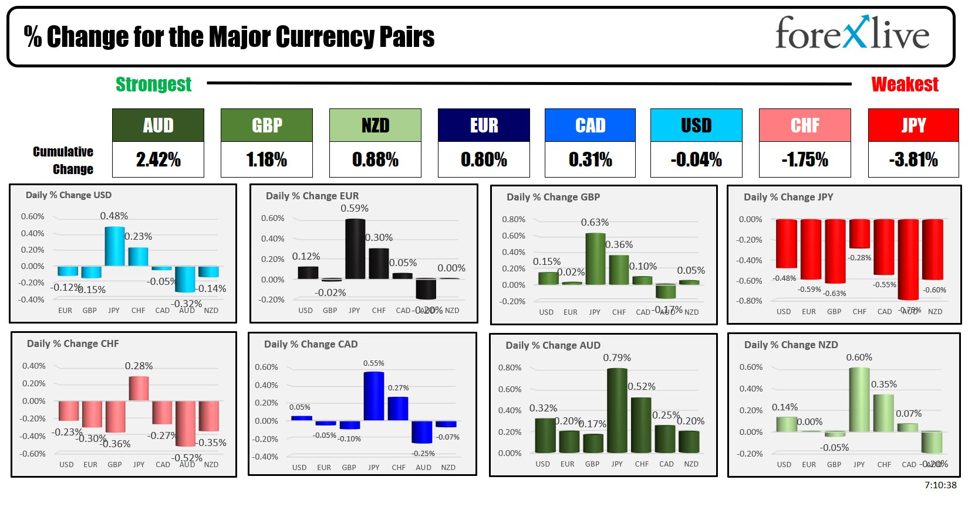

As the North American session begins, the AUD is the strongest and the JPY is the weakest. That combination reverses what has been more of a familiar theme with the AUD (or NZD) weakest and the JPY the strongest. Not surprisingly, there is a rebound in US stocks in the pre-market which is helping the reversal. The Nasdaq is up 200 points (currently) in premarket futures trading. That reverses the -160 point decline from yesterday. Nevertheless, the major US indices are on pace for a declines this week.

The unwind of the USDJPY and the so called “carry trade” where some investors borrow the yen at low rates to invest in USD assets (or other countries assets) for better returns,has been an excuse for the flow of funds out of some assets and into others.Having said that, the Nikkei 225 had its worst day since 2021 this week. Bitcoin, oil, silver, copper and even gold fell this week. So there may be selling of the USD and liquidation in things like the US stocks but it seems to be going into cash. It will be interested how this story unwinds.

Of course, when you have moves like we have had this week especially out of assets like the Magnificent 7, it is always fun to find the “reason” (i.e. carry trade unwind), but it just can be “taking profit” and yes parking in cash or money market for a while. The Fed does meet next week, and with 2% or thereabout growth in the 1H of 2024, it may make it hard to cut. So parking funds for a while and buy a dip might be a sound idea.

BTW, The BOJ does meet next week,and the market is pricing in a 65% chance for a 10 basis point rise in rates. The US Fed also meets and the focus by the markets is on the central bank starting the cuts in September.

Today’s data, may help the Fed with that decision as the favored measure of inflation (the core PCE) will be released at 8:30 AM ET. A review of the economic data to be released today, will be highlighted by the PCE data along with the University of Michigan consumer sentiment (final) at 10 AM ET. :

- PCE price index MoM: Forecast 0.1% versus 0.0% last month. YoY estimate 2.5% versus 2.6% last month.

- Core PCE Price Index m/m: Forecast 0.2% versus 0.1% last month. Estimate 2.5% versus 2.6% last month

- Personal Income m/m: Estimate 0.4% versus 0.5% last month

- Personal Spending m/m: Estimate 0.3% versus 0.2% last month

- Revised UoM Consumer Sentiment: Estimate 66.0 versus 68.2 last month and 66.0 preliminary

- Revised current conditions: Preliminary 64.1. Last month 65.9

- Revised expectations: Preliminary 67.2. Last month 69.6

- 1 year inflation expectations. Preliminary 2.9% versus 3.0% last month

- 5 year inflation expectations. Preliminary 2.9% versus 3.0% last month

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading down $0.37 at $77.91. Although lower today, at this time yesterday, the price was even lower at $76.36. The price is down -0.80% for the week

- Gold is trading up $7.80 or 0.33% at $2373. At this time yesterday, the price was trading at $2371.44. For the week the price of gold is down -1.07%.

- Silver is trading down eight cents or -0.32% at $27.73. At this time yesterday, the price is trading at $27.57. For the week the price of silver has tumbled -5.02% which comes after 8-5.10% decline last week.

- Bitcoin trading higher at $67,298 (well there is some buying in bitcoin today) . At this time yesterday, the price was trading at $64,208

- Ethereum is trading higher as well as $3246. At this time yesterday, the price was trading at $3174.03

In the premarket, the snapshot of the major indices are trading higher.

- Dow Industrial Average futures are implying a gain of 287.93 points. Yesterday, the Dow Industrial Average rebounded with a gain of 81.20 points or 0.20% to 39935.08.

- S&P futures are implying a gain of 47.78 points erasing the declines from yesterday. Yesterday, the S&P index closed lower by -27.89 points or -0.51% at 5399.23. The S&P is on pace for back-to-back weeks of 2% declines.

- Nasdaq futures are implying a gain of 223 points . Yesterday, the index closed lower by -160.69 points or -0.93% at 17181.72. Coming into today (with the gains, it may not play out), the NASDAQ was on pace for back-to-back weeks of -3% declines (at the close yesterday the index was down -3.08% after falling -3.68% last week). It hasn’t done that since September 2022.

- Yesterday, the Russell 2000 index rose by 27.60 points or 1.26% at 2222.98.

European stock indices are trading mostly higher. For the week the indices are also mixed:

- German DAX, +0.49%. The index is up 1.19% this week.

- France CAC, +0.91%. The index is down -0.56% this week.

- UK FTSE 100, +0.85%. The index is up 1.22%.

- Spain’s Ibex, -0.07%. The index is up 0.44% this week.

- Italy’s FTSE MIB, +0.25% (delayed 10 minutes). The index is down -1.01 percent this week

Shares in the Asian Pacific markets closed lower:.

- Japan’s Nikkei 225, -0.53%. For the week the Nikkei fell -5.98% it’s worse decline since April 15 week when it tumbled -6.21%.

- China’s Shanghai Composite Index, +0.14%. For the week it fell -3.06%.

- Hong Kong’s Hang Seng index, +0.10%. For the week it fell -2.28%.

- Australia S&P/ASX index, +0.76%. For the week the index fell -0.60%.

Looking at the US debt market, yields are trading mixed:

- 2-year yield 4.434%, -0.8 basis points. At this time yesterday, the yield was at 4.366%. 2-year yield are currently down -7.8 basis points this week

- 5-year yield 4.132%, -1.2 base points. At this time yesterday, the yield was at 4.088%. Currently the 5-year yield is down -3.6 basis points this week.

- 10-year yield 4.240%, -1.5 basis points. At this time yesterday, the yield was at 4.225%. Currently, the 10 year yield is unchanged this week

- 30-year yield 4.481%, -1.9 basis points. At this time yesterday, the yield was at 4.495%. Currently, the 30-year yield is up 3.4 basis points.

Looking at the treasury yield curve,

- The 2-10 year spread is at -19.6 basis points. At this time yesterday, the spread was at -14.4 basis points. Currently, the spread is up 8.0 basis points this week

- The 2-30 year spread is +4.5 basis points. At this time yesterday, the spread was 12.6 basis points. Currently, the spread is up 11.0 basis points this week

In the European debt market, the benchmark 10-year yields are lower: