Torsten Asmus

A dip within the roaring market is coming.

When the market is at all-time highs and rising day by day, it is easy to get caught up within the frenzy. However persistence can result in greater returns later. There will likely be a pullback; the solely query is when.

Why is the inventory market booming?

Many shares have gone parabolic in 2024, eclipsing 2021 highs and pushing valuation metrics out of the norm. There are lots of causes, and I will spotlight two.

First, the economic system is in higher form than many thought. The recession we had been promised has but to materialize. I believed we might see a softening in client spending by now, however there may be little signal of that. Nonetheless, I by no means purchased the narrative that we might see as much as six fee cuts this yr.

It is modern to criticize the Federal Reserve and Jerome Powell; nevertheless, it has set itself up properly. The economic system is rising even with charges above 5%. Every proportion level is an arrow within the Fed’s quiver if the economic system slows. Do not count on it to offer them up simply.

Persons are additionally returning to the workforce, easing the labor scarcity and inflation. I lately spoke to a “small” ($70 million income) enterprise affiliate who operates in an trade vital to the economic system. The enterprise had 140 candidates for a latest job posting. Popping out of the pandemic, there would usually be only one or two (and typically zero).

Might the dearth of fee cuts be the catalyst for a wholesome pullback?

The second is synthetic intelligence (AI). Make no mistake; the know-how is transformative. However, it’s pushing the boundaries of many inventory valuations, and there’s a lot of hype. A pullback may very well be so as.

Having a “market dip” want record is sensible. Listed here are a number of on mine.

CrowdStrike

Firms can lower many bills in periods of financial uncertainty, like advertising, analysis, and worker prices. However cybersecurity is a vital want that may be silly to trim. That is the argument I used throughout the canine days of 2022 and restoration in 2023 when shopping for CrowdStrike (CRWD) and Palo Alto (PANW). Each shares have outperformed.

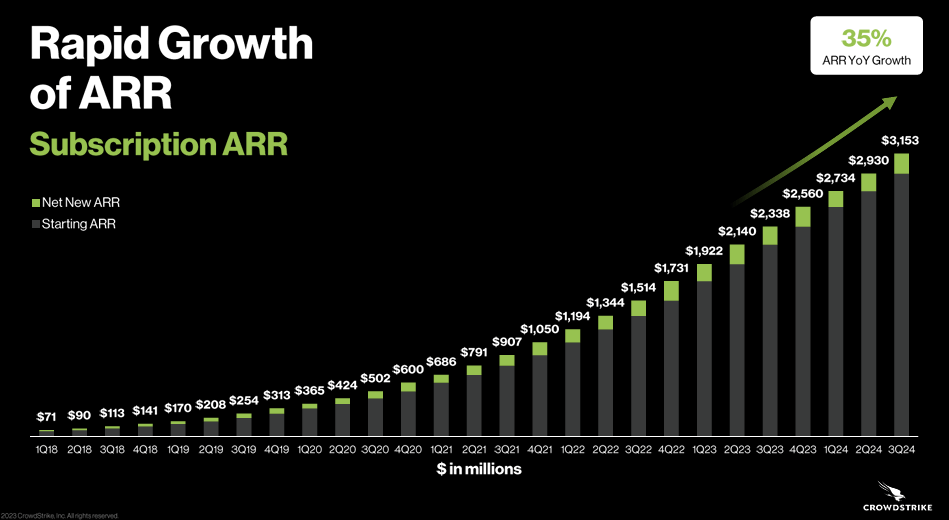

CrowdStrike led the cost of complete, cloud-based, modular safety to $3.2 billion annual recurring income (ARR) final quarter, as proven beneath.

Supply; CrowdStrike

The corporate improved its working leverage, and free money circulation is booming to the tune of $655 million via Q3 fiscal 2024.

I’ve lengthy been on the CrowdStrike bandwagon, together with this article the place I “doubled down” at $130 per share on this article. The inventory rocketed 150% since and trades at a hefty 28 occasions gross sales – too wealthy for me. Maintain look ahead to a strong pullback.

Arm Holdings

There’s a motive Nvidia (NVDA) (one of many smartest corporations on the planet) tried to purchase Arm Holdings (ARM) in 2020. Arm is deeply embedded within the semiconductor market. You probably use its design day by day, as 99% of smartphones include it.

Right here is a crucial distinction: Arm would not produce chips; Arm creates the structure and licenses it to the highest chip producers. It then receives royalties for every chip that goes out the door. Thus far, 280 billion have shipped. You’ll have heard of a few of its prospects, Apple (AAPL), Alphabet (GOOG)(GOOGL), Amazon (AMZN), Microsoft (MSFT), and Taiwan Semiconductor Manufacturing (TSM). The market is booming.

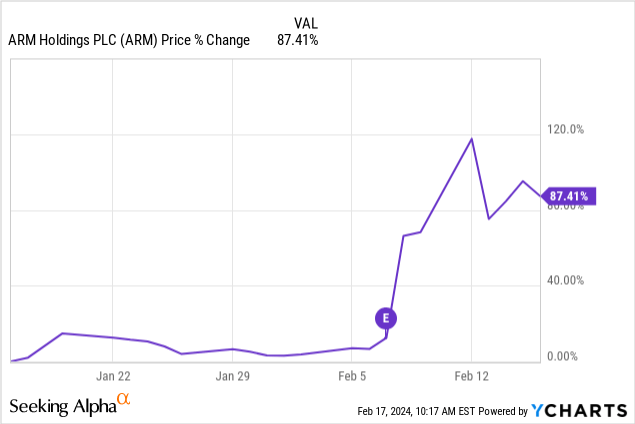

Arm’s Q3 fiscal 2024 outcomes noticed income rise 14% to $824 million – however that wasn’t the story that induced this unimaginable bounce within the inventory.

The corporate reported elevated adoption of its newest structure, “Arm v9”, which produces double the royalties of the earlier model. Arm’s remaining efficiency obligation jumped 38% yr over yr (YOY) from $1.75 billion to $2.4 billion.

Arm has a terrific enterprise mannequin. It would not produce chips; capital expenditures are low, so free money circulation is considerable. It reported a 30% margin final quarter.

A $130 billion market cap for an organization with $3 billion trailing twelve-month gross sales is extraordinarily pricy. The inventory will doubtless retrace a lot of its latest explosion because the preliminary pleasure wanes, and this will likely be a chance for long-term buyers.

Palantir

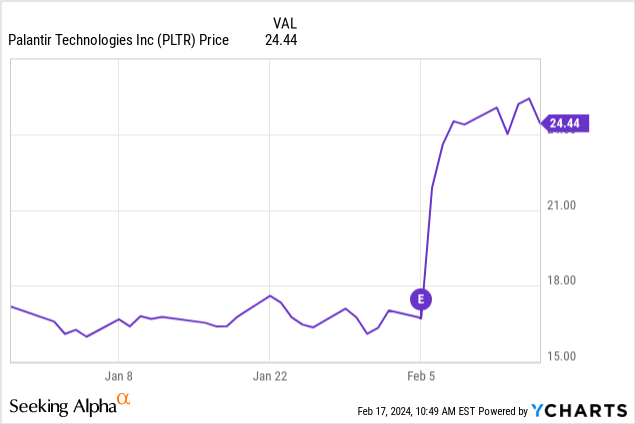

I’ve made cash on Palantir Applied sciences (PLTR) inventory with out proudly owning a single share. When the inventory crashed beneath $8 per share in 2022, I purchased long-dated $10 name choices, which I’ve since closed. Additionally, by promoting put choices going into the newest earnings name and shutting them on the transfer depicted beneath.

Palantir seems to be like a wonderful long-term play if it retraces a few of this bounce.

Lengthy entrenched within the protection trade, Palantir sought to increase its market by rising its business enterprise, and it is bearing fruit. U.S. business gross sales rose 70% YOY final quarter to $131 million, and the U.S. business buyer depend elevated 55% to 221.

Whole gross sales for the quarter rose 20% to $608 million, and Palantir was GAAP worthwhile for the fourth straight quarter.

The discharge of Palantir AIP (Synthetic Intelligence Platform) comes as many corporations look to leverage generative AI for higher decision-making and effectivity. Palantir will likely be a wonderful companion, and this can drive additional inroads into the non-public sector.

Warren Buffett mentioned:

Most individuals get taken with shares when everybody else is. The time to get is when nobody else is.

Sage recommendation. There are lots of unimaginable corporations doing wonderful issues now, however valuations nonetheless matter, and persistence is rewarded in the long term.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.