Nastassia Samal/iStock by way of Getty Pictures

The inventory market is the story of cycles and of the human conduct that’s liable for overreactions in each instructions.

– Seth Klarman, billionaire investor and writer

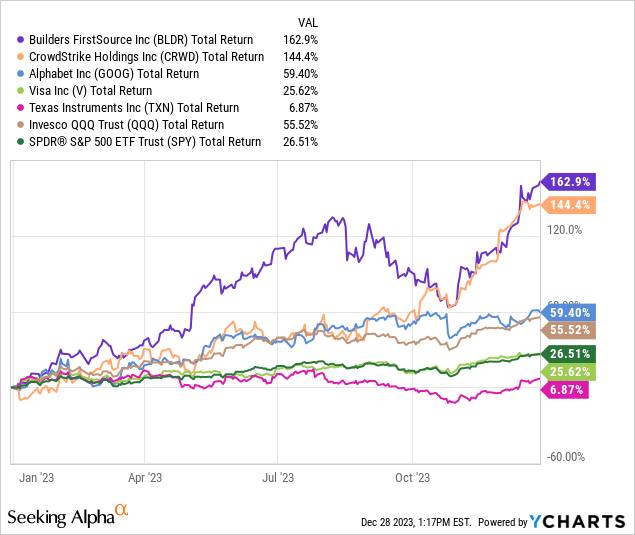

2023 was a terrific yr for traders after a tough 2022. Whereas many traders have been working for the hills, there have been large values to be discovered. My high picks final yr produced a mean complete return of 78%, beating the Nasdaq (QQQ) and S&P 500 (SPY), due to large positive aspects by Builders FirstSource (BLDR) and CrowdStrike (CRWD), whereas Texas Devices (TXN) struggled.

To have a look again, you possibly can take a look at the unique article and the yr in evaluate here and here.

Seeking to 2024

First, let’s acknowledge that we do not make investments year-to-year and that the enterprise cycle does not adhere to the Gregorian Calendar. The Earth’s place across the solar does not have an effect on Nvidia’s (NVDA) gross sales cycle, client debt, or rates of interest.

Nevertheless, a brand new yr is a wonderful time to step again and take inventory (pardon the pun) of our investments and technique; plus, it is an incredible dialog starter.

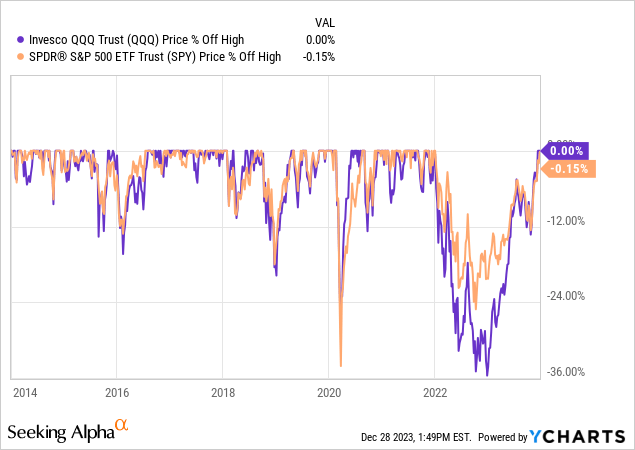

However this is the rub. The inventory market’s latest livid rally has stretched valuations. Buyers are enamored with potential price cuts in 2024, and the Concern and Greed Index reveals extreme greed. Now isn’t one of the best time to purchase many shares, with markets at all-time highs, as proven beneath.

The market can all the time proceed its rally; nobody is aware of what is going to occur sooner or later. Actually not me. Investing is partly about possibilities. We wish to make investments extra when the chances are in our favor (like at first of 2023 with the market method down) and fewer when the chances are the opposite method, as they’re now at report highs.

There’ll probably be a wholesome pullback sooner relatively than later.

Because of this, I’m placing buy value targets on a few of this yr’s picks. Nothing excessive. Typically, these are costs that the inventory has traded for prior to now 30 days.

Let’s go forward and get to it.

Reserving Holdings

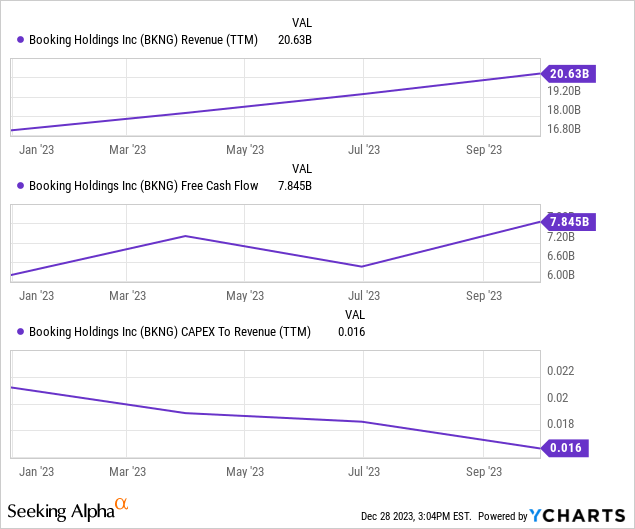

Reserving Holdings (BKNG) is worthwhile and extremely capital-light, resulting in large free money stream (FCF). It’s ramping up its share buyback program, and the longer term is vivid.

Reserving runs main journey websites, together with Reserving.com, Priceline, KAYAK, and OpenTable. It additionally competes with Airbnb (ABNB) for short-term leases (which Reserving calls “alternative accommodations”), though Reserving focuses on leases offered by skilled administration corporations relatively than people. This implies Reserving avoids among the complications that Airbnb offers with however has a smaller potential addressable market. This section accounted for 33% of complete room nights final quarter on 24% year-over-year (YOY) development.

The corporate is targeted on growing its presence in airline ticket bookings (up 57% YOY final quarter) and turning into an end-to-end journey companion. Each shall be profitable.

Why I just like the inventory

Reserving’s enterprise makes use of little or no CapEx, which suggests tons of free money stream. The FCF margin over the trailing twelve months (TTMs) is 38%, as depicted beneath.

Which means that 38 cents of every greenback earned falls proper into the corporate’s pocket, enabling Reserving to go on a share buyback bonanza that ought to proceed. Listed here are the numbers:

- $6.6 billion repurchased in 2022;

- $7.9 billion repurchased by Q3 2023;

- 13% discount in diluted shares excellent since January 2022;

- $16 billion remaining on the present authorization; and

- This system is dynamic.

Administration expresses that they take note of the share value when making purchases.

Administration stated they anticipated This autumn purchases to outpace Q3 purchases due to the share value on the November 2nd convention name. The value was $2,839 that day and has rocketed to over $3,550. Which means that buybacks have most likely slowed, and traders could be affected person and await a pullback.

Reserving has $11.9 billion long-term debt on the stability sheet; nevertheless, $7.5 billion comes due in 2028 and past and $4.9 billion after 2030. The charges are favorable, so it doesn’t concern me.

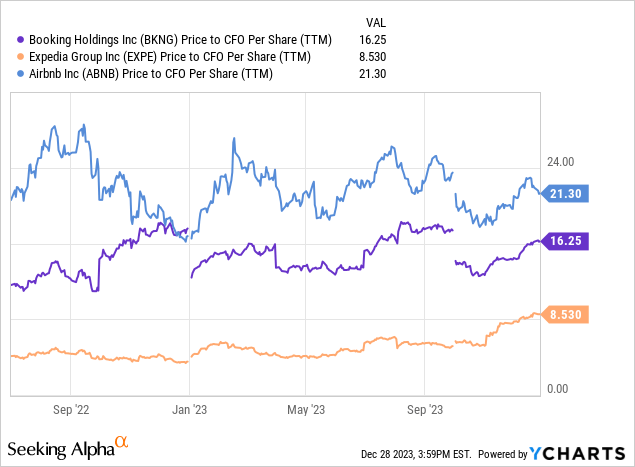

The inventory trades at a price-to-operating money stream (CFO) per share of 16, which is larger than Expedia (EXPE) and decrease than Airbnb, as proven beneath.

This valuation is decrease than the 18 it traded for in January 2020, simply earlier than the pandemic upended metrics.

Nonetheless, there are macro considerations. Shopper spending continues to be rising, however so is client debt. The latest price hikes have not had an opportunity to work totally by the financial system, pupil mortgage funds just lately restarted, Buy Now Pay Later balances make me nervous, and I’m involved a few client pullback.

The inventory is up 25% since November 2nd, and I am not chasing it till it cools off. I am able to accumulate shares at $3,200 per share and beneath.

RTX Company

Venturing out to an organization that I have not coated earlier than is RTX Company (RTX), previously Raytheon. Given the geopolitical local weather in Europe, the Center East, and the Pacific, Aerospace and Protection (A&D) is a terrific sector. I believe RTX is recession-resistant, with a $190 billion backlog and important authorities contracts.

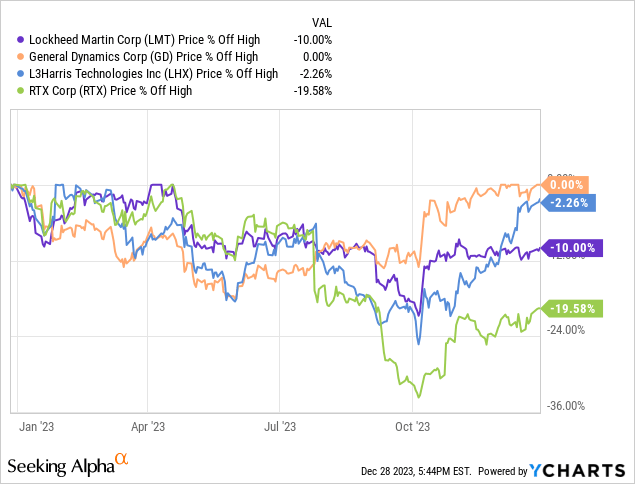

The issue is that this is not precisely breaking information, proper? Shares like Lockheed Martin (LMT), Basic Dynamics (GD), and L3 Harris (LHX) are driving excessive, as proven beneath.

RTX missed the boat due to serious issues with some Pratt & Whitney engines. The short-term ache could possibly be a long-term achieve for affected person traders.

RTX introduced one other accelerated $10 billion share buyback program in Q3 to help shareholders, and the yield of two.8% is larger than latest averages and simply coated by free money stream.

Amazon

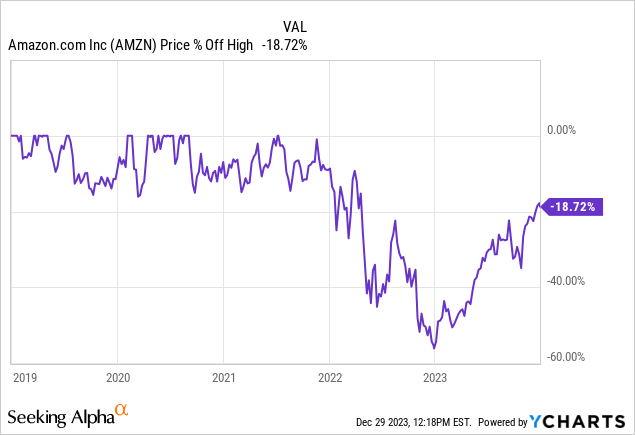

A lot has been made in regards to the Magnificent 7’s unimaginable rise in 2023. However once more, that is an arbitrary timeframe. Amazon inventory rose 81% in 2023 however continues to be 19% off its all-time excessive. It simply occurred that the inventory troughed close to the brand new yr, as proven beneath.

That is the longest the inventory has gone in over 5 years with out making a brand new all-time excessive. Its 2021 excessive was partly pushed by financial stimulus resulting in a tech bubble, however it’s nonetheless telling.

In the meantime, the enterprise is superior to any time within the firm’s historical past.

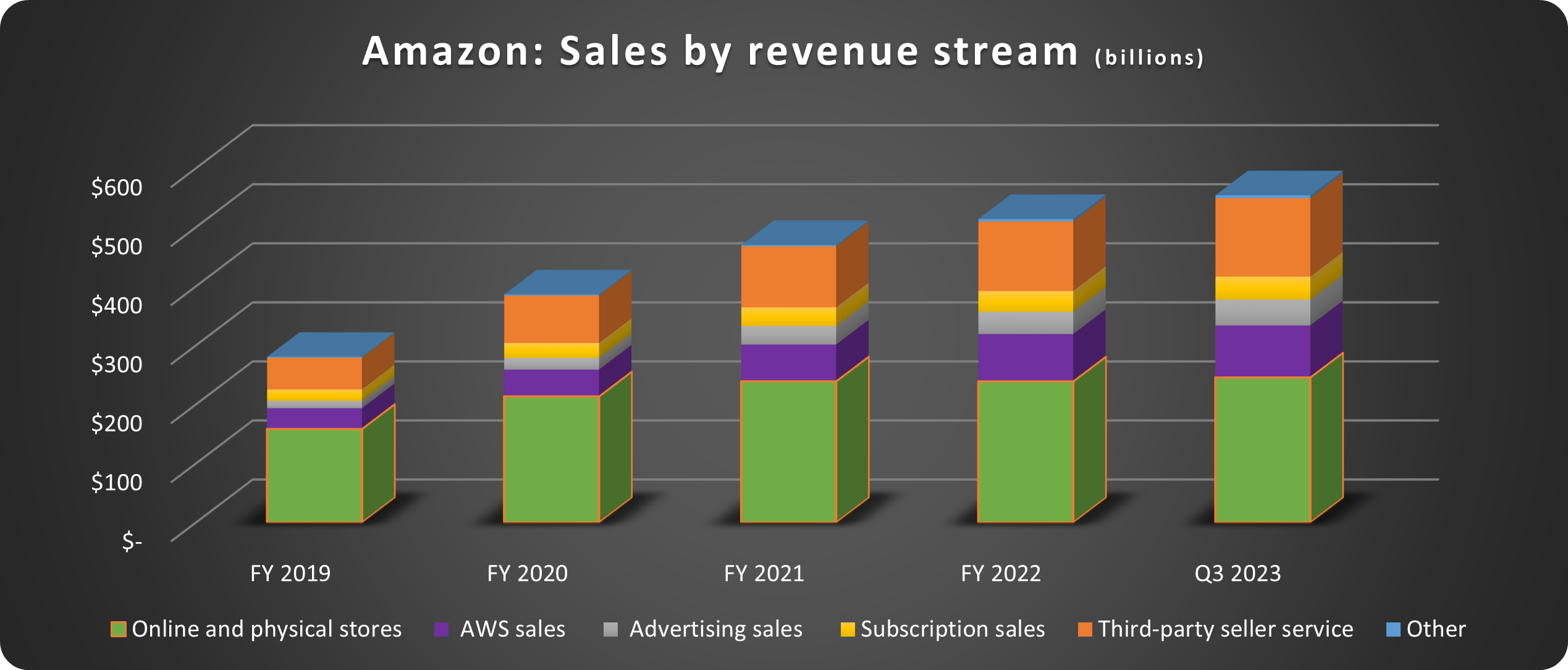

Income is diversified, and companies now outpace low-margin product gross sales, as proven beneath.

Information supply: Amazon. Chart by the writer.

Corporations minimize information utilization budgets in 2023 due to recession fears, which led to Amazon taking warmth this yr as a result of AWS development slowed to the mid-teens. The other might occur in 2024. Generative AI and loosening budgets might trigger a reacceleration of development in AWS. If this occurs, the inventory will probably embark on a major rally.

UiPath

Constructing a profitable firm (and fruitful funding) is loads like making a cake. It takes many components all coming collectively on the proper time to rise. An organization can have an excellent thought, however nothing will come of it if the timing is mistaken. Or it might have an thought and timing however want extra monetary assets to implement it. That is particularly necessary now when so many corporations combat for a place in synthetic intelligence (AI).

The robotic course of automation (RPA) firm UiPath (PATH) has the components to achieve success. Listed here are just a few.

Tech and timing

Think about you run an organization’s accounts payable division. The unit receives invoices from suppliers over electronic mail, presumably lots of every day. The handbook means of opening emails, downloading attachments, after which inputting the invoice into the accounting system is extremely inefficient.

Now, think about for those who might use an RPA program to do that robotically or with restricted human supervision. That is exactly the kind of drawback that UiPath’s know-how solves. Extra corporations shall be taking a look at utilizing AI to unravel these issues as we head into 2024.

UiPath reported 10,865 prospects final quarter, together with 1,974 offering over $100,000 in annual recurring income (ARR) and 264 over $1 million – YOY will increase of 15% and 31%, respectively.

Monetary outcomes

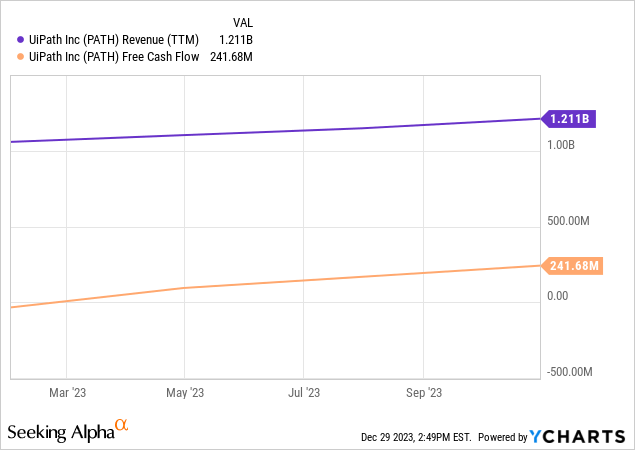

UiPath’s ARR reached $1.4 billion final quarter, and TTM gross sales crossed $1.2 billion. Simply as importantly, UiPath produced $242 million FCF, as proven beneath.

This has allowed UiPath to amass a battle chest of $1.8 billion in money and investments to fund development and make strategic tuck-in acquisitions in the event that they come up. The corporate can be long-term debt-free – a giant plus for shareholders.

Naturally, FCF is created by important stock-based compensation (SBC), which raised the diluted shares excellent by 3% YOY final quarter. However this is not essentially detrimental. Put it this fashion: Would you relatively the corporate use SBC and align workers and executives with shareholders or subject debt in a high-interest surroundings to fund operations? I will take the SBC.

Is UiPath inventory a purchase?

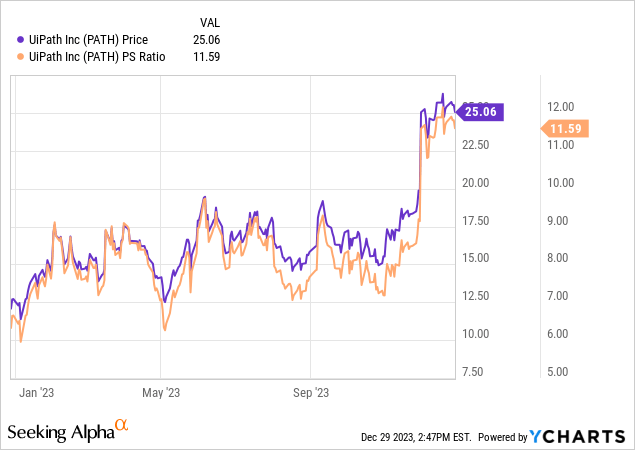

UiPath inventory trades at 11.5 occasions gross sales, which is not out of this world for a rising, excessive gross margin-tech firm. For example, Palantir (PLTR) and Cloudflare (NET) commerce for 18 and 23 occasions, respectively. Nevertheless, the inventory is on a tear (proven beneath), and ARR development is forecast to gradual to twenty% YOY subsequent quarter. Administration wants a giant yr in 2024.

The inventory has gotten forward of itself. I’ll proceed accumulating shares underneath $20.

Medtronic And Quipt House Medical

Medical machine shares have been stymied this yr by the concept that weight-loss medicine would damage the long-term outlook for issues like mobility tools, insulin pumps, diabetes therapies, CPAPs, oxygen machines, and so on.

Then, simply after I thought I had heard all of it, Stifel got here out with this gem stating that attire shares would profit. Apparently, Stifel thinks Individuals will take a miracle drug and hit the health club in droves.

I perceive the logic for every, however they’re ludicrous and juvenile of their naivety. Weight-loss medicine aren’t a magic elixir; unwanted effects are rising, and the impression on the medical tools market is wildly overblown. In the meantime, our inhabitants is getting old, and illnesses like Diabetes have an effect on a big and rising share of the inhabitants.

This makes Medtronic (MDT) and microcap firm Quipt House Medical (QIPT) compelling.

Medtronic’s dividend yields 3.3%, nicely above its 4-year common of two.5%, and its valuation metrics are higher than trade averages.

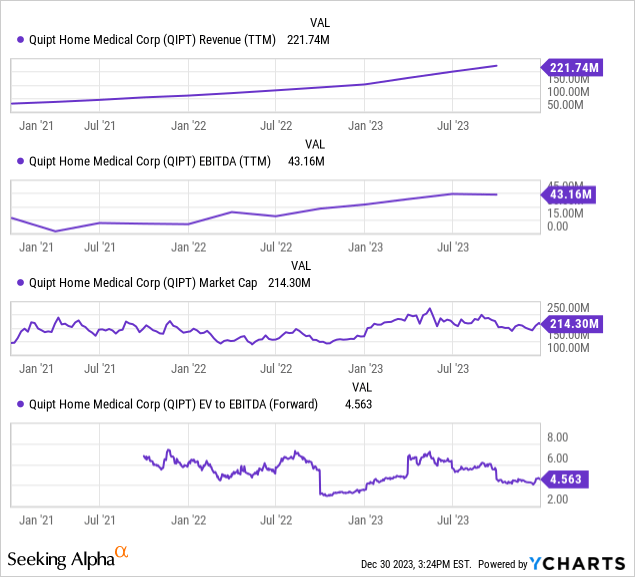

Quipt is riskier as a microcap however has important upside potential. The corporate is rising by acquisition, increasing to 26 fascinating states for respiratory care, and 78% of income is recurring.

Earlier this yr, a proposed at-the-market (ATM) inventory sale to fund acquisitions upset many shareholders. The ATM was canceled after the outcry, however the inventory stays out of favor.

Income and EBITDA are ramping up on accretive acquisitions, and the market cap doesn’t replicate the potential, as proven beneath.

The corporate has important debt to handle, primarily a $61 million credit score facility, however the dangers seem priced in.

Ringing in 2024

The latest inventory market rally makes it necessary to be selective about purchases by specializing in long-term worth performs which can be out of favor or ready till the worth is correct to build up high-flying development shares.

Wishing everybody the perfect within the New 12 months.