andresr/E+ via Getty Images

Investment Thesis

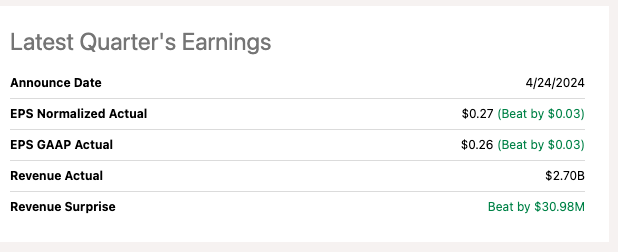

Chipotle Mexican Grill (NYSE:CMG) is a fast casual restaurant chain, that continues to experience growth. They reported strong earnings in the first quarter of 2024, exceeding consensus expectations. Revenue grew 14.1% to 2.70B, operating margin kept increasing to 16.3% and same-store sales rose 7%. The company is optimistic about the future, projecting continued growth throughout the year.

SeekingAlpha

After carefully looking into the company, I find that their strategy is multifaceted. They plan to double their store count in North America and have a new leadership team focused on international expansion, particularly in Europe. They are also investing in digital sales and plans to keep expanding their drive-thru options for faster service in a concept called Chipotlane.

Chipotle’s stock price has soared in recent years, reflecting its strong performance. The company recently completed a 50-1 stock split to make shares more “affordable” for individual investors. However, despite the split, Chipotle’s valuation still causes some areas of concern when compared to other companies in the sector.

In this article, I aim to find if Chipotle is a solid candidate for my growth at reasonable price portfolio. To accomplish this, I will explore various factors like Management effectiveness, corporate strategy, and of course valuation to determine if CMG aligns with this investment style. As you will find out at the end, I have decided to start my coverage of Chipotle with a hold as I believe the stock is slightly overvalued due to the recent positive momentum leading up to the stock split.

Management Evaluation

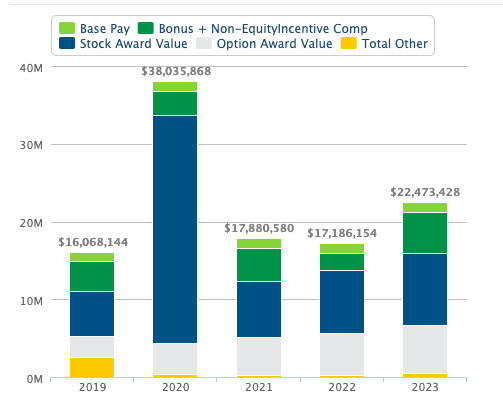

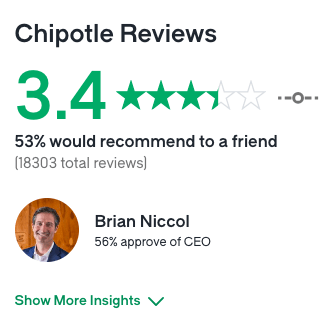

Brian Niccol, is the Chairman and CEO of Chipotle, is leading the company through an ambitious growth phase. While both Niccol and Chipotle itself have approval ratings around 50% according to Glassdoor, there seems to be room for improvement. Interestingly, Niccol’s compensation structure is unique – on average only 20% is tied to stock options, with the remaining 80% being a combination of cash salary and stock awards. This stock option compensation is low compared to other public company’s CEOs who are compensated mostly with stock options.

Salary.com

During the last earnings call: Niccol, described his growth plan:

- Doubling down in North America: Chipotle has a massive appetite for growth, aiming to nearly double its restaurant presence to 7,000 restaurants.

- European Expansion: a dedicated leadership team is focused on learning from Canada’s successful turnaround to tackle the European market.

- Menu innovation: expect a steady stream of new menu items like Barbacoa, with 1-2 additions every year.

- Digital Focus: investments are aimed at simplifying online ordering and boosting efficiency.

Niccol also revealed some promising progress. There seems to be a focus on improving “throughput” which is yielding results thanks to staffing adjustments and improved visibility tools. I’m also very positive on the transaction growth is strong across income brackets and operational improvements are strengthening broadly, especially during this inflationary period.

For the quarter, sales grew 14% to reach $2.7 billion, driven by a 7% comp. In-store sales grew by 19% over last year, as throughput reached the highest levels in four years.

Niccol mentioned that the company is leveraging data-driven marketing to re-engage less frequent customers. Without given specifics he also mentioned that the worker turnover was improving and that it reached the lowest level he has ever seen. Last year this rate was 183% meaning they are replacing the whole staff every year + 83% of the staff that was hired to replace them.

Glassdoor

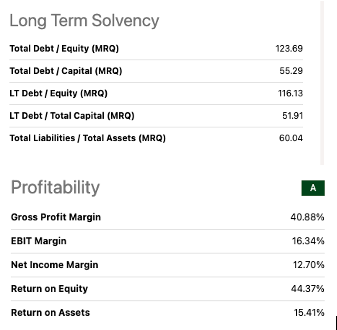

John Hartung, Chipotle’s CFO, has steered the company towards financial stability since 2002 after working for McDonald’s for 18 years. From outside, Chipotle seems to have a high D/E ratio of 100%; however, all of its debt are from capital leases as Chipotle owns all of its dining’s, which I believe gives them greater control over the supply chain and as Hurtung mentioned during the earnings call, this strategy allow us to “invest in premium ingredients” and “maintain industry leading margins”.

These three characteristics are incredibly difficult to replicate. Premium ingredients, affordable prices, and attractive margins. And this is a huge competitive advantage.

Chipotle’s strong free cash flow growth has averaged over 97% over the last 3 years and its ROE sits at just over 40% further solidify their financial health. Looking ahead, Hartung mentioned Chipotle plan to reach the top of 8%-10% annual growth by 2025. While rising ingredients costs and sticky inflation pose a threat, Chipotle’s robust cash balance, zero debt, and shareholder-friendly moves like the recent stock split and share repurchases should allow it to achieve this target.

SeekingAlpha

Overall, I find that Chipotle leadership delivered a positive message on the last earnings call. Specifically, Niccol seems to be capitalizing Chipotle strong brand by passing through inflation to consumers while others in the industry are moving in the opposite direction. Financially, Hartung highlighted an increase in margins and funding expansion through cash flows. While ROE is high, and management is focused on international expansion this strategic growth initiatives should create positive momentum despite Niccol high compensation. Given all this factors, I am rating CMG management a “Meets expectations”.

Corporate Strategy

Chipotle is still aiming for aggressive growth with a focus on opening new restaurants, especially Chipotlane drive-thrus, to reach an expansion of 8-10% annually by 2025. Their strategy hinges on fresh, customizable meals made with high-quality ingredients, appealing to health-conscious consumers.

This positions them differently from competitors offering lower prices or faster service. However, navigating higher menu prices, potential labor shortages, and rising ingredients costs remain challenges.

Here is a table I created with key differentiators between CMG and some companies in the industry:

|

Chipotle |

CAVA Group (CAVA) |

McDonald’s (MCD) |

Starbucks (SBUX) |

|

|

Corporate Strategy |

International expansion, particularly in Europe, and double stores in North America. |

Expand Footprint, focus on catering, loyalty program |

Franchise expansion, optimize existing locations |

Open new stores, mobile app focus. |

|

Advantages |

Fresh ingredients, customization, sustainability. |

Fresh ingredients, customization, healthy perception. |

Established brand, affordability, speed. |

Tight integration with Adobe marketing tools, good data management. |

|

Disadvantages |

Higher prices labor shortages. |

Limited footprint compared to Chipotle, newer brand. |

Limited health-conscious options. |

Higher prices. Wait times. |

Source: From companies’ website, presentations, SeekingAlpha

Valuation

CMG currently trades at around $62.25 on a split adjusted basis. The stock is up around 6% since its last reported earnings in late April and hovering around its all-time high of $69.26 achieved after the split announcement rally. The stock, however, is up around 36% YTD.

Now, to assess its value, I employed a 11% discount rate, this rate reflects the minimum return an investor expects to receive for their investments. Here, I am using a 5% risk free rate, combined with the additional market risk premium for holding stocks versus risk free investments, I’m using 6% for this risk premium. While this could be further refined, lower or higher, I’m using it as a starting point only to get a gauge using unbiased market expectations.

Then, using a simple 10 year two staged DCF model, I reversed the formula to solve for the high-growth rate, that is the growth in the first stage.

To achieve this, I assumed a terminal growth rate of 4% in the second stage. Predicting growth beyond a 10-year horizon is challenging, but in my experience, a 4% rate reflects a more sustainable long-term trajectory for mature companies that should be close to historical GDP growth. Again, these assumptions can be higher or lower, but from my experience I will use a 4% rate as a base case scenario due to the nature of their business. The formula used is:

$62.25 = (sum^10 FCF (1 + “X”) / 1+r)) + TV (sum^10 FCF (1+g) / (1+r))

Solving for x = 30.5%

This suggest that the market currently prices CMG FCF to grow at 30.5%. According to Seeking Alpha analyst consensus FCF over the next 2 years at 27.18%. Therefore, it seems that CMG is overvalued on a fundamental basis.

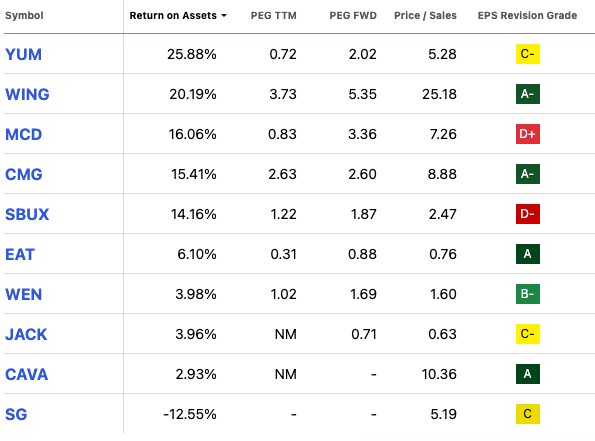

Further, I’ll also look at their price earnings to growth (PEG) ratio sits at 2.60x -versus a sector median of 1.48x- implying the stock price is overvalued. Also, their price to sales (P/S) ratio also seems overvalued but when compared to a select group of companies, highlighted below, that are considered leaders in the industry, this overvaluation seems to be in line.

SeekingAlpha

However, even if there is some overvaluation in the market, I believe earnings should catch up to this valuation at some point, unless there is an economic slowdown or if interest rates stay higher for longer, impacting consumer spending.

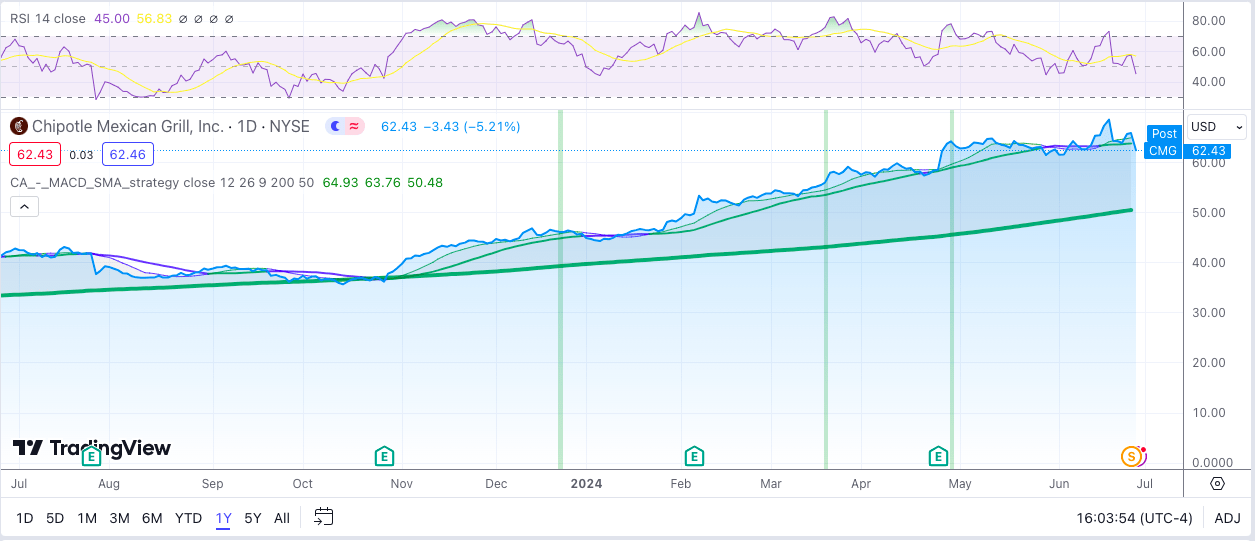

Technical Analysis

CMG has been on a positive momentum this year. However, on a technical basis, the stock looks appropriately valued, its 1-year average RSI is in a neutral territory at 45 and under its 14-day moving average of 56, indicating the stock price might be changing trends.

TradingView

CMG has formed a strong support level at just shy of $60 and a resistance level at just under $70, the stock should move around this band awaiting more news and breach its all-time high.

Next earnings report is estimated to be on July 24.

Takeaway

Chipotle growth is impressive, quality ingredients, strong brand, and customization fueling success. They own all their restaurants and have zero debt. They plan to double their North America stores and have a turnaround for expansion in Europe. However, the stock appears slightly overvalued after a recent rally after announcing their stock split. Therefore, considering all factors, I’m starting coverage with a hold. Please let me know your thought in the comments section below.