andresr/E+ via Getty Images

Despite the fact that its shares are up 49% in USD terms (65% in JPY) over the past 12 months, most readers will likely be unfamiliar with Toyo Tire Corporation (OTCPK:TOTTF). While nothing goes up forever, and I believe that there is a material chance of a pullback, both TYO:5105, and its American Depository Receipt (TOTTF) represents good value at current levels. Accordingly, I rate both as a hold for long-term investors.

I. Overview of Toyo Tire

Toyo Tire Corporation manufactures and sells tires in Japan, North America, and internationally under the brands of Toyo Tire, Silverstone, and Nitto. Approximately 10% of its revenue is derived from the sale of automobile parts such as engine mounts, struts, and anti-vibration parts, that in general, have rubber as a critical material.

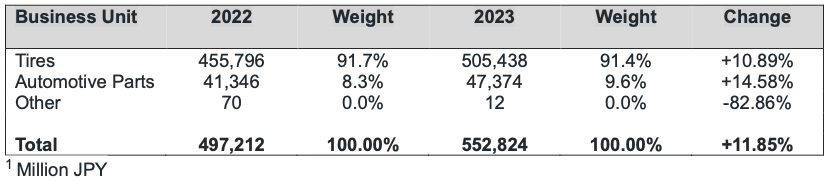

Table 1: Toyo Tire – Sales by Business Unit1

Toyo Tire’s sales by business unit (Analyst’s analysis and Toyo Tire’s financial statements.)

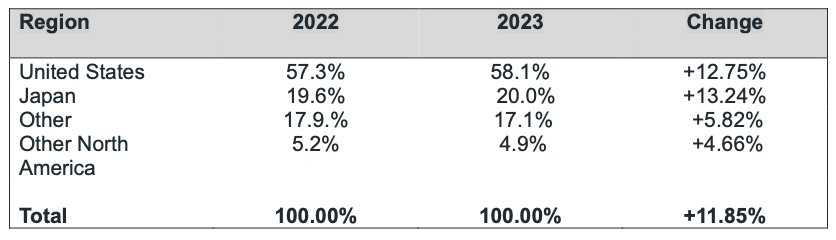

Although it is a Japanese company, 63% of Toyo’s sales are in North America, and Japan is only its second-largest market. The EU and China are in the “Other” Region, and both represent growth opportunities for Toyo.

Malaysia, a significant producer and exporter of natural rubber, serves as a production hub for the company’s network of factories in the US, Canada, China, Japan, and Serbia. The Serbian factory was opened in late 2022, and it has the capacity to produce 5 million tires annually. Serbia was chosen to support Toyo’s European business because of its low labour costs, and because goods produced in Serbia are able to be exported duty-free “to a market of more than 1 billion people that includes the European Union, the Russian Federation, USA, Kazakhstan, Turkey, Southeast Europe, the European Free Trade Agreement members, and Belarus.”

Table 2: Toyo Tire – Sales by Region

Toyo Tire’s Financial Statements

II. Ownership

Toyo Tire’s five largest shareholders are the Mitsubishi Corporation (20%), Orbis Investment Management Ltd. (4.88%), Asset Management One Co. Ltd. (3.53%), Bridgestone Corporation (3.24%), and Toyota Motor Corporation (3.10%). Three of these shareholder, Mitsubishi Corporation, Bridgestone Corporation (OTCPK:BRDCY), and Toyota Motor Corporation (TM), should be highlighted.

When Japan first industrialized in the late 19th Century, a number of family-owned conglomerates, or Zaibatsu, formed large diversified trading companies called Sogo Shosha, to trade with the rest of the world. These companies were recently featured in Berkshire Hathaway Inc.’s (BRK.A) annual meeting by Warren Buffett. The Zaibatsu were broken up after the Second World War into thousands of smaller companies. However, when the American occupation of Japan finished in the 1950s, many re-formed into a number of loosely linked alliances, often with cross-shareholdings of member companies. Mitsubishi is one of the largest of these groups, and other group members include MUFG Bank (Japan’s largest bank), Mitsubishi Electric, and Mitsubishi Heavy Industries. Toyo Tire benefits from its affiliation with Mitsubishi Corporation, as it offers a stable source of raw materials, and access to other affiliated companies such as Isuzu Motors Ltd., the second-largest seller of commercial in Japan.

Bridgestone is the second-largest manufacturer of tires in the world. In 2008, Toyo and Bridgestone each purchased shares in the other to form an alliance designed to enhance cooperation in R&D and procurement. In 2020, each company reduced their holdings in the other by 50 percent.

Toyota Motor Corporation is the largest manufacturer of cars in the world, and it is Toyo’s largest customer.

III. Toyo Tire’s Market Position and Customer Base

The tire business is extremely fragmented and competitive; the ten biggest companies have, collectively, only 65% of the market. As the tenth-largest Tire Company in the world, with more than 60% of its sales in North America, Toyo is a niche player.

Per Table 3, Toyo had a very good year in 2023, with overall sales increasing by 10.8% – only The Yokohama Rubber Company, Limited (OTCPK:YORUF) did better.

Table 3: Top Ten Global Tire Manufacturers by Revenue, 2023

Sources – Car Logo Magazine, Seeking Alpha, Financial Statements of the of the companies referenced

The OE (Original Equipment) market sector consists of tires that are placed upon the approximately 75 million new cars that are sold annually. It is dwarfed by the replacement market, which is replacing worn-out tires on the 1.47 billion cars that are already in service. Having your tires placed upon new vehicles is important, not only for the initial sale, but also for follow-up replacement sales. Toyo’s OE sales are concentrated in a few Japanese car manufacturers (Toyota, Mazda, and Nissan), with which it has cross-shareholding arrangements. These deep relationships form a moat, and sales to these customers are very stable, though it must be noted that if Toyota, Mazda or Nissan start to lose market share, their demand for tires will decrease.

Toyo’s market share in the North American OE segment in 2023 was only 1.2%, or 14th overall. This may be due to supply limitations (Toyo produced 46,500 tires per day in North America versus Goodyear’s 270,500 per day), or it may be due to the fact that supplying tires to competitors of Toyota, Mazda, and Nissan would be frowned upon by those companies.

Toyo occupies a more favorable position in the North American replacement tire segment. In 2023, Toyo ranked joint 9th (2.5% market share) in the Passenger Vehicle Segment. Michelin and Goodyear, the joint number one companies, each had 10% of the market. In the more profitable Commercial Vehicle Segment, Toyo ranked 7th, with a 5.5% share of the market. This compares favorably with Goodyear, the market leader in the Commercial Vehicle segment, whose share of this segment is 7.5%. The fact that Toyo’s market share is higher in the replacement market than it is in the OE market speaks well of Toyo’s overall value proposition of price, performance, durability, and noise reduction.

Table 4: Toyo Tire – Significant Customers

Toyo Tire’s website

IV. Financial Data and Valuation

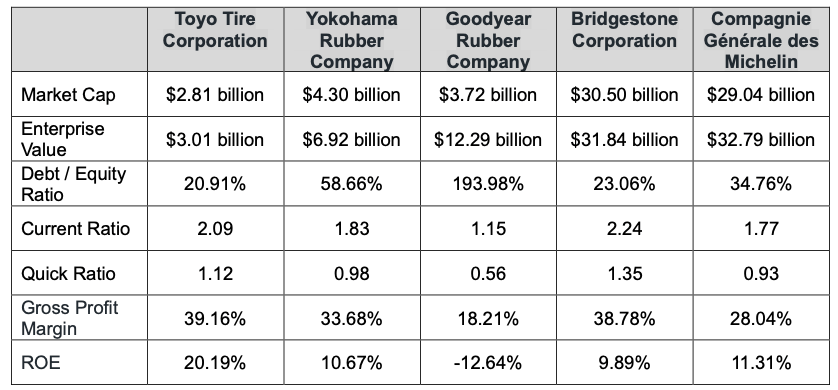

Tables 5 and 6 compare Toyo Tire to four competitors. Bridgestone and Compagnie Générale des Établissements Michelin Société en commandite par actions (OTCPK:MGDDF) are the two market leaders, each with approximately 15% of global sales. The Goodyear Tire & Rubber Company (GT) is the third-largest tire company in the world, and Yokohama Rubber Company is a similar-sized Japanese tire company.

Toyo Tire has an extremely strong Balance Sheet as indicated by its Debt / Equity Ratio of 20.91%. It is also extremely liquid as shown by its Current Ratio and Quick Ratio, and of the companies analyzed, only Bridgestone is comparable on these metrics.

With a Gross Margin of 39.16%, Toyo’s profitability is superior to its competitors, again, with only Bridgestone being comparable. Finally, Toyo’s ROE of 20.91% is extremely high, nearly double that of Michelin, the next best performer.

Table 5: Select Financial Data

Seeking Alpha

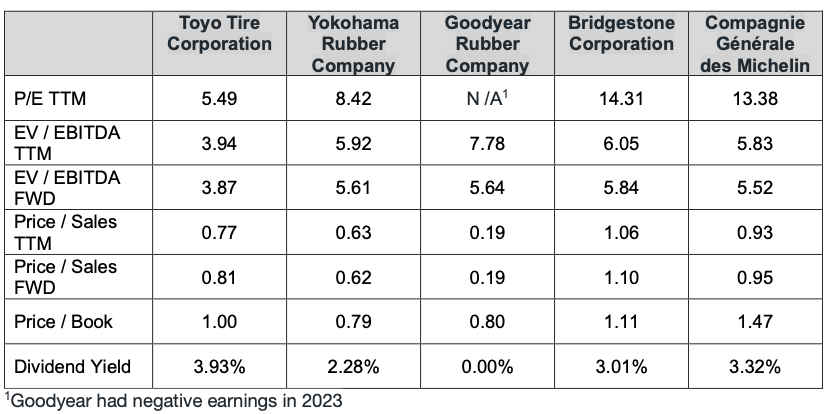

Despite its superior Balance Sheet, profitability, and Return on Equity, as per Table 6, Toyo Tire’s shares trade at a discount to the other four companies featured. It is possible that the market is penalizing Toyo Tire for its size or its country of origin. However, Yokohama Tire is a similar size, and it is also a Japanese company, and it trades at much higher multiples of earnings and EBITDA.

Table 6: Valuation

Seeking Alpha

V. Recent Performance

Toyo Tire Corporation’s revenue and earnings have grown rapidly over the past three years. As a result, its shares are up 65% over the past 12 months in JPY terms, and 49% in USD.

Table 7: Compound Annual Growth Rates*

| YoY | 3Y | 5Y | 10Y | |

| Revenue | 11.18% | 17.16% | 7.05% | 4.09% |

| EBITDA | 52.09% | 23.38% | 9.57% | 6.61% |

| EPS | 50.69% | 83.56% | 41.38% | 17.79% |

* Figures as at Year End December 31, 2024

On May 14, 2024, Toyo reported its Q1 ’24 financial results. Overall revenue was down 1.2% from the same period the year before, and 11.2% from the previous quarter. However, EBITDA increased by 46.4% from Q4 ’23, and by 115% from the same quarter in 2023. Operating income was $174.9 million, which was 78% greater than Q1 ’23. The market was disappointed by these figures as the underlying Japanese equities have fallen by approximately 4%.

VI. Other Factors to Consider

There are a few things to note about TOTTF.

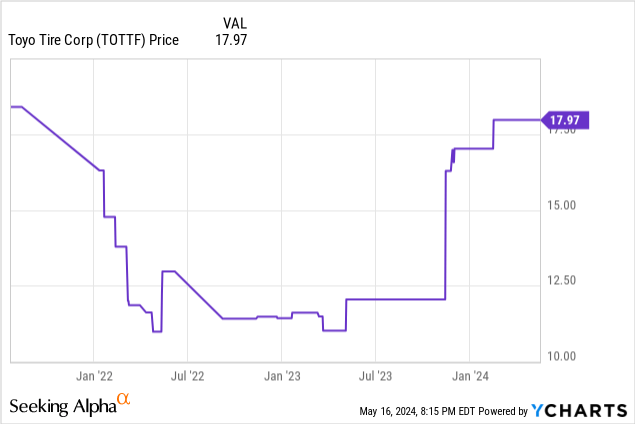

1) TOTTF trades over-the-counter (OTC). As per Chart 1, it is extremely illiquid and those looking for real-time pricing information are referred to the OTC Bulletin Board. Being illiquid, there is a wide Bid / Offer Spread. For example, the closing price on May 16, 2024, was $17.97. The best Bid was $17.49 and the best Offer was $18.38. Meanwhile, The closing price of the underlying equity in Tokyo, TYO:5105, translated into a USD price of $17.91 using the JPY / USD exchange rate at the time.

I note that many brokerage firms such as Charles Schwab are able to execute trades for their clients on the Tokyo Stock Exchange, and as the liquidity of TYO:5105 is much better than TOTTF’s, those looking to invest in Toyo Tire Corporation may want to explore this alternative.

Chart 1

2) As an ADR, TOTTF does not confer direct ownership in Toyo Tire Corporation to holders. A sponsoring bank (Citibank in this case) is the actual owner of the shares, and they issue certificates that are backed by those shares. This is what ADR holders are actually purchasing.

3) Dividends paid to foreign investors by Toyo Tire are subject to Withholding Tax. This tax is deducted at source, and it varies by country. In the case of America, the withholding tax rate is 10%, and as a result, TOTTF’s dividend is less than the dividend on TYO:5105.

While holders of the underlying Japanese equity may be able to use the foreign tax paid as a tax credit (readers should consult with their own accountant), this is not the case for ADRs such as TOTTF.

VII. Conclusion

Toyo Tire Corporation, as part of the Mitsubishi group, benefits from a network of related companies. Its deep relationships with Toyota, in particular, but also Nissan and Mazda, provide Toyo with a stable source of demand in the OE, or Original Equipment market. This in turn has allowed Toyo Tire access to the much larger replacement tire market segment, particularly in North America. Its market share in this segment is approximately double its share of the OE market, which indicates that car owners whose vehicles were originally equipped with competitors’ tires, often chose to replace these tires with ones manufactured by Toyo.

Operationally, Toyo Tire has performed exceptionally well in the past 3 years. As a result, its equity has outperformed both the S&P 500 and its benchmark indices, the Nikkei 225 and the Topix, by some margin. Despite this, TOTTF and TYO:5105 still look like good value, and holders of TOTTF should maintain their position.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.