MEDITERRANEAN

Investment Thesis

Mama’s Creations, Inc. (NASDAQ:MAMA) operates in the deli-food industry and recently announced the release of new products. In the last quarterly report, the company has gone through a strong growth: the stock price increased by 150% in the last year, and revenues have been growing steadily for years.

Analyzing the company’s strategy and the business plan, I think that new products along with direct-to-consumer selling device could lead to a further increase in sales.

I believe that the management actually has a clear idea on how to penetrate the market, offering new products to expand its customer base.

I think that the introduction of these new products will be a successful move, because they are suitable for the American Market both in terms of flavor and type of food.

Mama’s e-commerce platform and new products

On November 28, 2023, Mama’s Creations launched its online e-commerce platform. The main goal is to optimize the business model, allowing customers to buy their product directly online. The products are shipped and delivered directly to the customers’ houses, and this leads to two major advantages.

Firstly, it improves the business cycle and allows Mama’s Creation to better understand the customer preferences, and secondly, it creates a business-to-consumer model that will lead to a cost reduction.

It is currently too early to assess the extent of e-commerce sales, but I believe that in the future, e-commerce has the potential to become a strong source of revenues for the company.

The CEO Adam L. Michaels commented:

Our move into e-commerce was the result of thoughtful planning and market analysis, to developing an efficient and sustainable business model that we expect will improve upon common industry pain points.

Another advantage of e-commerce is that through it the products can reach the demand in particular geographical areas which faced obstacles with the traditional business model.

On June 6, 2024, the company announced the launch of new products, and I think that it can be a smart move that will increase the firm’s value and sales.

Mama’s Creations focuses heavily on traditions, offering products based on Italian recipes. This, over time, led to concerns that the company was becoming too “path-dependent” and that a change in consumer tastes would cause a reduction in sales. If we look at the new products that the company has launched, we notice that they cater to American tastes, for example, breakfasts based on eggs and bacon. In my opinion, the strength of this strategy does not derive only from the new flavors introduced but also from the type of food that the company wants to sell. In fact, the offer now also covers breakfasts and snacks, which are a type of food that is generally very successful in the American market.

Another piece of good news is that the introduction of these new products is not particularly expensive, since the company can use the same production facilities and similar production techniques to those it already uses for traditional products.

If we consider that sales have grown constantly in recent years, the addition of new products can be the key to broadening the target of buyers. Breakfasts and snacks also have a higher repurchase frequency, and this can help make the company’s revenue streams more stable.

In the picture below, we can see the new products:

New Products (Company’s website)

Looking at the product, we notice that they are designed to be perceived as healthy. They are not junk food, and this characteristic is in line with the traditional products offered by MAMA. In addition to that, trends show that in the snacking market, the preferences among consumers are switching toward healthy food, so as we can see, there are many reasons why these new products could be successful.

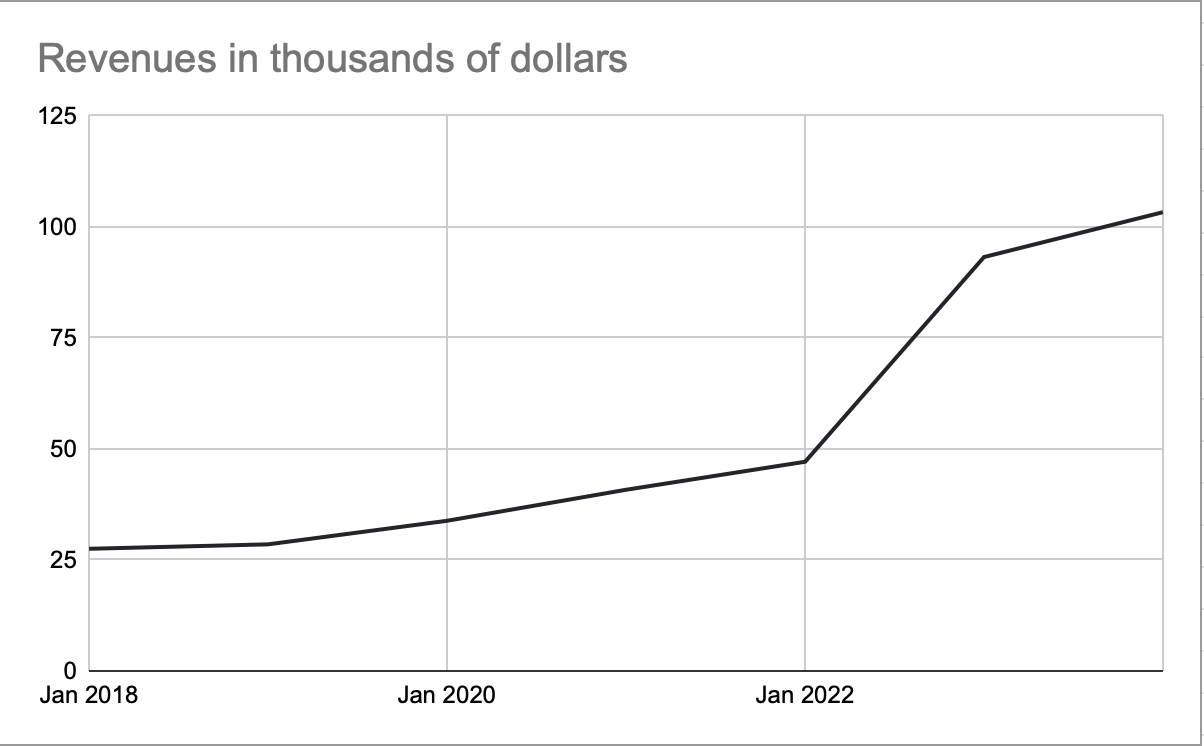

Mama’s Creations revenues and stock overview

To better understand the extent of the revenues, we can look at the plot below:

Revenues (Seeking Alpha)

If we consider the last period we have that in January 2022 revenues amounted to 33 million while in January 2024 revenues were 103 million with a CAGR of 19%.

So the company’s revenues are increasing a lot, and its products are highly appreciated by consumers. Furthermore, according to some studies, the deli-food market is becoming increasingly important.

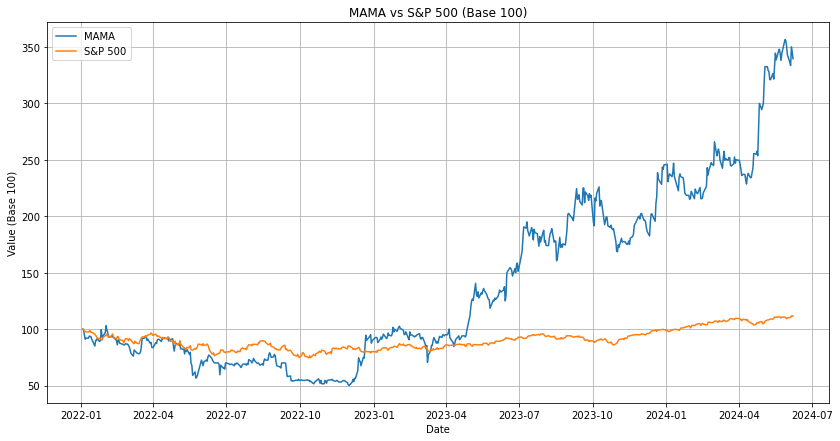

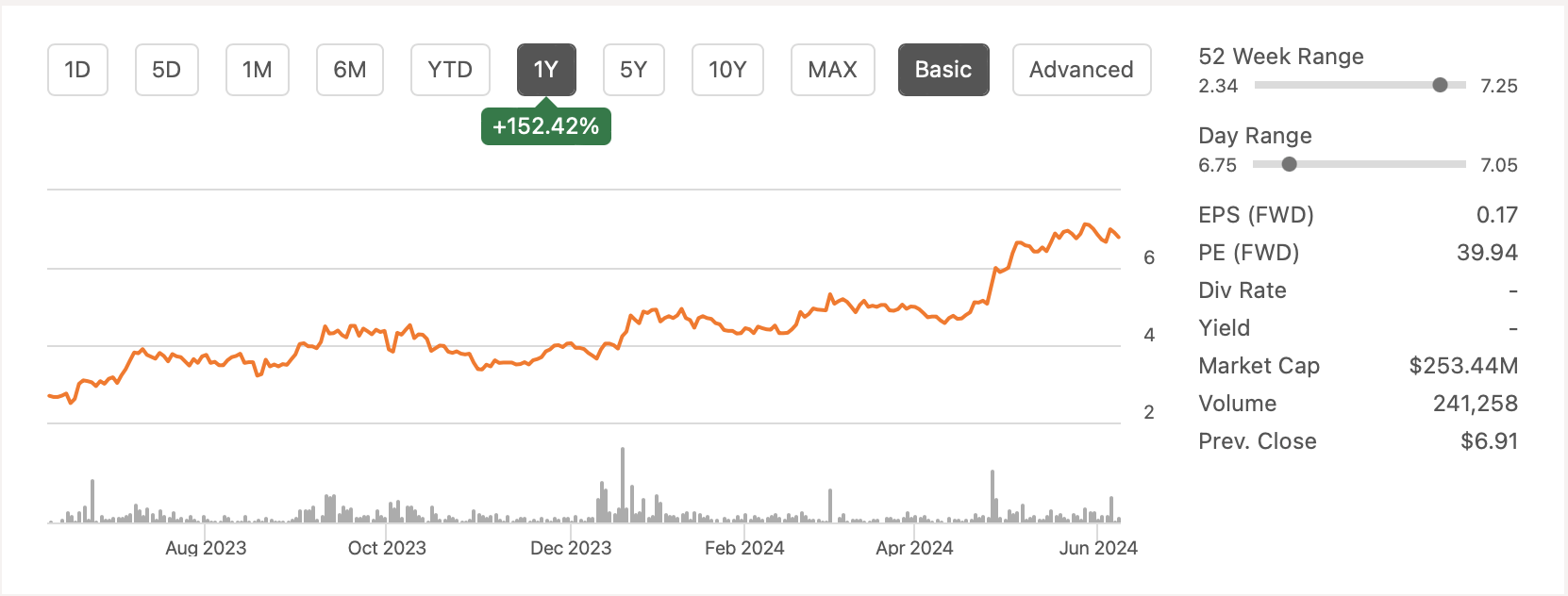

Stock (yFinance)

In the chart above, I wanted to compare the MAMA stock price to the S&P from 2020 to June 2024. I converted the time series to BASE100 to make them comparable, and as we can see, MAMA performed much better than the market average. In the period considered, the MAMA share price had a return of 350%.

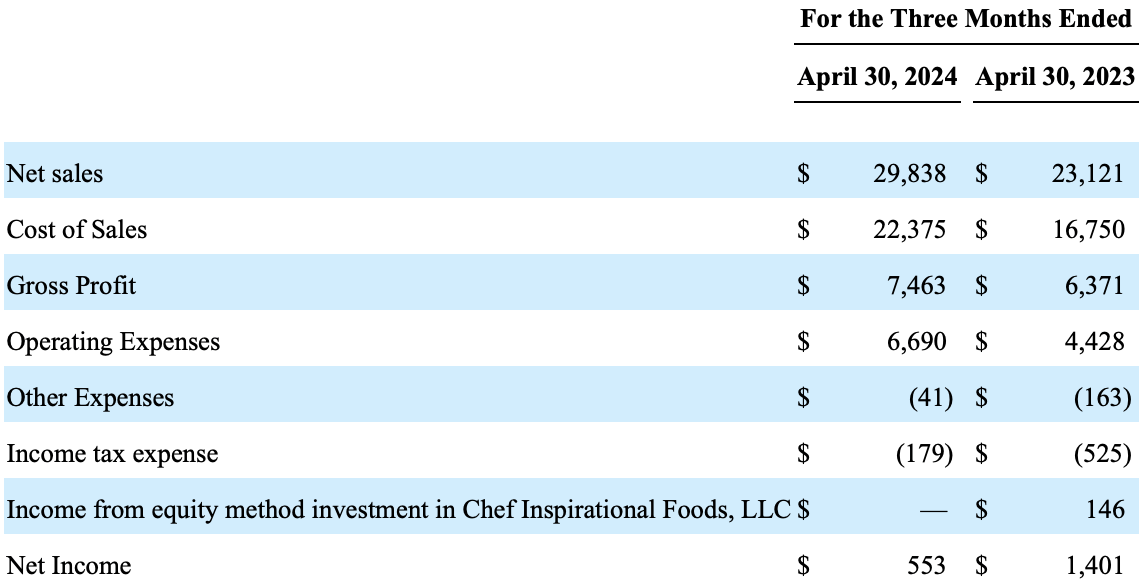

MAMA last 10-Q Overview

On June 11th, the company released its quarterly report, and the results are satisfactory.

Sales (Company’s 10-Q)

As we can see, net sales increased by 29% compared to the same period last year.

We can also see an increase in operating expenses which, according to the company, were mainly caused by one-time legal settlement expenses and stock-based compensation. Furthermore, the company stated that it has increased marketing expenses. In my opinion, this is a positive factor because the company can utilize the working capital it has to promote new products. All in all, the results are positive. Despite the new projects it is undertaking, MAMA managed to record a net income of 553 million in the first 3 months of 2024.

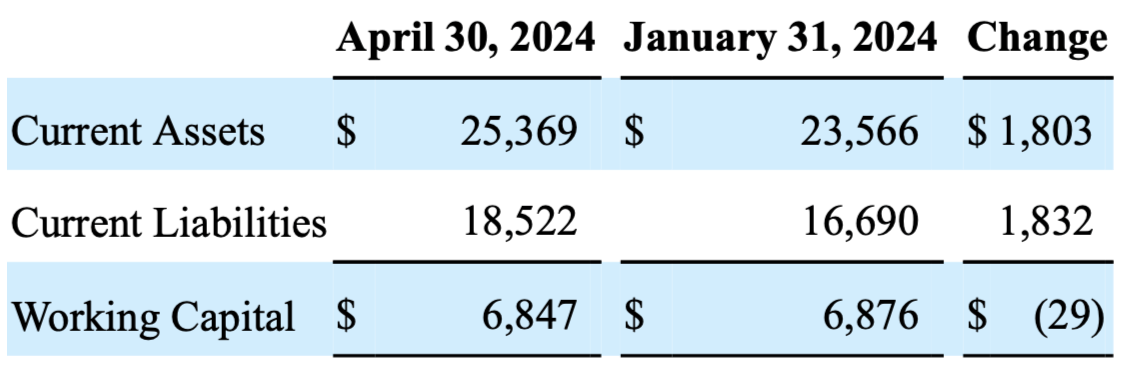

Working Capital (company 10-Q)

As we can see from the table, working capital remained almost unchanged compared to January 2024 because current liabilities increased equally to current assets.

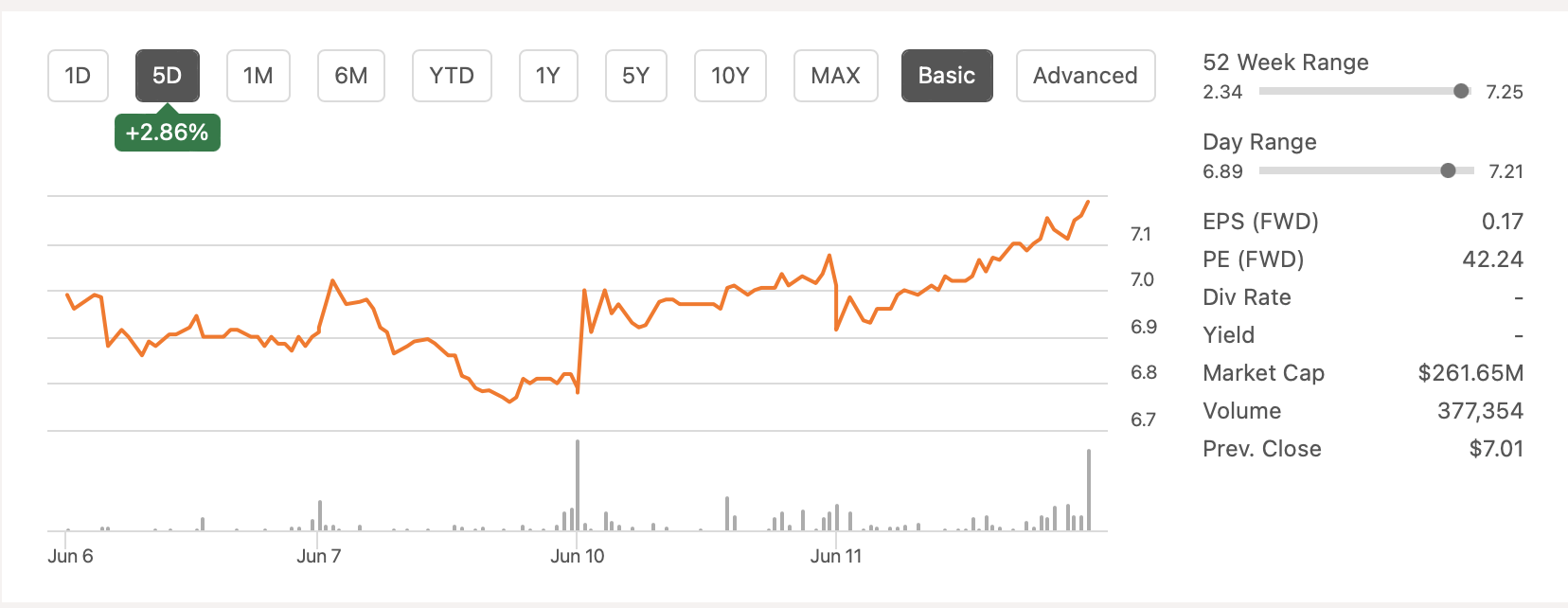

Stock (Seeking Alpha)

The market also seems to have appreciated the results of this first quarter of 2024, in fact, in the last 5 days the stock has appreciated by 2.86%

Financial Analysis

Now I want to analyze some key financial information about the company to assess the results in 2024 both in terms of profitability and solvency.

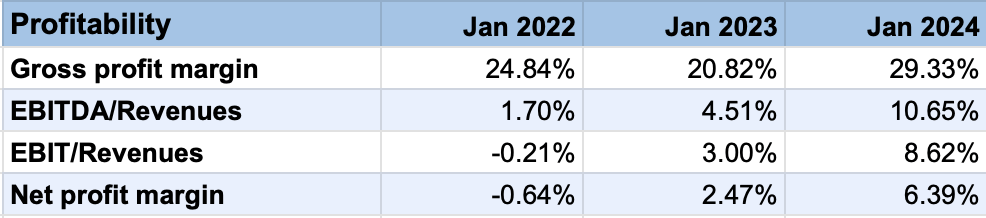

Profitability (Author’s calculation)

Looking at the profitability ratios, we see that in 2024 all margins have increased compared to previous years. In particular, if we look at the gross profit margin, it is surprising that during 2023 the company increased sales but the cost of goods sold remained the same as in 2022.

Cost of sales (Company’s 10k)

I think that the introduction of the e-commerce platform could make it possible to increase this ratio even more in 2024 for the reasons that we have seen before.

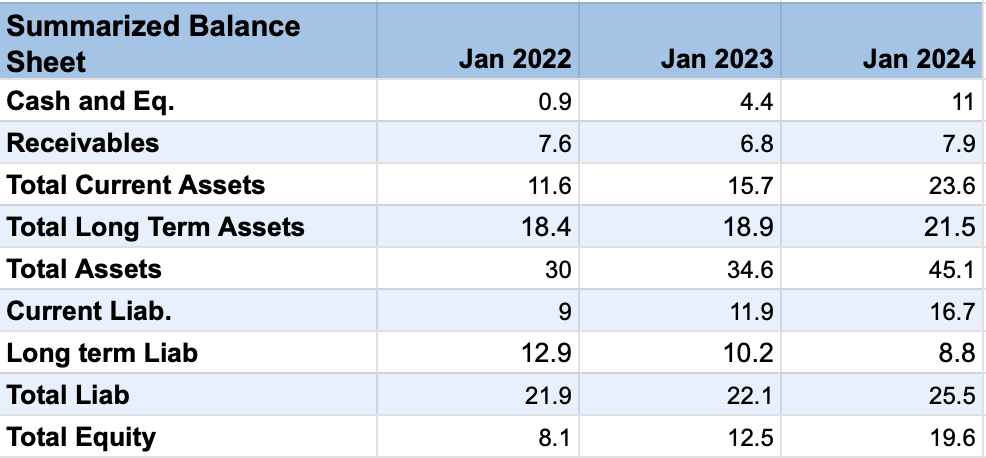

A consequence of the increase in the profit margin is the possibility for the company to generate more free cash flows. In fact, when we look at the balance sheet, the main thing that we notice is the strong increase in cash and cash equivalents. Cash has risen by more than 50% during the past year. This is positive if we contextualize this figure with the strategy of the firm, since it has more available net working capital to support investments in new products and marketing.

Summarized Balance Sheet (Seeking Alpha)

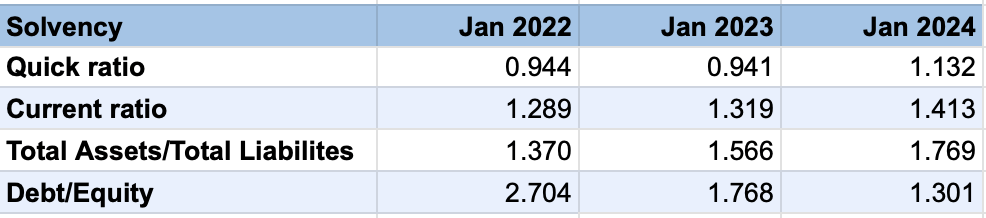

To be more general, we can say that the company has strengthened its financial position in 2024, and this is confirmed also by the solvency ratios that you can see in the table below.

Solvency (Author’s calculation)

Both the quick and current ratios are above 1. This means that the company is able to fulfill its short-term financial obligations.

Even in the long term, the value of the Total Assets/Total Liabilities is above 1, so I do not see any concerns related to debt.

As for the Debt to Equity ratio, it has decreased in 2024 primarily due to an increase in the total equity that passed from 8.1 million to 19.6 million with a CAGR of 34%.

Valuation

During the last year, we have seen a constant growth in the stock price, so now we want to try to forecast what will happen next.

Stock Chart (Seeking Alpha)

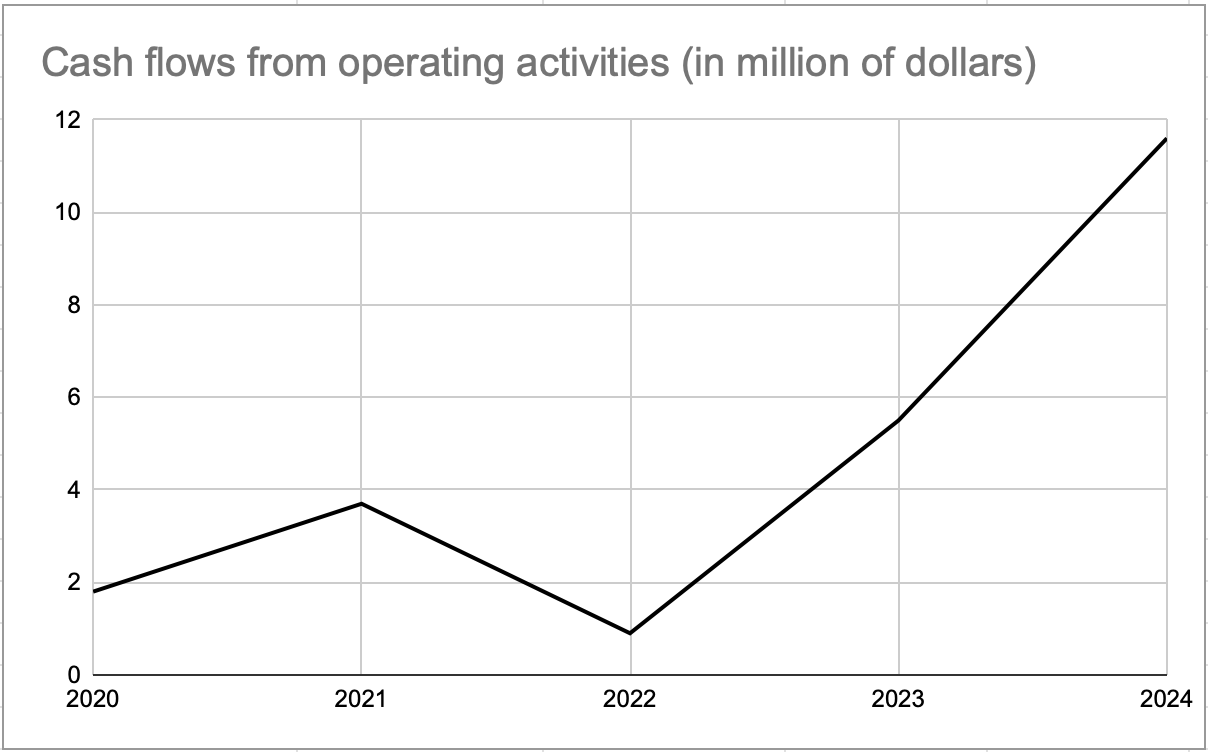

Looking at the cashflows from operating activities of the last years, we can notice that the company has greatly increased its capabilities to generate free cashflows.

Cash flows (Seeking Alpha)

Considering the strong financials of the company and the promising strategy, I think that cash flows will continue to grow. The e-commerce and the new products could lead to an increase in sales, and the company has already demonstrated that it can improve its cost structure. I do not expect a growth like the one in the chart in the next years, but I believe that a future growth rate of 5% can be a reasonable assumption.

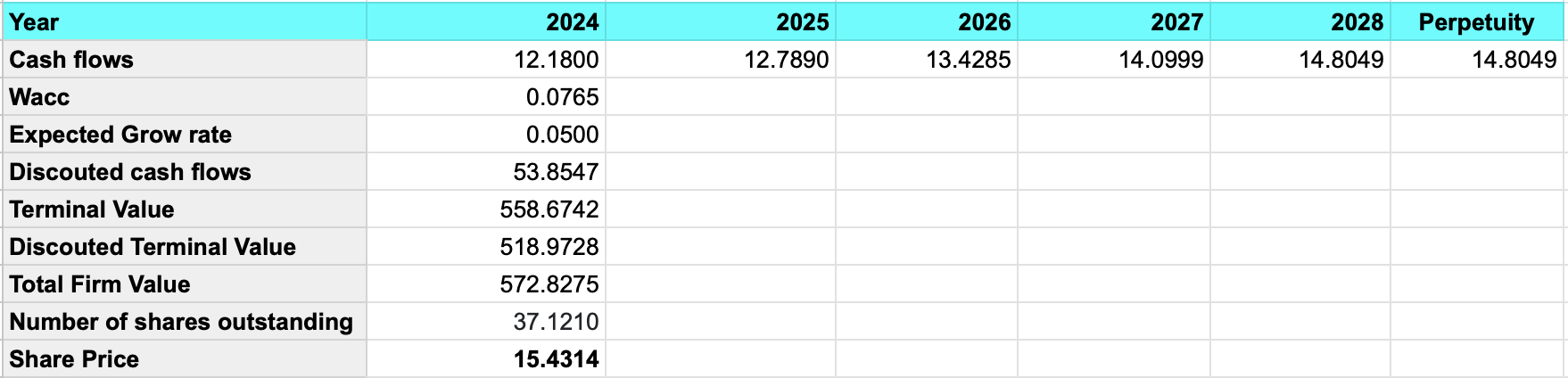

Using a beta of 0.7 estimated using the capital assets pricing model, we obtain a WACC of 7.65%.

According to the discounted cash flows model, we get a total firm value of 572.8 million dollars, and dividing it by the number of outstanding shares, we get a fair share price of $15.4.

Discounted cash flows model (Author’s calculation)

So, to conclude, we observe that according to the model the stock price appears to be under-priced. If the company will execute its strategy successfully and expand sales volume, I believe it will be possible to see Mama’s stock price above the $10 barrier in the next period.

Downside risk

To date, the company’s largest customers are distributors, such as grocery stores. In particular, as indicated in the 10k, in 2024 the majority of sales were made by three main customers:

During the twelve months ended January 31, 2024, the Company earned revenues from three customers representing approximately 26%, 11%, and 10% of gross sales.

E-commerce, in my opinion, could help to mitigate this risk, but it requires time, and in the short term, the demand that comes from these three customers will be determinant for the success of the company. This is a factor to consider, because these customers purchase traditional products from MAMA, which currently represent the core business of the company’s offer.

Conclusions

In conclusion, I believe that MAMA is an interesting company that shows strong financials and has good management. The business plan for the next years, based on increasing the variety of the offer, can be a successful move to strengthen the position of the company. In addition to that, if the e-commerce platform brings a significant source of revenue, the company will become more independent and have more freedom in determining its prices.

The new product seems to fit the American market very well, and the characteristics of these new products will make it possible to diversify and increase the stability of the revenue stream.

According to the discounted cash flow model, the fair price of this company is around $15, and at the time of writing this article, the shares are trading at $7. I think this is a good opportunity with relatively low risk, so my advice is BUY.