Egeris/iStock Editorial via Getty Images

Investment Thesis

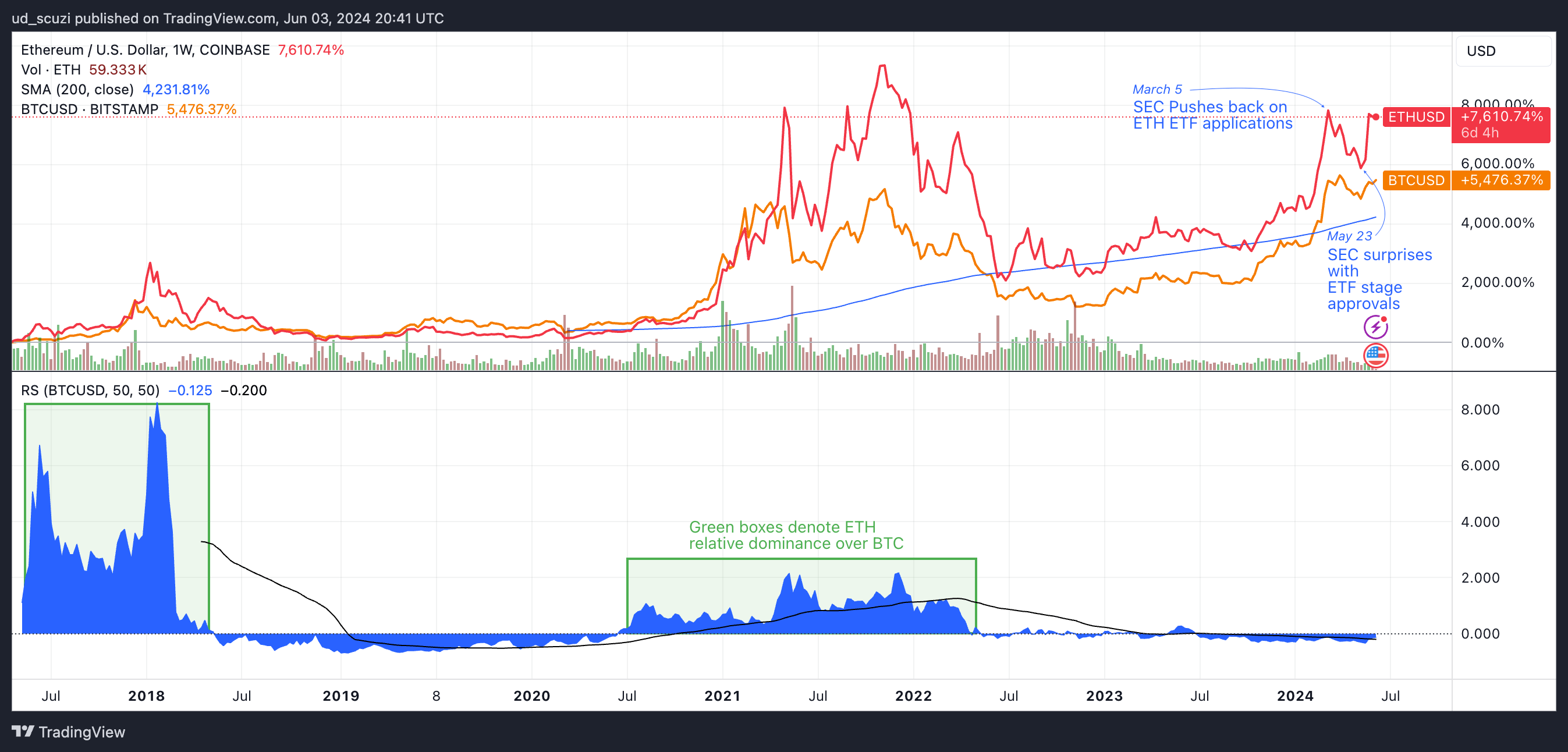

While Bitcoin (BTC-USD) has been a big beneficiary in the wake of the SEC’s approvals on bitcoin etfs, its altcoin peer, Ethereum (ETH-USD), has been trailing in relative performance so far this year, as seen in the chart below.

Exhibit A: Relative performance of Ethereum vs Bitcoin since 2017, weekly (TradingView)

In Exhibit A above, I see how Ethereum surged in early March only for investors to be suddenly pessimistic after the SEC pushed back on the Ethereum-based ETF applications by a few asset management firms. That led to the likelihood of the firms securing approvals for their ETFs getting slashed to just 30%.

The odds drastically changed a couple of weeks ago when the SEC suddenly amended rules to permit the listing of Ethereum ETFs on U.S. exchanges. This takes all Ethereum applications one step closer to securing approvals to finally begin trading on U.S. exchanges and for Grayscale’s Ethereum Trust Fund (OTCQX:ETHE) to convert to a fully-functional ETF.

This move by the SEC has created the perfect conditions for a rally to continue in Ethereum and the ETHE fund, which could see Ethereum retest its all-time highs struck in 2021. I recommend buying ETHE.

About Grayscale’s Ethereum Trust Fund

The Ethereum Trust Fund, whose assets are managed by Grayscale, the largest crypto asset management firm in the world, The ETHE fund aims to offer investors exposure to Ethereum by investing the fund’s assets directly into it. At the time of writing this research note, ETHE is still the only fund currently available to investors that offers investors exposure to Ethereum while avoiding the housekeeping needs of buying and holding Ethereum directly.

Grayscale achieves its purpose of offering investors exposure to Ethereum by tracking CoinDesk’s Ether Price Index.

The fund’s shares still operate as an over-the-counter instrument, and Grayscale, via NYSE Arca, filed its 19b-4 form last year to convert its trust fund into an ETF instrument. In ETHE’s case, Coinbase provides the necessary custodial services, holding Ethereum on behalf of the ETHE fund that is used to back the fund’s assets.

As noted in the previous section, the SEC has recently approved Grayscale’s 19b-4 forms as well as the 19b-4 forms of at least seven other Ethereum ETFs by Grayscale’s peers, including BlackRock, Fidelity, VanEck, etc.

ETHE’s current peer ETF ecosystem commentary

I had mentioned earlier how most asset management firms that have filed for their respective Ethereum ETF applications have gotten one step closer after the SEC approved the 19b-4 forms. This leaves the final stage remaining, where each fund’s S-1 must be approved for the respective Ethereum to start trading on exchanges.

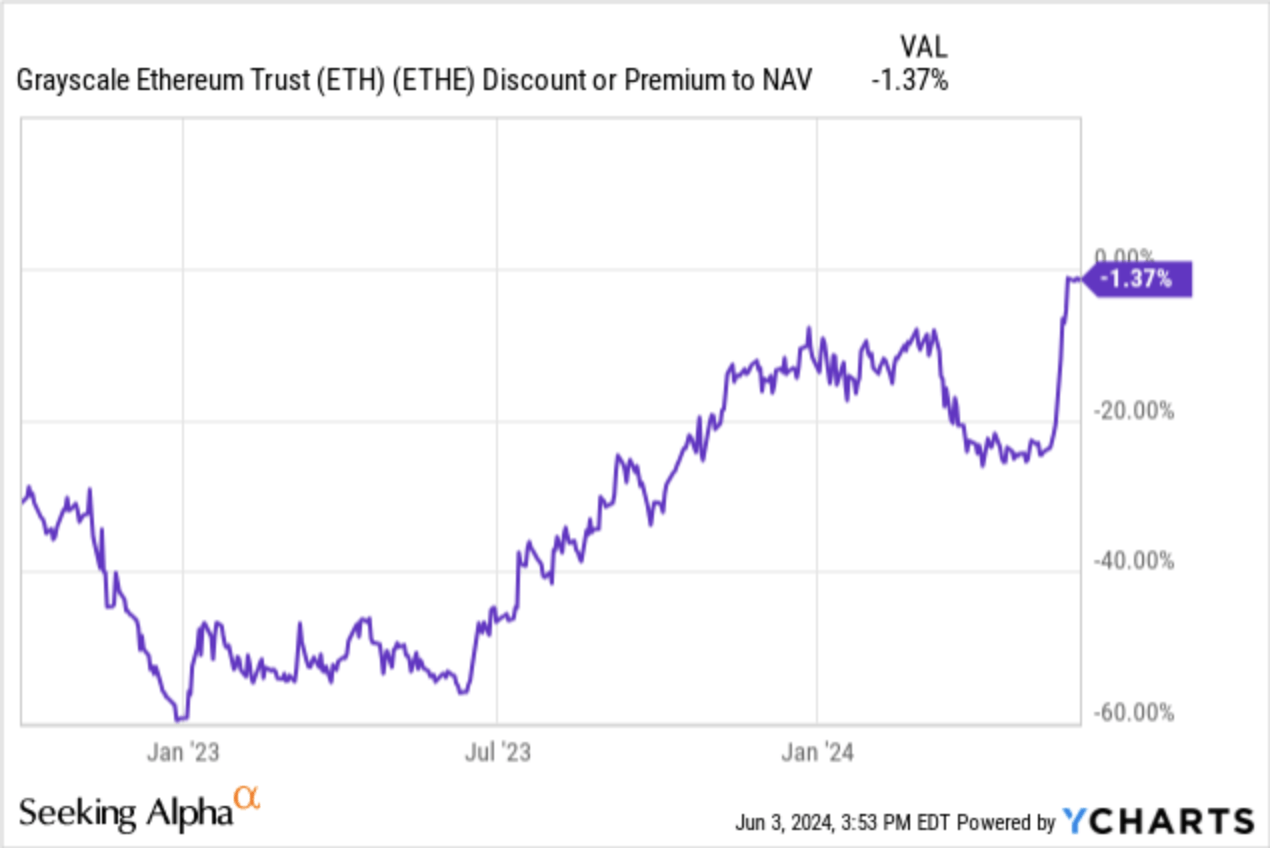

The same can be assumed for Grayscale’s ETHE, which will start trading as an ETF instrument after final approval. I believe this is just a formality, and the final approval could be done by the SEC as early as this month, per some projections. This is also reflected in the ETHE fund’s premium/discount metric, which still points to the fund trading at a 1.4% discount to the fund’s (NAV) Net Asset Value as seen in Exhibit B. As we get closer to approval, I expect demand for the ETHE to increase, with the fund eventually trading either at par or at a premium to its NAV.

Exhibit B: Grayscale Ethereum Trust Fund trades at a 1.4% discount to the fund’s Net Asset Value (YCharts)

Post approval, I expect some outflows from the ETHE fund by investors who have been securing positions in ETHE as part of their arbitrage play in anticipation of the final approvals of ETHE and its peer ETFs. Per the fund’s current prospectus, ETHE has a fund management fee of 2.5%. I anticipate all of ETHE’s peers will list their respective expense ratios far lower than the current ETHE’s fund management fee to attract capital, just as I pointed out in my coverage of the iShare Bitcoin Trust ETF (IBIT).

Grayscale is quite aware of this and anticipates elevated levels of outflows, but it plans to address that by launching Grayscale Ethereum Mini Trust and has already filed the S-1 for that. The seed capital for the mini ETH ETF will be allocated from the ETHE, per the prospectus, thus giving existing ETHE investors access to the mini ETH ETF in addition to the shares held in the ETHE fund.

Assessing demand for underlying Ethereum

I had mentioned earlier in Exhibit A how Ethereum had been relatively underperforming Bitcoin this year. But there are a couple of dynamic changes in the market that I believe point to favorable conditions for Ethereum and the ETHE fund.

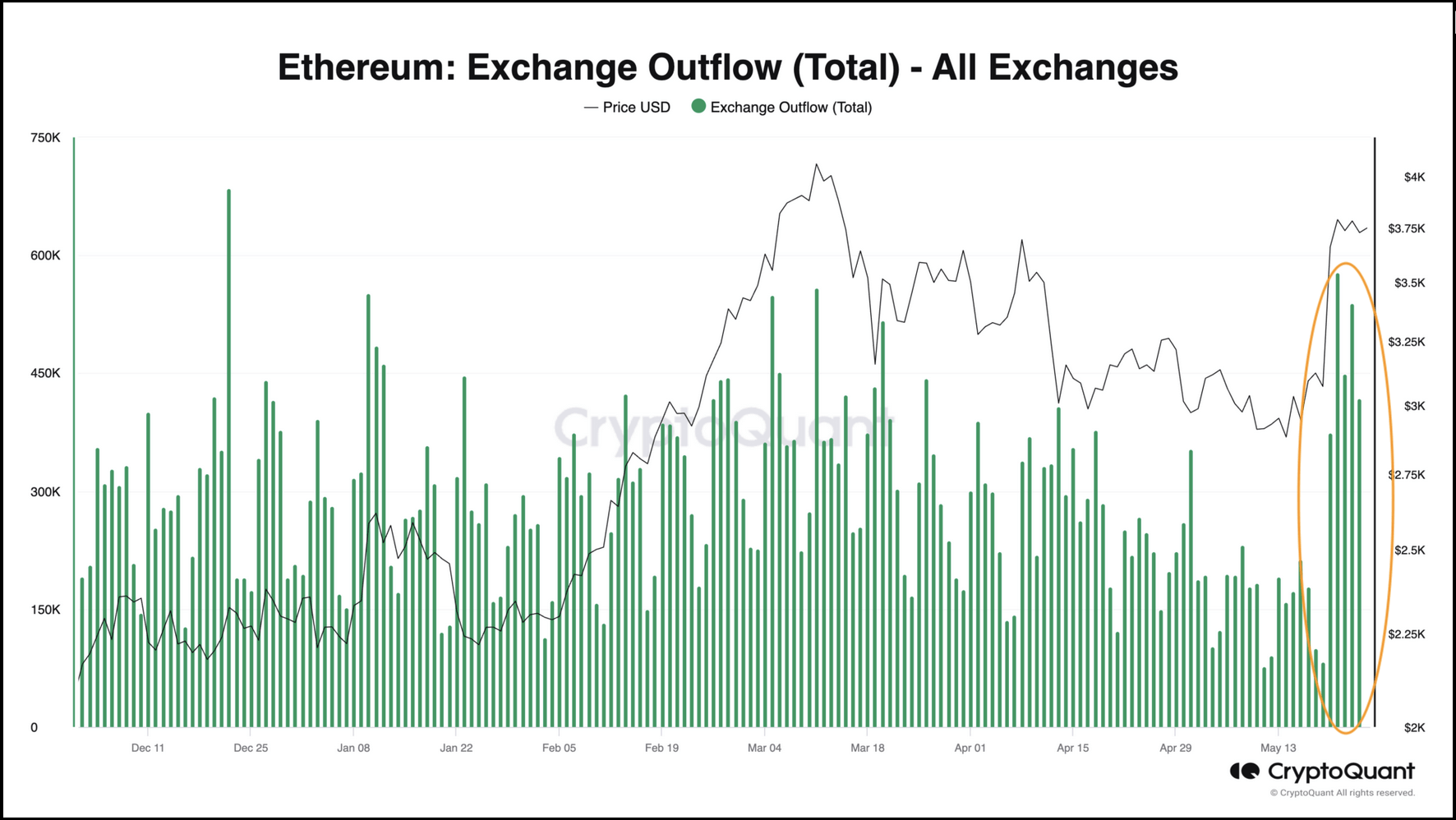

First is the outflow of digital assets, such as Ethereum, out of exchanges and usually into digital wallets. I observe this by borrowing a chart from CryptoQuant that illustrates the flow of Ethereum out of exchanges, as shown in Exhibit C.

Exhibit C: Outflow of Ethereum from Exchanges (CryptoQuant)

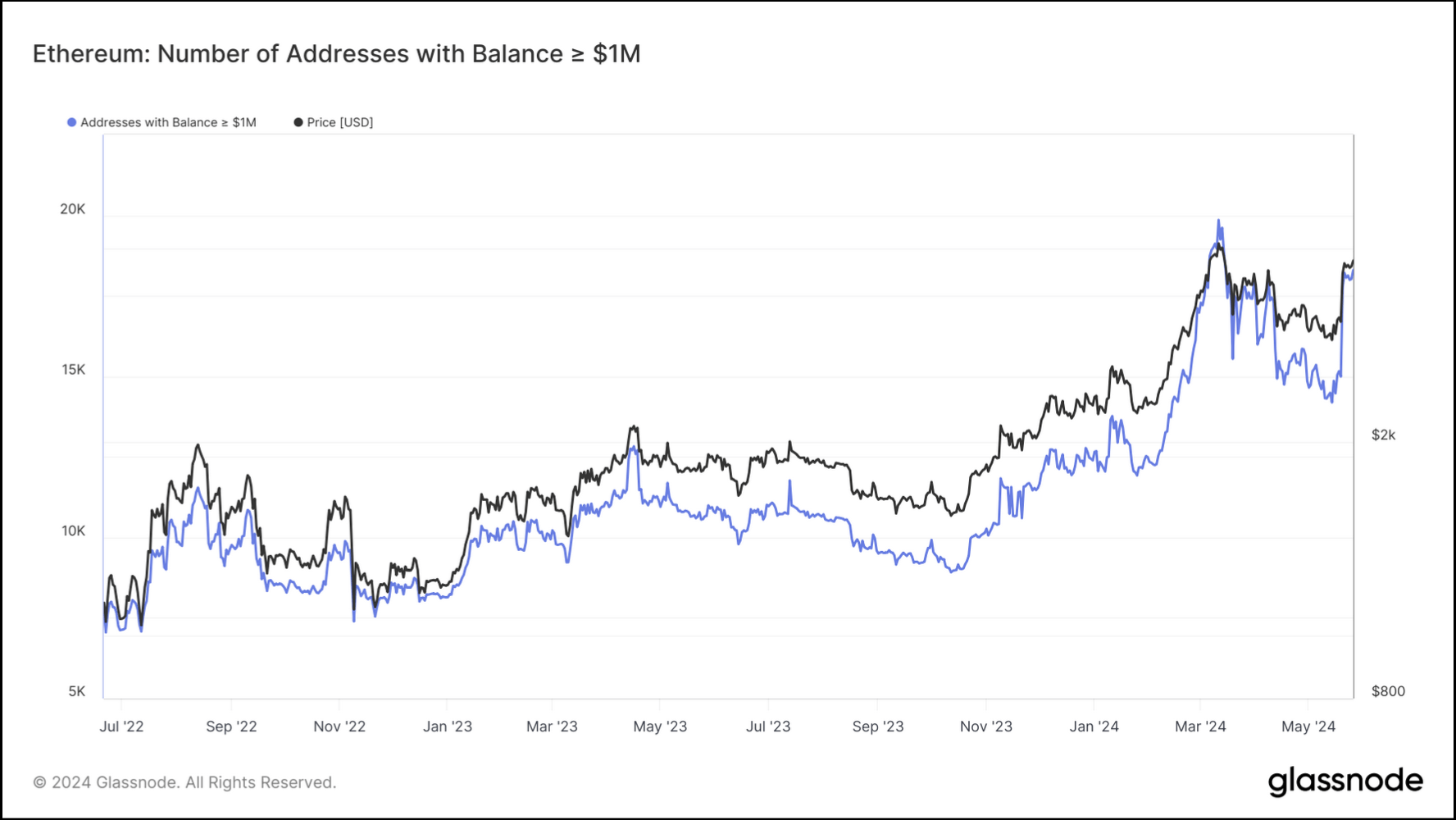

I believe the trends illustrated in Exhibit C imply favorable trends in Ethereum to follow as investors move more Ethereum from exchange to their digital wallets. This is usually a sign that crypto investors holding Ethereum would prefer holding on to their Ethereum in their digital wallets rather than having it ready to trade on the exchanges. This deduction is also corroborated by the chart borrowed from Glassnode, as seen in Exhibit D below, which shows the number of wallet addresses holding at least $1 million in Ethereum.

Exhibit D: Number of Wallet addresses holding >$1M in Ethereum (Glassnode)

My takeaways from both the charts combined in Exhibits C & D point to crypto markets with reduced Ethereum supply. As more investors get bullish again about Ethereum, they move their assets to digital wallets, thus reducing the supply of Ethereum. The diminished supply of Ethereum creates supply/demand imbalances, which should create upward price pressures-factors that imply bullishness for Ethereum and ETHE as a result. Based on the sentiment that I see, Ethereum could easily continue on its current trajectory closer towards retesting its ATHs (all-time highs).

Staked Ethereum to be excluded from ETFs

There are many differences between Ethereum and Bitcoin that investors should be aware of, but for the purpose of this note, staking is something that will be key in impacting Ethereum ETFs over the long term.

First, a quick primer on Ethereum and how it works. Ethereum is the largest digital currency by market cap, and is an alternative to Bitcoin. Bitcoin’s design characteristics resemble those of fiat currencies; hence, it trades more as a medium of exchange and store of value. On the other hand, Ethereum’s modular design philosophy positions the altcoin closer to relative usability in terms of user applications. Smart contracts and Staking are some of those features, and the Ethereum blockchain network became more serious about staking after it switched its reward mechanism to Proof-of-Stake in 2022. Simply put, staking is quite similar to term deposits, where Ethereum holders “stake” some of their holdings and lock them up while earning rewards through the lock-up period.

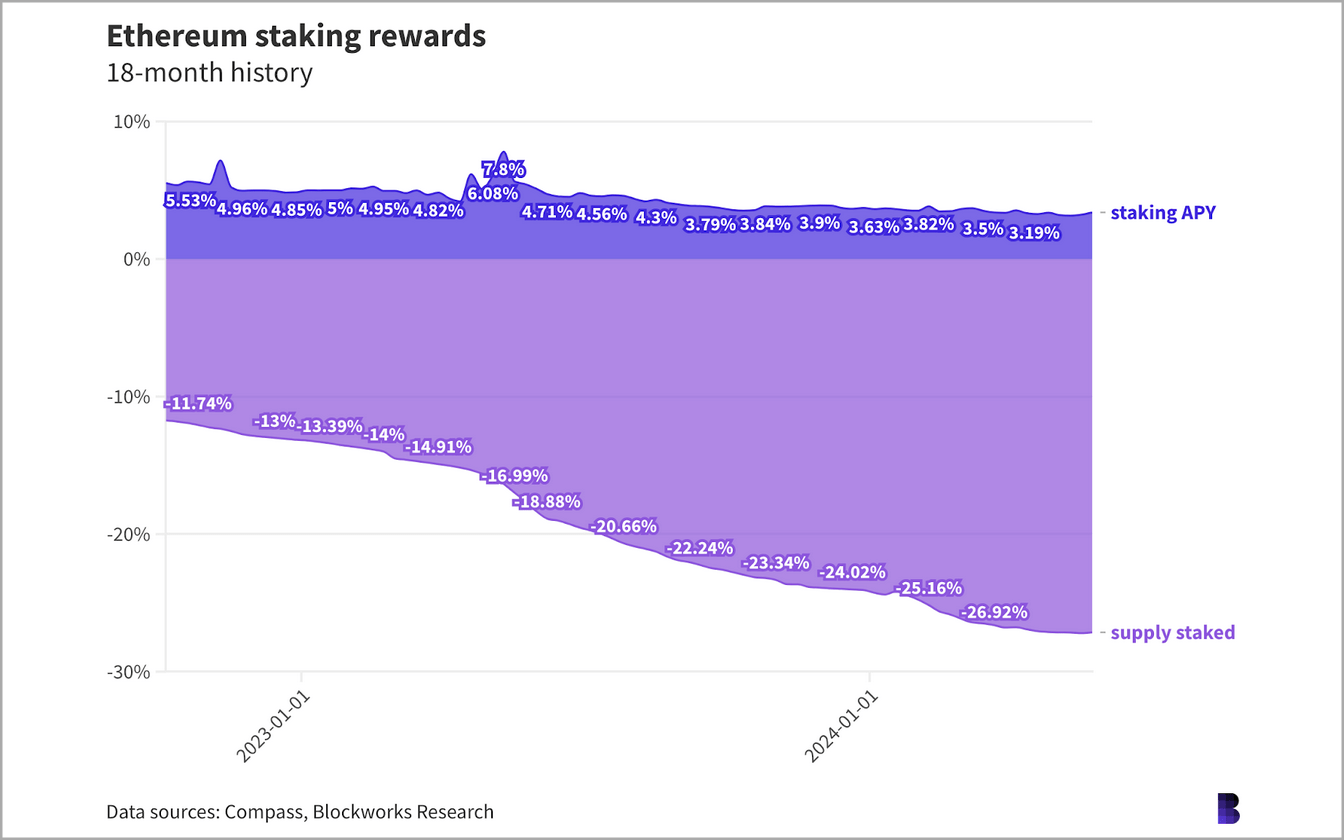

The chart in Exhibit E highlights the staking APY yield versus the percent of supply staked.

Exhibit E: Ethereum staking rewards in terms of APY over the past 18 months (Compass, Blockworks Research)

The chart shows that as of last month, ~27% of Ethereum’s supply was staked, almost doubling from a year ago. At the same time, Ethereum pays any crypto investor a blended APY of ~3.4% to stake their Ethereum holdings. With 27% of the supply staked, this has a meaningful impact on the supply of Ethereum.

Especially after ETF applications were updated by most asset management firms to exclude any staked supply of Ethereum from their holdings, The SEC regards staking as a security and has set enough precedents to act on its opinion in the past. As of now, to me, this indicates investors holding Ethereum would hold a performance edge over investors who allocated their capital towards Ethereum ETFs such as ETHE. But a lot can change between now and the eventual S-1 approvals for Ethereum ETFs.

Therefore, this would be one potential area to watch for long-term impact.

Takeaway

Regardless of the long-term impacts that I alluded to earlier, I believe there is enough hype that has been generated by the recent SEC approvals that indicate investors are closer than ever to start investing and trading in Ethereum ETFs without the need to manage digital wallet infrastructure. Long-term implications are currently uncertain for Ethereum ETFs with respect to the exclusion of staked Ethereum holdings, but on a short-term basis, I believe the sentiment is strong enough for ETHE to move higher and possibly even retest its all-time highs.

For now, I recommend a Buy on ETHE.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.