iantfoto

3M Firm (NYSE:MMM) has carried out in accordance with my expectations since my previous update (Maintain/Market Carry out score) in early October. I up to date 3M traders that the MMM is in a long-term downtrend. Consequently, it might transform a worth entice if shopping for sentiments do not recommend a sturdy backside, underpinning the market’s confidence in its reversal. Nonetheless, MMM’s current developments recommend that it might lastly change.

Accordingly, MMM barely carried out consistent with the S&P 500 (SPX) (SPY) in price-performance phrases (7.8%) since then, however barely outperformed when contemplating whole returns (9.5%).

Consequently, 3M traders might ask whether or not the worst is lastly over, as MMM additionally outperformed its industrial sectors (XLI) friends since early October. I urged holders to not catch the falling knife in MMM, assessing it as a debilitating worth entice. Nonetheless, that does not imply MMM can not stage spurts of short-term outperformance, because the market does not transfer in a straight line. Given its well-oversold standing in early October, it explains why I did not assign MMM a Promote score.

The vital query dealing with traders is whether or not they have the conviction to catch MMM’s falling knife if they’ve loads of alternatives out there. They will even contemplate shopping for SPY if they don’t seem to be certain about coping with 3M’s important authorized uncertainties hitting its GAAP earnings transferring forward. Nonetheless, MMM bulls might additionally justify their thesis, indicating that the market appears ahead and never backward, arguing that such challenges have seemingly been priced in.

The corporate’s third-quarter or FQ3 earnings release means that 3M’s authorized woes might have reached a nadir (a minimum of within the close to time period). 3M reported an adjusted EPS of $2.68, however a GAAP EPS of -$3.74. It is a marked enchancment from Q2’s GAAP EPS of -$12.35 as the corporate makes an attempt to raise itself from the malaise engendered by its authorized liabilities.

3M has reached its PWS settlement, which is anticipated to be inside $10.5B to $12.5B, unfold over 13 years. Nonetheless, we nonetheless must assess the result of the final hearing, which is not anticipated till February 2024. As well as, the corporate just lately acquired a pivotal ruling from the US Court docket of Appeals for the Sixth Circuit over a category motion lawsuit, which lifted MMM’s shopping for sentiments. Accordingly, the choice concerned the “rejection of a lower court’s ruling that would have allowed nearly 12 million Ohio residents to sue these companies collectively in a class action lawsuit.” Consequently, I gleaned that the optimistic response is a step in the precise course for 3M because it makes an attempt to regain momentum in its core enterprise to get better its valuation.

3M is ready to spin off its healthcare enterprise in 2024 because it appears to unlock worth, given the malaise seen in MMM, because it recovers from a 2012 low. Furthermore, with the global economy not anticipated to fall into a tough touchdown, it ought to present additional impetus to spur 3M’s restoration, at the same time as its China enterprise might proceed to affect its near-term efficiency.

Regardless of that, traders are seemingly targeted on whether or not its GAAP earnings might take a development inflection transferring forward, which might raise it from its materials undervaluation. 3M additionally raised its 2023 adjusted EPS steering vary to between $8.95 and $9.15, underpinning the corporate’s confidence in its underlying enterprise restoration.

There’s little doubt that MMM is materially undervalued. With a ahead EBITDA a number of of seven.6x, it is nicely beneath its 10Y common of 12x. As well as, MMM has a “B” dividend security grade assigned by Looking for Alpha Quant, corroborating the robustness of its ahead dividend yield of 6.1%. With the Fed anticipated to have reached the top of its mountain climbing regime, earnings traders in search of extra engaging yields might return to MMM if they do not anticipate an imminent risk to its dividend safety.

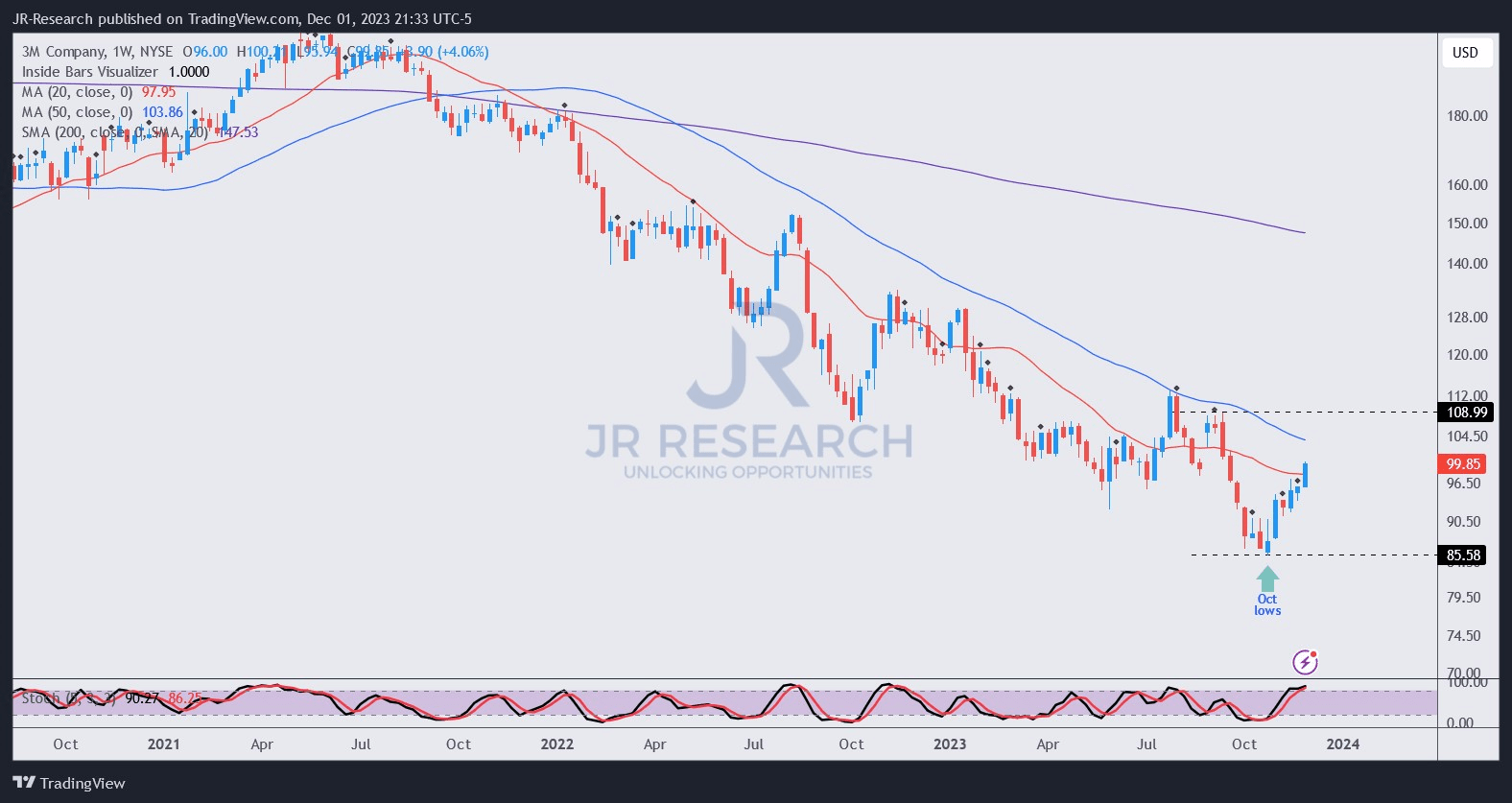

MMM value chart (weekly) (TradingView)

I gleaned that MMM seemingly staged a capitulation low in October 2023 ($86 stage), forming a bear entice in early November. In different phrases, dip consumers have returned with conviction, trying to assist MMM backside out, anticipating the worst of its authorized woes may very well be over.

Analysts’ estimates are in line, as 3M’s GAAP EPS is anticipated to inflect again into optimistic territory via 2024, corroborating the energy of MMM’s backside.

As well as, in price-action parlance, it is also a double-bottom bear entice (see price action glossary), suggesting peak pessimism. I now anticipate MMM’s $115 stage to be retaken decisively, because it stays materially undervalued.

Consequently, I consider it is well timed for me to show extra constructive on MMM, because the worst is probably going over (Buyers cannot look ahead to the information to inform them it is over; by then, it is likely to be so much increased).

Ranking: Upgraded to Purchase.

Vital be aware: Buyers are reminded to do their due diligence and never depend on the data offered as monetary recommendation. Please all the time apply unbiased considering and be aware that the score will not be supposed to time a particular entry/exit on the level of writing until in any other case specified.

We Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a vital hole in our view? Noticed one thing essential that we didn’t? Agree or disagree? Remark beneath with the goal of serving to everybody in the neighborhood to be taught higher!