12 dogs for the 12% dividend yield Eriklam/iStock via Getty Images

If you clicked the title, you’re probably into high-dividend stocks. Alternatively, you may just enjoy my snarking writing. Either way, thank you for joining me.

If you didn’t click the title, I have no idea how you got here.

The first thing I want to talk about today is PMT-A and PMT-B. These two preferred shares from PennyMac Mortgage Trust (PMT) have been the center of controversy for nearly 10 months.

I’m sharing an article we wrote for subscribers here. I made a few slight edits to replace paywalled links with free links (to articles published later).

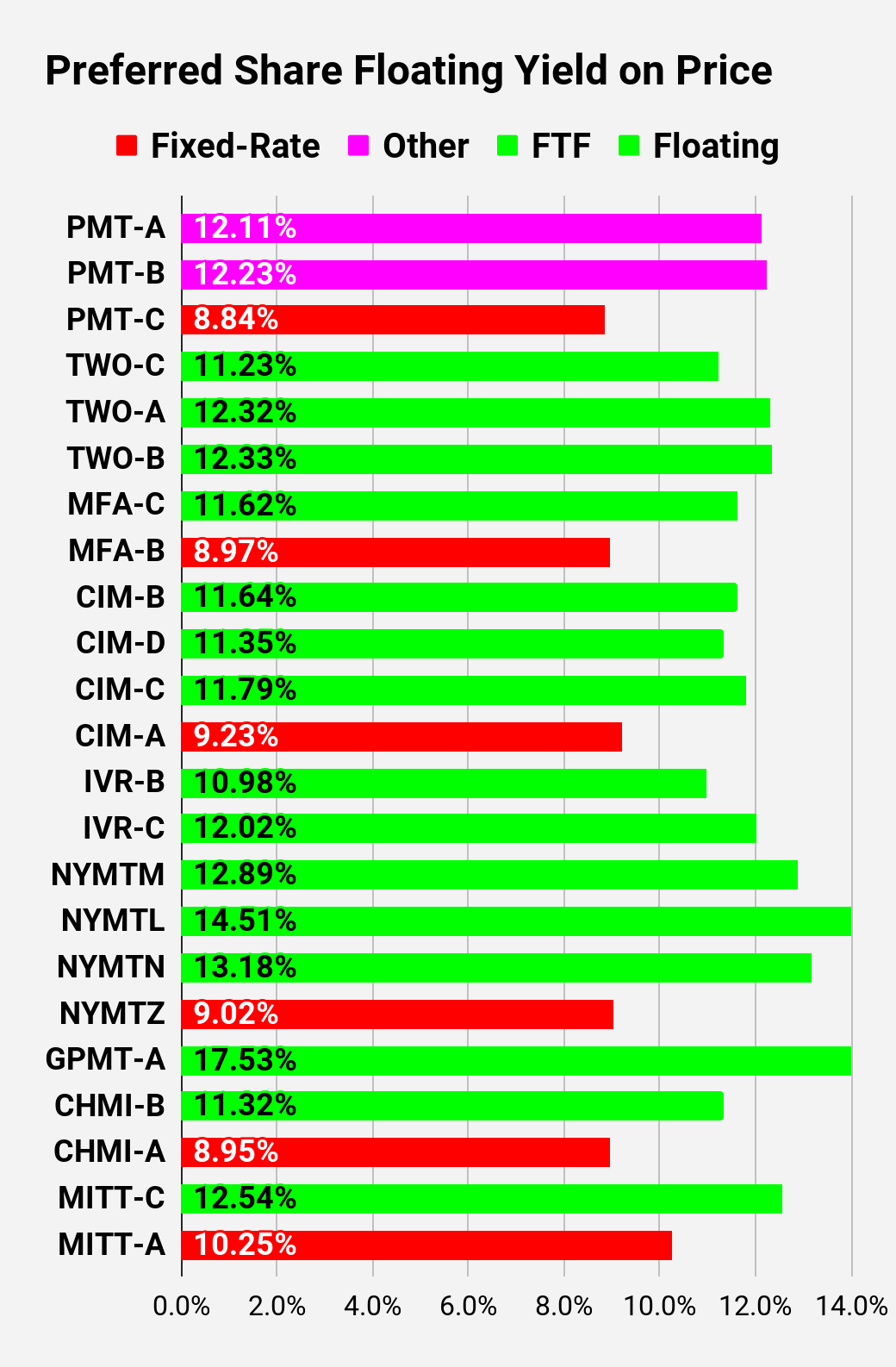

We’re covering PMT-A and PMT-B. Shares currently have a stripped yield of 8.6% and 8.43% respectively. However, if management is forced to honor the floating rate, that jumps to 12.11% and 12.23% respectively.

Start of Subscriber Post

We referenced a few times recently that we would be interested in reopening our position in the PMT preferred shares. Specifically, we were targeting PMT-B.

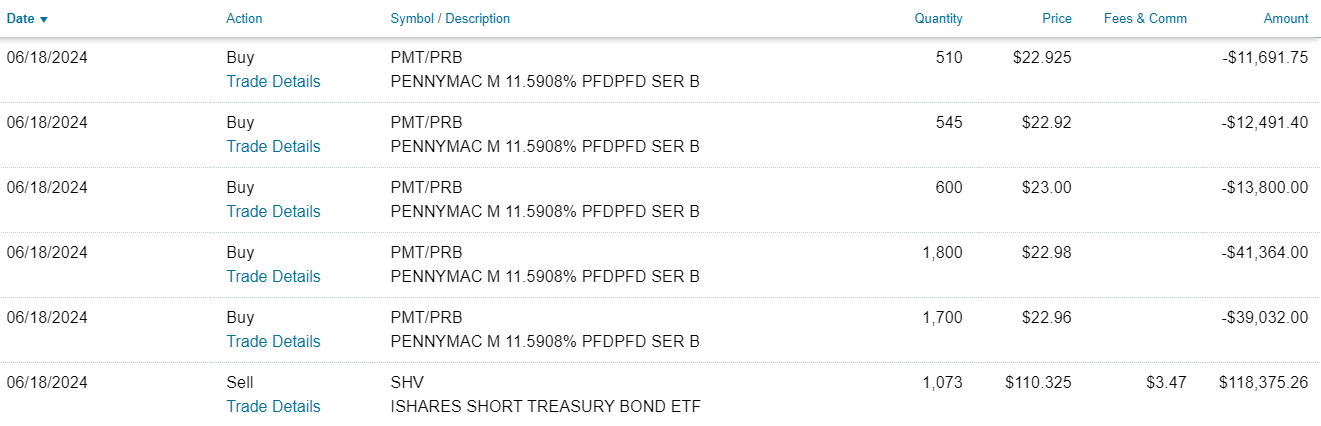

We executed multiple purchases of PMT-B:

- 1700 shares at $22.96

- 1800 shares at $22.98

- 600 shares at $23.00

- 545 shares at $22.92

- 510 shares at $22.925

Note: Execution screenshots are at the bottom, so you can always verify exact share counts, prices, and tickers.

That comes out to a total of 5,155 shares worth about $118,379 (based on my prices paid). This represents about 7.76% of the total portfolio.

This also follows through on my prior commentary that I would be looking to put some cash to work.

Note: I split this up into several transactions to prevent showing the market a big buy order. All shares went into my solo 401k account, which is a tax-advantaged account. I’m trying to shelter the potential short-term capital gains. We do not provide tax advice. I’m merely sharing which account I used.

Background in Chronological Order

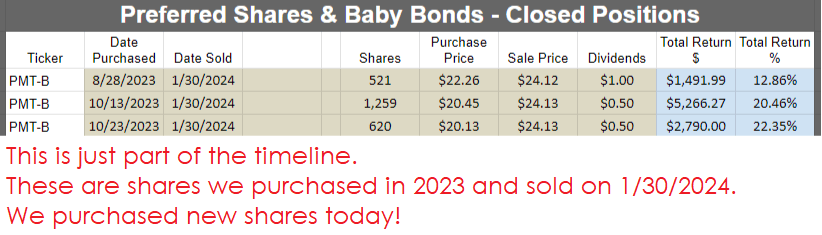

08/25/2023 (Friday): PennyMac Mortgage Trust (PMT) asserted that the LIBOR Act would cause their fixed-to-floating preferred shares to become “fixed-to-fixed” shares. We spent the entire evening researching.

08/26/2023 (Saturday): After another solid day of work, despite no experience as a lawyer or judge, we declared that PMT appeared to be wrong. There is an article, but it’s paywalled so we’re skipping it.

08/28/2023 (Monday): First market day after announcement. Share prices for PMT-A and PMT-B tumbled, because a fixed-rate dividend would result in a much lower yield.

08/28/2023 (Monday): We began building a position at $22.26 because we liked the price for a share that should be required to float.

08/28/2023 (Monday) evening: I provided the public release of that article: How PennyMac is Hurting Their Preferred Shareholders

08/28/2023 to 09/01/2023: We published multiple articles covering the prospectus terms for every mortgage REIT preferred share we cover.

Over the next month: I’m in touch with other investors bouncing ideas and working through the scenarios.

10/05/2023: We publish a huge update on our research.

11/17/2023: We provided the free release of that huge update: PennyMac: Good Luck Fixing The Floating Rate

Extremely Brief Review:

There are two parts to the law:

- The United States government posted: The law according to house dot gov.

- The Federal Reserve posted the final rule: Regulations Implementing the Adjustable Interest Rate (LIBOR) Act

Note: This whole thing would’ve been much quicker and easier if the law and regulations made any efficient use of tables and charts to convey information.

In that exceedingly long article, we demonstrated:

- Securities could be classified into 3 different categories.

- We found ample evidence that the correct category for PMT-A and PMT-B was “Category 2”. Under that definition, they would be using SOFR + .26161%.

- We concluded by demonstrating that even if PMT-A and PMT-B were classified as “Category 1”, it would prevent the LIBOR Act from covering them.

- If the LIBOR Act didn’t apply to them, because they had sufficient backup provisions, then they would be forced to use Synthetic LIBOR while it exists.

- Synthetic LIBOR shall exist until September 30, 2024 (according to The Financial Conduct Authority, which has the authority to make that decision).

10/13/2023: We purchased more shares of PMT-B at $20.45.

10/23/2023: We purchased more shares of PMT-B at $20.13.

11/17/2023: We provided our research to the public for free.

1/30/2024: Market prices for PMT-B had rallied past $24.00. At this point, that was comparable to other shares with upcoming floating dates. The market was pricing shares as if there was a very high probability that they would float on-time and with zero issues. We closed our positions for a healthy gain.

There are the trades:

The REIT Forum

At this point (1/30/2024), we believed the most likely method to fix PMT would be a lawsuit or enforcement action by regulators. We planned to inform regulators and teach other investors how to alert regulators to draw more attention to it.

06/17/2024 (evening): A lawsuit against PMT was announced. The lawsuit specifically targets PMT’s attempt to fix the rate on their preferred shares.

06/18/2024: We have a catalyst in play. We were hoping for enforcement action or a lawsuit. We have the lawsuit, which should draw more attention to it. I see no reason not to alert regulators as well.

I plan on contacting the plaintiff’s legal counsel to share a free copy of our article.

The claim they referenced focuses on our first assertion:

- PMT-A and PMT-B were “Category 2” securities and were converted to use SOFR + the spread by force of law.

However, they might as well have the backup ready. Even if PMT-A and PMT-B were ruled as “Category 1”, synthetic LIBOR would come into play.

Note: When PMT declared the shares would remain fixed, they provided a pathetic explanation of how they reached their decision. Other mortgage REITs with very similar terms all came to the opposite conclusion.

Valuation

We’re looking at about an 8.7% to 8.8% stripped yield based on the fixed-rate dividend. PMT-B enters the floating rate period (which is a defined date range and cannot be changed by the company) on 6/15/2024.

If PMT is forced to honor the contract, as we understand it, then the floating yield would be around 12.7%.

That’s a great deal. At that rate, I think PMT would probably call the shares.

Given that PMT is facing the legal cost of a trial and I believe they would most likely lose, the cheapest option available to them is to call the shares (and pay the appropriate rate for all days prior to the call). By calling the shares and paying the appropriate rate, they could argue for dismissing the lawsuit. That’s cheaper than losing a court case, being forced to pay the appropriate rate, and then calling shares because the rate is so high.

PMT-B has been trading between 94.7% and 95.6% of our target buy-under price.

That gives it one of the largest discounts to target prices, especially or shares with a lower risk rating and a dividend that SHOULD begin to float if shares are not called.

Not For Everyone

This play is not for everyone.

Some investors may not:

- Be comfortable with PMT’s management after that stunt.

- Want the risk of investing in a share that could still end up with a fixed rate.

- Like the potential delay while waiting for resolution.

- Want to invest anything given the return on cash and the valuation of the S&P 500 or relatively thin credit spreads in many parts of the economy.

However, it fits my risk tolerance well.

I’m not a lawyer, and I’m not giving legal advice.

I like PMT-B at this price.

I think the market is treating shares as if there is a very high probability that they remain fixed rate.

I believe there is a high probability that they will float. The lawsuit was precisely the kind of catalyst we were hoping for.

Conclusion

Things appear to be playing out nicely.

We’re getting another opportunity to buy shares.

We closed our prior position when the market was pricing shares as if they were almost certainly going to float.

Since then, share prices declined while many of the other preferred shares rallied to trade around $25.00.

The disparity in prices today suggests that relatively few investors believe the rate will float.

Surely some investors agree the shares will float, but it seems to be a much more rare view today.

That leads to a favorable risk/return profile.

If share prices dip further, I could add a bit more to our position. However, putting over $106k to work this morning seems like a good chunk.

I think as more investors become aware of the lawsuit, we may see prices trend upwards as investors evaluate whether these shares are really going to remain at a fixed-rate dividend.

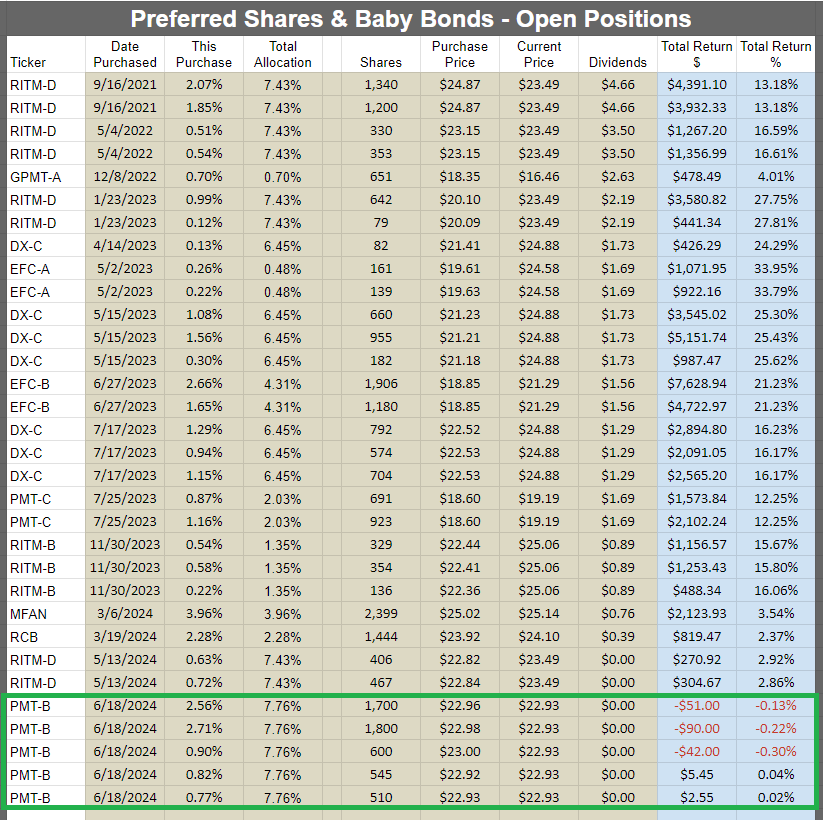

Open Positions

The REIT Forum

Execution

Below is the screenshot from my Schwab account:

Charles Schwab

End of Subscriber Article

I include those screenshots because some analysts like to post “trades” where they didn’t actually buy or sell a security in a real account.

Note: A “real” account is one where you insert money and can withdraw money. Trades only occur if they are actually executed in the stock market.

With a screenshot, there’s no doubt about my action.

I use a few ETFs for Treasuries. They are an easy way to earn a respectable yield on my cash. The iShares Short Treasury Bond ETF (SHV) is one of them.

PMT-A and PMT-B are both viable securities for this trade. I used PMT-B because at the time it was quite a bit cheaper than PMT-A.

Both securities are still reasonably attractive, despite an increase in the share prices.

Fun Fact

PMT-A and PMT-B were the two shares we labeled as “FTL” in our subscriber spreadsheets.

FTF stands for “fixed-to-floating”. That’s a very common designation.

FTL stands for “fixed-to-lawsuit”. It was a special label created just for PMT’s preferred shares.

We applied that label back around late August of 2023.

Now the lawsuit has arrived (note: huge paywall, just linking for evidence).

Preferred Share Guide

If you’re interested in preferred shares, make sure to check out our huge free guide to preferred shares.

Many readers have told me it’s their primary resource for learning how preferred shares work.

It took a few years to bring it all together, so I hope readers enjoy it.

Stock Table

We will close out the rest of the article with the tables and charts we provide for readers to help them track the sector for both common shares and preferred shares.

We’re including a quick table for the common shares that will be shown in our tables:

If you’re looking for a stock that I haven’t mentioned yet, you’ll still find it in the charts below. The charts contain comparisons based on price-to-book value, dividend yields, and earnings yield. You won’t find these tables anywhere else.

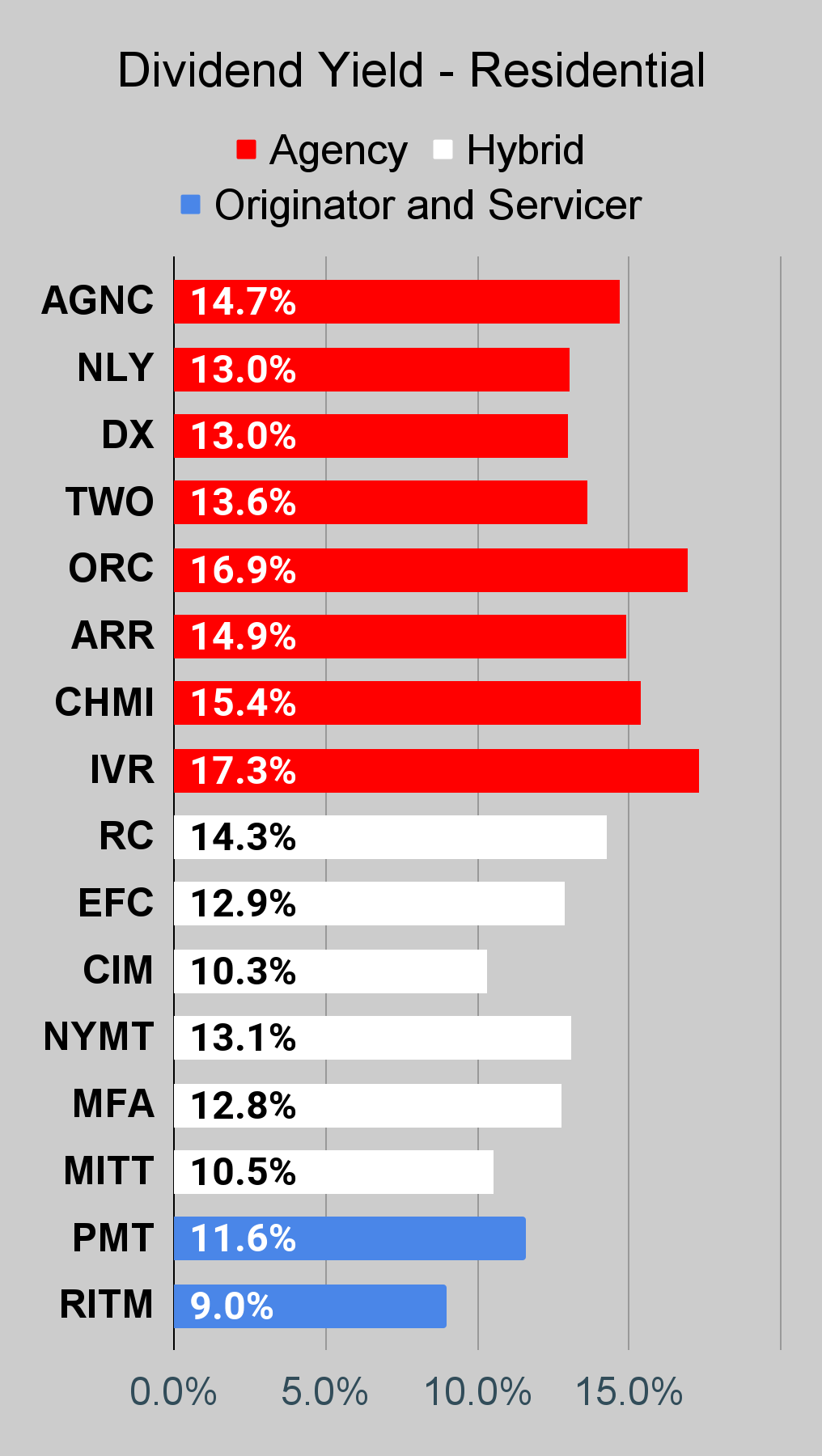

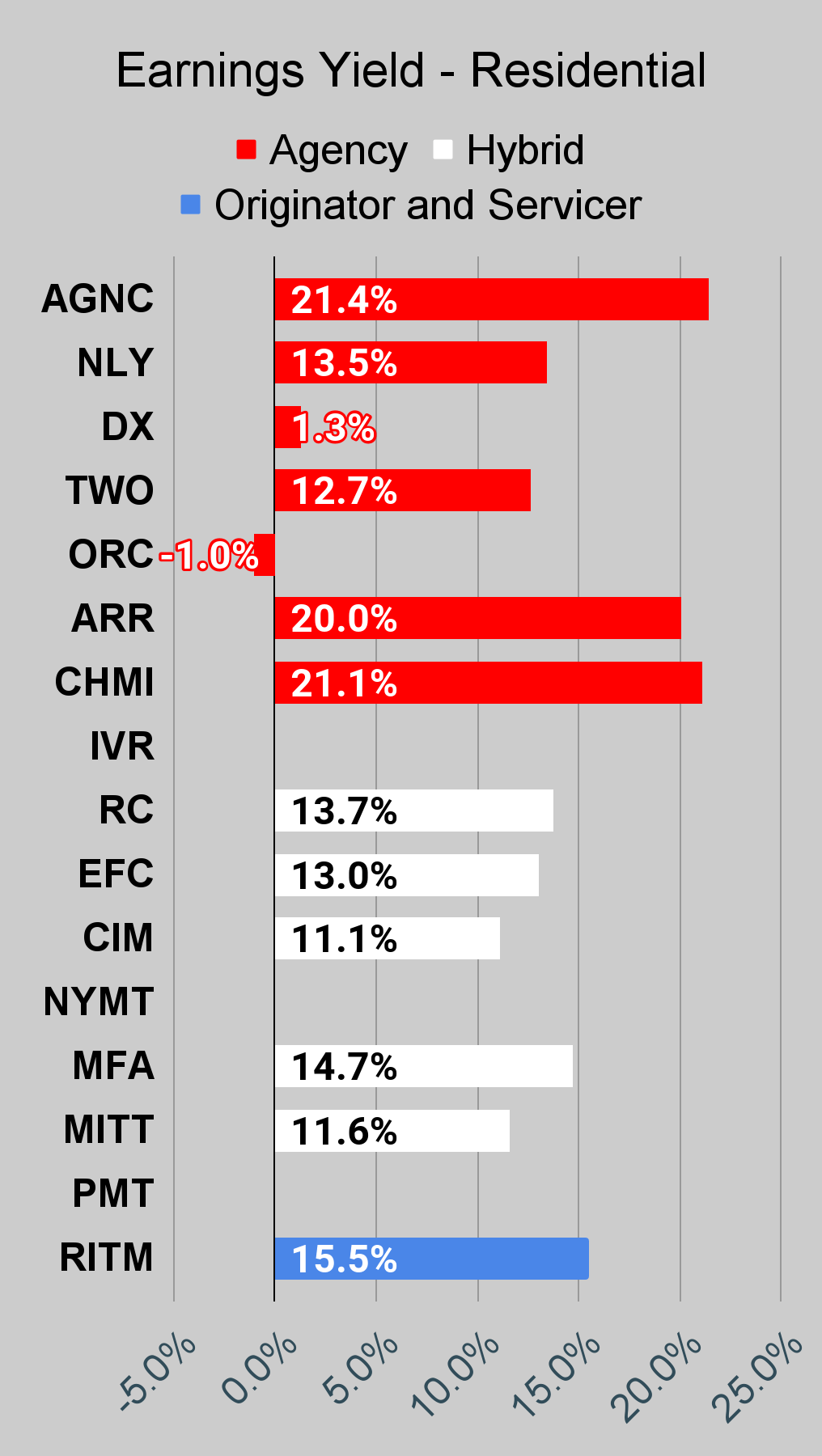

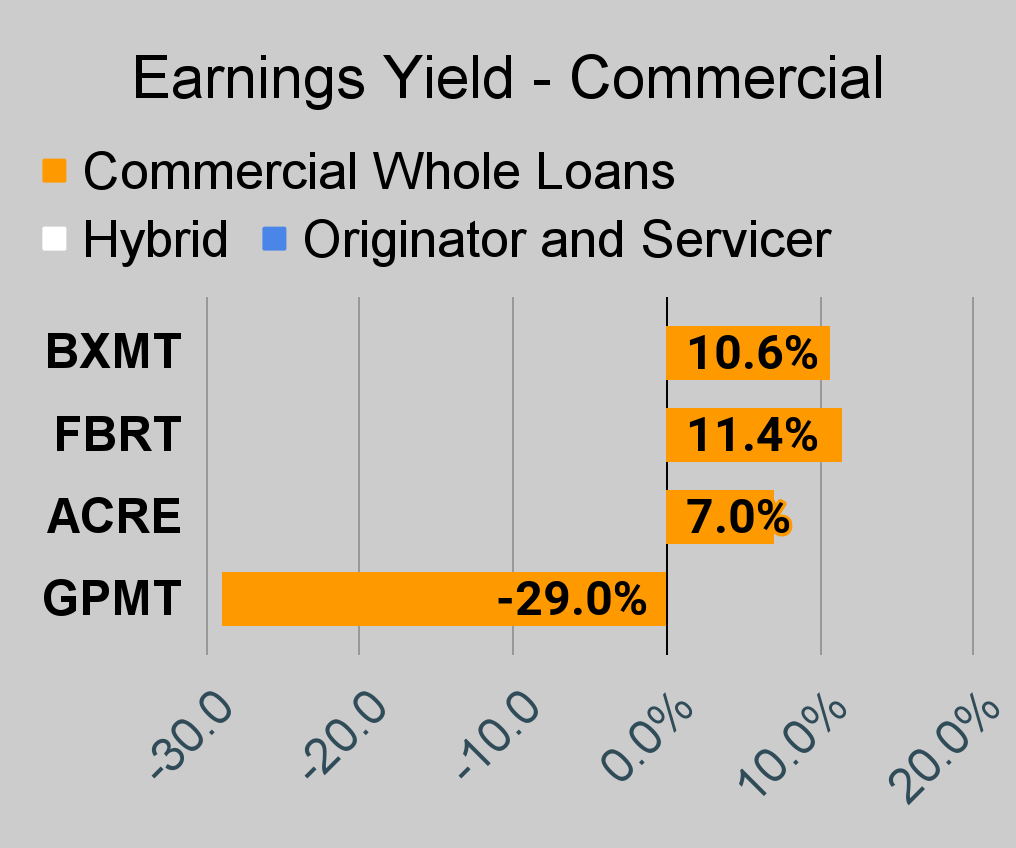

For mortgage REITs, please look at the charts for AGNC, NLY, DX, ORC, ARR, CHMI, TWO, IVR, CIM, EFC, NYMT, MFA, MITT, AAIC, PMT, RITM, BXMT, GPMT, WMC, and RC.

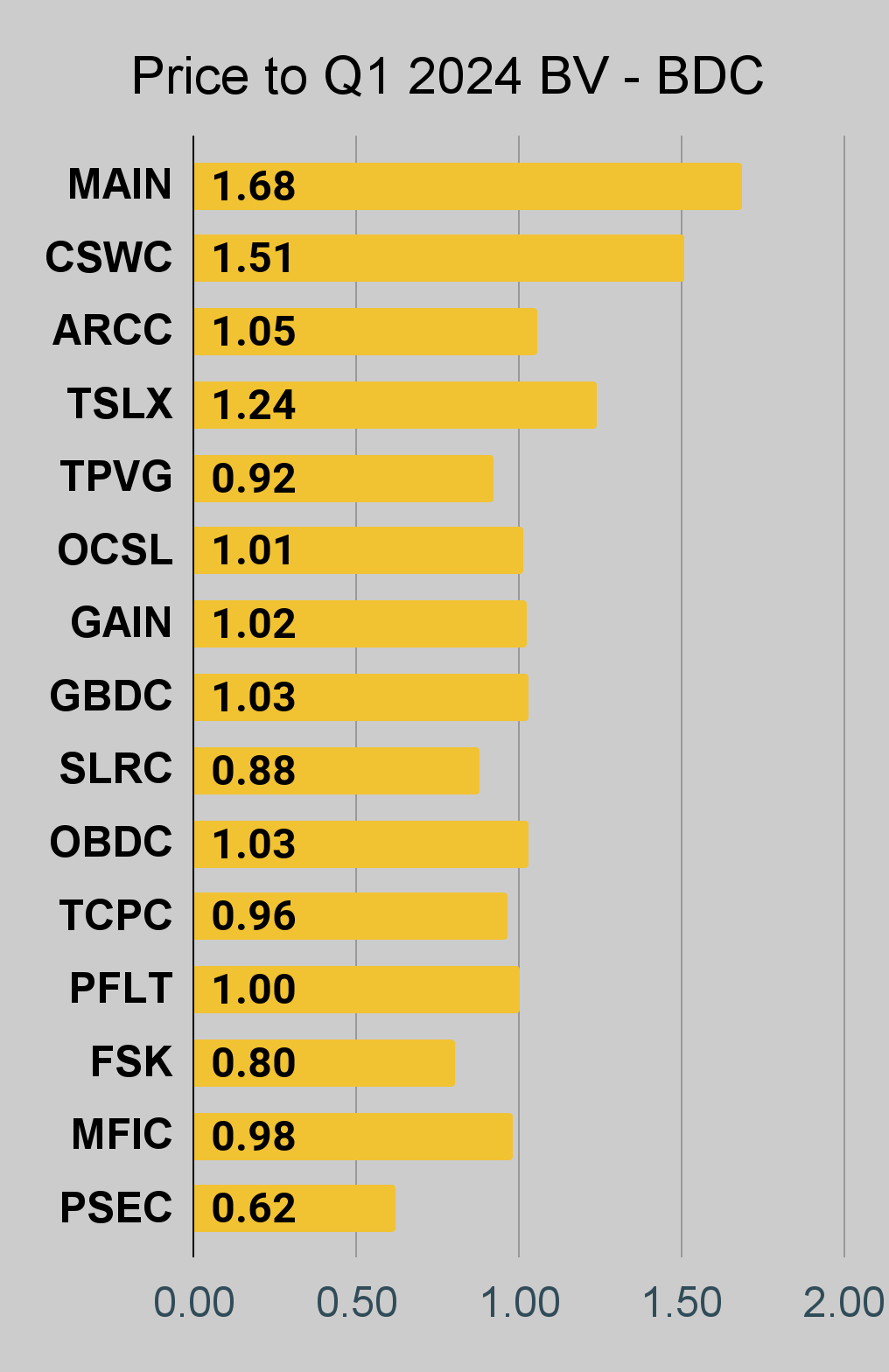

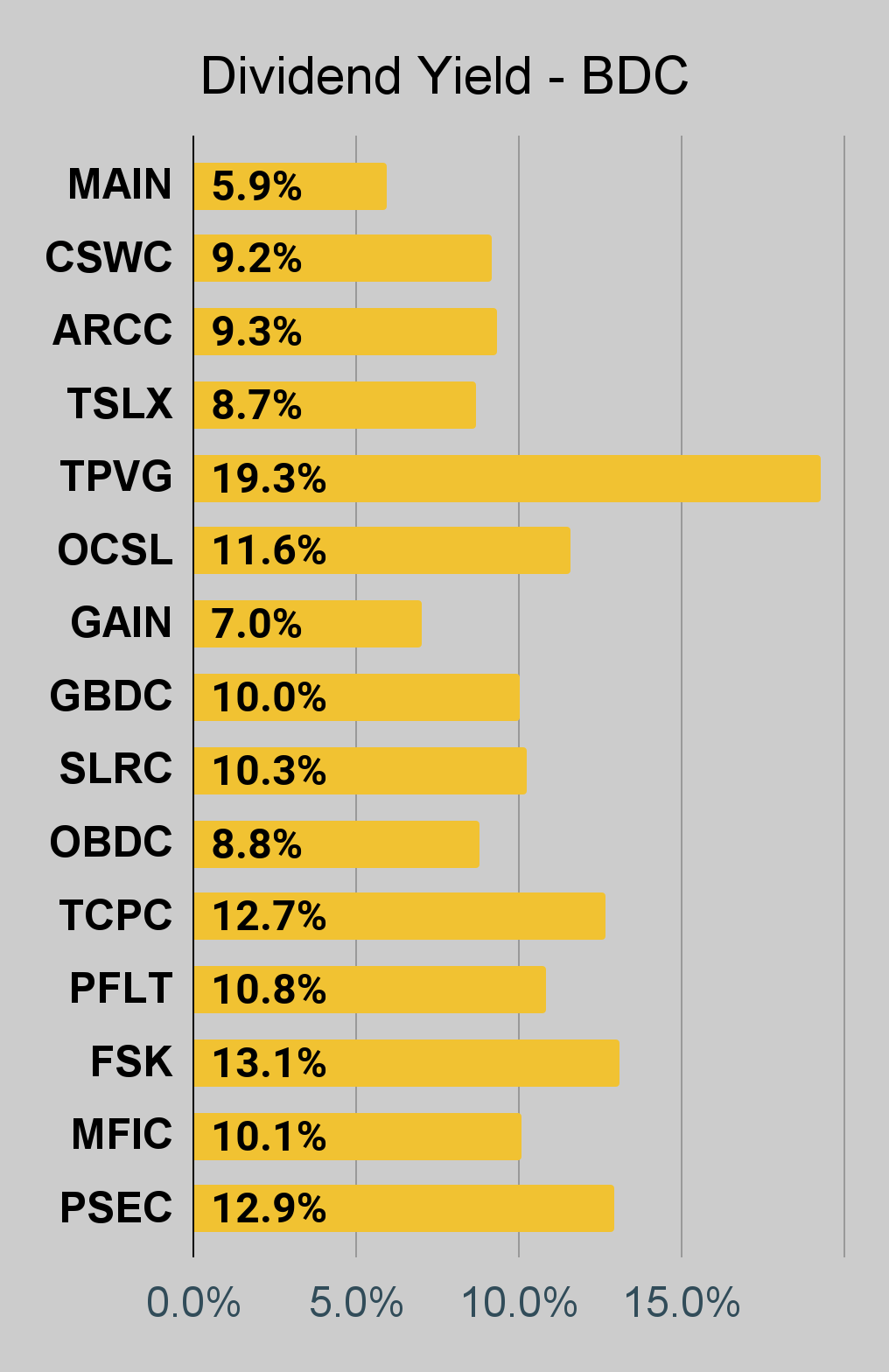

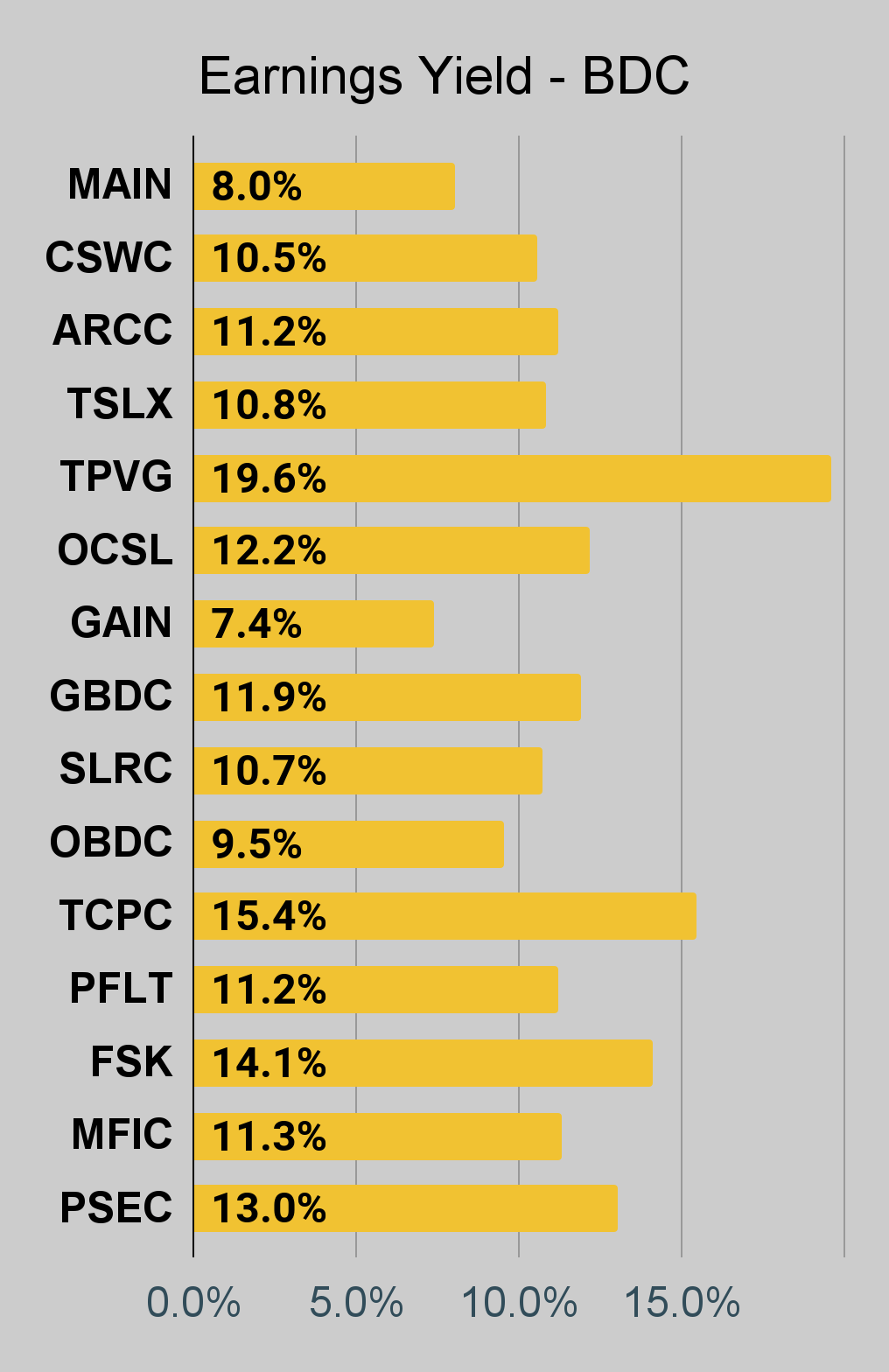

For BDCs, please look at the charts for MAIN, CSWC, ARCC, TSLX, TPVG, OCSL, GAIN, GBDC, SLRC, OBDC, PFLT, TCPC, FSK, PSEC, and MFIC.

This series is the easiest place to find charts providing up-to-date comparisons across the sector.

Notes on Chart Sorting

Within each type of security, the sorting is usually based on risk ratings. However, it is quite common to have a few shares that are tied. When the shares are tied for risk rating, the sorting becomes arbitrary. There may occasionally be errors where a share’s position is not updated quickly following a change in the risk rating. That can happen because the charts come from a separate system. When I update the system we use for members, it doesn’t change the order in the charts.

When I say “within each type of security”, I’m referencing categories such as “agency mortgage REITs”. The “hybrid mortgage REITs” are all listed after the “agency mortgage REITs”. However, that does not mean RC (lowest hybrid) has a higher risk rating than the highest agency mortgage REIT. Each batch is presented by themselves.

PMT and RITM are tied for risk rating.

This could probably be written better. If someone feels inclined to take it upon themselves to write a section that is objectively better at communicating these points, I would be interested in using it. I’m grateful to have the best readers on SA. I attribute this to self-selection bias. I include enough things to offend the dumb people that I’m left with the best readers.

Note: The chart for our public articles uses the book value per share from the quarter indicated in the chart. We use the current estimated (proprietary estimates) book value per share to determine our targets and trading decisions. It is available in our service, but those estimates are not included in the charts below. PMT and NYMT are not showing an earnings yield metric as neither REIT provides a quarterly “Core EPS” metric. Presently, a few other REITs also have no consensus estimate.

Second Note: Due to the way historical amortized cost and hedging is factored into the earnings metrics, it is possible for two mortgage REITs with similar portfolios to post materially different metrics for earnings. I would be very cautious about putting much emphasis on the consensus analyst estimate (which is used to determine the earnings yield). In particular, throughout late 2022 the earnings metric became less comparable for many REITs.

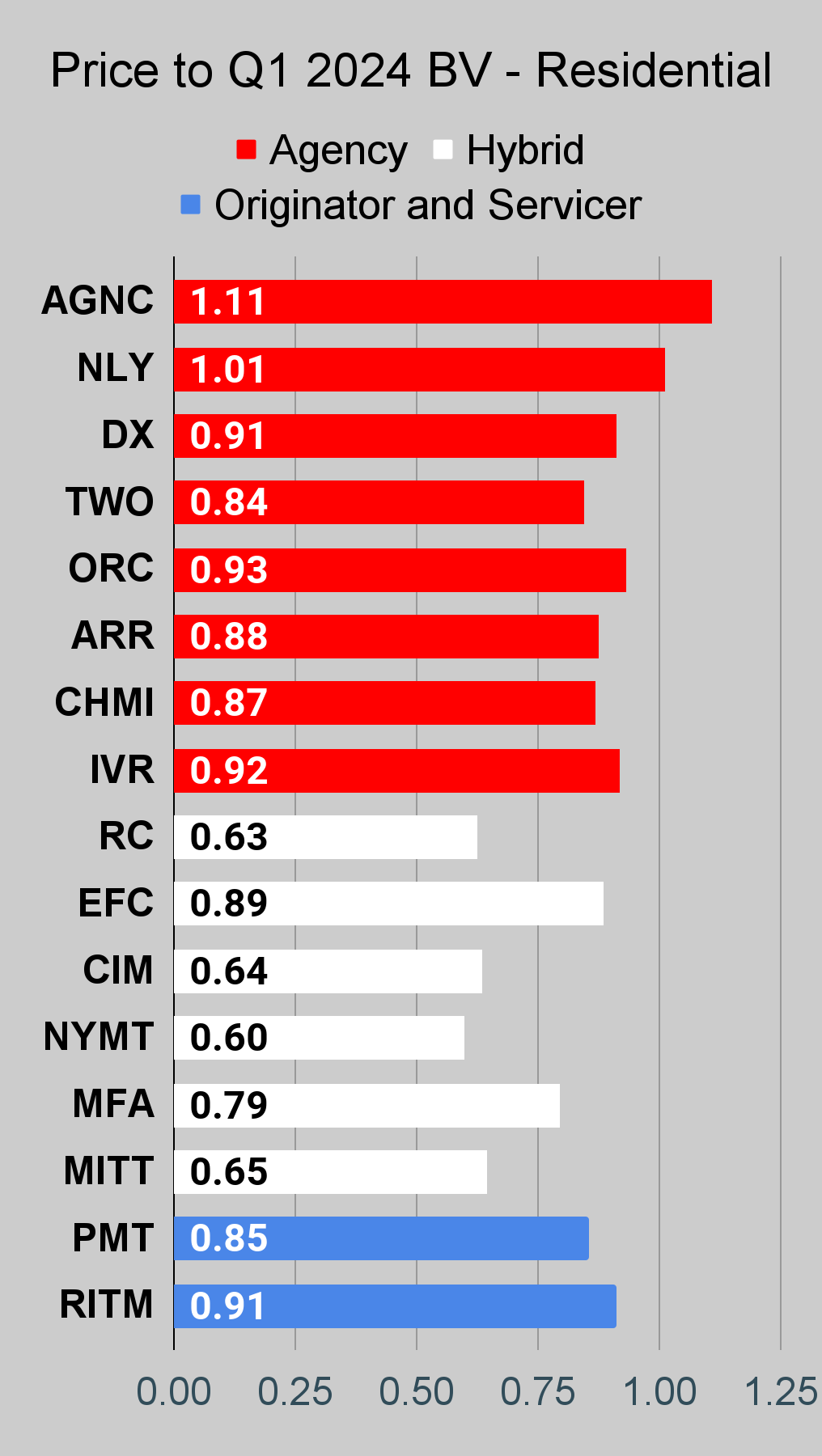

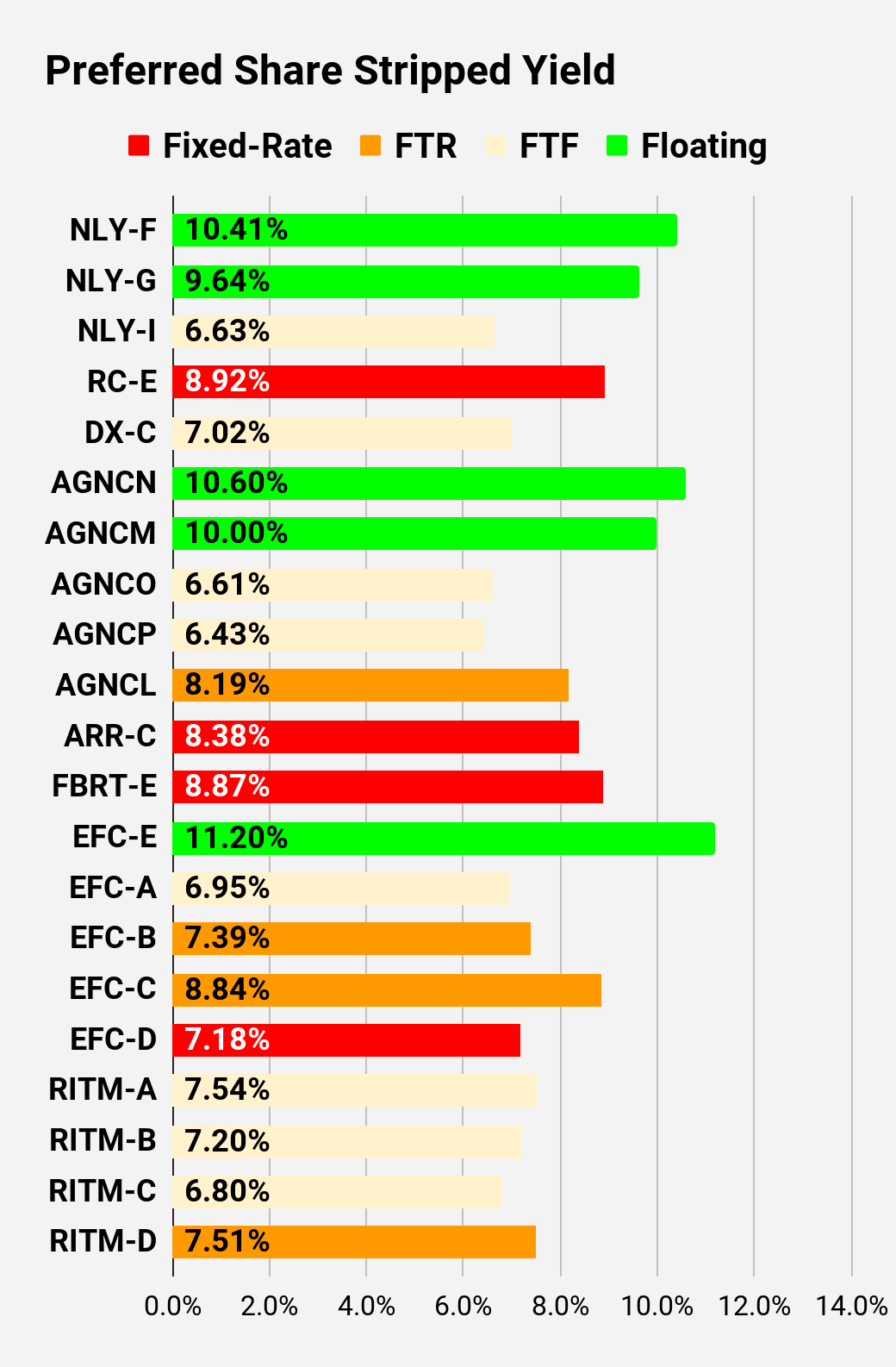

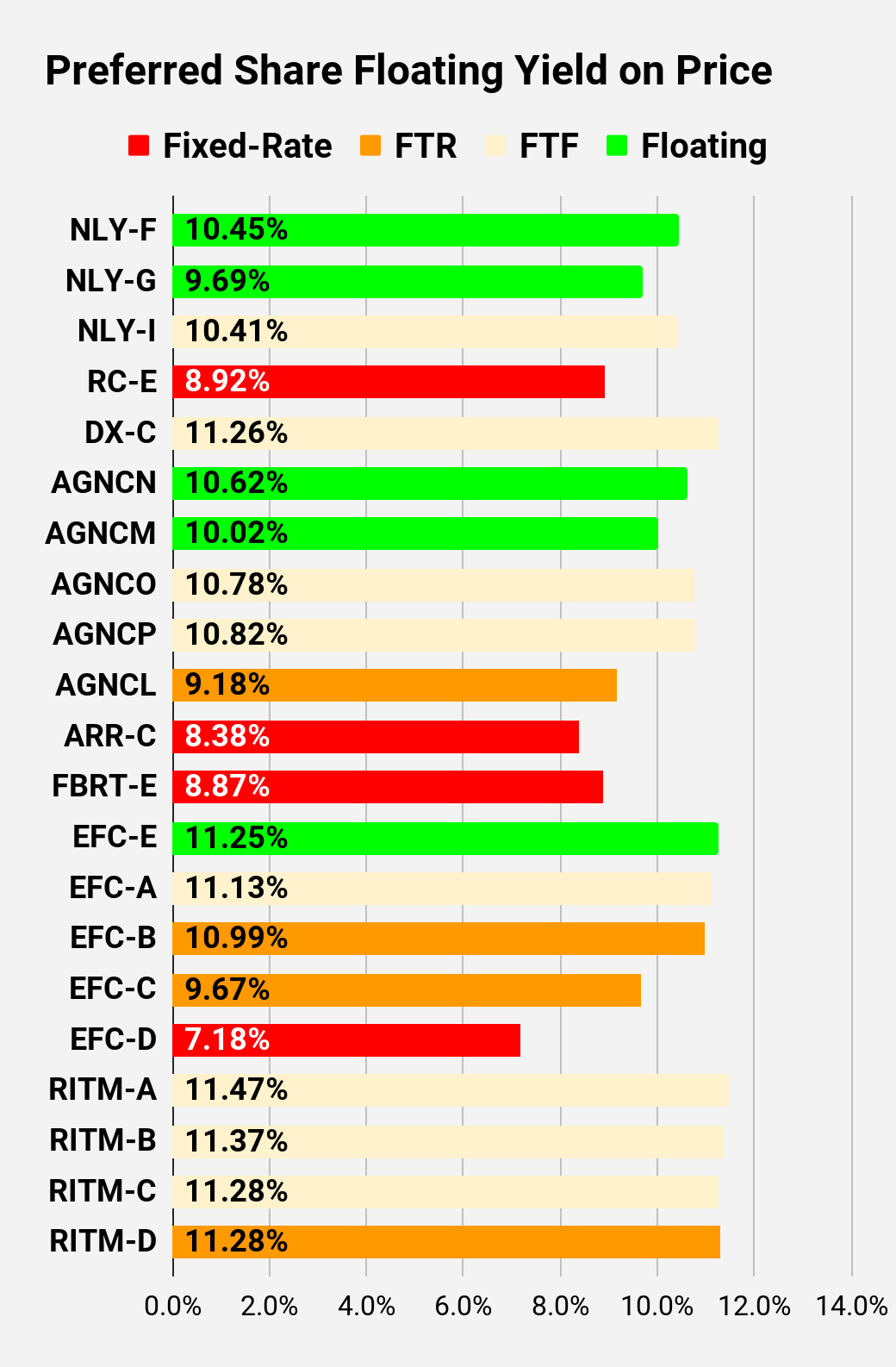

Residential Mortgage REIT Charts

The REIT Forum |

The REIT Forum |

The REIT Forum |

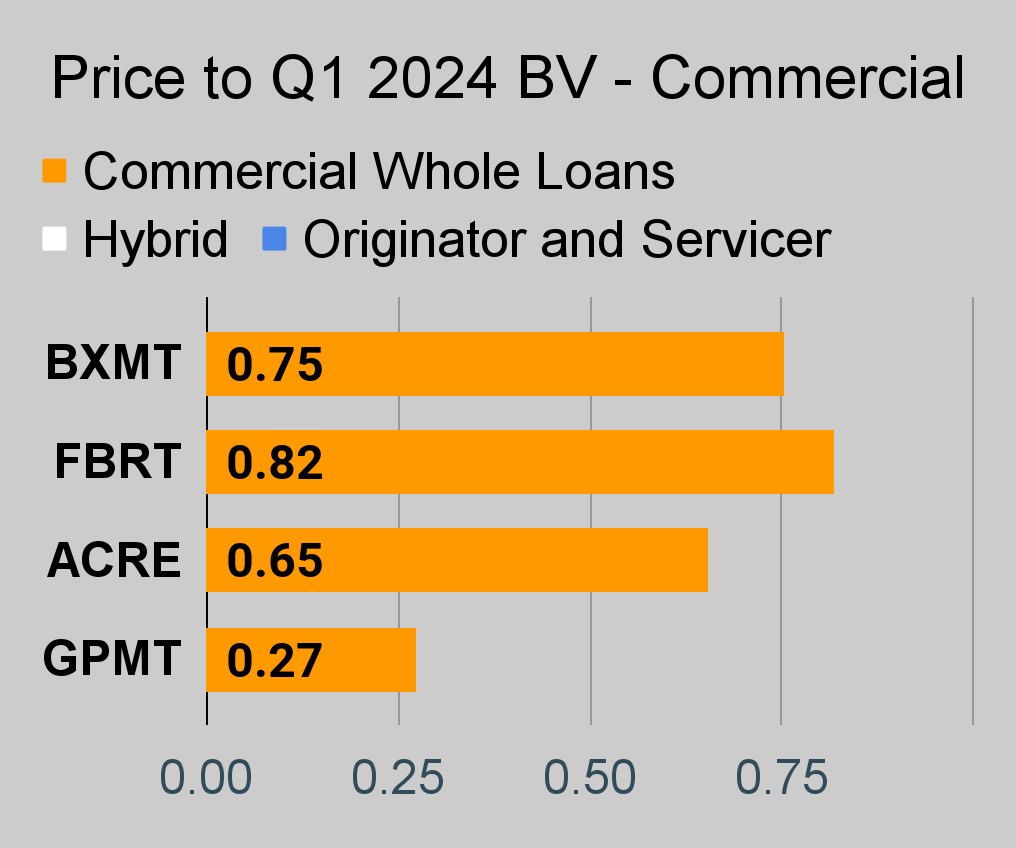

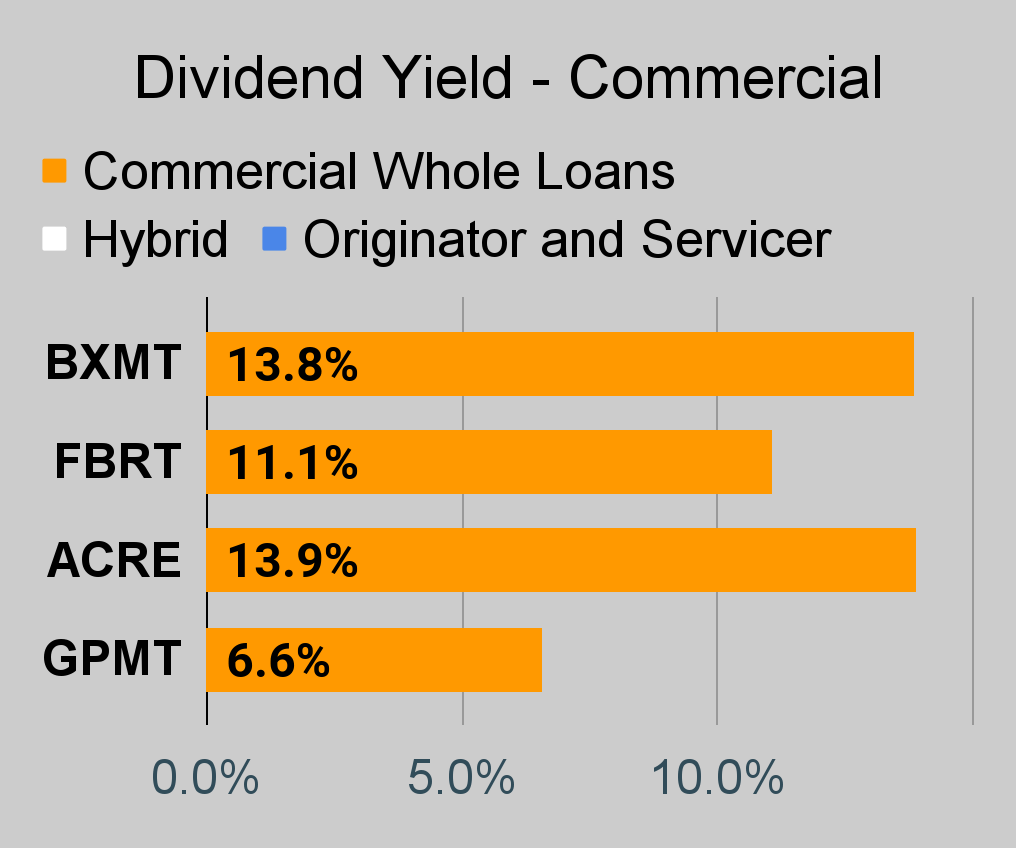

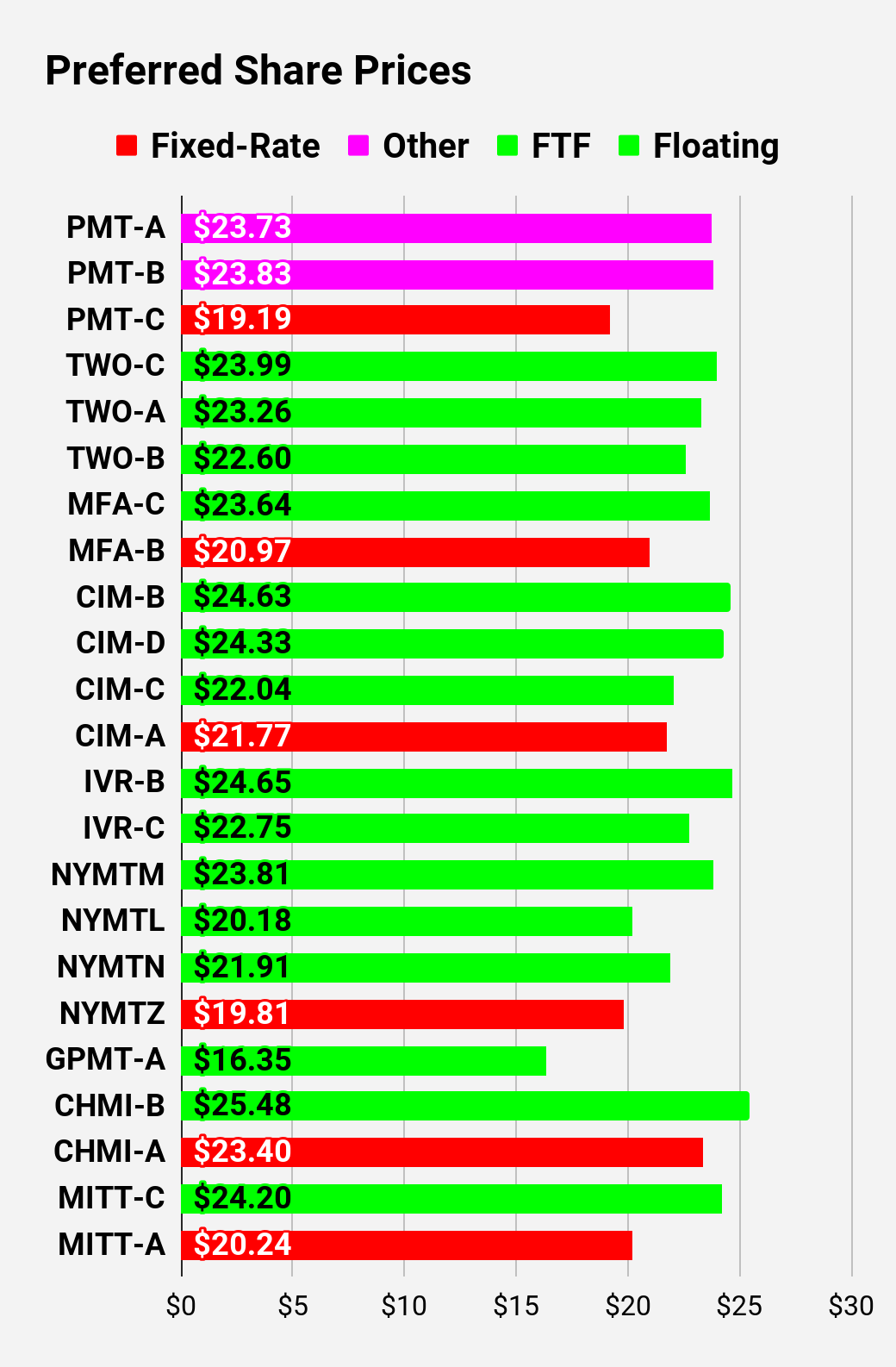

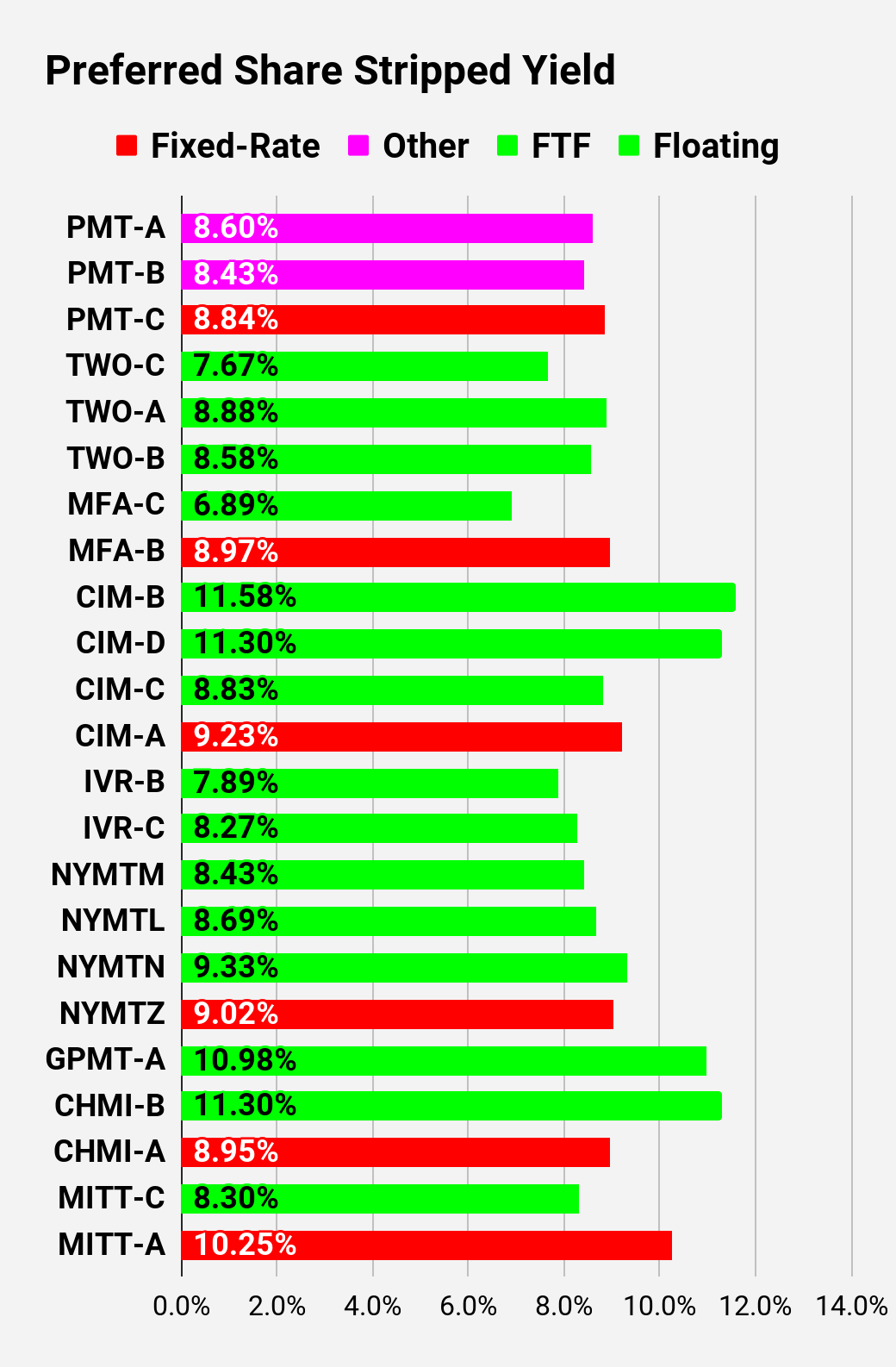

Commercial Mortgage REIT Charts

The REIT Forum |

The REIT Forum |

The REIT Forum |

BDC Charts

The REIT Forum |

The REIT Forum |

The REIT Forum |

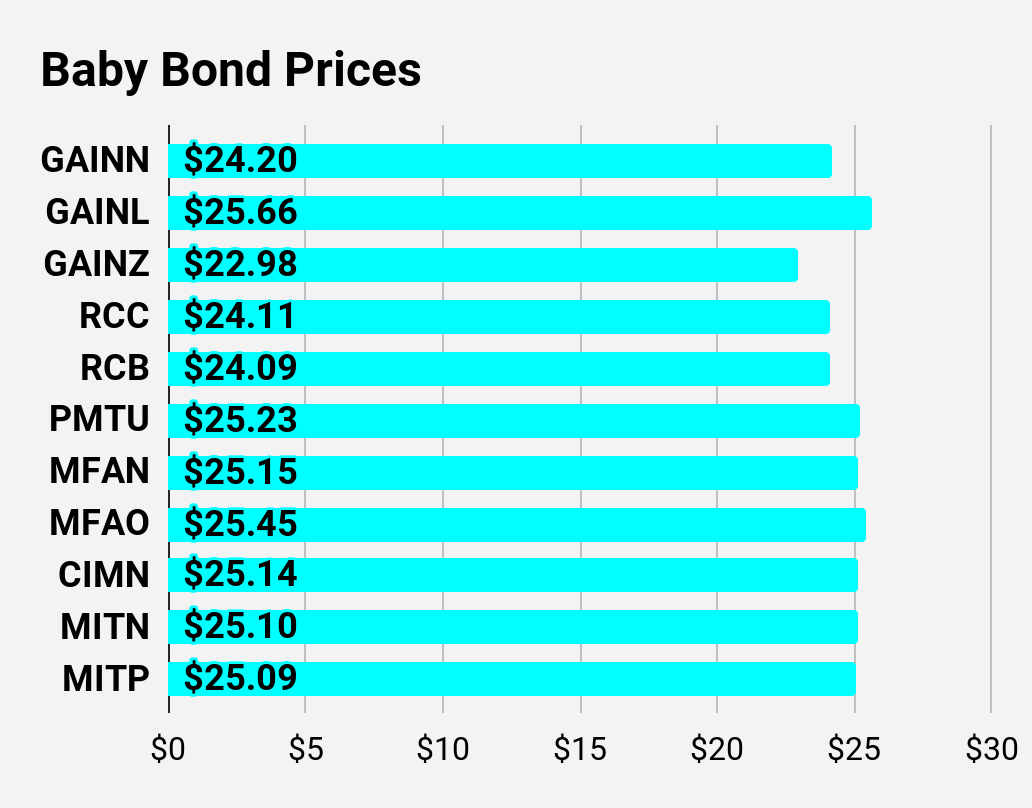

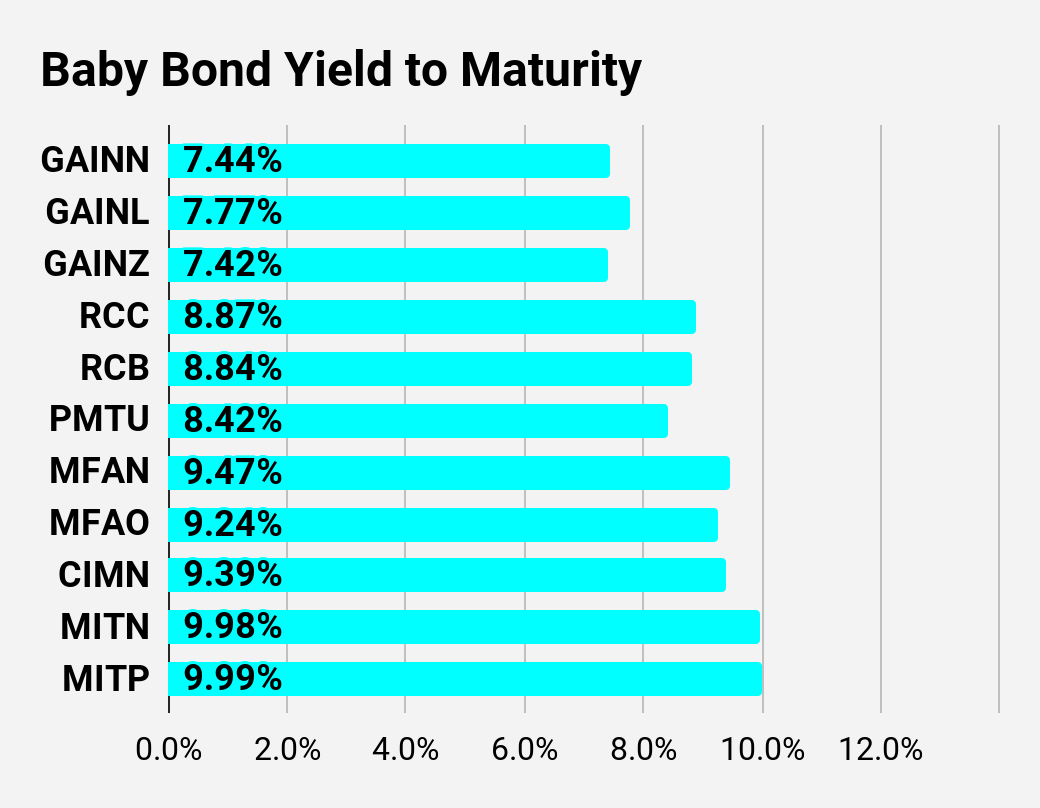

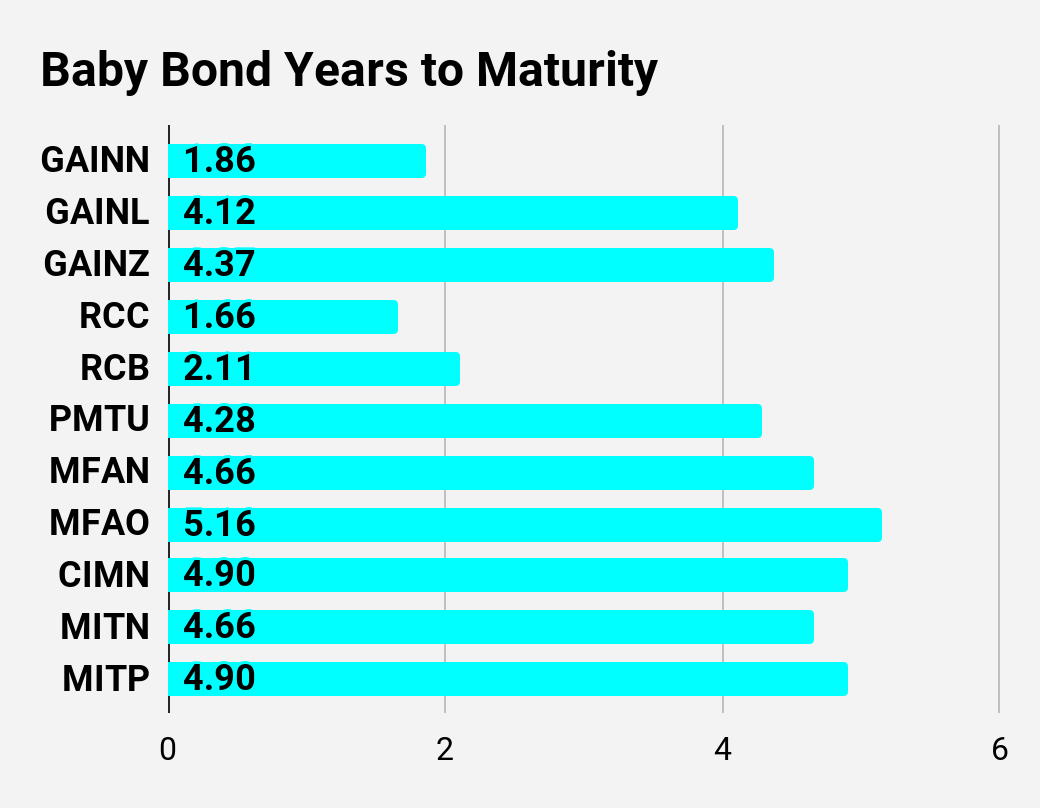

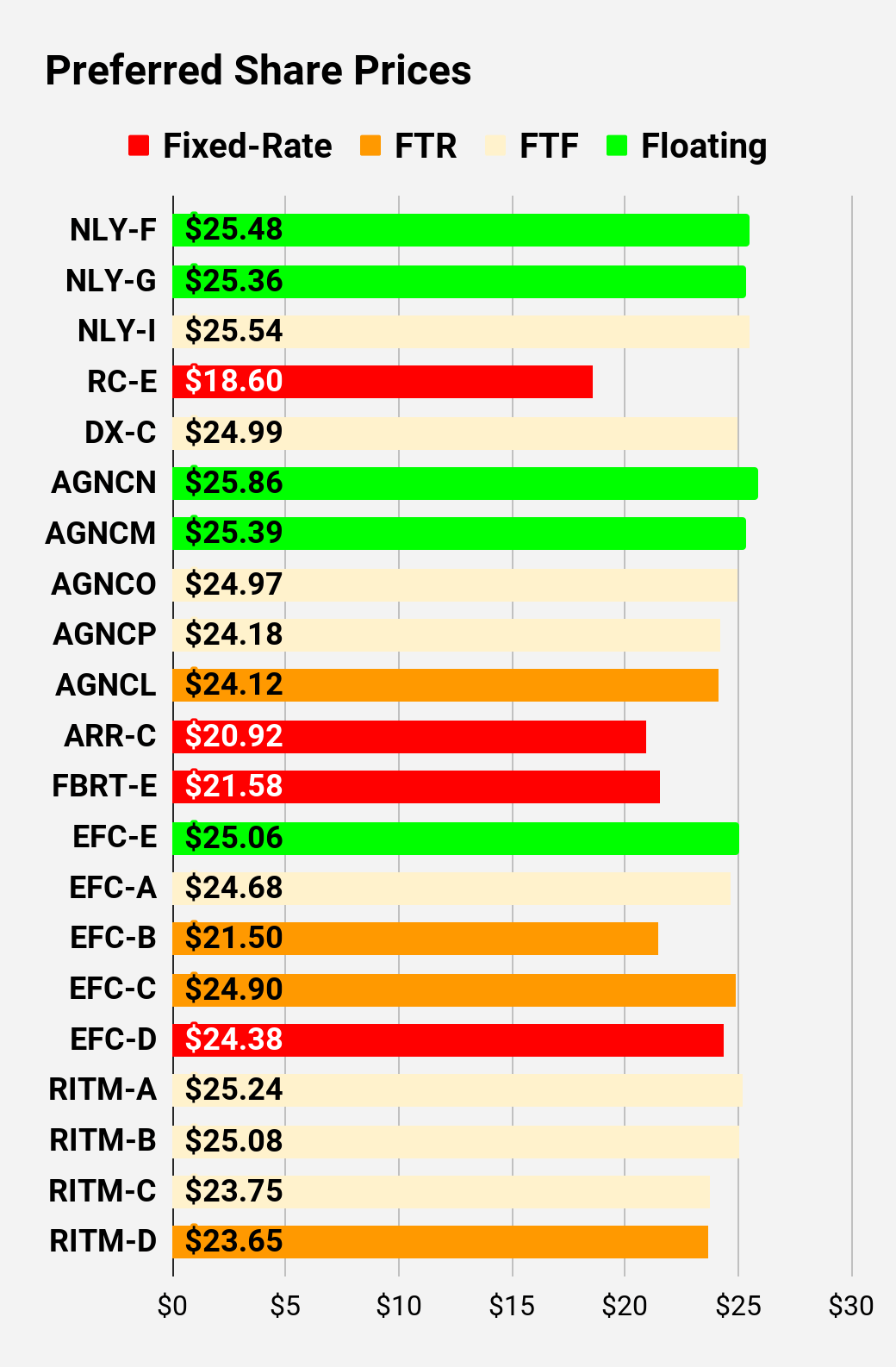

Preferred Share and Baby Bond Charts

I changed the coloring a bit. We needed to adjust to include that the first fixed-to-floating shares have transitioned over to floating rates. When a share is already floating, the stripped yield may be different from the “Floating Yield on Price” due to changes in interest rates. For instance, NLY-F already has a floating rate. However, the rate is only reset once per 3 months. The stripped yield is calculated using the upcoming projected dividend payment and the “Floating Yield on Price” is based on where the dividend would be if the rate reset today. In my opinion, for these shares the “Floating Yield on Price” is clearly the more important metric.

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

Note: Shares classified as “Other” are not necessarily the same. Within The REIT Forum, we provide further distinction. For the purpose of these charts, I lumped all of them together as “Other”. Now there are only two left, PMT-A and PMT-B. Those both have the same issue. Management claims the shares will be fixed-rate, even though the prospectus says they should be fixed-to-floating.

Preferred Share Data

Beyond the charts, we’re also providing our readers with access to several other metrics for the preferred shares.

After testing out a series on preferred shares, we decided to try merging it into the series on common shares. After all, we are still talking about positions in mortgage REITs. We don’t have any desire to cover preferred shares without cumulative dividends, so any preferred shares you see in our column will have cumulative dividends. You can verify that by using Quantum Online. We’ve included the links in the table below.

To better organize the table, we needed to abbreviate column names as follows:

- Price = Recent Share Price – Shown in Charts

- S-Yield = Stripped Yield – Shown in Charts

- Coupon = Initial Fixed-Rate Coupon

- FYoP = Floating Yield on Price – Shown in Charts

- NCD = Next Call Date (the soonest shares could be called)

- Note: For all FTF issues, the floating rate would start on NCD.

- WCC = Worst Cash to Call (lowest net cash return possible from a call)

- QO Link = Link to Quantum Online Page

Second batch:

Third batch:

Strategy

Our goal is to maximize total returns. We achieve those most effectively by including “trading” strategies. We regularly trade positions in the mortgage REIT common shares and BDCs because:

- Prices are inefficient.

- Long-term, share prices generally revolve around book value.

- Short-term, price-to-book ratios can deviate materially.

- Book value isn’t the only step in analysis, but it is the cornerstone.

We also allocate to preferred shares and equity REITs. We encourage buy-and-hold investors to consider using more preferred shares and equity REITs.

If you would like notifications when my new articles are published, please hit the button at the bottom of the page to “Follow” me.