TayaCho/E+ via Getty Images

Late last week, Wells Fargo put out a large list of potential and logical buyout targets in the biotech sector. They focused on the midcap space for various reasons. One of the names on the report was Viking Therapeutics, Inc. (VKTX), which is on my short list of likely biotech acquisitions as well. However, I recently covered this mid-cap GLP-1 concern in this article, and I haven’t been alone (I, II) here on Seeking Alpha in reaching that conclusion.

Today, we highlight three other names on Fargo’s list that I hold in my portfolio and would make logical and strategic acquisitions for Big Pharma.

Let’s start with the gene editing concern Intellia Therapeutics, Inc. (NTLA). Wells Fargo is hardly alone in calling out the company’s potential recently. Intellia was one of 14 biotech stocks that Cantor Fitzgerald said were worth a second look in the first half of this month. Intellia Therapeutics also got some “shout-outs” from a Seeking Alpha forum around the question about which gene editing concern would successfully garner the next FDA approval.

May 2024 Company Presentation

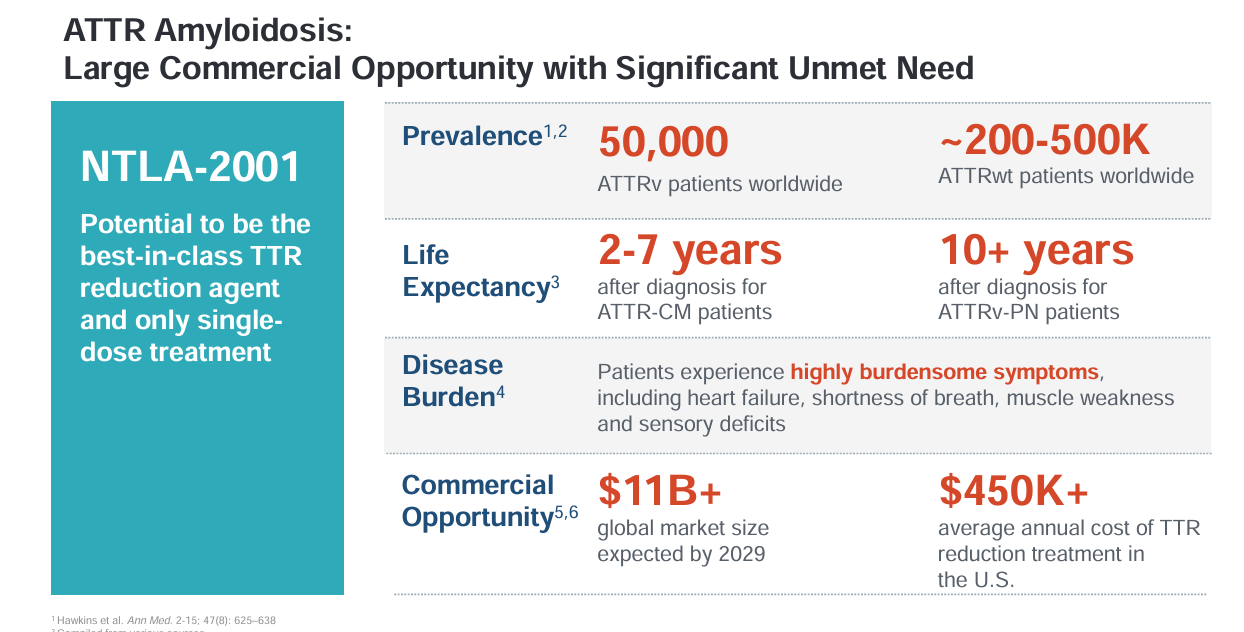

With a market cap of approximately $2.4 billion, Intellia would make a bite-size acquisition for any number of Big Pharma firms. The company’s most advanced gene editing candidate is NTLA-2001, which is being evaluated for the treatment of transthyretin (ATTR) amyloidosis, an affliction that impacts 250K to 550K individuals globally. There are several approved products on the market to treat ATTRv-PN and one to treat ATTR-CM. However, they all require lifetime dosing. NTLA-2001 is targeting both variations of ATTR and has the potential to be a one-time curative solution. Management has put this potential market at north of $10 billion by FY2029.

November Company Presentation

The company just kicked off a pivotal Phase 3 study ‘MAGNITUDE’ to evaluate NTLA-2001 to treat ATTR-CM. Just over 750 individuals will be evaluated in this trial. The first person in the program has recently been dosed. The company is currently in the “preparation” stage for a Phase 3 study to evaluate the candidate against ATTR-PN. This program is partnered with Regeneron Pharmaceuticals, Inc. (REGN) which shares 25% of the costs and profits of this effort. The company has a cash runway well into 2026 and if all goes well, NTLA-2001 could be approved in 2027. The potential size of the ATTR market could logically draw the interest of a larger suitor.

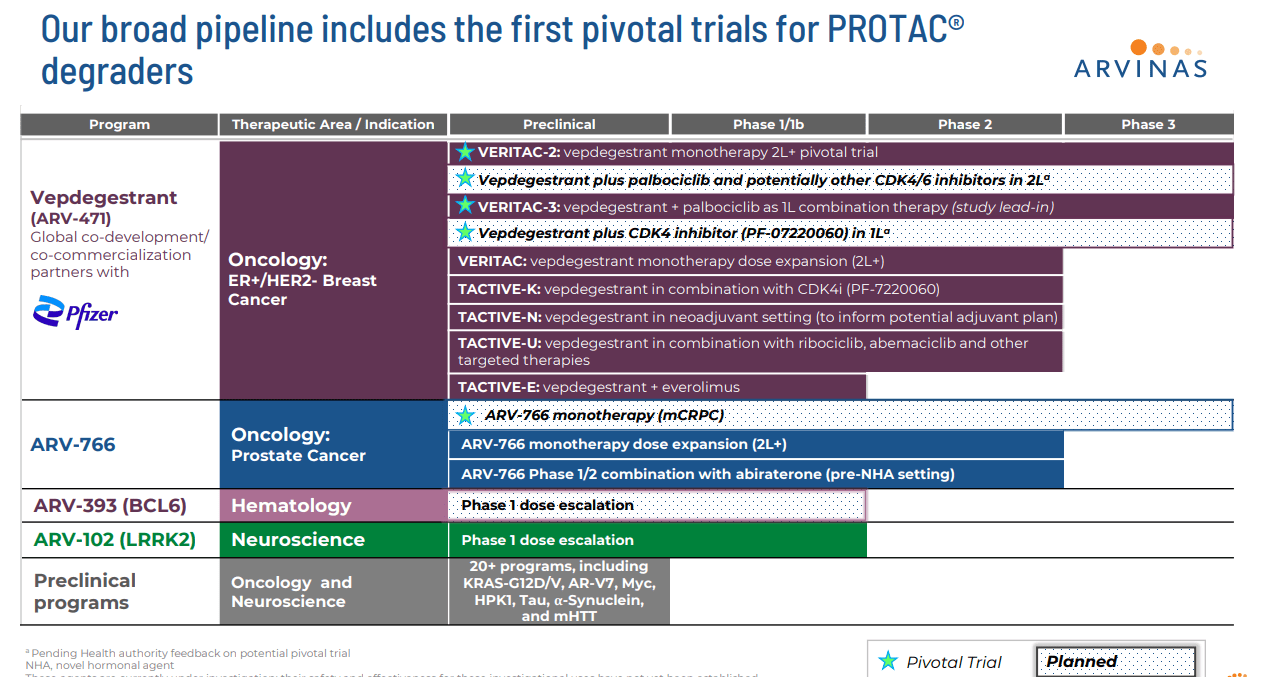

Arvinas, Inc. (ARVN) also made Wells Fargo’s list. This clinical-stage developmental firm has almost the identical current market cap ($2.4 billion) as Intellia and also has funding in place to fund all planned activities well into 2027. The company has several candidates in its pipeline that came off its proprietary PROTAC® platform. This technology allows Arvinas to produce protein degraders to harness an individual’s own natural protein disposal system to degrade and remove disease-causing proteins.

The company’s most advanced pipeline asset is a compound called Vepdegestrant or ARV-471. This is an estrogen receptor [ER] targeting PROTAC® protein degrader that is currently being evaluated to treat women with locally advanced or metastatic ER-positive/human epidermal growth factor receptor 2 (HER2) negative (ER+/HER2-) breast cancer.

January 2024 Company Presentation

As can be seen above, the company also has several other compounds in its pipeline, some of which are entering Phase 3 development. Oncology has been one of the hottest areas for M&A for years and will likely remain so given the global oncology market is estimated to be $220 billion in 2024.

ARV-471 is being evaluated as both a monotherapy and in combination with CDK inhibitor IBRANCE from Pfizer Inc. (PFE). Importantly, Pfizer has put its money where it is mouth is with this partnership, paying $650 million upfront with a $350 million equity investment within this collaboration deal. Profits and costs are shared equally within this arrangement as well. Two Phase 3 studies, VERITAC-2 and VERITAC-3 are currently enrolled, the first of which should be completed by the end of 2024.

Cantor Fitzgerald called out Arvinas as one of its top biotech targets in the oncology space in March of this year. The ARV-471/Ibrance combination therapy also garnered Fast Track status in February of this year as well. This combination therapy showed good Phase 1 results late in 2023. Obviously, Pfizer would be the most logical suitor for Arvinas given their deep partnership. Novartis AG (NVS) also entered into a license agreement with Arvinas last month that involved Novartis paying a $150 million upfront payment, it should be noted.

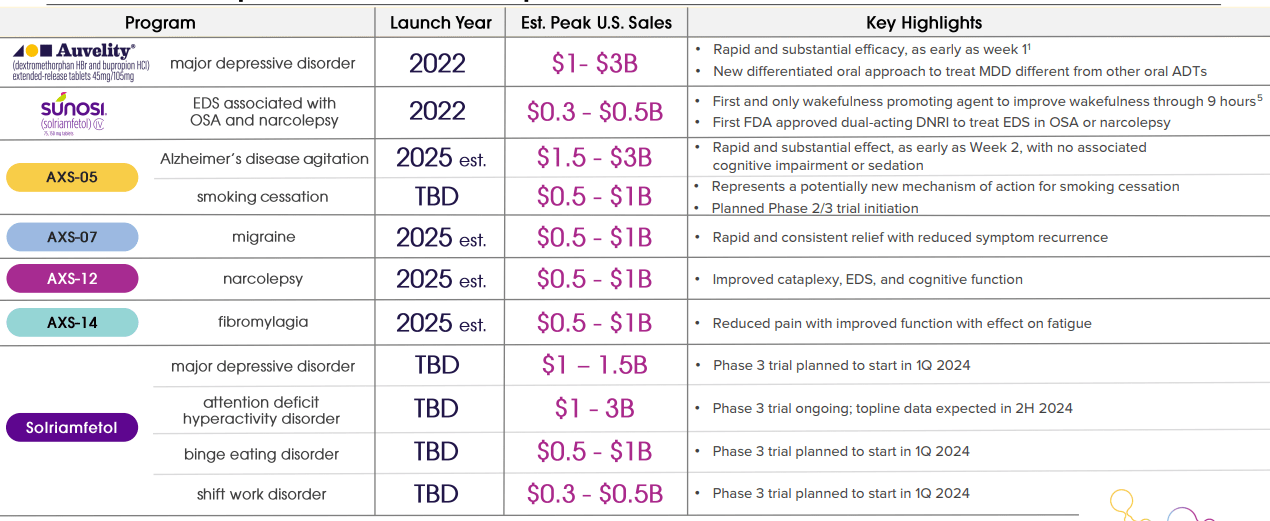

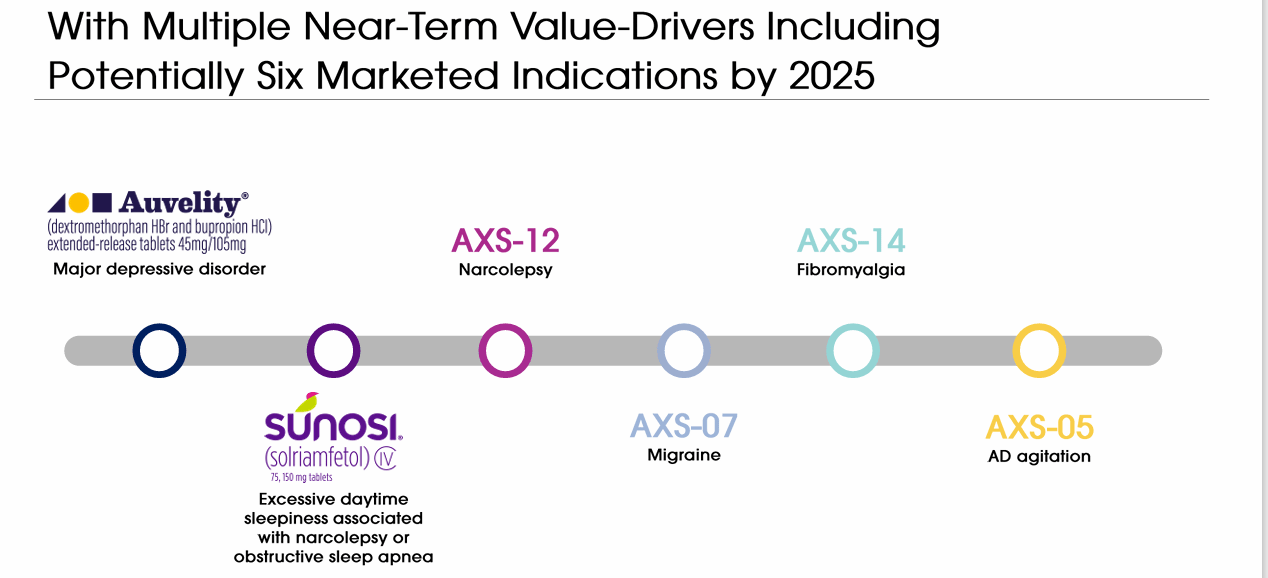

Moving over to the CNS (Central Nervous System) space, we will end with Axsome Therapeutics, Inc. (AXSM) which is a bit larger than our first two names with just over a $3.5 billion market capitalization. And unlike Arvinas or Intellia, Axsome is a commercial-staged biopharma with two drugs already on the market. Both of which were approved in 2022. One is Sunosi, which treats sleep disorders linked to narcolepsy and obstructive sleep apnea. The other is Auvelity that is green-lighted to treat major depressive disorders or MDD. Auvelity net products sales were up 240% in the first quarter on a year-over-year basis to $53.4 million. Sunosi revenues were up a tamer 64% from the same period a year ago to $21.6 million.

February 2024 Company Presentation

In addition, the company has several late-stage compounds in development for other CNS disorders, as can be seen above. The company’s most likely next FDA approval is AXS-12 that is targeting narcolepsy, given that the compound hit its primary endpoint in a Phase 3 trial in late March. The company also has promising late-stage candidates targeting migraines (AXS-07) and agitation (AXS-05) associated with Alzheimer’s. If all goes well, the company could have half a half dozen approved drugs on the market by 2025 or soon thereafter.

February 2024 Company Presentation

Given the depth of Axsome’s product portfolio and pipeline, it would be surprising if some larger pharma concerns didn’t at least “kick the tires” around a purchase. After Bristol Myers Squibb Company’s (BMY) acquired Karuna Therapeutics (KRTX) for $14 billion near the end of 2023, Axsome Therapeutics was on Cantor Fitzgerald’s short list of potential CNS deals. Axsome ended the first quarter with just over $330 million in net cash on its balance sheet. Management stated within the quarterly earnings press release that this should be sufficient to get the company to profitability without doing an additional capital raise.

An acquisition of one of your portfolio holdings with a big buyout premium is always a great way to start the trading day. However, purchases are few and far between, so it is important that an investor like the company as a standalone entity as well. Two weeks ago, Cytokinetics, Incorporated (CYTK) would have been on my top 10 potential biotech buyout list. However, last week the company’s CEO decided to go it alone and then the firm botched a large capital raise, triggering a significant decline in the stock. I covered these events in this article last week.

The three companies highlighted in this article I own mostly via covered call holdings. I would love to wake up one day seeing one of them acquired with a 90% buyout premium, but I also like their longer-term prospects should that not occur.