Just_Super

Cyclical commodity producer in a downturn

Albemarle Corporation (ALB), many would argue is in a cyclical downturn as the consumer’s ravenous appetite for EVs has seemed to quell. On top of that, arguments that different battery chemistries may be popping up to challenge lithium as a cathode material have also been ringing bells.

My last article on the company was in March of this year. Albemarle came out with a cost-cutting program in order to find a solution to return to positive free cash flow. While on the surface the company looks to be a good deal based on trailing numbers, new forward revisions are less than appealing.

If you believe in the lithium story, there’s no better time than the present to get involved in a commodity producer when their numbers look the bleakest. The worst time is at the top of a cycle when the return on invested capital [ROIC] appears phenomenal.

The biggest problem I see with the above thesis, which is a popular commonly held belief with some of history’s best-value investors, is that we do not understand the lithium cycle. Lithium has never been in demand on such a large scale as it is today. Luckily for us, Albemarle has recently floated a new preferred issue (NYSE:ALB.PR.A) which is mandatorily convertible to common in the future. This article will take a look at which is a better deal at today’s prices, the common or the preferred.

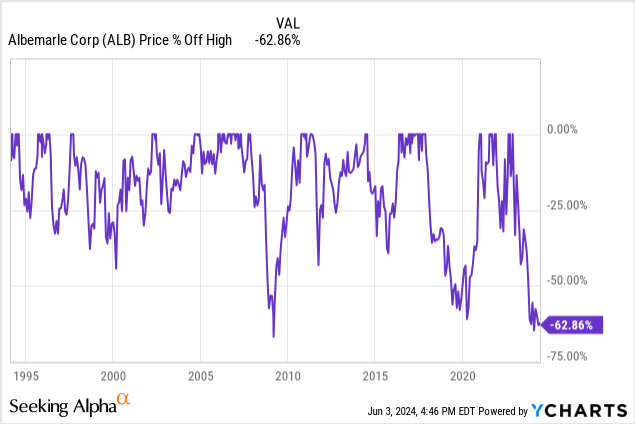

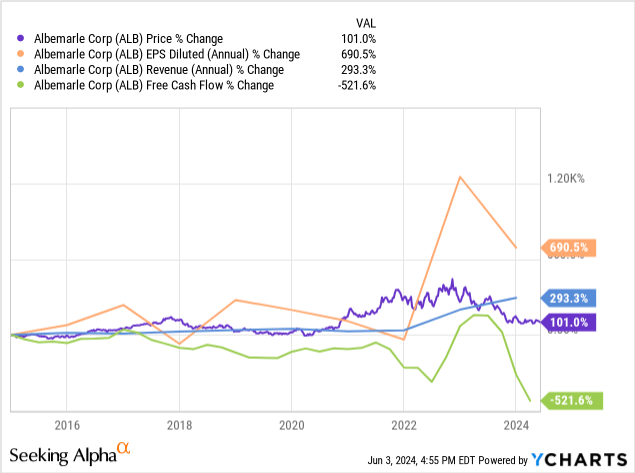

Percent off high

I have been in and out of this stock over the years. I had been lucky to have timed my top of the commodity cycle sell during Covid when the market was elated with anything EV-centric. -62.86% off the all-time high has been a heck of a downfall. Should we expect the one major US producer of lithium to bounce back when the EV story picks back up?

Details on the preferred

Each share of our Mandatory Convertible Preferred Stock has a liquidation preference of $1,000 (and, correspondingly, each Depositary Share represents a liquidation preference of $50). Unless earlier converted, each share of our Mandatory Convertible Preferred Stock will automatically convert on the second business day immediately following the last trading day of the final averaging period (as defined below) into between 7.6180 and 9.1400 shares of our common stock, subject to anti-dilution adjustments. The number of shares of our common stock issuable on conversion will be determined based on the average VWAP (as defined herein) of our common stock over the 20 trading day period beginning on, and including, the 21st scheduled trading day prior to March 1, 2027, which we refer to herein as the “final averaging period.” At any time prior to March 1, 2027, a holder of 20 Depositary Shares may cause the bank depositary to convert one share of our Mandatory Convertible Preferred Stock, on such holder’s behalf, into a number of shares of our common stock equal to the minimum conversion rate of 7.6180, subject to anti-dilution adjustments. If a holder of 20 Depositary Shares causes the bank depositary to convert one share of our Mandatory Convertible Preferred Stock, on such holder’s behalf, during a specified period beginning on the effective date of a fundamental change (as described herein), the conversion rate will be adjusted under certain circumstances, and such holder will also be entitled to a make-whole dividend amount (as described herein).

Hypothetical pref vs. equity scenarios

So here is my attempt to break down the scenario of buying the pref versus the common from here until the conversion date. These assumptions are based on my previous article price target.

| Stock | shares | cost | dividend |

| ALB.PRA | 20 | 1020 | 6.99% |

| ALB | 9.02 | 1020 | 1.40% |

Firstly, to get a round lot of 20 pref shares of the ALB.PR.A, you currently need to invest $1,020 as the shares are selling at a slight premium.

Based on recent presentations by Albemarle, I pegged future fair value FY 2027 at $263.87/share. While this is based on aspirational cash flows, for the sake of this comparison, that will be our terminal value.

Months from June 11th until the exercise date of March 1, 2027

total return of pref with dividends

| year | months | dividend 6.99% |

| 2024 | 6 | 3.495 |

| 2025 | 12 | 6.99 |

| 2026 | 12 | 6.99 |

| 2027 | 3 | 1.7475 |

| total | 33 | 19.22% |

| conversion rate | times terminal value 263.87 | price return on $1020 | total return with 19.22% dividend |

| 7.61 | 2008.05 | 96.87% | 116.09% |

| 9.14 | 2411.77 | 136% | 155.22% |

total return of common with dividends

Please note, although Albemarle is a dividend aristocrat, known for raising the dividend consistently, I am going to err on the side of caution and put their dividend increases as negligible token raises that do not add anything to the total pie in this current cash crunch.

| year | month | dividend 6.99% |

| 2024 | 6 | 0.7 |

| 2025 | 12 | 1.4 |

| 2026 | 12 | 1.4 |

| 2027 | 3 | 0.35 |

| total | 33 | 3.85 |

The same $1020 got us 9.02 shares initially at this outset, using the same terminal value of $263.87 would result in a total end value of $2,380, a return of 133%. Adding in the 3.85% total dividend returns would get us to a max total return of 136.85%. The common total return beats the low-end conversion pref rate of 116% but is under the top-end total return of 155%. The average total return in the pref scenario is 135.5%, basically equivalent to the total return prospects of the common.

Using the pref as a hedge makes more sense to me at the moment as that dividend can be reinvested elsewhere to de-risk some of the investment. However, tax implications on the higher dividend rate will hurt the actual after-tax total return on the pref if owned in a non-tax advantaged account.

Share price performance

This is a classic case of a capital-intensive, inefficient business that has not yet matured. The income statement has been telling one story and the cash flow statement another. Once the company took on lithium as its primary business, CAPEX consistently outpaced cash from operations as lithium mines ramped up.

Many getting into this sector with junior miner bets must keep in mind that to complete the lithium supply chain, you also have to refine the lithium carbonate or hydroxide to an end product that is battery grade. Some projects may contain lots of lithium, but never be feasible due to the tailings. It has proven to be such a difficult business that I personally wouldn’t invest in any lithium company outside of the largest players, notably Sociedad Quimicia y Minera (SQM) and Albemarle. I personally don’t invest in Chinese stocks, but Ganfeng (OTCPK:GNENF)(OTCPK:GNENY) is the other large player that may be worth a look along with a handful of other producing miners.

As I consistently see adverts on YouTube pumping pre-production lithium stocks, I say stay away. The production-to-refinement timeline is so long and so capital intense that it is similar to the artificial intelligence play, only the largest survive.

My 2027 price targets

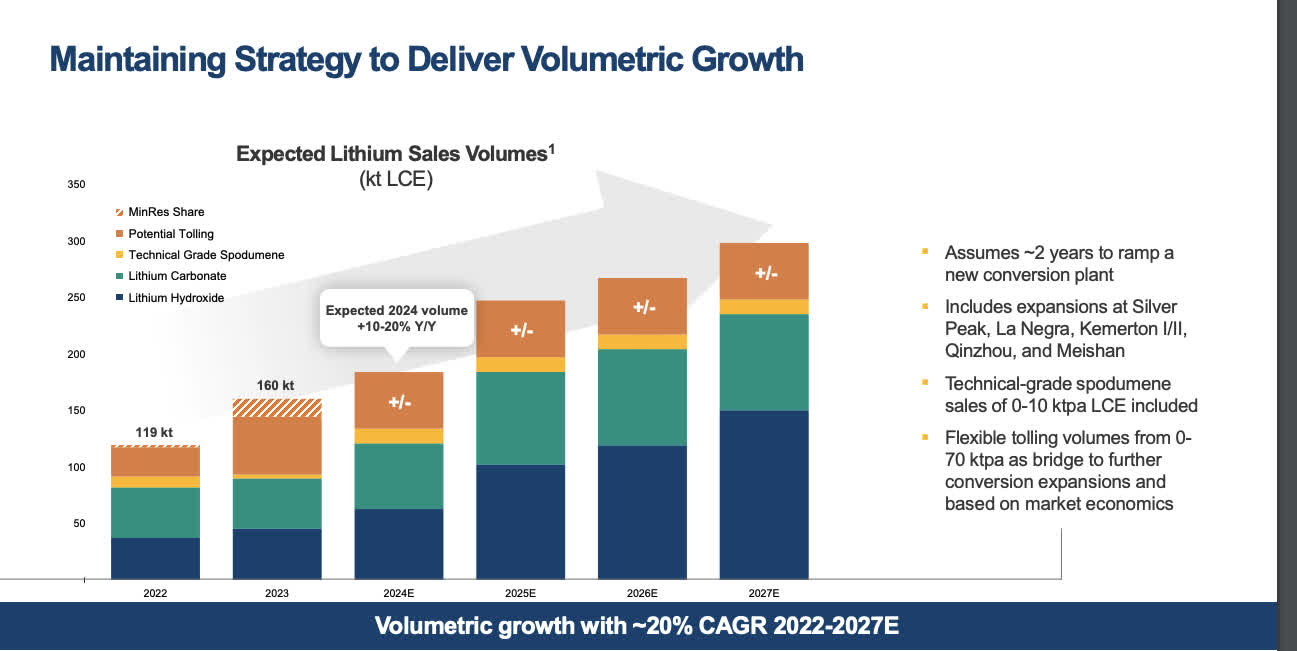

Albemarle Annual presentation FY 2023

Looking over the CAPEX targets going forward to 2027 combined with net income trends based on Albemarle revenue projections and margins by 2027, I came up with the following in my previous article:

- A + B : 2027 Net income + Depreciation and Amortization : $4.34 Billion

- Minus C :2027: CAPEX $2.229 Billion

Using an Owner Earnings model with :

A+B-C / RFR, with A being the equivalent modeled net income, B being 2027 D&A, and C being CAPEX, we would have A+B= $4,340-$2,229= $2,111 million free cash flow. Divided by the current risk free rate of 5% gets us to a $42.22 Billion fair market cap. Let’s also assume the convertible pref adds at least 10% more shares to the current 117 million, thus 128 million shares outstanding in 2027. 42,220 market cap/128 million shares could get us to a future fair intrinsic value of $329.84/share.

Being that Benjamin Graham and Warren Buffett as described in the Warren Buffett Way would not want to pay more than 80% of intrinsic value, I would peg 2027 future value at $263.87/share should Albemarle be able to execute.

Most recent quarter earnings, comments and guidance

investors.albemarle.com

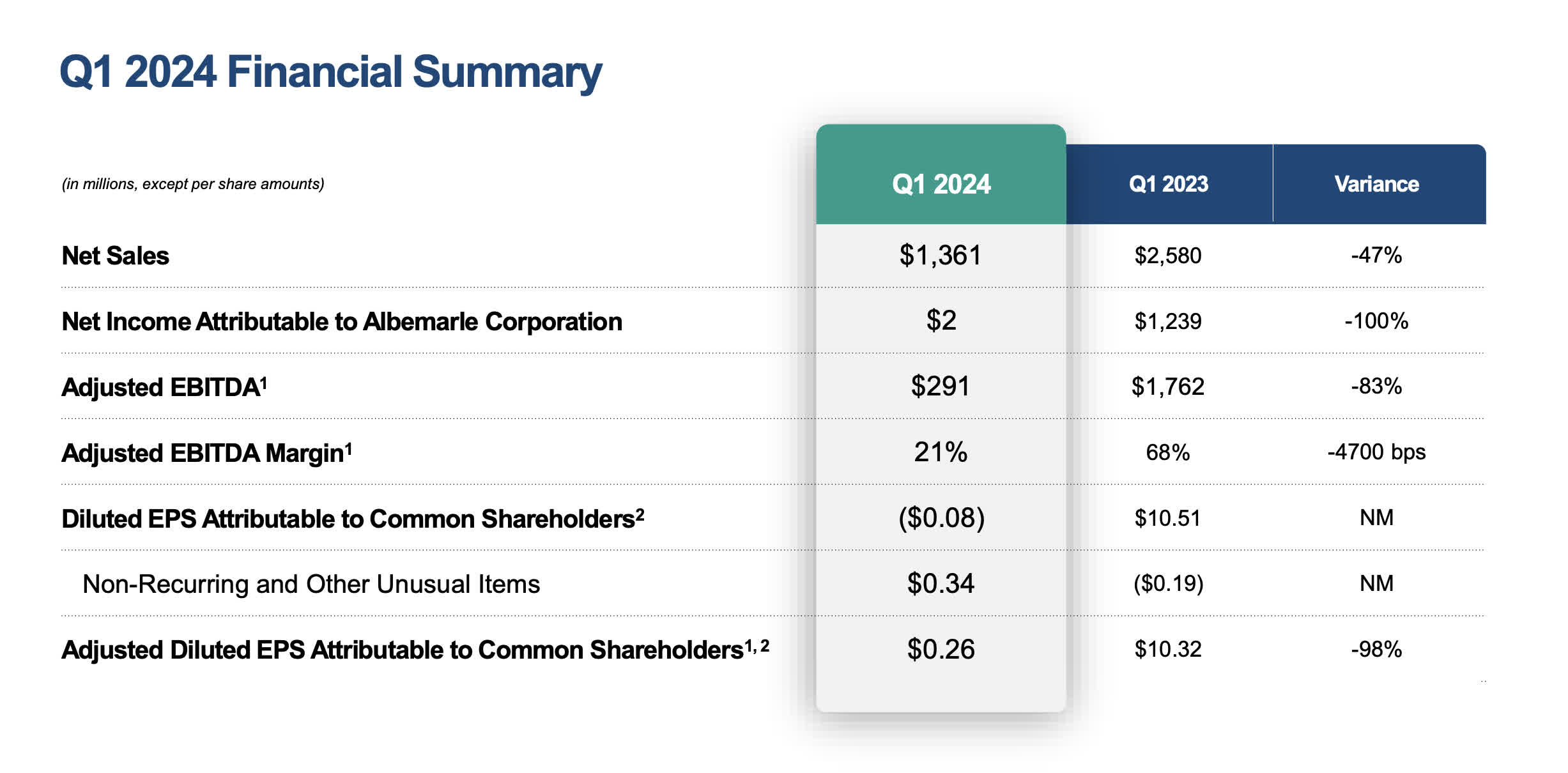

This is the quarter where Albemarle is commencing some of the cost-cutting I mentioned in the previous earnings guidance from the FY 2023 presentation. The Q1 24 presentation shows a decimation in nearly every category. -47% revenue is the biggest one, showing that the demand and price for lithium are both taking a toll. Adjusted EBITDA margin is -47% off the same time last year and the company has now posted the first negative EPS print in a while.

This is the bottom of the lithium cycle, the dreariest moment[hopefully] in the history of lithium. I say the history because the history is so short. Lithium has never been mined at this scale and never had a demand use case that rivaled other forms of energy-related commodities. The truth is, none of us know what the real lithium cycle looks like.

investors.albemarle.com

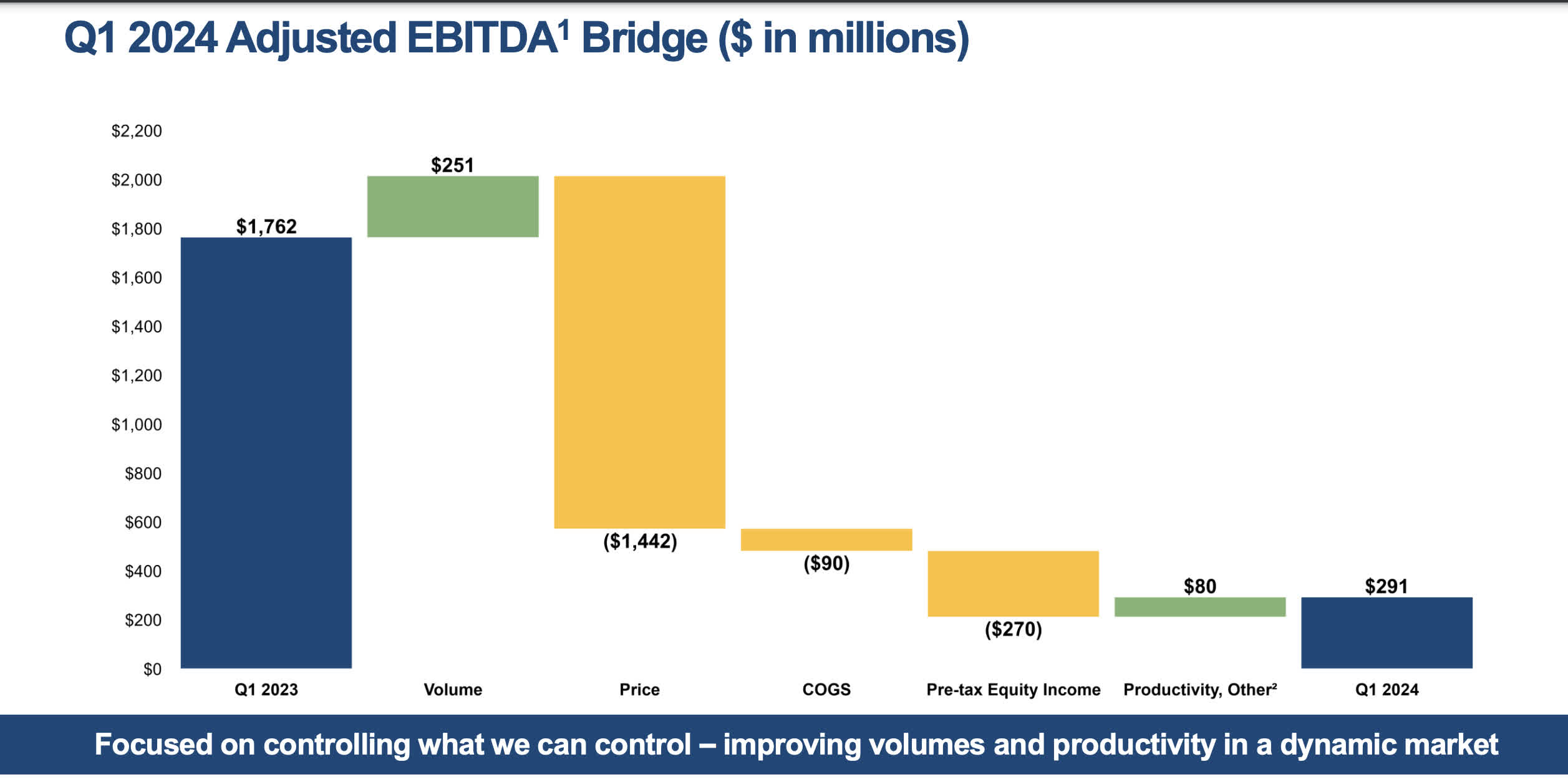

Adjusted EBITDA margin data is really bad compared to the year prior. The main take away here is the quote at the bottom of the page:

Focused on controlling what we can control-improving volumes and productivity in a dynamic market.

That is one very downtrodden statement from an investor relations presentation, which tend to be overly optimistic. I appreciate the candor and again, in a cyclical commodity space, the best opportunities can be when the numbers look the worst. I can’t imagine them getting much worse than this, but buyers of the stock need to keep checking in, caveat emptor.

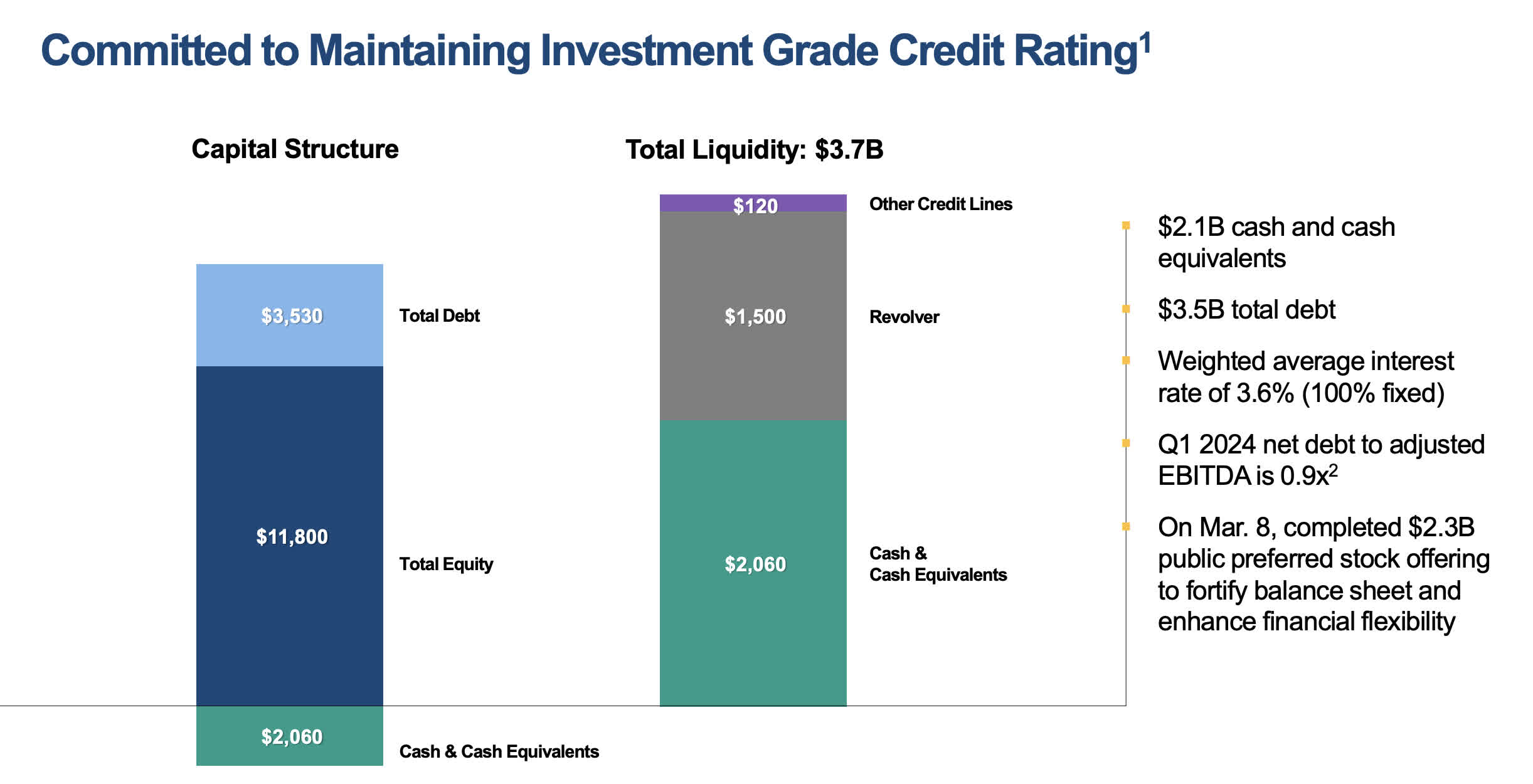

Balance sheet

investors.albemarle.com

As noted in the right-hand column, the company completed a $2.3 B capital raise via the preferred stock offering looked at in this article. The cash from the offering represents the lion’s share of the current company’s liquidity. Albemarle is not heavily indebted with only about a 31 % debt-to-equity ratio. The preferred convertible is a nice trick used to maintain the investment grade credit rating as it will get lumped into the equity versus debt side of the balance sheet.

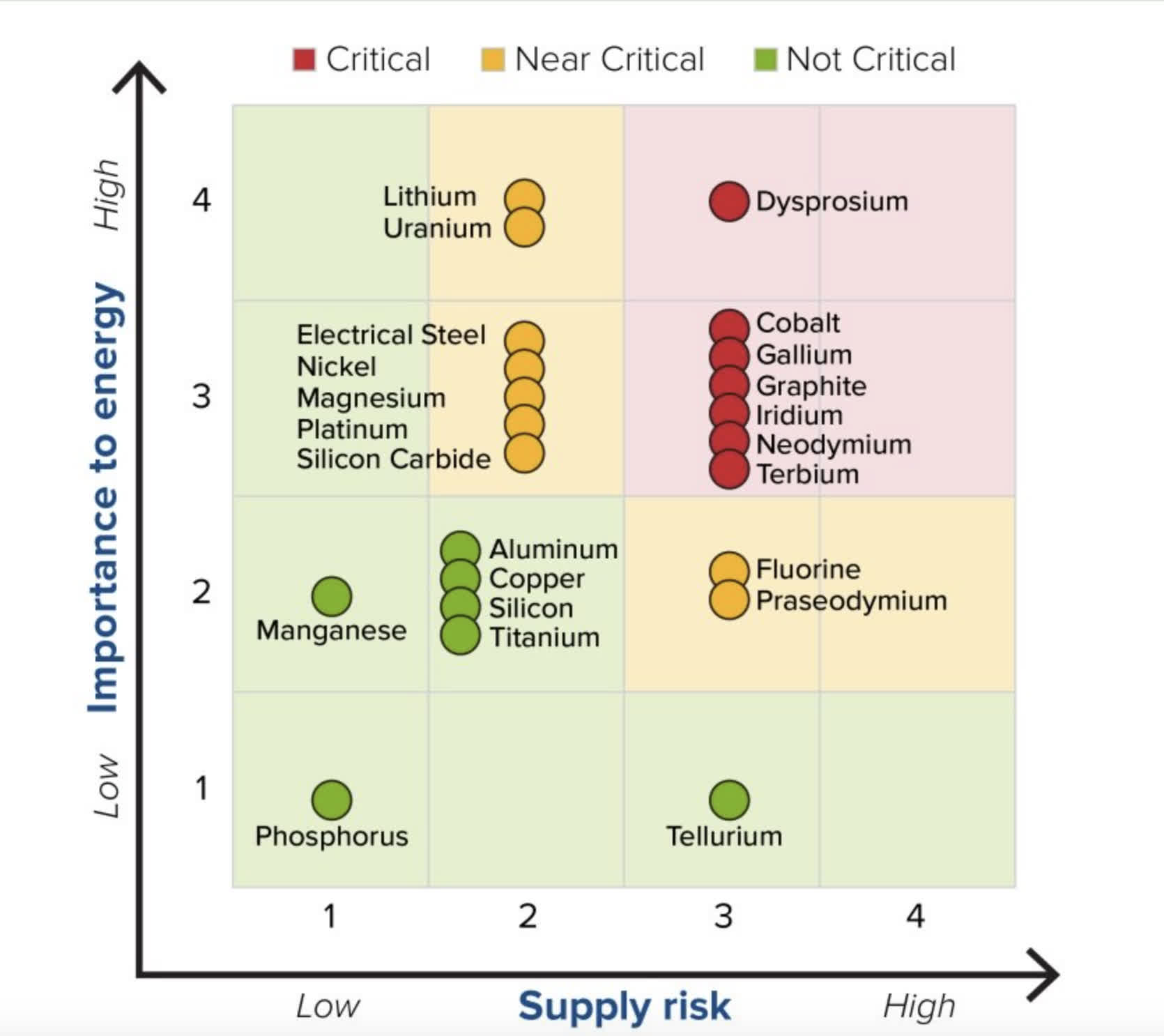

Lithium is also being considered a near-critical energy element by the US Department of Energy in the short term and critical in the medium term. Subsidies to US-based lithium miners could also act as a supplement to the company’s liquidity in the future and add fuel to a bull thesis:

Short term 2020-2025

energy.gov

Medium term 2025-2030

energy.gov

Risks

Albemarle being a successful investment is a bet on both EV demand increasing evermore by 2027 and lithium-ion batteries remaining the best battery technology going forward.

sodium ion batteries

electrek.co

While you will see many pros being floated around the internet about superior tech and environmental suitability of sodium-ion and other battery chemistries, the downfall of most other chemistries is that the energy density lags behind lithium-ion. I remember Alcoa (AA) even had a 1,000-mile aluminum battery that supposedly worked back in 2014. I have yet to see one on the road. I won’t laugh at other battery types, if one does match the density by weight and can charge faster than lithium plus has a feasible supply chain, you could see some new battery-powered cars come out between now and 2027.

The Chinese are of course the prime candidates to experiment with these new battery technologies being that they are a less regulated country/economy than the Western countries. Should one hit, that could reduce Albemarle’s 2027 revenue projections by virtue of demand dilution.

Summary

Lithium batteries work and are proven. Yes, other rival chemistries will try their hands, but let’s not forget that lithium batteries will continue to improve and most R&D dollars floating in the ether are being spent on improvements in lithium-ion. That being said, the industry outlook in the near term is not good. This is the bottom of a cycle, but also the time to have the highest conviction when it comes to commodity investing.

I believe the preferred shares are the way to go and I am accumulating. The total return average on my bull case is nearly equivalent for the pref versus common when purchasing either today. The pref lets you hedge away some of your risk by reinvesting your dividends elsewhere. If the bull case misses and the price remains flat to down from here, the additional 19.22% in dividends over the period to convertibility buffer the pain. You don’t have that flexibility with the common.