Vector/iStock via Getty Images

Investment Thesis

Since coming public via SPAC in March 2020, the business experienced pandemic-induced volatility, which is reflected in its share price over the period. Despite this, the company has managed to pay a dividend consecutively for seventeen quarters, reflecting the resilience of the business and management’s commitment to return capital to its shareholders. The company is led by a long-standing management team comprising of its Chairman Luis Campos and CEO Andres Campos.

Shares currently have a dividend yield of 8% and are trading at an EV to 2024 EBITDA multiple below 5. The company’s entry into the US market would add a new chapter to its growth story, and possibly act as a catalyst to drive further upside. I therefore believe the current share price offers an extremely attractive valuation for investors to go long this name.

Company Overview

Betterware de Mexico (NASDAQ:BWMX) is a direct-to-consumer company selling a broad collection of household items in Mexico. The company operates a capital-light business model and primarily makes sales to end consumers through multi-level marketing [MLM], using independent distributors throughout the country. It also sells its products directly through its own website.

In April 2022 Betterware de Mexico acquired Jafra, which operated on a similar business model selling beauty and cosmetic products in Mexico as well as the US. For FY2023, Jafra accounted for 57% of the consolidated revenue, while the Betterware segment accounted for 43%.

Financial Review

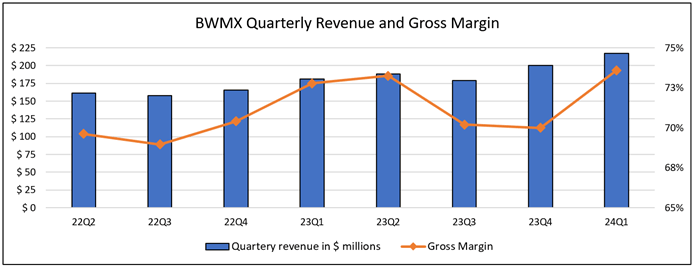

Solid revenue growth

Created using company data

Despite benefiting greatly from an increase in the number of distribution partners during the pandemic, the business struggled since the re-opening as the distribution partners returned to their prior jobs. Having navigating these headwinds in 2022, the business returned to a robust growth of nearly 13% in FY2023. Furthermore, the company has managed to increase its gross margins sequentially over the recent quarters, reaching as high as 74% in Q1 2024 as shown above.

While the year-over-year growth rate in Q1 was 10.4%, management’s guidance for FY2024 calls for revenue growth of 8% at the mid-point. Given management’s history of beating its revenue guidance, it is likely that these figures are fairly conservative. Moreover, with Mexican GDP growth expected to be close to 2.4% in 2024 according to Statista, it should be a tailwind that further supports the company’s growth.

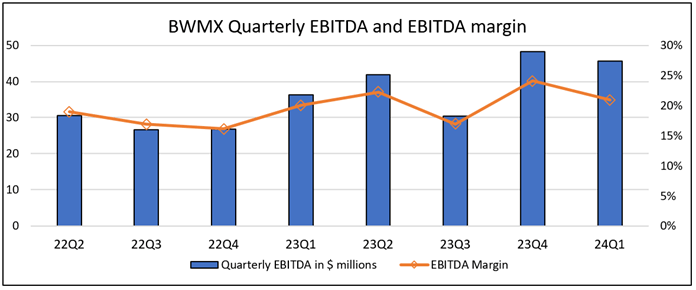

Improving profitability

Created using data from Seeking Alpa

Along with its double-digit revenue growth rate, the company has been able to significantly improve its profitability, as shown above. In its most recent quarter, with revenue up 10%, its EBITDA grew even faster at 15%, showing the operating leverage that the business has due to its capital-light model. Likewise, management’s guidance for 2024 calls for an EBITDA growth of 11% at the midpoint, outpacing the expected revenue growth by three hundred basis points.

Debt reduction in focus

The acquisition of Jafra was largely funded by debt, which subsequently raised the leverage of the company. When the company’s share price was near its all-time low’s towards the end of 2022, its net debt to TTM EBITDA ratio stood at 2.6. Today, with its net debt close to $250 million, this ratio is at 1.78, leaving the company in a much healthier financial condition. The interest rate on its debt is around 14% which leads to interest payments of close to $40 million annually. Management is now prioritizing debt repayment, and the recent sale of the Jafra headquarters will contribute towards this.

Valuation

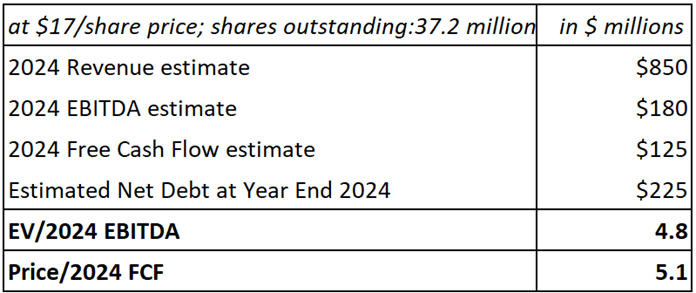

BWMX is expected to deliver close to $180 million in EBITDA for 2024 at a margin of roughly 21%. The business has inherently good free cash flow conversion from EBITDA due to low capital expenditures of roughly $15 million. However, its free cash flow conversion metric has recently been weaker due to the high interest payments. Accounting for the capex and interest costs, I estimate its FCF for 2024 to end up close to $125 million, which would imply a 70% conversion from its EBITDA. This would be more than sufficient to cover its current dividend payments, leaving room to paydown debt.

My valuation model based guidance and my estimates

According to my estimates shown in the table above, BWMX trades at an EV to 2024 EBITDA and Price to 2024 FCF of just 4.8 and 5.1 respectively. This is a significant discount to D2C peers selling household products such as Newell Brands (NWL) and The Container Store Group (TCS) which trade at EV to 2024 EBITDA ratios of 9.4 and 17.7 respectively. The valuation discount remains towards its D2C peers in the beauty and cosmetics industry such as Coty (COTY) and L’Oreal (OTCPK:LRLCF), which trade at EV to 2024 EBITDA ratios of 12.3 and 23 respectively.

It is evident the business trades at a cheap valuation on both a relative and absolute basis. My reasoning behind the discounted valuation is that the company operates mainly outside the US and also the market’s skepticism towards the MLM model. I believe the former is being addressed as the company has entered the US market this year.

Entry into the US market a catalyst for valuation to re-rate

The company entered the US market officially earlier this month. Management remains highly confident of this strategic direction and Chairman Luis Campos re-iterated this during the Q1 2024 conference call, saying:

So, I am pleased to announce that Betterware US has begun operations as scheduled. We are very optimistic about the growth that we can achieve in the US market, given its size, dynamism and strong consumption levels. We believe we have the right strategy to effectively penetrate the US home solutions market and we will do everything necessary to maximize our results and return on investment.

Due to Jafra’s existing presence in the US, Betterware de Mexico derived 8% of its FY 2023 revenue from the region, according to its 2023 Annual report. Management plans to leverage Jafra’s minor presence to make a more significant push into the market. CEO Andres Campos outlined their strategic rationale on the conference call when he said:

We selected Dallas, Texas for our US headquarters for several strategic reasons. Number one, it is home to Jafra USA’s distribution center, which we will be leveraging on for Betterware US operations. Number two, it offers a strategic distribution location within the US. Number three, it is close to Mexico. And number four, it has a substantial Hispanic population, which is our primary target market.

According to CEO Andres Campos, the Hispanic population in the US that the company is targeting, generates a GDP that is twice that of Mexico’s GDP. Therefore, in addition to the geographic diversification, entry into the US market promises to be an enormous opportunity which could drive strong revenue growth for the company in the years ahead.

Risks to the thesis

US market entry is unsuccessful

The venture into the US market may not go according to plan, leaving the company with depleted resources and loss of trust from investors. However, judging by management’s prudent strategy thus far, this is less of a concern for now but should be monitored carefully going forward.

Debt burden

Even though the company’s balance sheet looks in good shape at present, the high net debt position could affect the company’s leverage ratio in case profitability declines in the future.

China

Manufacturing outsourced to third-party contractors in China accounted for approximately 40% of the company’s revenue last year, as per its 2023 Annual report.

Buy Betterware de Mexico

Betterware de Mexico’s management team has carefully managed their entry into the US market while also benefitting from Jafra’s existing presence there. The US market promises to be a significant growth driver for the business going forward. With shares valued at a substantial discount to peers and offering an 8% dividend yield, I believe this presents an attractive opportunity for investors to get Long this company as its growth story continues.