RoschetzkyIstockPhoto

This article was co-produced with Wolf Report.

It’s been some time since we’ve looked closely at Simon Property Group, Inc. (NYSE:SPG); however, the time has come for an update on the company for a basic reason – the company recently hit my highest-level rotation target, the target that would mark the REIT as a “HOLD” for me, when it moved over $150/share.

Why do I view this as such an important limit, and why do I think the company is now a “HOLD” and it should no longer be bought?

That’s what we’ll look at in this article and make sure to convey.

Mind you, I am not saying that this is not a good REIT.

There is, in fact, no doubt in my mind that this is a very good REIT.

But being a good REIT or a good company is never enough to be a “BUY” for me.

That’s only the first step – the relevant step for any company is being at a good valuation relative to the upside the company can achieve.

And for a number of reasons, I do not believe SPG to be able to outperform its current valuation for the next few years – which means that anyone investing now is, in my opinion, at risk of longer-term underperformance and would probably be better investing in something else – preferably at a better valuation than this one.

A quick investment history – I owned SPG both before the COVID-19 crash, and sold most of it before, only to invest in the company (significantly) when the company crashed to well below $60/share.

I then enjoyed triple-digit returns as the company went up to well above $150/share in 2021, sold off most of my stake, then invested slightly again at $90/share in 2022.

Now I only have a token position left – and that is after selling most of my stake.

So here is why.

Yahoo Finance

Simon Property Group – A good company, but a bad valuation

A “bad valuation” as I see it is a valuation that for me does not guarantee a 15% annualized upside for the investor – and that is the situation that we currently have.

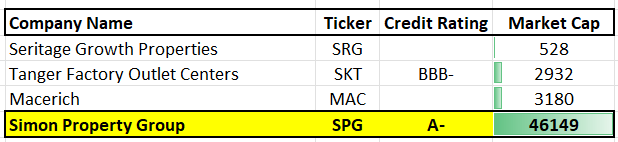

SPG is an A-rated Retail REIT.

It’s one of the best Retail REITs out there.

It yields over 5.2% here, and over the past 6–8 years has managed, inclusive of COVID-19, an average of 2-3% AFFO growth.

Its volatility in share price does not reflect its fundamentals.

It has shifted significantly over the past few years, from highs of almost $200/share to lows of below $50/share, all without really changing much in its earnings potential.

This has to do with Retail and Mall REITs, which were hit hard.

Many in the mall and outlet sector have seen some incredible volatility regarding their share price in the last few years.

But this is, in my mind, completely weighed up by the company’s underlying fundamentals, stability, management, and solid operating performance. (And it still is here).

Despite some truly massive volatility for the last 2–3 years, the only real impact since 2019 was a 25% drop in 2020, followed by normalization about a year later.

So, from a 9-10-year perspective, including 2025E, the company is growing slowly, around 2.5% per year – and that is also still the case here.

Simon Property Group IR (Simon Property Group IR)

At previous valuations closer to $100/share, we could forecast the company flat and still get a 7%+ yield and get over 15% annualized here.

That’s no longer the case.

This is, by the way, despite the overall strong start to the year.

Simon Property Group has long been able to deliver outperformance.

This quarter saw even some other trends that are worth mentioning – such as the sale of what remained of Authentic Brands, at a non-trivial $1.45B in proceeds, which resulted in a raise in the company dividend (over 8%).

Net income was up, AFFO was up, and domestic NOI was up 3.7%.

Occupancy was at really quite great levels, 95.5%, which rivals some of the multifamily REITs, which is quite wonderful when you think about it (we’re talking about Malls after all), and base minimum rent on a sq ft basis was up 3% as well. Again, this is a very difficult macro situation.

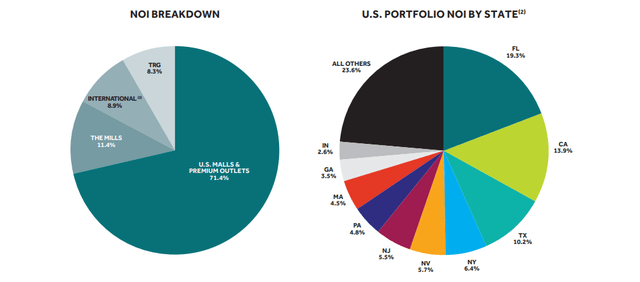

Take a look at the current company NOI composition, and you’ll see that SPG remains US-heavy, and premium-heavy.

SPG IR (SPG IR)

And seeing here that FL and TX make up around 30% together, this gives a very good weight against the risk represented by California, which is still at just south of 14% of the total.

The company’s fundamentals or credit profile does look “bad” on a surface level – over 80% long-term debt to cap, but it’s a bit of a wrong picture you get here.

The company has a fixed charge coverage of 4.3x, with a weighted average interest rate of less than 3.75%.

Also, FFO payout for SPG, even TTM, is less than 60%, and net debt has been declining since 2020 by about $4B – and this is during one of the more difficult macro situations that we could fathom for a REIT such as this.

The company’s execution on the ABG sale is something else that’s really worth highlighting here – it was quite exceptional, giving the timing and the resulting upside.

The company-specific downside or risk that I would mention here is the California and northeast trends – very similar to trends I have been highlighting in other articles as well.

This is weighted up by the markets in Florida and Texas, both of which are showing exceptional strength (Florida especially).

A good comment by Mr. Simon really summarizes the situation here, and what Simon Properties is seeing.

I think people, at the end of the day, they as part of — when they go on holiday, they love shopping as part of that experience, dining, shopping, being with their families. And as I said earlier, I mean, we feel like the mall has made a big comeback, physical stores or where it’s happening. We’re seeing a resurgence and reinvigoration of that whole product.

(Source: David Simon, 1Q24 Earnings Report.)

The main forward upside potential comes from a moderation in the cost of living and increases in wages, as well as a reduction in overall inflation.

Overall, anything that makes the economy more “healthy” will drive positives for SPG, and anything that does the opposite is quite likely to do the opposite here as well.

And therein lies the current problem with Simon Property Group – not because the company has done poorly in any way – but instead because the company is unlikely, as I see it, to do as good or better going forward.

This is because I do not see macro improving all that quickly – and I am hardly alone in this.

Simon Property Group – The problem lies in valuation

Things can change quickly.

In an article in late 2023, I called the company “cheap” and even invested – and successfully so.

Now, that time is over.

I gave the company a $150/share PT.

I’m not changing that PT.

That means that SPG is now a “HOLD.”

Why is it a “HOLD”?

Because I do not believe you’re likely to get 15% annualized or above.

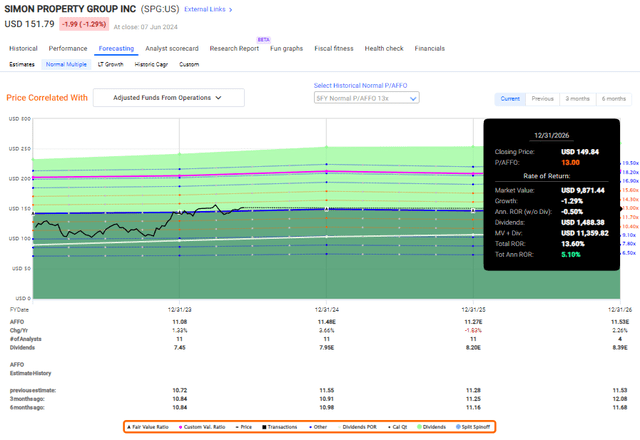

The company currently trades at a 13.5x P/AFFO, which when you consider that the company is estimated to grow at less than 1% per year for the next few years (F.A.S.T Graphs Paywalled link), gives us an upside at the 5-year normalized level that looks like this.

SPG Upside F.A.S.T. Graphs (SPG Upside F.A.S.T. Graphs)

That means, to make it clear to you, a smaller upside than the yield the company currently offers.

Why, you might ask, do I consider the 5-year average the way to go here?

Why not the 10 or 20-year?

Because using those would be unfair to the company’s estimated growth rate.

During the 10-20 year averages, we had years when SPG saw growth of over 10% per year in AFFO.

Correspondingly, it makes sense that the company would be valued at a far higher rate – and if I could see that SPG was going to grow better than we’re seeing, here, I would have no issue with such a forecast or a valuation.

At this point, though, I have a major issue or gripe with such a forecast in exactly what you see above.

And let’s say, as an example, that you demand a 20-year forecast of this company at an average of 15.76x.

That’s still not a 15% annualized rate of return – it’s only around 12% at the AFFO growth forecasts we see today.

Granted, SPG has a non-trivial historical risk of seeing outperformance – but even in that case, it’s barely enough to interest me here.

S&P Global gives SPG a target range starting at a low of $140 and going up to a maximum of $190/share.

The average here is $160/share.

My PT in my last article was $150/share, and that’s also where I remain at this time.

That $150/share represents about a 12.3x-13x P/FFO, which is where I believe this particular REIT is entirely justified in trading – that and no higher.

Analysts have improved their targets quite significantly in a short time – and I believe this improvement to be as much an overreaction as the company’s drop to very low price targets not that long ago, when the average target for SPG was less than $105/share – and during COVID-19 it dropped even to below $40 from some analysts.

I have personally never believed SPG to be worth less than a full $110/share, even during the worst of the drop, but I also see the danger here.

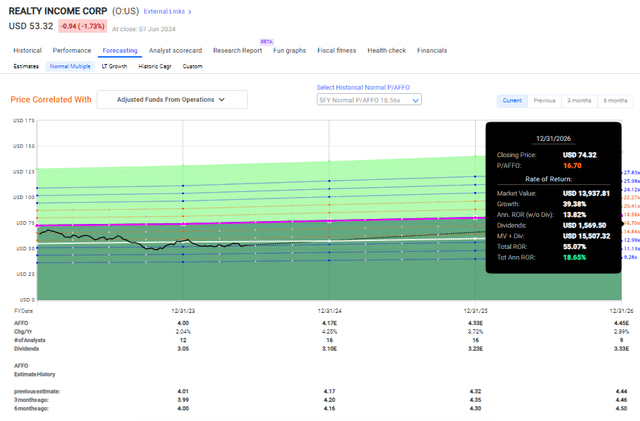

Let me show you an alternative for your capital if you’re so inclined to invest in REITS.

Realty income F.A.S.T Graphs Upside (Realty income F.A.S.T Graphs Upside)

While the AFFO is similar, this company is set to grow more, has a higher yield, a lower debt, a better market position (not to say that SPG is bad in any way), and far more downside protection.

Simon to me, at this point, is a “HOLD” – and I believe this to be a good time for rotation.

Thesis

- Simon Property Group is a class-leading A-rated REIT that has significantly outperformed since dipping during the pandemic. Savvy investors have made 40-70% RoR inclusive of dividends, and the trip was far from over before – but I consider it to be over now.

- I rate SPG a “HOLD” here, which marks a downgrade for me, and I also say that future growth for the company here seems less likely. Its releasing spreads remain positive, but the best that can be hoped for here is outpacing cost increases/inflation somewhat. Is this enough? Not to me.

- My PT for SPG remains $150 – as you may recall, this was the target the last time I wrote about it. As I said in that previous article, my rotation target for starting to really push capital into other investments is around this level, and we also need to look at the market overall and recognize opportunities to rotate cash into better-performing investments (or lower-valued ones).

- SPG is a “HOLD” here – and I have rotated most of my position.

Remember, I’m all about :

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies discounted, allowing them to normalize over time and harvesting capital gains and dividends meanwhile.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

I’ll call SPG a “HOLD” here, due to the valuation being too high.

Data Duel

(I hope you’re enjoying our new “data duel” feature. Let us know your feedback, please. Thank you.)

iREIT® iREIT® iREIT® iREIT® iREIT®