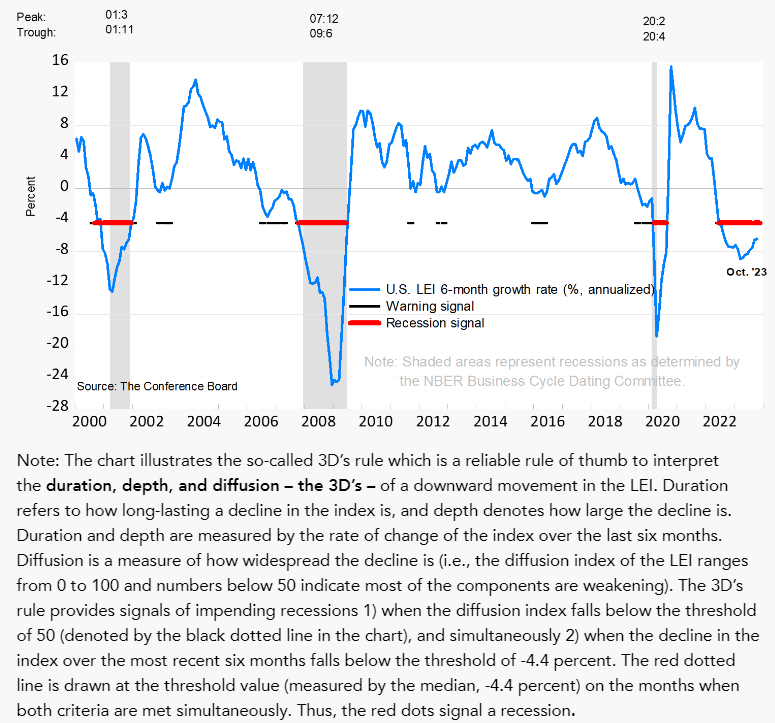

Main financial indicators have are available destructive consecutively for the previous 19 months, and proceed to level towards an imminent recession:

Convention Board

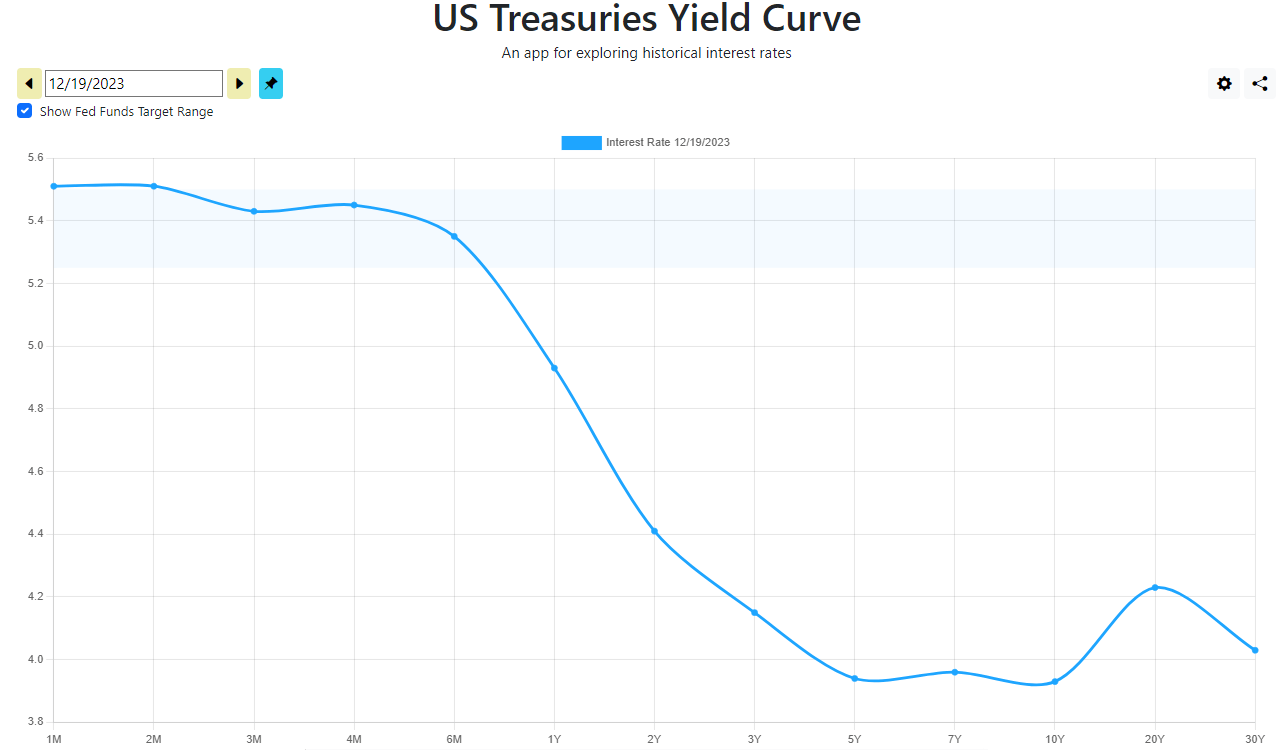

Moreover, the bond market is pricing in 6 fee cuts for 2024 (front-running the Fed by a good distance) and screaming “recession ahead” through a deeply inverted yield curve:

Treasury Yield Curve

As you might know, the 10-year treasury yield (US10Y) has dropped precipitously from its cycle excessive of ~5.2% on twenty ninth October 2023 to ~3.9% as of at this time (twentieth December 2023). Whereas equities have celebrated this fast drop in long-duration treasury yields (by rallying up greater than 15% from October 2023 lows), the bond market may very well be pricing in recession or deflation threat through this aggressive re-pricing. Solely time will inform if the bond market is correct or unsuitable, however I believe it’s truthful to say that bonds and shares are at odds with one another as soon as once more.

For 2024, I view deflation as a a lot larger threat to the financial system in comparison with inflation. Whereas the Fed has guided 3 fee cuts for 2024, the continued quantitative tightening (stability sheet discount) is prone to adversely influence liquidity within the monetary system at a time when –

- The buyer is operating out of extra financial savings

- Family money owed are reaching new highs

- Shopper mortgage delinquencies are rising quickly

- Company bankruptcies are spiking.

For my part, the U.S. financial system is about for a big slowdown subsequent 12 months. The Fed is projecting 1.4% GDP progress for 2024, however I stay very skeptical in regards to the concept of a “soft” touchdown. Historical past exhibits that each exhausting touchdown appeared like a delicate touchdown till it did not! For 2024, my base case prediction is that we are going to see some type of recession, which can ultimately be the set off for financial coverage easing.

My Magic Quantity For S&P 500 Is 4,000

With the Fed nonetheless tightening financial coverage right into a deeply inverted yield curve, an much more richly valued fairness market is going through the double whammy of a a number of contraction and an earnings recession in 2024.

This is my outlook for the S&P 500 in 2024:

- An asset’s P/E (price-to-earnings) ratio is straight ruled by the risk-free fee out there. Given the huge quantity of treasury provide about to hit the markets, I can see long-duration treasury yields staying elevated for some time (even when we see a recession subsequent 12 months). Assuming the 10-year treasury yield stays within the 4-5% vary in 2024, I anticipate market individuals to demand an earnings yield of 6-8% from the S&P 500. Invert that earnings yield and we get a P/E ratio of ~12.5-16.7x. With the Fed expressing a willingness to ease financial coverage (earlier than inflation reaches the goal fee of two%), I imagine the S&P 500 can commerce nearer to the upper finish of that P/E vary. To formulate my 2024 worth goal for the S&P 500, I’m assuming an exit buying and selling a number of of ~16x P/E (which additionally occurs to be the long-term imply P/E ratio for S&P 500).

- As of at this time, S&P 500 EPS is presently projected to rise by 12% to $250 in 2024 in accordance with consensus analyst estimates. In a backyard selection recession, EPS tends to go down by 15-20%, however even when we see solely a light recession, S&P 500 earnings are prone to disappoint bullish buyers. In our view, S&P 500 earnings progress for the following couple of years will probably be within the mid-single-digit vary, and we’ll hit $250 in S&P earnings solely in 2025.

- Assigning a ahead P/E of ~16x to 2025 S&P 500 EPS of $250, we attain an end-of-year goal of 4,000 for the S&P 500 index ($400 for the SPY ETF). This goal implies a draw back of -15% from present ranges.

Concluding Ideas

The immutable legal guidelines of cash dictate that threat property equivalent to equities provide a optimistic threat premium relative to the risk-free fee out there. Regardless of the lengthy finish of the treasury yield curve shifting all the way down to ~4% in latest weeks, the S&P 500 earnings yield nonetheless must rise to the 6-8% vary for fairness markets to develop into engaging as soon as once more.

Given the present state of the financial system (Goldilocks), long-duration treasury yields ought to stabilize right here and probably transfer larger in Q1 2024. Nonetheless, if yields proceed to break down additional, the bond market would then be signaling an financial recession.

At ~20x ahead P/E, the S&P 500 is priced for a “soft” or “no” touchdown state of affairs, and I stay skeptical in regards to the “soft” touchdown narrative given a deeply inverted yield curve and destructive main financial indicators proceed to level towards a tough touchdown within the financial system.

As we famous in our article, “SPY: You Have Been Warned By Jerome Powell,” there are uncanny similarities between 1987 and 2023. Will we see a 1987-esque crash? Frankly, I do not know, however below the given set of financial and monetary situations, I merely can not rule out a inventory market crash.

Winston Churchill as soon as stated:

Those who fail to study from historical past are doomed to repeat it.

Heading into a possible recession, the fairness market (S&P 500) valuation displays a excessive diploma of investor complacency. A inventory market crash could or could not materialize in 2024; nonetheless, prudent buyers should put together themselves for a variety of attainable outcomes [tail events] on this unsure setting.

Key Takeaway: Contemplating the easy yield math behind inventory valuations, the S&P 500 is ripe for a big correction. We see the S&P 500 index declining to 4,000 by the tip of 2024. Henceforth, I fee the SPY S&P 500 ETF a “Sell” at $475.

Editor’s Observe: This text was submitted as a part of Searching for Alpha’s 2024 Market Prediction competition, which runs by means of December 20. With money prizes, this competitors — open to all contributors — is one you do not need to miss. If you’re eager about turning into a contributor and collaborating within the competitors, click here to seek out out extra and submit your article at this time!