ablokhin

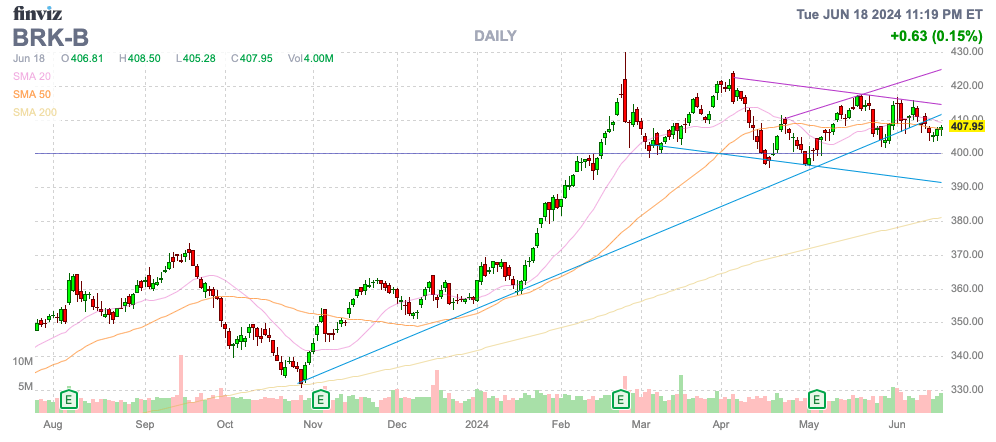

At least since the start of the 2020s, Berkshire Hathaway (NYSE:BRK.A, NYSE:BRK.B) hasn’t done much with a sizable cash balance. The market faced a couple of substantial downturns during this period and a lot of non-tech stocks are considered rather cheap, yet the investment firm run by Warren Buffett continues to hold a massive amount of cash. My investment thesis is Neutral on the stock, as Berkshire Hathaway has mostly been turned into a minimal growth investment, generally tracking the S&P 500 index over the last decade.

Source: Finviz

Difficult To Value

One of the main issues with valuing Berkshire Hathaway is the mixture of an investment portfolio and operating business units from Geico in insurance to BNSF in railroads. Typically, Wall St. doesn’t accurately value investments with a complete focus on the earnings stream of the operating business with no value assigned to the investments.

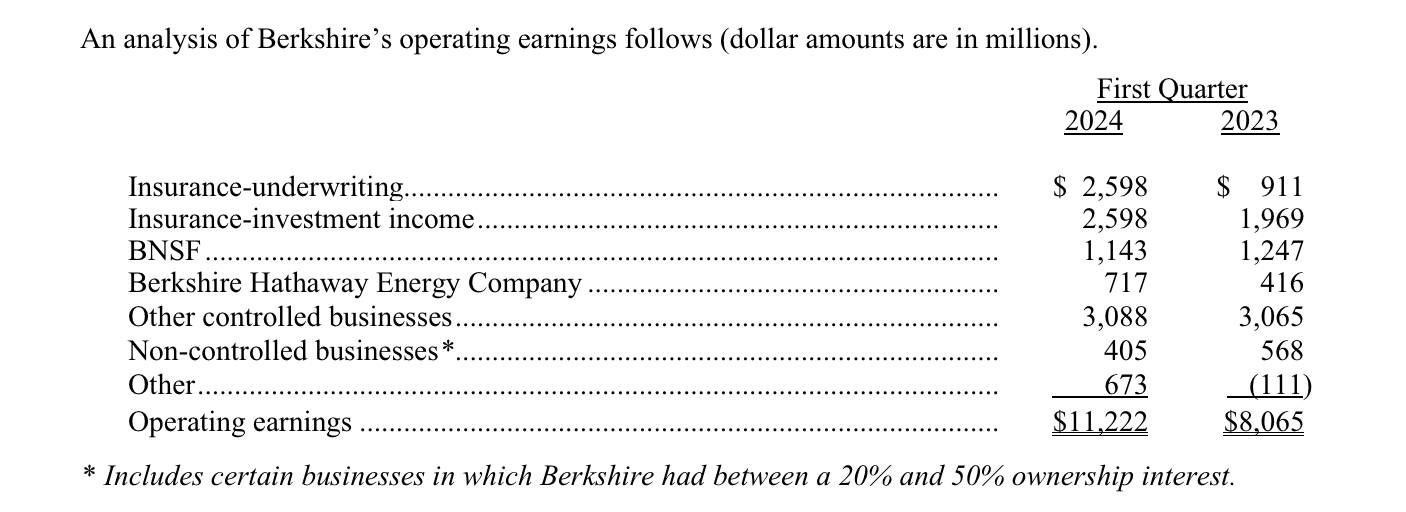

Berkshire Hathaway recently reported a quarter where BRK.B shares reported net earnings of $5.88 per share. The company reported operating earnings of $11.2 billion in the quarter, based on the following segment results:

Source: Berkshire Hathaway Q1’24 shareholder letter

As one can see, Berkshire Hathaway generates a large portion of the profits of the operating business from insurance. Outside of the insurance business, BNSF, the Energy Company, and Other controlled businesses had limited to no growth in the last year.

The consensus estimates have Berkshire Hathaway B shares earning ~$20 per share in 2024 with forecasts for minimal growth through 2026. The stock trades at nearly 20x EPS estimates of $21 for 2026, which is extremely high considering the limited growth.

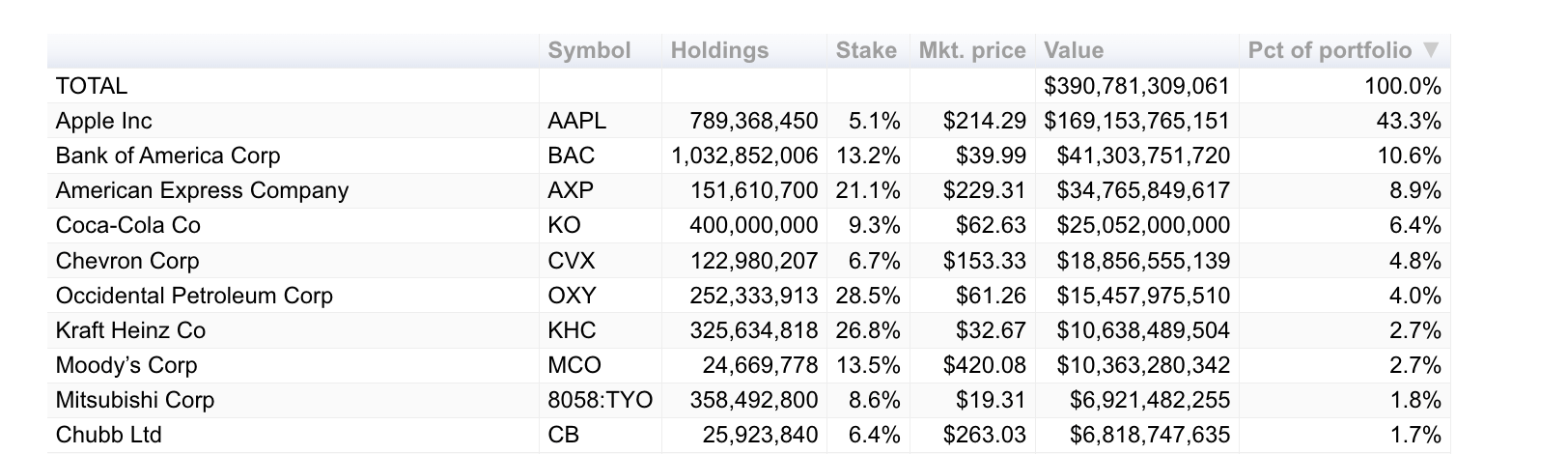

On top of these profits, Berkshire Hathaway has a large investment portfolio. Based on the portfolio tracking from CNBC, the firm has $391 billion in investments of public companies, with the following top 10 holdings.

Source: CNBC

The key here is that these investments don’t flow through to the quarterly financial results outside of dividend income. On top of that, Buffett wasn’t aggressive with investments over the last 5+ years.

For various reasons, Buffett actually dumped the airlines near the all-time lows during the Covid period. On top of that, the investment firm dumped long-time holding Wells Fargo (WFC) at $24 and the stock recently surged to $60.

From an investor standpoint, the frustration here is that Buffett appears the opposite of what made Berkshire Hathaway a runaway success in the past. The company could’ve decided to sell these stocks due to major trade-offs, but the firm ended the last quarter with a cash balance of nearly $189 billion, and Berkshire Hathaway has held excessive cash the whole period.

Chubb Addition

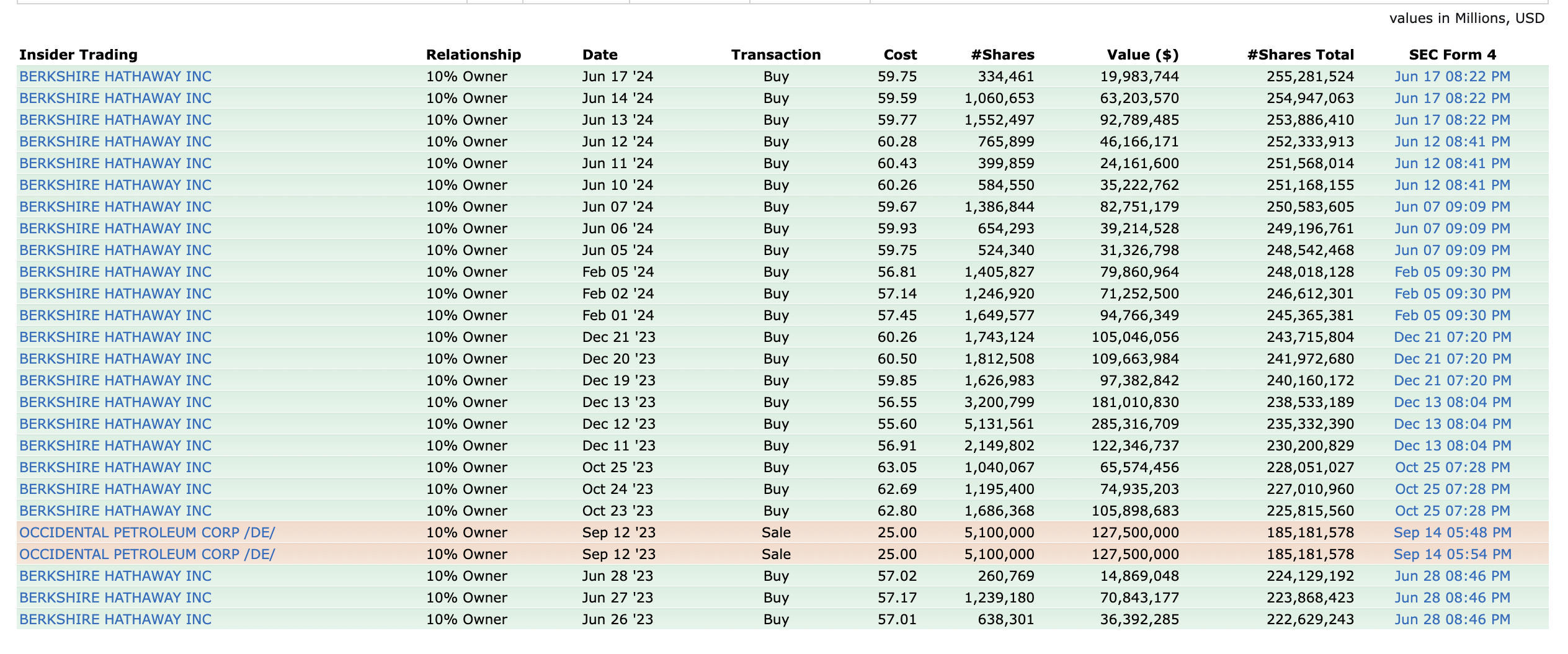

Some recent examples of bizarre moves, Berkshire Hathaway had a confidential filing to acquire shares of Chubb Limited (CB) in the past few quarters. The company finally released a $6.7 billion investment in the insurance giant along with the following moves during Q1’24 as follows:

- Chubb – bought 26 million shares for $6.7 billion

- Occidental (OXY) – bought 4 million shares

- Liberty SiriusXM Series A (LSXMK) – bought 22 million shares

- Liberty SiriusXM Series C (LSXMA) – bought 11 million shares

- HP (HPQ) – sold 23 million shares

- Apple (AAPL) – sold 116 million shares

- Paramount Global (PARA) – sold 55 million shares

- Sirius XM Holdings (SIRI) – sold 4 million shares

After all of these transactions, Berkshire Hathaway actually boosted the cash balance by $21 billion during the quarter. The Apple sell alone contributed the majority of the cash boost in the March quarter.

While the stock is relatively cheap at 10x forward EPS targets, Chubb currently trades near all-times highs, which is an odd time for Warren Buffett to load up on a stock. The insurance stock could’ve been had for $100 following the Covid dip, and the stock now trades at $263.

If anything, Buffett is momentum trading these days, possibly a sign the nearly 100-year-old is no longer taking major risks or other portfolio managers are making the calls.

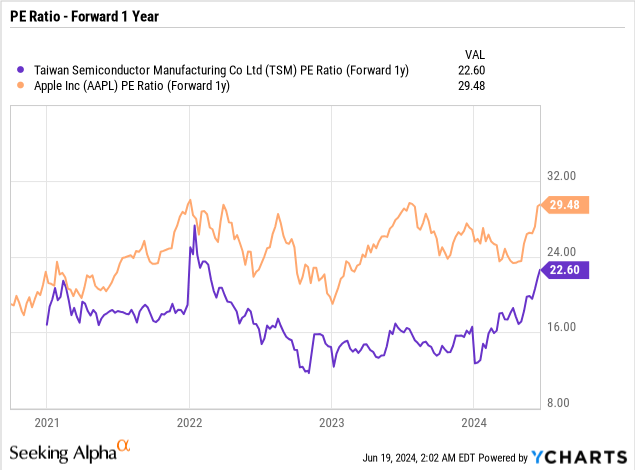

TSMC Debacle

Only about 18 months ago, Berkshire Hathaway famously unloaded a position in Taiwan Semiconductor Manufacturing Company Limited (TSM) in the $90s, not long after buying the Taiwanese chip giant. TSMC has doubled during this period to nearly $180 while the largest portfolio company in Apple faces the same risk as Taiwan with business operations highly reliant on China not trying to militarily invade the small island country.

If anything, Apple is the safe investment acceptable by the market, whereas TSMC was viewed as a high-risk investment. As our research at the time highlighted, TSMC was the smart investment and the far cheaper option, trading regularly below 15x forward EPS targets versus the expensive Apple.

Buffett and Berkshire Hathaway sold the stock when the opportunity existed to double down on a chip manufacturing company unloved by the market at the time, while the potential for advanced chip manufacturing and the booming AI chip play made TSMC a near no-brainer. The Buffett way was to buy the cheap stock, not the largest company in the world trading at 30x earnings.

TSMC is now worth $738 billion, allowing for a sizable position to solve a lot of the problems supposedly facing Buffett when claiming opportunities to own positions of size don’t exist.

Occidental Obsession

Berkshire Hathaway continues buying Occidental Petroleum shares on a such a regular basis that the energy stock never dipped with the market. Investors continue to buy up OXY around $60 knowing Buffett will continue buying shares.

Source: Fiinviz

The firm recently added another 2.9 million shares to build the OXY position up to over $15 billion. While Buffett famously began an investment in the energy company back in 2019 to help facilitate the acquisition of Anadarko Petroleum, Berkshire Hathaway got preferred stock with an 8% dividend and warrants to buy 84 million shares at over $59 per share. Buffett could’ve loaded up while OXY was beaten down below $20 all throughout 2020. Other energy stocks were just as cheap, if the position size in OXY was an issue.

In fact, the prime thesis here with Chubb, Occidental, and TSMC is that all 3 stocks faced periods of substantial weakness since the start of 2020 and Berkshire Hathaway didn’t use the weakness to overly invest in either stock. Chubb wasn’t bought on the 2020 low, OXY wasn’t fully invested during the 2020 lows, and TSMC was actually unloaded on weakness at the end of 2022.

New Conservative Path

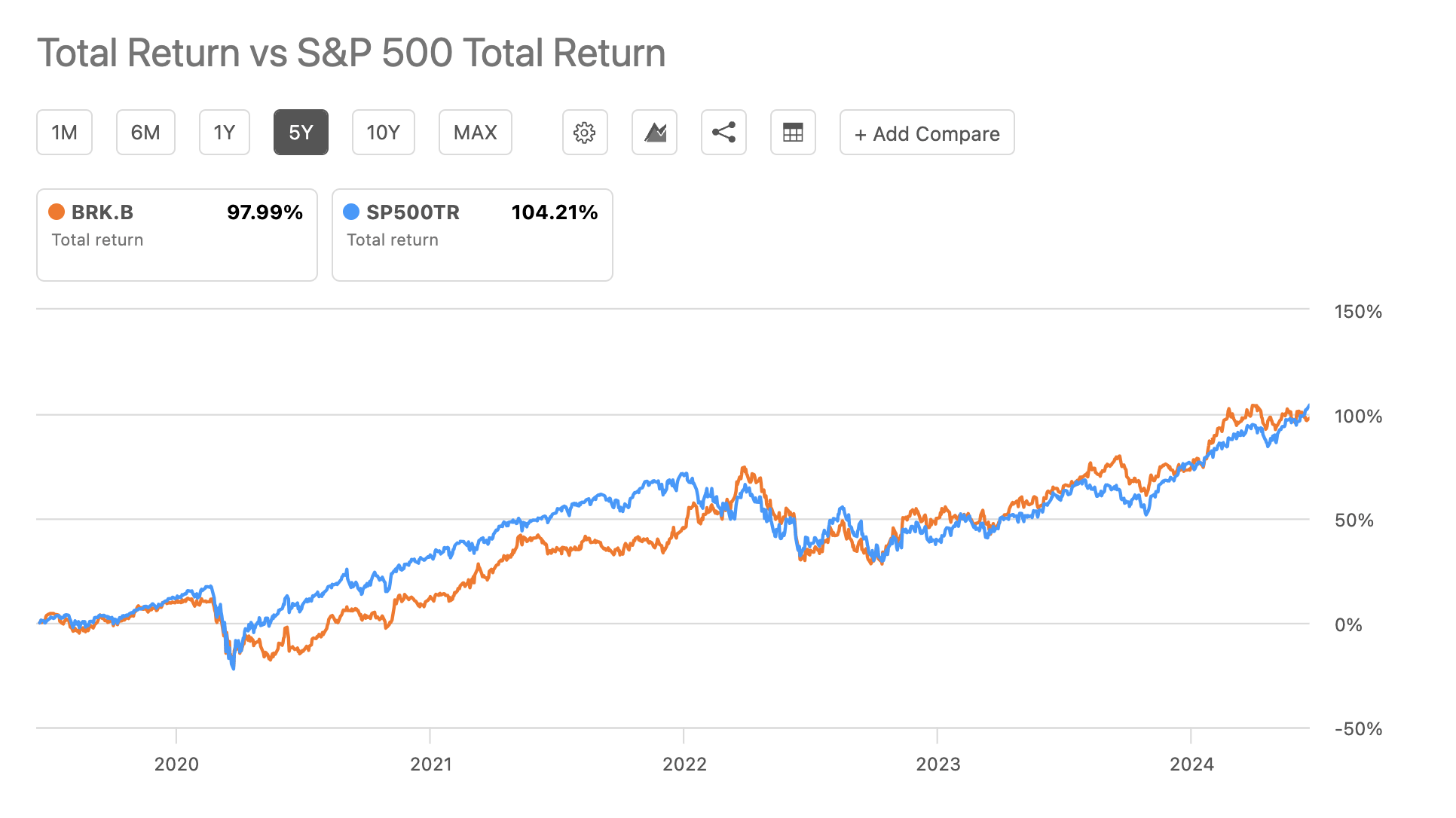

The biggest issue for investors is realizing Warren Buffett is nearly 100 years old now, and the company no longer makes big bets to generate outsized gains. Over the last 5-years, Berkshire Hathaway has generally tracked the investments of the S&P 500 index, with a slight under performance over the period.

Source: Seeking Alpha

Naturally, most investment funds have struggled to beat the major indexes with heavy weights towards the Magnificent 7 stocks. Any fund without Nvidia (NVDA), Microsoft (MSFT) and others is doing well to match such a performance.

The key is for investors to understand the difference in the returns from the prior decades. In the past, Buffett was making killer deals with banks to survive the financial crisis and used his size for premium deals with the likes of OXY.

In a similar manner, Buffett would’ve made a deal with a major airline to help them survive the Covid shutdowns. Instead, Berkshire Hathaway cashed out and didn’t make any major investments during the market collapse due to Covid shutdowns

If one excludes the public investments and cash, Berkshire Hathaway has an enterprise value in the $300 billion range. The stock is fairly valued based on this view, with limited EPS growth.

The market looks at Berkshire Hathaway as trading at 20x EPS targets. These numbers are very rich for a firm unwilling to invest available cash to enhance returns.

Takeaway

The key investor takeaway is that Berkshire Hathaway and Warren Buffett don’t make the aggressive investments in order for the stock to crush the S&P 500 like in prior decades. The stock has a reasonable valuation, but due to the structure, investors are unlikely to see outsized gains anytime soon.