Maxxa_Satori

The world of REITs is vast, with all sorts and sizes of companies for investors to choose from. One of the biggest players out there, however, is undoubtedly Realty Income (NYSE:O), a diverse REIT with assets that cater to grocery stores, convenience stores, dollar stores, restaurants, health and fitness centers, automotive service companies, and more. About 79.6% of the company’s annualized contractual rent is dedicated to the retail space. However, the company also has exposure to the industrial space, as well as gaming. Most of the firm’s revenue comes from The US market. But it is truly diverse from a geographical perspective, with 11.1% of annualized contractual rent, for instance, coming from the UK.

The last article that I wrote about Realty Income was published in the middle of March of this year. At that time, I pointed out the multi-trillion dollar opportunity that existed for investors. To be precise, the total addressable market for the US alone for the business was estimated to be worth about $5.4 trillion. And in Europe, the opportunity is about $8.5 trillion. In that article, I acknowledged that shares were not exactly the cheapest. But they were priced similar to other comparable enterprises, and the high quality of the company justified a ‘buy’ rating. Given the time that has passed, as well as some new developments that popped up, I think it’s only appropriate to revisit the picture. And what I found confirms that I was not wrong in my prior assessment of the business, even though shares have marginally underperformed the broader market since the publication of that article.

Things are looking good

Fundamentally speaking, things are going really well for Realty Income and its investors. Revenue in the first quarter of the 2024 fiscal year, for instance, came in at $1.26 billion. That’s 33.5% higher than the $944.4 million reported one year earlier. A small portion of this growth came from same store rental revenue growth that was driven by rent escalators that the company has, as well as by new lease contracts being signed by customers. Foreign currency fluctuations also helped slightly. But the largest contributor to the $316.1 million year-over-year growth in revenue for the company, by far, was a $265.7 million increase caused by properties acquired during 2023 and 2024. This included the properties that the company acquired in early January of this year when the business completed its merger with Spirit Realty Capital in a move that brought to the business 2,018 additional properties.

Author – SEC EDGAR Data

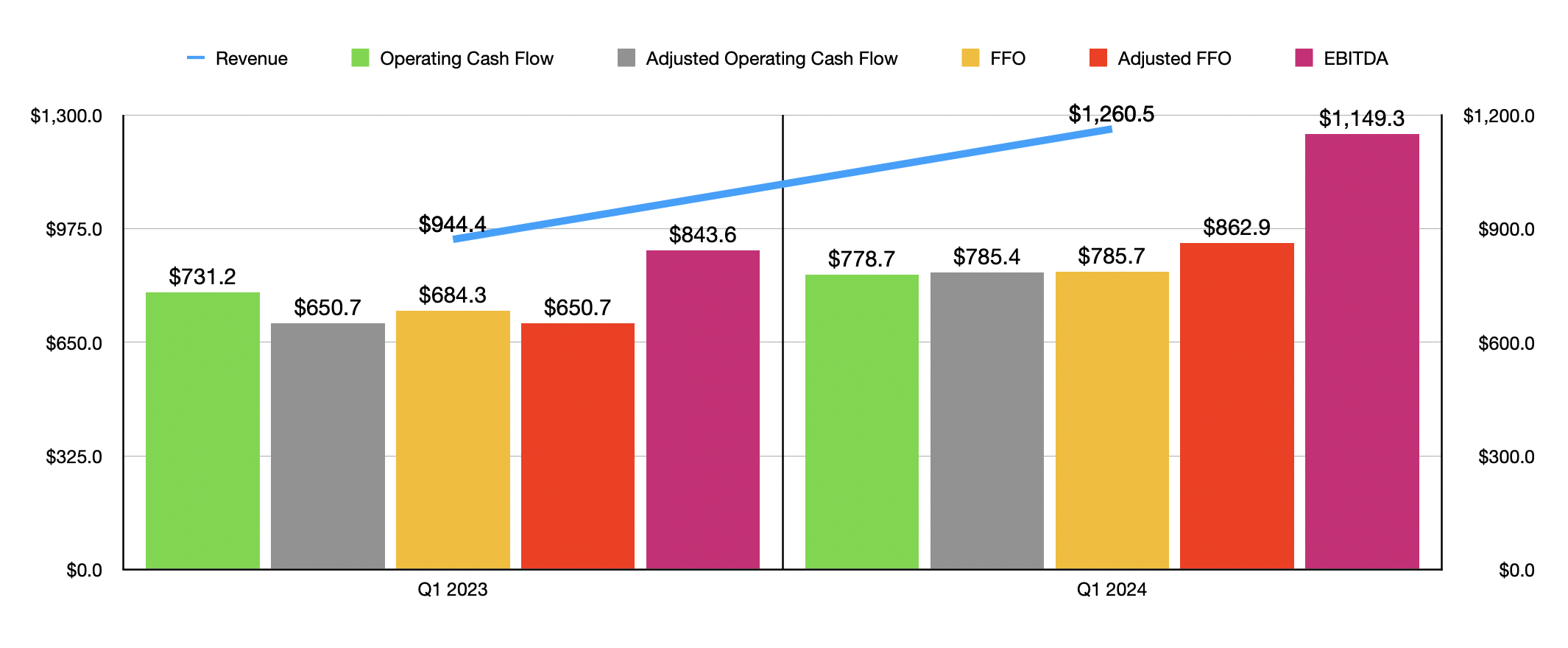

With revenue rising, profitability metrics for the business also improved. Operating cash flow, as an example, increased from $731.2 million to $778.7 million. If we adjust for changes in working capital, the increase was even more significant, from $650.7 million to $785.4 million. There are, of course, other profitability metrics to pay attention to. One of these is FFO, or funds from operations. This metric increased from $684.3 million to $785.7 million. The adjusted figure for this grew even more, from $650.7 million to $862.9 million. And lastly, EBITDA for the business expanded from $843.6 million to $1.15 billion.

So far, things are going really well for investors. This is evidenced by a couple of factors. For starters, in May of this year, the company announced that it was increasing its common stock dividend by 2.1%. This was followed up by another modest increase in the firm’s dividend in June of this year. This marked the 126th dividend increase since the company became listed on the New York Stock Exchange. It’s also the fourth dividend increase that the company has seen this year, and it marked the 648th consecutive monthly dividend throughout the company’s 55-year operating history.

Realty Income

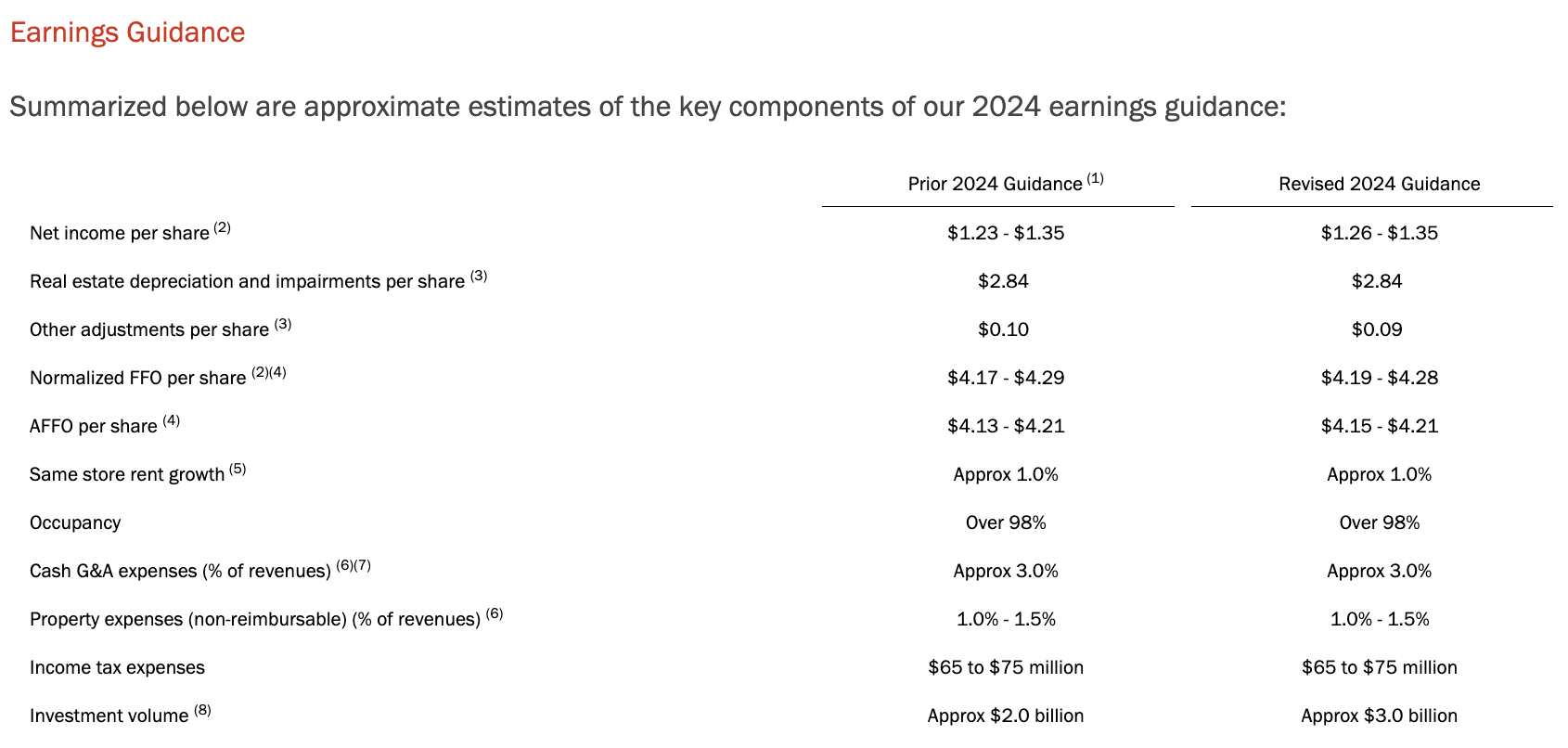

As great as this is to see, it pales in comparison to management’s announcement on June 4th of this year that the company is increasing guidance for 2024. There are many working parts to this guidance, so instead of detailing out each one, I would refer you to the image above. It shows prior guidance compared to the revised guidance that we should rely on now. Most notably, adjusted FFO per share should now come in between $4.15 and $4.21. At the midpoint, that’s a bit higher than the $4.17 previously anticipated. Even more significant, to me, is the fact that the company announced plans to spend $3 billion on investment opportunities this year. That’s 50% higher than the $2 billion management was previously expecting. And none of this includes the aforementioned merger that occurred in January.

Author – SEC EDGAR Data

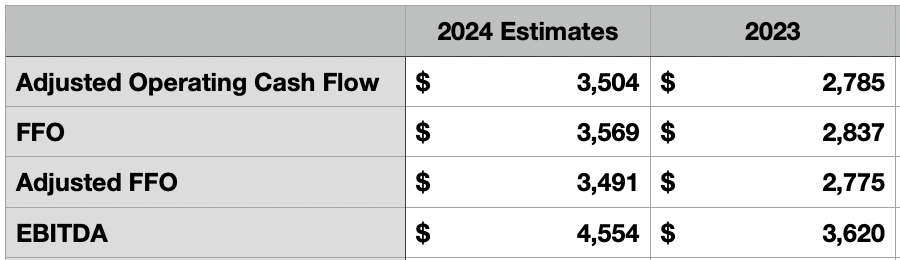

If we assume the company’s share count does not change from where it is right now, then the increase in guidance should result in adjusted FFO of about $3.49 billion. FFO should be around $3.57 billion if this is the case. If we assume that other profitability metrics should rise at the same rate, this would translate to adjusted operating cash flow of about $3.50 billion and EBITDA of approximately $4.55 billion. In the table above, you can see these figures and how they compare against results seen for 2023.

Author – SEC EDGAR Data

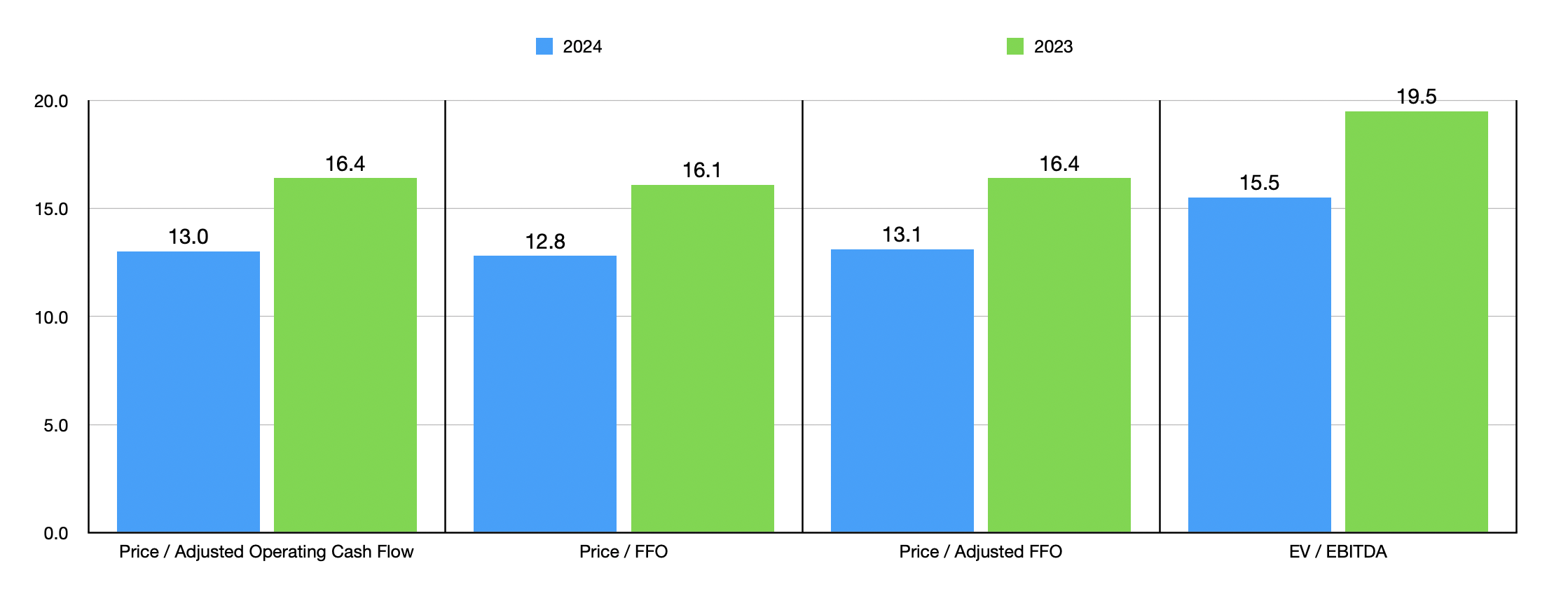

With this data taken into consideration, I then decided to value the stock. This can be seen in the chart above. As you can see, the stock looks much more attractive on a forward basis than if we were to use 2023 figures. But in all fairness, this is more of an apples to oranges comparison since the 2023 figures do not factor in any cash flows from the aforementioned merger. As part of my analysis, I then decided to compare Realty Income to five similar firms, as shown in the table below. I did this using only two of the four valuation metrics so that I could minimize complexity. On a price to operating cash flow basis, three of the five companies were cheaper than Realty Income. But when it comes down to the EV to EBITDA approach, this number drops to two of the five.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Realty Income | 13.0 | 15.5 |

| Simon Property Group (SPG) | 12.9 | 13.7 |

| Kimco Realty (KIM) | 12.9 | 16.8 |

| Regency Centers (REG) | 15.0 | 17.2 |

| Federal Realty Investment Trust (FRT) | 14.9 | 17.5 |

| NNN REIT (NNN) | 12.2 | 14.9 |

Takeaway

As things stand, Realty Income does look to be more or less fairly valued compared to similar enterprises. But this doesn’t mean that investors shouldn’t be bullish. Management continues to make big investments focused on the future and, for such a high-quality company, its trading multiples are not unrealistic. Management seems very bullish, as evidenced by the continued dividend increases and the uptick in guidance. The big investments being made this year should do well to further create value for investors down the road. Given these factors, I do not think that rating the company a ‘buy’ was a bad decision. Rather, I suspect that the company will just need additional time to realize the upside it should enjoy.