The best photo for all

Introduction

Since the last time I reviewed Kinsale Capital, shares of the company have fallen over 22%. I felt that Kinsale had a strong growth trajectory in the excess & surplus insurance market and a strong competitive advantage in providing faster quotes with technology-enabled processes. In this article, I’ll provide an update to my original investment thesis, dissect the latest quarterly results, and share my thoughts on the outlook and valuation.

Company Overview

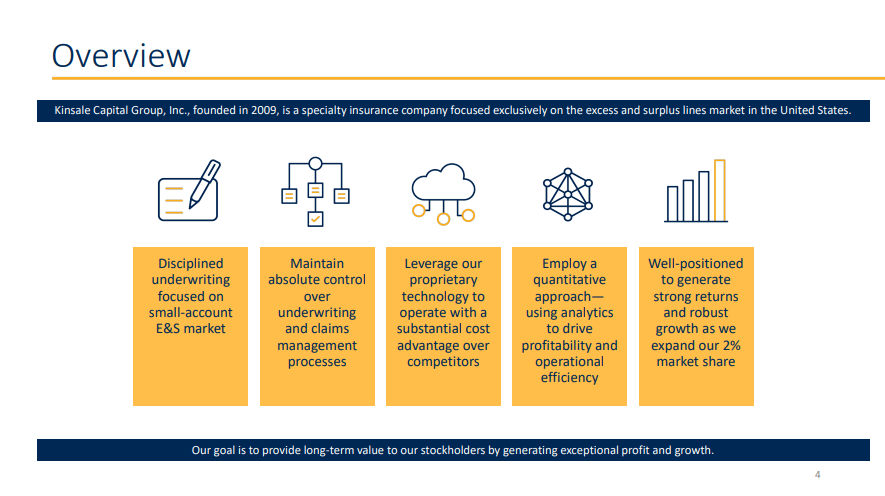

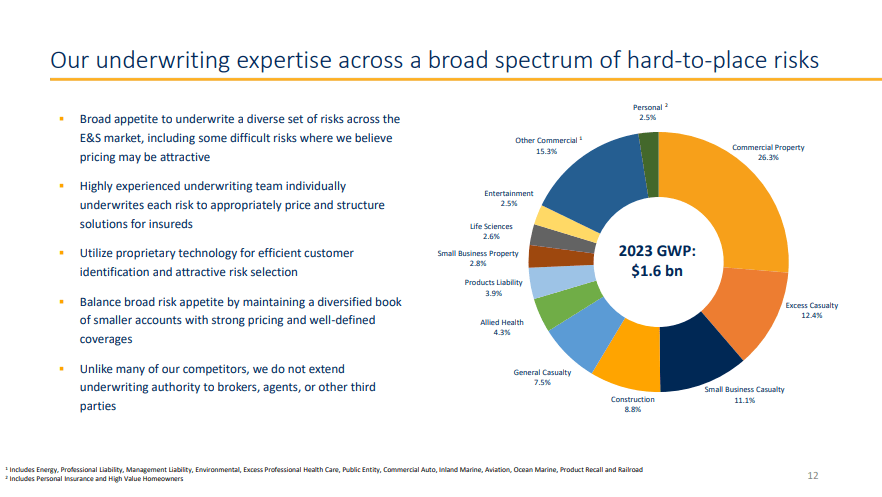

Kinsale Capital Group, Inc. (NYSE:KNSL) is a specialty insurance company. What makes Kinsale unique is that it exclusively targets the excess and surplus (E&S) market, which is the fastest part of the insurance market. Based out of Virginia, Kinsale was founded in 2009 by the current Chairman and CEO, Michael Kehoe, who had previously served as the President and CEO of James River Group Holdings (JRVR). Specializing in hard-to-place commercial property & casualty insurance for small- to -medium-sized businesses, a significant portion of Kinsale’s business is in commercial lines, including Commercial Property, Excess Casualty, and Small Business Casualty.

Investor Presentation

Investment Thesis

Positioned as a leader in the E&S market, I think Kinsale is poised to benefit from long-term secular tailwinds. As a market that’s often underserved by traditional insurance, E&S continues to get a large inflow of business from standard companies and rate driven by inflation and relatively tight underwriting conditions. Among the subsegments of the insurance industry, E&S is relatively exciting because it’s still in its early stages. Growth at Kinsale will continue to benefit from more underwriting in the E&S market as a whole, but Kinsale in particular will benefit given its tech-driven service and product expansion. With faster turnaround times relative to peers and 14 new underwriting divisions in recent years (bringing Kinsale to 25 divisions today) Kinsale should continue to maintain its market leading position.

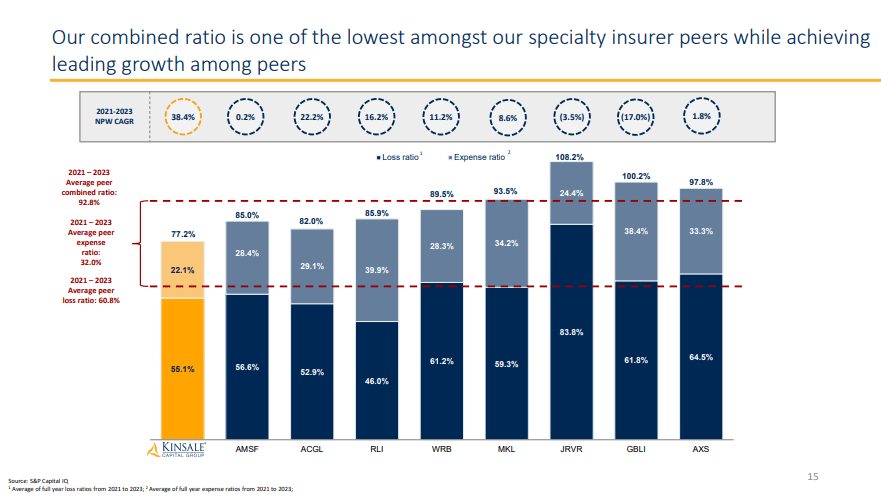

I think Kinsale’s industry-leading underwriting performance is likely to continue. As I’ll discuss later, the company has some of the best returns on equity and combined ratios for insurance. I think strong results like the recent results are replicable going forward, and the company’s favorable reserve development reflects diligence on general liability. There’re very few insurance companies who are able to do what Kinsale has done. The only insurance companies to my knowledge that have better combined ratios are AMERISAFE (AMSF) and International General Insurance (IGIC), a company I previously covered in February.

Investor Presentation

Finally, Kinsale’s focus and technological advantage are a source of moat. Kinsale’s expense ratio is very low (at 20.8% in 2023, according to S&P Capital IQ), which is supported by a centralized structure and proprietary technology. In an interview with Ron Baron, Kinsale discussed how its IT systems are built in-house, eliminating constraints on adding new product lines or features that reduce labor for underwriters. For most new business submissions, this helps Kinsale to swiftly issue quotes where fast turnaround times and responsiveness builds goodwill with brokers and allows KNSL to pay lower commissions, as brokers are willing to trade commissions for service and specialization in hard-to-place risks. It also means that Kinsale can charge a small premium because it underwrites faster.

Investor Presentation

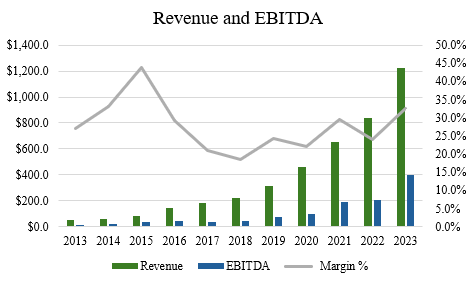

Operating in a rapidly growing segment of the insurance market, Kinsale has been benefitting from strong tailwinds. Over the last ten years, the company has produced a 38.1% CAGR on the top line and 40.7% on the bottom line (EBITDA). In the last five years, the company has shown no signs of slowing down, growing revenues and EBITDA at CAGRs of 40.7% and 57.4%, respectively (source: S&P Capital IQ).

Author, based on data from S&P Capital IQ

Recent Results

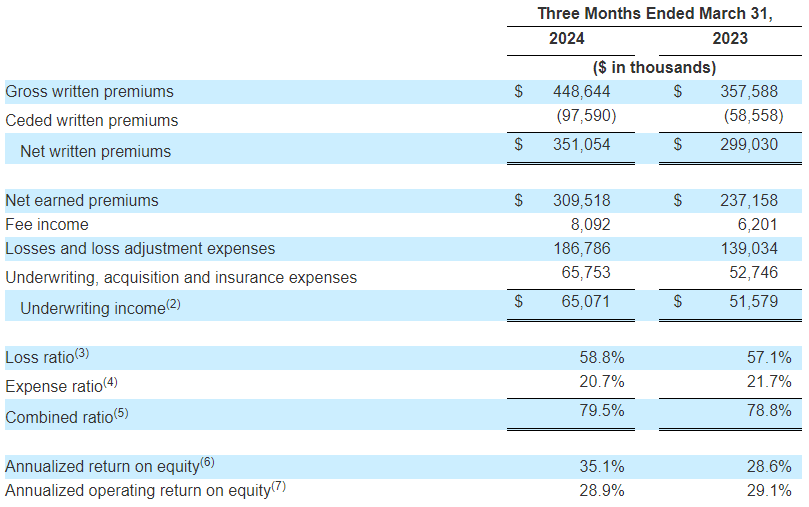

When looking at the most recent results for Kinsale, the company reported earnings per share of $4.24, which was 76.7% higher than Q1’23. Gross written premiums increased by 25.5% to $448.6 million, and underwriting income was up 79.5%.

Overall, these were very impressive results. Not only does Kinsale continue to put up strong top line growth, but the company’s profitability has also rapidly improved.

We see that reflected in the company’s combined ratio and ROE metrics too. At the end of the quarter, the company had combined ratio of 79.5%, and it posted an operating return on equity of 28.9%. On the expense ratio, the company saw a decline from 21.7% last year to 20.7% this quarter. Most of this was driven by the benefit of higher ceding commissions from the Company’s casualty and commercial property proportional reinsurance agreements as a result of growth in the lines of business ceded into those treaties. This is sustainable, in my view, given that brokers are willing to trade commissions for volume for business with Kinsale.

Company Filings

On the earnings call, management noted that the growth in gross written premium of growth of 25.5% from 33.8% in the Q4’23 highlights a deceleration in growth rate from the 40% growth we’ve experienced over the last several years. This deceleration is mostly attributable by a return to a more normal level in competition.

In P&C, property is an exciting area of growth for Kinsale because of its high growth rates and strong pricing. In casualty, challenges with respect to the frequency and severity of inflation, rising loss cost, and an unpredictable legal system make for a market that provides Kinsale a long-term growth opportunity.

In terms of my outlook for Kinsale, I would continue to expect strong profitability ratios. Where I do see cause for concern is the deceleration in premium growth. As Kinsale gets larger and the market matures, I foresee premium growth settling towards a long-term run rate in the mid-teens. In the past, management has said that it believes that Kinsale can grow 10-20% through the cycle. Although I think that market conditions should eventually normalize, a potential uptick in casualty pricing (due to reserving issues facing by the industry) could prolong an already extended market and be beneficial for Kinsale.

Another element in Kinsale’s financial profile to consider is how management will begin trading off growth and margins in a more normal market (i.e., more growth for lower margins resulting in higher underwriting income dollars) given the company’s meaningful expense advantage (8-9 combined ratio points). In the current hard market, Kinsale has been somewhat of a price taker and has experienced both outsized growth and margins.

Valuation

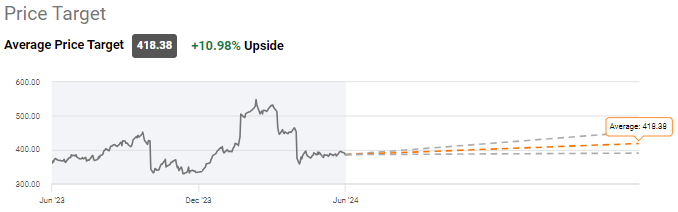

Based on the 10 sellside analysts covering the stock, there are 2 ‘buy’ ratings and 8 ‘hold’ ratings. From current price to the average price target of $418.38 one year out, this implies about 11.0% upside, not including the current dividend yield of 0.2%.

Seeking Alpha

Kinsale trades for 25.6x P/E and 20.3x EV/EBITDA (source: S&P Capital IQ). While these might seem expensive on an absolute basis, keep in mind that Kinsale has been growing in excess of 20% on a compounded basis. For example, when using the forward multiples of 21.9x 2025 earnings and 18.4x 2026 earnings, the valuation seems much more reasonable when considering the company’s future earnings growth, in spite of a deceleration.

Historically, management hasn’t offered up guidance targets or growth forecasts. I find the 21.9x 2025 earnings and 18.4x 2026 earnings reasonable valuation multiples to use given the growth rate of the E&S market. According to a report from Allied Market Research, the E&S market is expected to grow at a rate of 15.2% from 2020 to 2027. This roughly in line with consensus revenue forecasts in 2025 and 2026 of 20.3% and 11.6%, so it seems that Kinsale should be able to grow with the industry (source: Bloomberg). This also helps to get over the current valuation multiple of 25.6x P/E, knowing that earnings are growing rapidly.

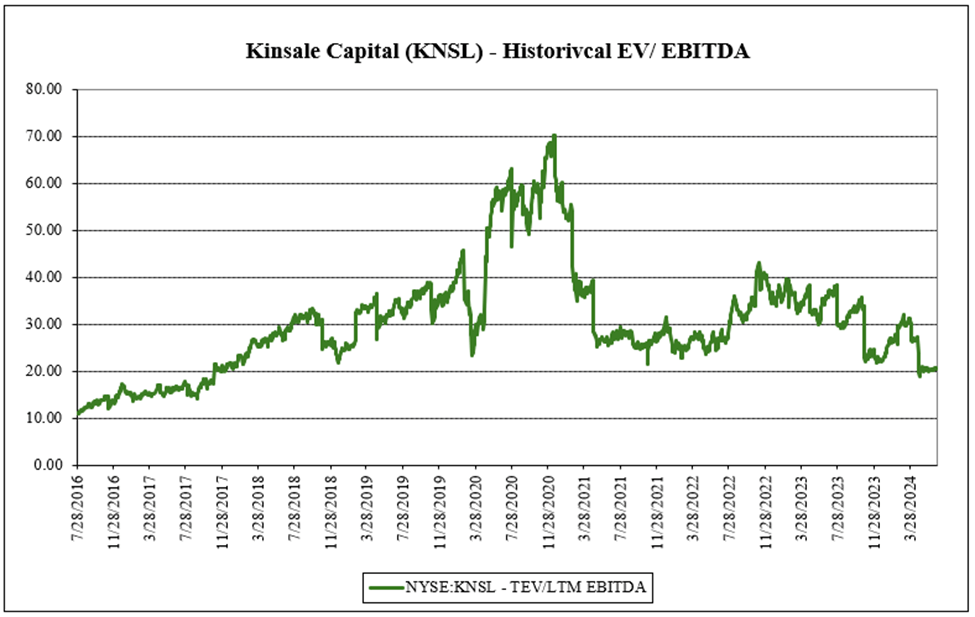

Compared to its historical valuation, Kinsale is trading at one of the lowest valuations it’s ever traded at. Historically, the company has traded at an average multiple of 30.3x EV/EBITDA. While the company may have been overpriced before, I think the recent pullback has given investors an opportunity to get long this compounder. At the current multiple of 20.3x, Kinsale offers up a strong discount to its ten-year average multiple, especially when we consider that this is a business that’s essentially been doubling in size every 2 years.

Author, based on data from S&P Capital IQ

In terms of the risks to the investment thesis, there are a few that investors should monitor, both macro and company specific. Firstly, there is a risk that the E&S market doesn’t grow as fast as expected (15.2% per year). This could come from the general insurance market slowing down. During the pandemic, insurance companies had become “essential businesses” where insurance was needed for coverage of business interruption or incidents related to physical loss (e.g., forced closedown due to physical damage). I view the growth rate of E&S to be more secular rather than event-driven by the pandemic, particularly as Kinsale had been growing 20%+ even before 2019.

Specific to Kinsale, there’s also a risk that new entrants into the market. For example, Kinsale enjoys a dominant market position in the E&S market and there’s always a risk that new entrants put pressure on profitability ratios. If new competition goes head-to-head with Kinsale, the company would be forced to reduce premiums to remain competitive. While the company has superior technology, faster turnaround times, and a first-mover advantage as being the leader in the space, where there’s money to be made, we can be sure that competition will eventually come to Kinsale. For now, I think the moat is very durable and even if the company can grow with the industry, the forward returns look quite attractive.

Conclusion

On this recent share price drop, I’m adding to my position in Kinsale Capital. Over the company’s relatively short life as a public company, Kinsale has grown from its founding in 2009 to a billion-dollar insurance company. Still, the company only has a 1% market share. With a track record of demonstrating remarkable business performance, I believe the share price decline has provided investors a gift to pick up shares of this compounder.

As we’ve discussed, Kinsale has clear competitive advantages that will make it a winner. With faster quotes compared to peers, a defensible moat with respect to its technology, and the ability to charge higher premiums, Kinsale is tapping into unmet needs in the E&S market. By focusing on smaller insurance premiums and diversifying risk across several industries, I think Kinsale offers up a compelling opportunity that offers elements of both growth and value. If the high multiple scares you, keep in mind that this business is doubling in size every couple of years. For investors who can get over this hurdle and can see a path to long-term growth, an investment in Kinsale makes sense.