tazytaz

Investment thesis

My interest in the gold mining industry was caused by this precious metal trading at an all-time high. I conducted an analysis of Newmont Corporation (NEM) in February, and today I want to share my opinion about another solid player in the industry, B2Gold (NYSE:BTG). The company’s financial performance over the last decade has been quite impressive, with solid revenue growth and profitability expansion. B2Gold has a fortress balance sheet and pays a generous 6.1% dividend yield, which underscores the management’s exceptional capital allocation efficiency. My valuation analysis suggests that BTG is around three times undervalued. All in all, I assign BTG a “Strong Buy” rating.

Company information

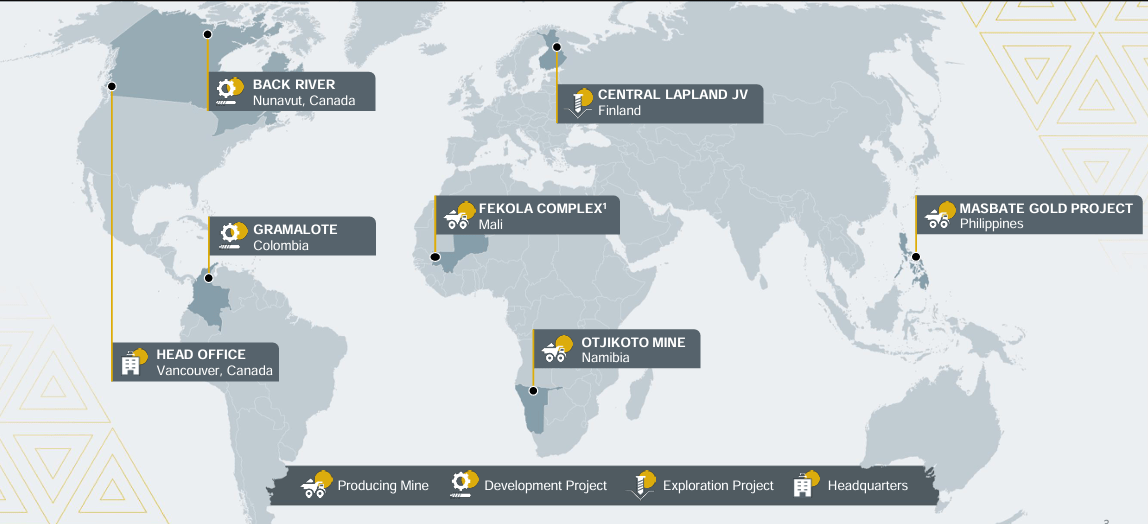

According to the management, B2Gold is a Vancouver-based gold producer with three operating mines: the Fekola Mine in Mali, the Masbate Mine in the Philippines and the Otjikoto Mine in Namibia, and a fourth mine under construction in Canada, the Goose Project. In addition, the company has a portfolio of exploration and development projects in a number of countries including Mali, Finland and Colombia.

BTG’s latest earnings presentation

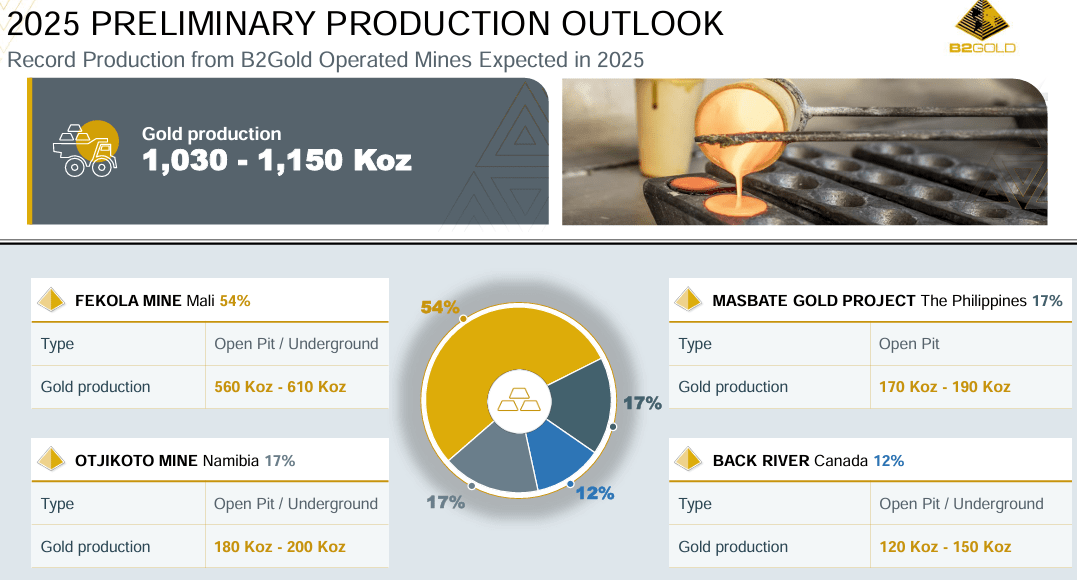

Fekola mine is the largest, and it has generated 55% of the company’s total revenue in Q1 2024.

Financials

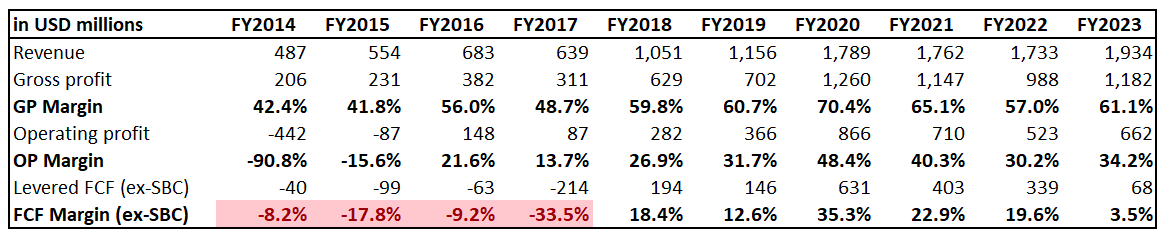

As I always do, I start analysis of a new company with looking at its financial performance over the last decade. From this point of view, BTG’s performance has been robust, with a 16.6% revenue CAGR and profitability metrics improving substantially compared to ten years ago.

Author’s calculations

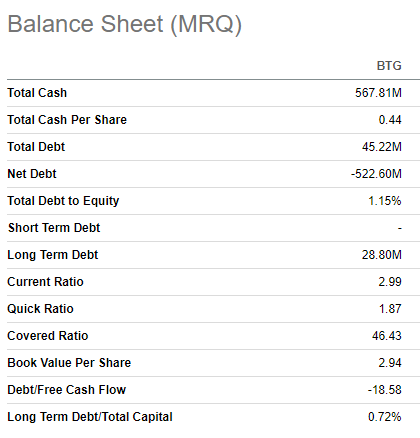

Since the company’s operations are involved in gold mining, its profitability is volatile and highly dependent on commodities prices. Moreover, the business is inherently capital intensive, which also significantly affects the free cash flow [FCF] margin. Despite inherent volatility in profits and capital intensity of the business, BTG’s management’s capital allocation is robust since the company balances successfully between investing in business expansion, paying a generous 6.1% dividend yield and sustaining a healthy balance sheet. The company has almost no debt and its liquidity position is strong, making BTG very financially flexible to finance its new expansion projects.

Seeking Alpha

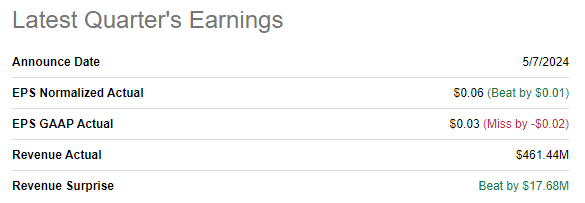

Recent financial performance has demonstrated strength as well. BTG reported its latest quarterly earnings on May 7 when the company delivered positive revenue and adjusted EPS surprises. There was a pullback in revenue dynamic with a 2.6% YoY decline, after stellar last year’s Q1 when BTG delivered a 30% YoY revenue growth.

Seeking Alpha

I consider BTG’s Q1 financial performance to be robust despite revenue decline because this decline is explained by temporary factors. The decrease in revenue was mostly caused by a sharp decrease in gold production at Fekola mine, from 166 thousand ounces to 119 thousand. This decrease was expected by the management because Q1 of 2023 benefitted from a favorable mine phasing sequence, with Phase 6 of the Fekola pit providing significant high-grade ore to the process plant.

BTG

Fekola’s revenue dip was almost in full, offset by two smaller mines. Masbate mine delivered a massive 73% YoY revenue growth, while Otjikoto mine revenue growth was more modest at 4% YoY. The company also enjoyed a 9% higher average realized gold price in Q1 2024 compared to the same quarter last year.

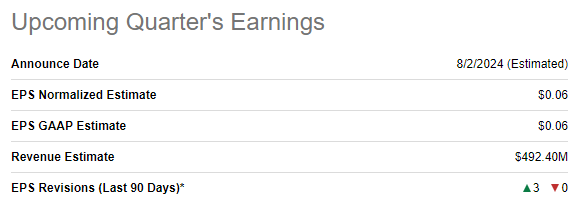

The fact that consensus estimates expect Q2 revenue to return to the growth path also underlines that Q1 revenue stagnation was temporary. Wall Street expects BTG to deliver $492 million in revenue in Q2, which will be 4.6% higher on a YoY basis. There were three upward Q2 EPS revisions over the last 90 days, which also emphasize the bullish sentiment around BTG’s near term prospects.

Seeking Alpha

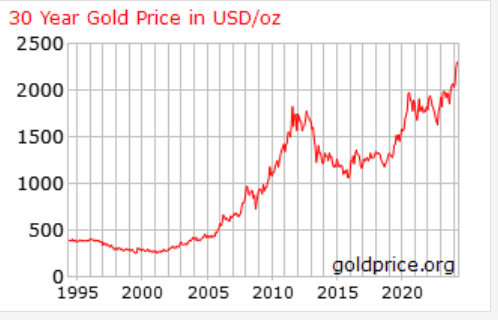

The optimism around BTG’s near term prospects appears to be sound as the gold price continues to break new records in 2024. The increased demand for gold is explained by the fact that it is a defensive asset. The world has experienced a lot of disruptions since 2020, including the one-in-a-century pandemic and the biggest war in Europe since WWII. The geopolitical situation in the Middle East is also complex, and the world’s two largest economies are in the condition of a “Cold War”. All these massive factors make investors more cautious, which pushes up the demand for gold.

goldprice.org

The U.S. Congress recently approved a new $61 billion aid package for Ukraine, which means that the probability of war ending soon is likely to be low. Israel continues its military operation against Hamas, which increases tensions with other Muslim countries in the region. Therefore, I do not expect the geopolitical situation to ease in the foreseeable future, which will highly likely keep gold prices higher for longer. This will be a solid tailwind for BTG, especially considering that the management expects to achieve record production in 2025.

BTG

To sum up, there are numerous fundamental reasons to be bullish about BTG. The company enjoys industry tailwinds, which we see from gold prices breaking new historical records in 2024. BTG demonstrates exceptional profitability across key metrics. What is more important is that the management allocates these profits wisely and successfully balances maintaining growth and financial flexibility together with keeping shareholders happy with generous dividends.

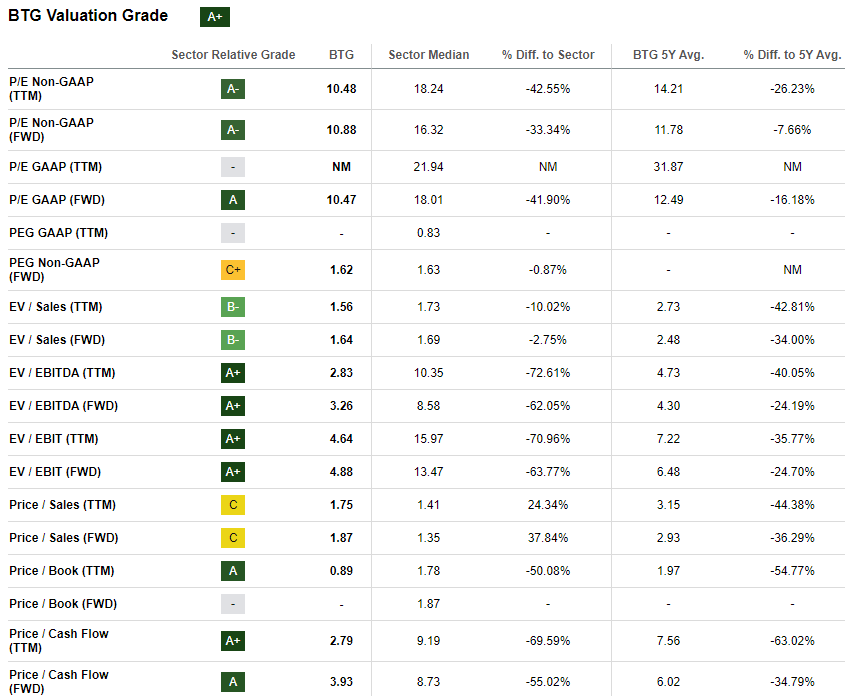

Valuation

BTG’s share price declined by 34% over the last twelve months and recorded a 12% decline YTD. BTG’s valuation ratios are extremely attractive, both compared to the sector median and to the company’s historical averages.

Seeking Alpha

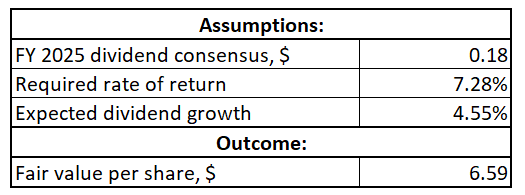

As I mentioned above, BTG pays a generous 6.1% forward dividend yield. Therefore, I think that using a dividend discount model [DDM] to calculate the stock’s fair value will be reasonable. I use a 7.28% cost of equity calculated by Gurufocus as a required rate of return. Since I am calculating a target price for the next twelve months, I use an FY 2025 consensus dividend estimates of $0.18. For dividend growth, I use the last three years’ CAGR of 4.55%.

Author’s calculations

As shown in my above calculations, BTG’s fair value per share is $6.6. This is almost three times higher than the current share price, meaning that BTG is massively undervalued.

Risks to consider

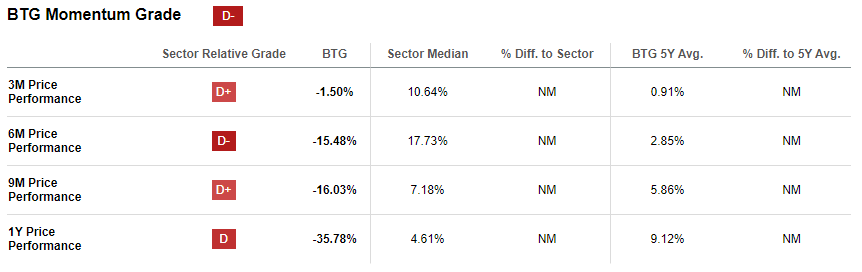

From the stock performance perspective, the momentum is quite weak. According to Seeking Alpha Quant, BTG has an extremely low “D-” momentum grade, meaning that the market’s sentiment around the stock is weak. This looks like a significant weakness to me because the share price stagnates even despite robust performance and overall bullishness around gold. Therefore, there is a very high level of uncertainty regarding the timing of BTG moving closer to its fair value.

Seeking Alpha

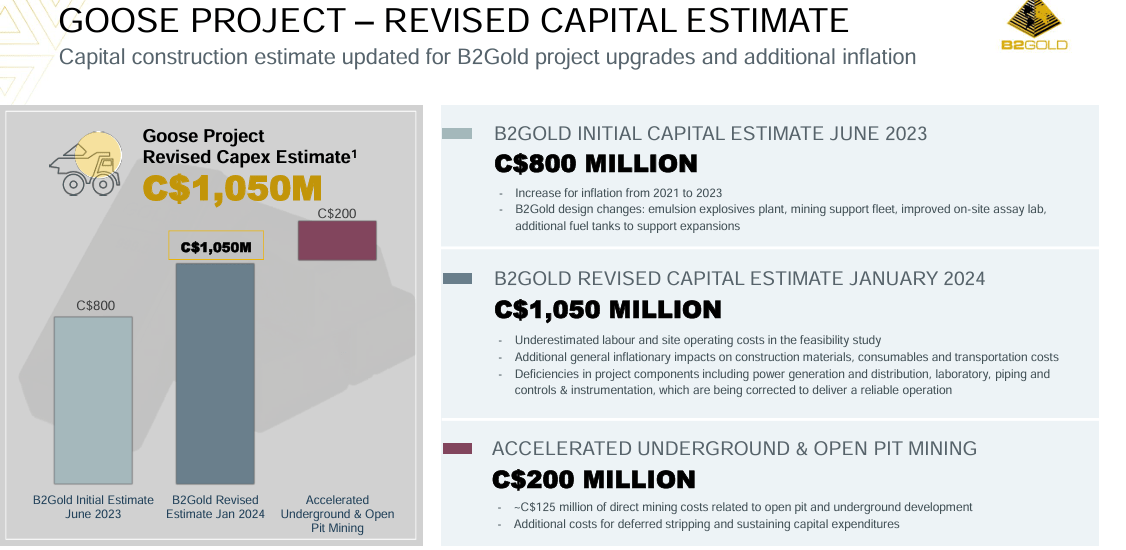

The current large capital project, Goose Canada, the company’s fourth mine, poses risks to BTG. According to the company’s latest presentation for investors, the latest revised capital expenditure estimate for the project is already 31% higher than the initial estimate. Since only six months passed between the initial estimate and its revision, there is a notable likelihood of another capital budget upgrades for the project. While budget revisions for large, complex projects are not something unusual, negative headlines might cause investors’ panic.

BTG

Bottom line

To conclude, BTG is a “Strong Buy”. The company’s financial performance is strong and B2Gold has ambitious plans to continue expanding its footprint. I like the management’s capital allocation approach since it successfully balances between investing in new projects, paying out dividends and sustaining a robust balance sheet. Therefore, I believe that a 6.1% forward dividend yield is relatively safe, and the company has significant financial flexibility to continue fueling growth over the long term. Moreover, my DDM analysis suggests that the stock is almost three times undervalued.