PM Images

Regeneron’s Q2 Surge: Blockbuster Drugs Drive Revenue Growth

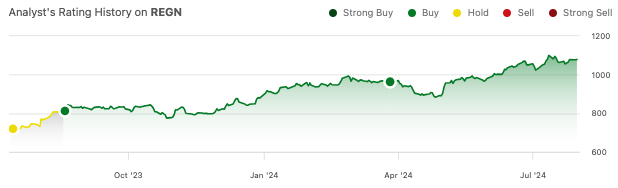

Regeneron (NASDAQ:REGN) is up another 13% since my most recent “buy” recommendation in March.

Seeking Alpha

My last article covered Q4 ‘2023 earnings, which revealed strong performances from blockbuster drugs like Eylea, Libtayo, and Dupixent.

In Q2 2024, it was more of the same for the $100 billion-plus pharmaceutical giant. Revenue grew 12% year-over-year, reaching $3.55 billion. The growth was, again, inspired by strong performances from key products like Dupixent and Libtayo.

Dupixent’s global net sales soared to $3.56 billion in Q2, up 27% from the same period last year. Remember that Regeneron is partnered with Sanofi (SNY) and records their portion of Dupixent revenues as “collaboration revenue.” This total was $1.146 billion in the second quarter. Regeneron’s Libtayo continued its strong growth, with Q2 revenue of $297 million, up 41% from the same period last year. This places Libtayo on track to be Regeneron’s next blockbuster drug.

Libtayo is a monoclonal antibody that primarily targets the PD-1 pathway. It was initially codeveloped with Sanofi until Regeneron acquired Sanofi’s stake in 2022 for $900 million upfront (plus an 11% royalty on worldwide net sales). It was initially approved for the treatment of non-melanoma skin cancers and basal cell carcinoma. More recently, Libtayo secured approval for advanced non-small cell lung cancer “whose tumors have high PD-L1 expression [Tumor Proportion Score (TPS) ≥ 50%] as determined by an FDA-approved test, with no EGFR, ALK or ROS1 aberrations.”

The FDA requested “additional efficacy analyses” for Dupixent’s sBLA in COPD, so the action date was pushed back. The company is confident that the minor setback will still result in supplemental approval in late September. Meanwhile, across the ocean, EU authorities gave Dupixent the green light last month to treat COPD patients.

Importantly, the new version of Eylea, Eylea HD, is making up for Eylea’s market share loss. Eylea’s US revenue fell 18% year-on-year to $1.231 billion in Q2. Meanwhile, Eylea HD is experiencing strong demand, earning $304 million in Q2 (there was no comparable data in Q2 2023). So, combined, they saw a 2% increase in Q2 compared to the same period last year, indicating that Eylea remains a strong brand in the competitive anti-VEGF therapy market, which includes biosimilars. Remember that Eylea HD, approved in August 2023, is a higher-dose formulation of standard Eylea that is intended to reduce the number of injections. Eylea HD’s strong performance, despite its youth, suggests that Eylea patients, as well as patients from other anti-VEGF therapies, are easily transitioning to Eylea HD.

Strategic Initiatives and Pipeline Developments

Regeneron is working to fill gaps in the lucrative and highly competitive obesity treatment market. GLP-1 agonists like Novo Nordisk’s (NVO) Wegovy and Eli Lilly’s (LLY) Zepbound, in addition to causing profound fat loss, may also cause considerable muscle loss. To address this, Regeneron is developing a combination therapy by adding trevogrumab or garetosmab to semaglutide. Trevogrumab is a monoclonal antibody that inhibits myostatin, which is a negative regulator of muscle loss, thereby helping to preserve muscle mass during weight loss. A Phase 2 study was just recently initiated.

Libtayo is being tested in combination with other therapies for indications like colorectal cancer and advanced melanoma. For the latter, Libtayo is teaming up with Regeneron’s LAG-3 inhibitor, fianlimab. The combination demonstrated an ORR of 61.2% in patients with advanced melanoma, with efficacy impressively holding up in high-risk subgroups (e.g., prior PD-1 therapy). Regeneron provided an update on the combination during their Q2 earnings call.

Moving to oncology and starting with fianlimab, our LAG-3 antibody in combination with Libtayo, at the upcoming ESMO meeting in September, we look forward to presenting longer-term follow-up on the metastatic melanoma cohorts from our first-in-human study. Responses have continued to deepen with the proportion of complete responders and median progression-free survival continuing to improve.

These results strengthen our view that fianlimab and Libtayo may be the most promising immunotherapy combination in clinical development. As we recently announced, we are looking forward to the Phase III readout in this melanoma setting next year, which could position fianlimab and Libtayo as a new standard-of-care in melanoma and eventually potentially other cancer settings.

Regeneron Q2 Earnings

Total revenues were $3.547 billion in Q2. The cost of goods sold was $257.8 million. R&D and SG&A expenses were $1.2 billion and $758.8 million, respectively. The cost of collaboration and contract manufacturing was $222.4 million. Income from operations totaled $1.069 billion, and after accounting for “other income” and income tax, the net income was $1.432 billion. This is good for an EPS of $13.25, a substantial improvement from the $8.50 per share in Q2 ’23.

Financial Health

As of June 30, Regeneron reported $17.531 billion in cash and marketable securities. Total current assets were $19.081 billion, while total current liabilities were just $3.508 billion. Regeneron has $1.983 billion in long-term debt.

The company recorded $1.866 billion in net cash provided by operating activities. Given the company’s robust balance sheet and its ability to generate significant cash from operations, there is no need to estimate the cash runway.

REGN Stock – Risk/Reward Analysis and Investment Recommendation

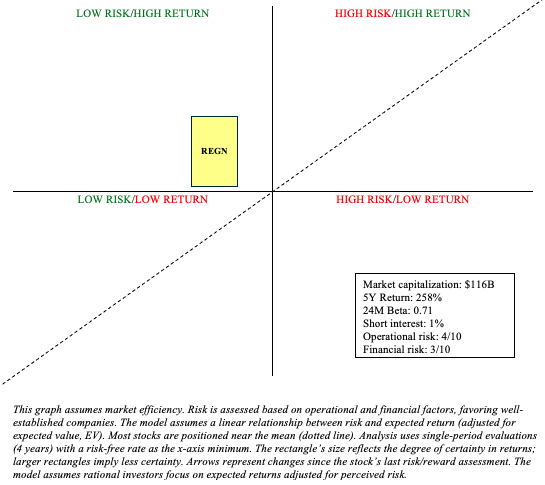

Returning to my previous analysis, I stated that Eylea and Dupixent will “provide a bedrock of $8-10 billion in revenue for years to come.” Recent developments continue to support my assertion. Libtayo appears to be on its way to becoming a cornerstone in cancer treatment. These three drugs, combined with a strong balance sheet that can easily support ongoing R&D efforts, significantly reduce Regeneron’s financial and operational risks. Yes, the stock is more pricey since my last look, but a $116 billion market capitalization appears easy to stomach.

Author

As such, it’s reasonable to continue adding at these prices (recommendation: maintain buy) with the expectation that REGN will continue to outperform the risk-free rate with a subdued risk profile thanks to drugs like Eylea and Dupixent.

There are some risks associated with my buy recommendation. Regeneron is highly dependent on their Eylea franchise. Although Eylea HD is taking the sting out of Eylea losing market share to biosimilar anti-VEGF therapies, a 2% year-over-year growth for the franchise is not entirely impressive within a market that is growing nearly 4% in CAGR. Within the oncology market, Libtayo faces tough competition, primarily due to the presence of a few other well-established immunotherapies like Keytruda and Opdivo. These are just two examples. As always, investors should maintain a diversified portfolio, spanning many industries, to mitigate the idiosyncratic risks associated with a REGN investment.