piranka/E+ via Getty Images

Investment Thesis

Intellicheck, Inc. (NASDAQ:IDN) faced a series of challenges, including sales execution issues and a notable concentration of customers within the retail sector, which proved vulnerable during periods of economic downturn. This led to a dip in revenue growth, and since then, the company has struggled to re-accelerate growth to FY21 levels. However, I anticipate that re-acceleration will occur between 2H24 and FY25, as Intellicheck has made substantial progress in revamping its sales team and building robust pipelines. This progress is evident from its success in securing multiple large deals scheduled to launch in the latter half of 2024. These deals are expected to further diversify its revenue stream across multiple verticals, reducing concentration risk. In light of these improvements and considering its valuation, I have assigned a ‘buy’ rating to the company.

A Quick Overview Of Intellicheck

Intellicheck provides identity verification solutions to customers across various sectors, including retail, financial services, automotive, government agencies, and more, with a primary focus on preventing identity fraud. Its solutions seamlessly integrate into the hardware customers use, such as point-of-sale system scanners, mobile phones, and browsers. Once integrated, companies can effortlessly authenticate their customers’ identities by scanning their driver’s licenses.

Financial Discussions

IDN 10-Q

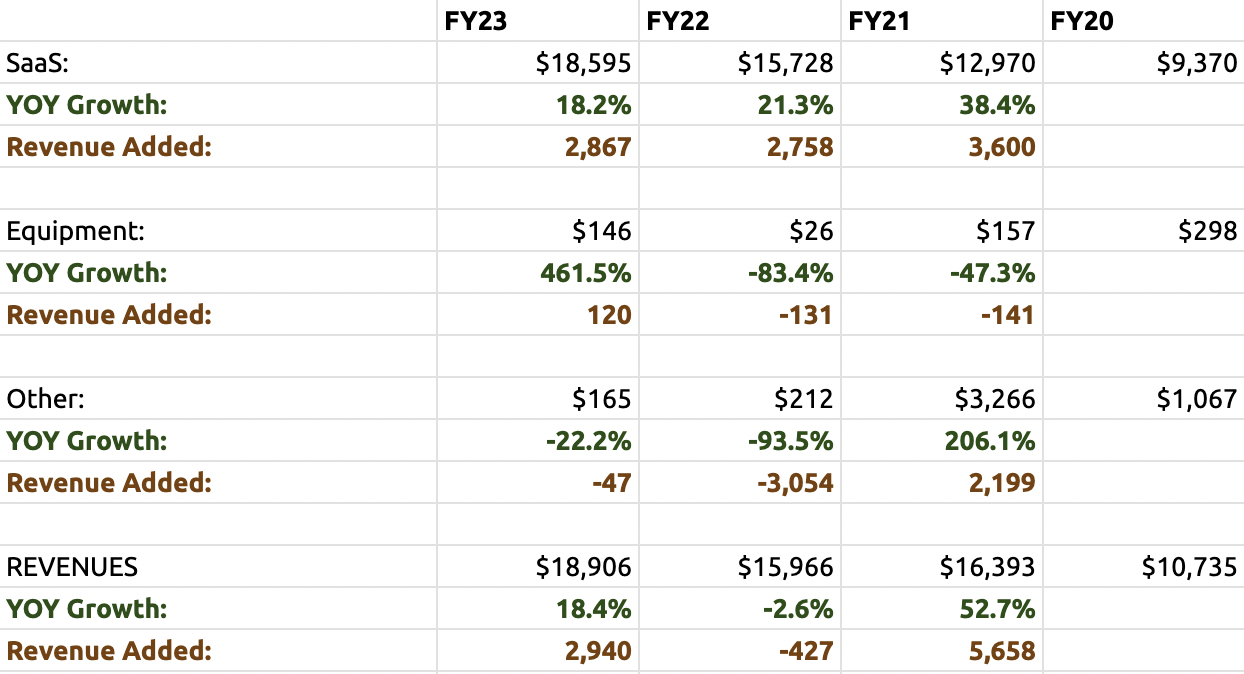

In FY23, Intellicheck delivered SaaS revenue growth of 18.2%, which slightly dipped from the growth of 21.3% in FY22. This is a decent growth, but still a far cry from the 38.4% growth in FY21. The deceleration can be attributed to 2 reasons:

1) Firstly, the sales execution issues coupled with a long sales cycle: The initial sales team in 2022 performed poorly, prompting the company to revamp its sales team. The new team has made significant progress in building up its pipelines. In the latest 4Q23 earnings call, CEO Bryan Lewis announced a wave of large deals, including a top 3 bank in the U.S., a renowned U.K. global media and tech company, one of the largest auto manufacturers, four of the largest title insurance companies, and many more. These customers are either already live or scheduled to be launched in 2H24.

This development is significant because it not only suggests a likely revenue re-acceleration in FY25, but also paves the way for more enterprises to adopt Intellicheck’s identity verification solution, bolstering its market leadership. Moreover, Intellicheck’s relationship with its customers does not end there. As customers grow larger, Intellicheck’s revenue will also grow. Customers are either charged a monthly subscription fee (capped at a certain transaction volume) or a per-transaction fee, and as they acquire more customers, the transaction volume processed through Intellicheck will also increase. However, there is a downside: this also means that its revenue is also dependent on the performance of its customers, which I will touch on later.

While there is certainly tremendous upside, in reality, smooth sailing is not always guaranteed. One challenge is that landing these customers typically requires a long sales cycle. Enterprises often have demanding needs, and Intellicheck must personalize its solution to fit each customer’s requirements. Additionally, there is the complexity of deploying its identity verification software across all of its customers’ hardware, which takes a considerable amount of time.

Thus, when combining the long sales cycle with the poor performance of the sales team, it is likely to put a drag on revenue growth. However, it appears that the sales issue has been improving, and therefore, re-acceleration is very possible.

2) Next is Intellicheck’s concentration of revenue within the retail sector

As mentioned earlier, Intellicheck’s revenue growth also depends on how its customers perform. During the 4Q23 earnings call, management reported that transaction volumes at some of their largest retail clients were down by 15% to 25%, prompting the management team to diversify revenue streams across other verticals. As the economic downturn persists, I foresee that this headwind will continue throughout FY24, albeit with a softer impact.

Next, Intellicheck’s gross margin for FY23 was 92.7%, compared to 92% in FY22, reflecting an exceptionally high gross margin for a tech company. This underscores the capital-light business model of the company, as most of its revenues are from SaaS. The operating margin sits at -12% versus -25% in FY22, marking a significant improvement as management focuses on enhancing operational efficiency and cost-cutting.

The main reason why the company is still unprofitable is because it continues to pursue growth, with SG&A expenses accounting for a significant 80% of its FY23 revenue. Typically, Intellicheck will incur initial losses as they are required to make upfront investments in onboarding enterprise clients, but as their customers go live and revenues start coming in, the company can start extracting operating leverage, which will likely occur in FY25.

Quick Overview on Balance Sheet and Cash Flow

The company also boasts a robust balance sheet, with total cash amounting to $7.98 million and no outstanding debt. Cash flow used in operations was $0.65 million, compared to $3.5 million in FY22, indicating a trend towards achieving cash flow positivity. Even if Intellicheck maintains its current cash burn rate of $0.65 million, the company has sufficient cash reserves to sustain its growth for the next 12 quarters. In summary, the risk of bankruptcy is minimal, and investors need not be overly concerned about it at this time.

Valuation

Relative Valuation

In my valuation, I included companies I see as Intellicheck’s closest competitors, specifically Mitek Systems (MITK) and OneSpan (OSPN), both of which offer identity verification software. I went a step further to include other tech firms that operate outside of Intellicheck’s industry but share similar gross margins. This was done to obtain a fair evaluation of where its valuation stands.

Currently trading at an EV/sales ratio of 2.9x, Intellicheck is at a discount compared to the average multiple of 3.5x. This discrepancy could be attributed to Intellicheck’s growth deceleration, its unprofitable status, and its position as a micro-cap company with a market cap of only $60 million, which has deterred interest from institutional investors and impeded a fair evaluation of the company. However, as growth re-accelerates and operating leverage kicks in, there may be increased interest from the market, potentially resulting in a higher multiple for the firm. In my opinion, uncertainties have already been factored into the stock’s current price, and with further upside anticipated in FY25, I rate the stock a ‘buy’.

However, if Intellicheck fails to re-accelerate its growth and revenue continues to decline, thereby delaying its path to profitability, I believe the market will assign a lower multiple to account for increased uncertainty. I would downgrade its rating to a “hold” in such a scenario.

Risks

Aside from the revenue concentration risk in the retail sector that was mentioned earlier, there are some other risks that investors should take note of is the customer concentration risk: As of FY23, the top 10 customers represent 71% of the company’s revenue. Since Intellicheck’s revenue is closely tied to how its customers perform, this could significantly impact the company’s revenue growth if its customers underperform or if it loses one of its customers. The key is to also focus on further diversifying its revenue, and mitigating this risk. Next is on execution risk. Its current sales momentum can be sustained depending on its ability to execute and maintain a robust pipeline. As we have seen how poor sales execution has resulted in growth deceleration, this could happen again if the sales team underperformed. This could also further delay its path to profitability, and as a result, the market may discount its valuation as they priced in greater uncertainty over its ability to attain profitability.

Conclusion

Intellicheck has made significant progress in resolving its sales execution issues, as evidenced by the robust pipelines announced in 4Q23. This suggests the potential for re-acceleration in revenue growth and increased profitability in FY25. Additionally, its balance sheet remains strong, with ample cash and zero debt. Valuation-wise, Intellicheck appears undervalued compared to its peers, likely due to its status as a micro-cap with an extremely low market capitalization of $60 million. However, this is not without risk, as investors should be cognizant of the risks highlighted, including revenue concentration and execution challenges. Considering the progress made and its valuation, I have assigned a ‘buy’ rating to Intellicheck.

What are your thoughts on the company? Do you agree or disagree with my analysis? Let me know in the comment section, as I would like to hear from you!

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.