JHVEPhoto/iStock Editorial via Getty Images

In our last coverage of TC Energy Corporation (TSX:TRP:CA) (NYSE:TRP) we recognized the strong results that were helping deliver yet another dividend increase for the company. At the same time, we found TRP to be lagging in other metrics when benchmarked against other midstream companies in Canada. Ultimately, we came away with a “hold” rating as we continued to hold the shares as well.

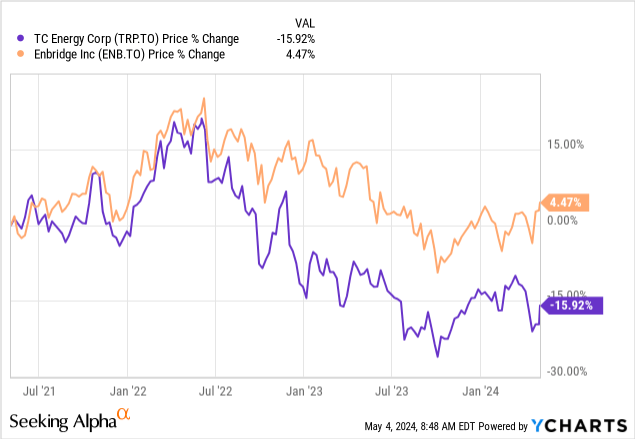

While we do own TC Energy Corporation shares, our covered calls (with $35 USD strikes) will likely evict the stock out by May of this year. We recently added a large position in Enbridge Inc. (ENB) and see that as the more attractive of the two.

Source: Massive Q4 Beat And 3% Dividend Increase

That was the story at the time, but as TRP dipped, we did create some fresh positions in the company. We review the latest results and tell you where we stand.

Q1-2024

TRP dipped a bit lower just before the earnings, as if investors feared the worst. That was definitely an error. There was nothing remotely wrong in the Q1-2024 earnings report.

TRP Q1-2024 Presentation

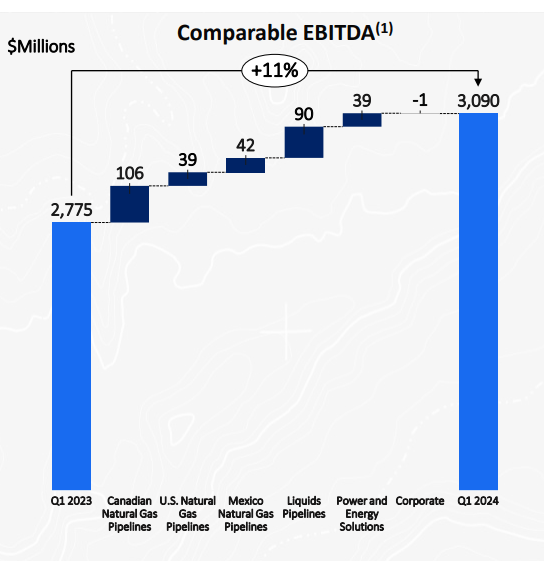

TRP’s adjusted EBITDA came in at $3.09 billion and this was far ahead of consensus which was estimating a sub $3.0 billion number. In other words, we got a 3.5% beat. That is a fairly large margin for a midstream company with highly contracted assets and 20 analysts modeling things from every side. The bridge from last year’s EBITDA shows that all asset segments contributed to this.

TRP Q1-2024 Presentation

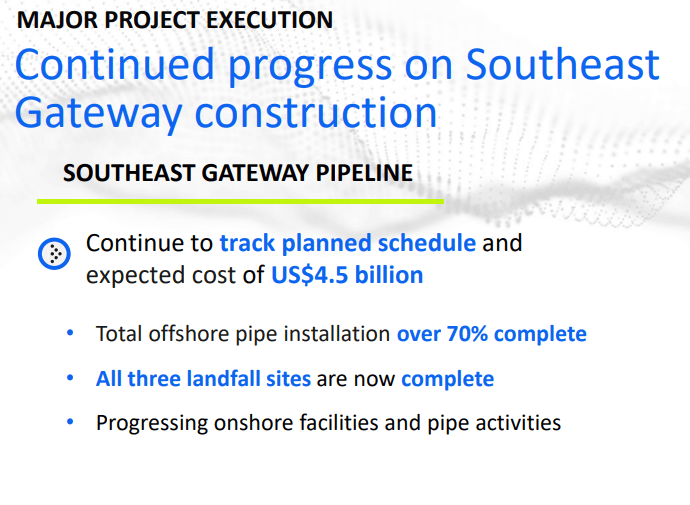

While all segments did beat where the Street was, it was Natural Gas that came in far stronger than expected. The company reiterated that it was on course for Southeast Gateway construction and the costs were tracking in line.

TRP Q1-2024 Presentation

In the energy space in general, cost overruns have plagued many firms, including TRP, in the past. One of the more recent examples we saw was from Capital Power Corporation (CPX:CA), where extremely late into the project, cost estimates were drastically increased.

CPX Q1-2024 Presentation

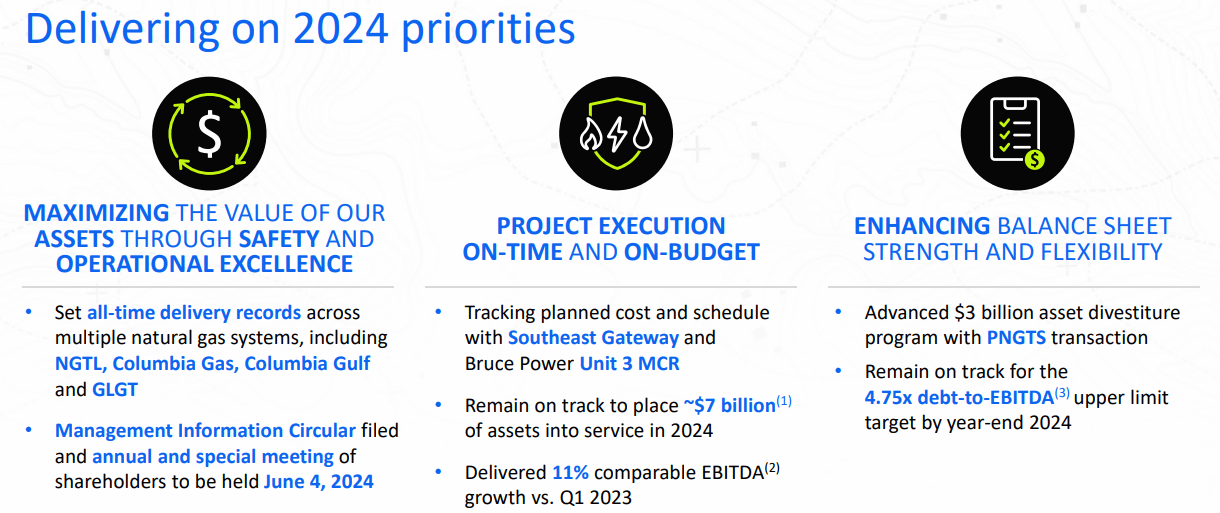

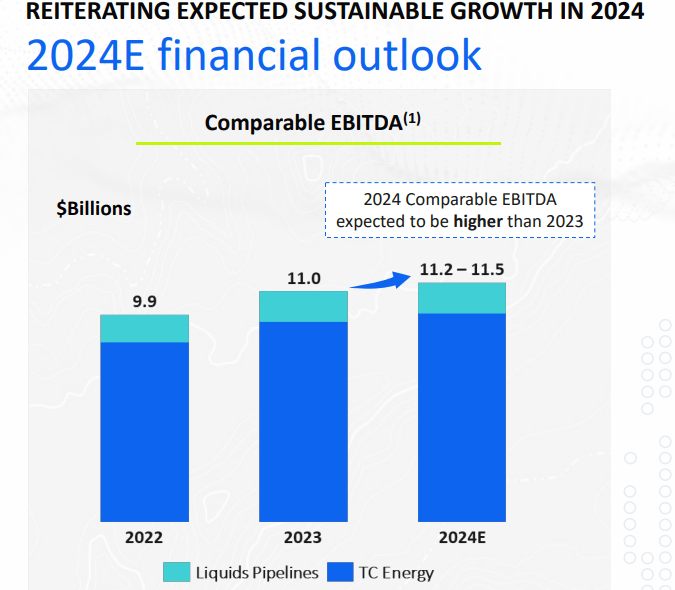

So that on-time and on-budget execution is a crucial part of the story, and it holds even more meaning for TRP as it is trying to deleverage. The company maintained its adjusted EBITDA guidance for the year and that was a bit of a surprise as the big beats so far might be seen as conducive for a higher target.

TRP Q1-2024 Presentation

But it is possible that TRP is just playing it conservative and plans to let the financials do the talking.

Outlook

At the end of last year, TRP’s debt to adjusted EBITDA was a bit away from where it (and the rating agencies) need it to be.

TRP Q1-2024 Presentation

The 4.75X target for the end of 2024 will not be achieved by just the stellar performance. It will require some asset sales, and those are coming shortly.

During the quarter, we progressed toward our $3 billion asset divestiture target with an agreement to sell PNGTS for expected pre-tax proceeds of approximately $1.1 billion (US$0.8 billion), which includes the assumption by the purchaser of the US$250 million of Senior Notes outstanding at PNGTS. This transaction implies a valuation multiple of approximately 11 times 2023 comparable EBITDA, and is expected to close in the second half of 2024 subject to regulatory approvals and customary closing conditions. In addition, we announced the sale of PRGT entities to Nisga’a Nation and Western LNG. This transaction demonstrates TC Energy’s commitment toward delivering its 2024 capital allocation priorities while supporting the continued development of critical natural gas infrastructure. This also highlights our commitment of staying within our $6 to $7 billion annual net capital expenditure limit, with a bias to the lower end, in 2025 and beyond. We are firmly on a path to enhancing balance sheet strength and achieving our 4.75 times debt-to-EBITDA3 target by year end 2024, which represents the upper limit we will manage to going forward.

Source: TRP Q1-2024 Financials

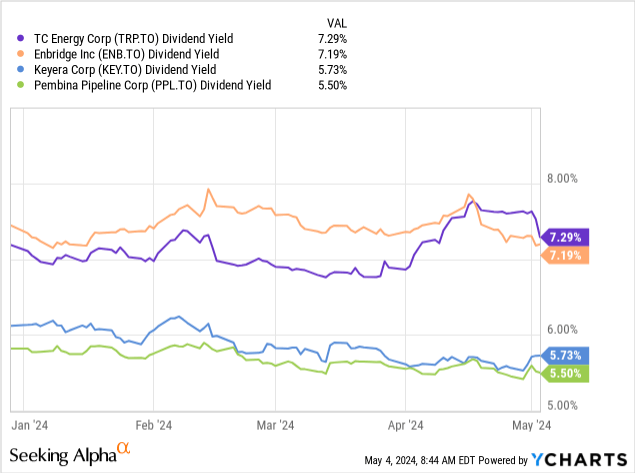

That, plus the liquids pipeline spinoff, should take TRP into the black as far as we are concerned. There are no big risks here, and the only relevant question is how an investment with TRP compares to the alternatives. TRP offers the highest yield relative to the alternatives for sure.

But as we said before, it carries far more debt. In the case of both Keyera Corp. (KEY:CA) and Pembina Pipeline Corp. (PPL:CA), the difference is almost two turns of debt to EBITDA. ENB remains the closest and is about 1 turn lower. This differential, though, will come down as TRP deleverages and ENB finally assimilates the Dominion (D) assets into its fold. We still see a slight advantage to ENB here, but the overall underperformance of TRP has faded this gap.

How We Played It

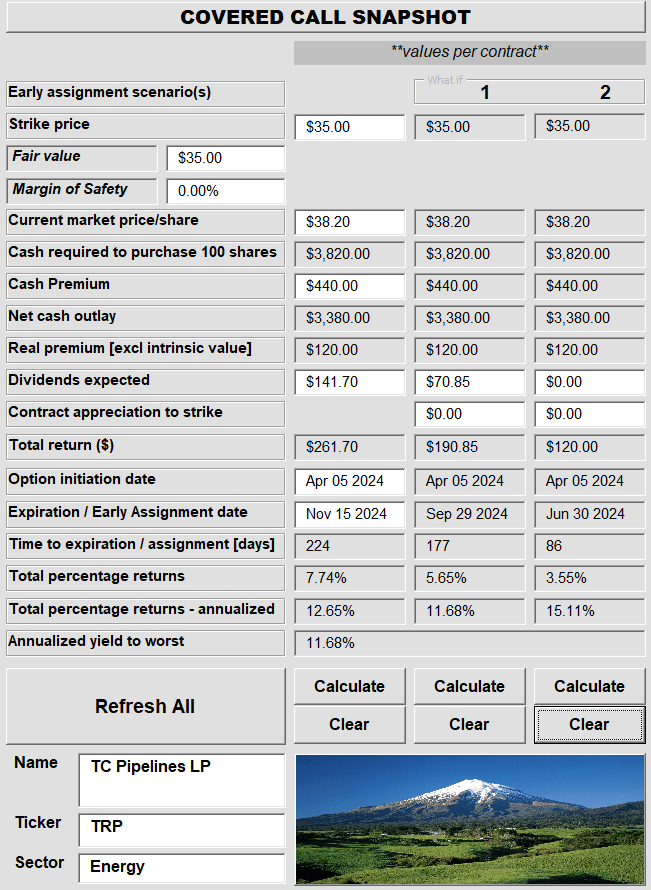

We are still hesitant to add to TRP far beyond $35.00 a share. So that is how we structured our setup. In our last trade, the stock was at $38.20.

Interactive Brokers April 5, 2024

The beauty of covered calls is that you can always choose where you want to get involved. By buying the stock and selling the $35 covered calls for November 2024, we ensured that we would only be long at that time, if the stock was under $35.00. But what if it was not? We would get a 12.65% annualized yield for choosing the price we love. While that was one of the outcomes possible, an early assignment would push our annualized yield down to 11.68%.

Author’s App

We keep making offers to own TRP at or below $35.00. Yes, with covered calls, you do purchase upfront. But by selling the calls, you are also going to hold it only if it falls hard. With those offers, we keep capturing double-digit yields while waiting to own it at a fantastic price. We rate the shares a hold for now. We will add that we got a great trade going on the preferred shares, which are rising rapidly into the reset.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.