Whenever I discuss Enbridge Inc. (NYSE:ENB) (TSX:ENB:CA), I get comments from disappointed investors who wonder why on earth I’m bullish on a stock that has generated no shareholder value in “recent” years.

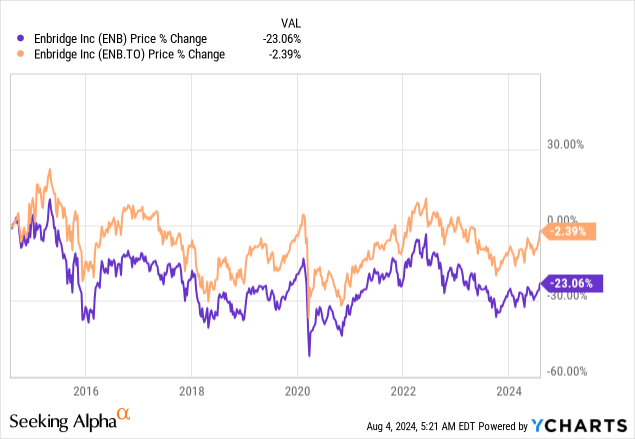

These comments make sense. After all, over the past ten years, Toronto-listed Enbridge shares have returned negative 2%. This includes its dividend! New York-listed shares have lost 23%, also including dividends. The difference is caused by unfavorable currency translations during this period.

Needless to say, it’s not hard to find a stock with a better performance since 2014, as the returns above are abysmal.

That said, I started to turn bullish on North America’s largest midstream company in early 2023. Since then, I have written six articles. Only the first two are still “underwater.”

My most recent article was written on May 17, titled “Wall Street Finally Woke Up To Enbridge’s 7% Yield.” Since then, shares have returned 3%, beating the 1% return of the S&P 500.

In this article, I’ll use the company’s just-released earnings and bigger economic picture to explain why I maintain a Strong Buy rating on the company, expecting it to outperform the market on a long-term basis, supported by consistent earnings growth, its juicy dividend, and secular tailwinds.

So, let’s dive into the details!

Pipelines – We Need Them

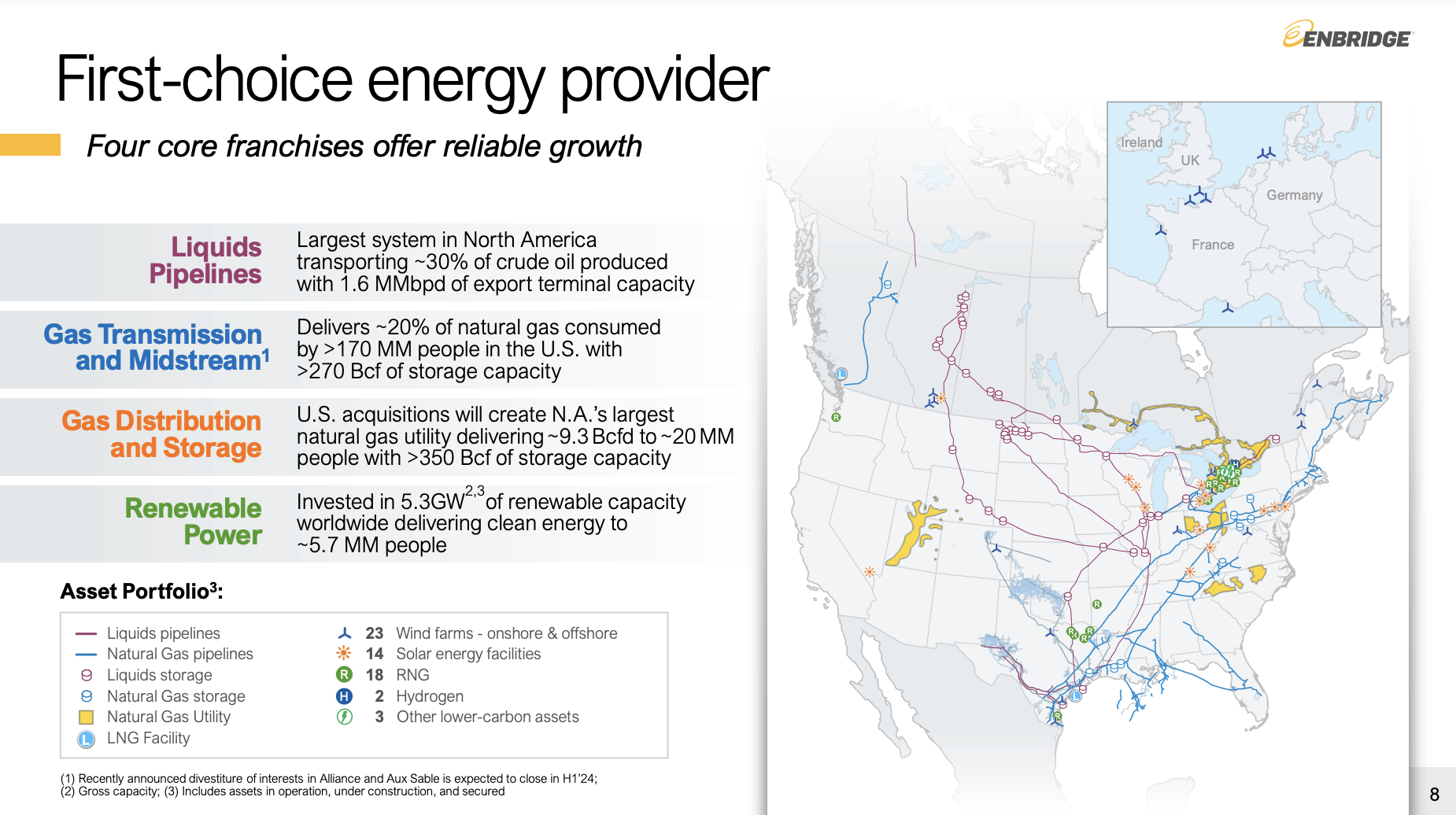

Enbridge is a giant. The company, which has a market cap of more than $80 billion, owns America’s largest pipeline system for liquids, transporting roughly 30% of crude oil produced with 1.6 million barrels per day of export terminal capacity.

It also delivers 20% of natural gas, consumed by more than 170 million people in the U.S., with more than 270 billion cubic feet of storage capacity. In addition to that, it owns gas utilities and 5.3 gigawatts of renewable energy capacity.

Enbridge

Although midstream companies do not allow investors to benefit from rising commodity prices due to fixed-fee contracts, they benefit from rising volumes.

Right now, that’s a hot topic.

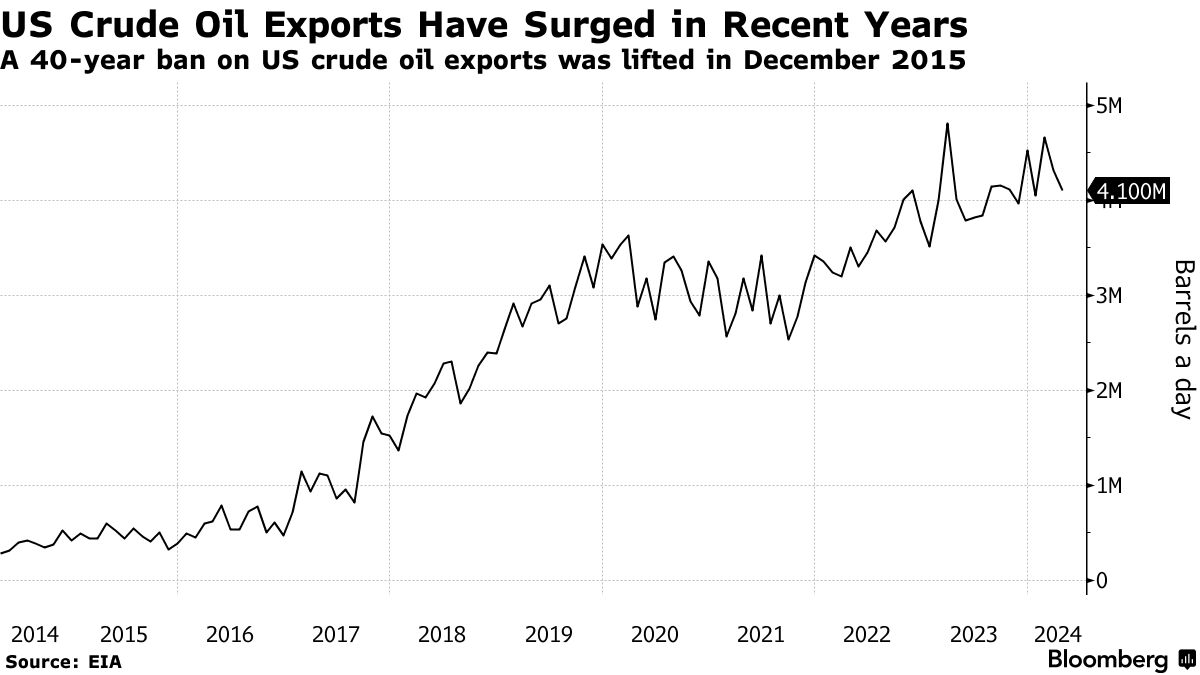

On July 29, Bloomberg reported that Texas, a key producer in North America, is seeing pipeline constraints. I added emphasis to the quote below:

Key pipelines that transport barrels produced in the Permian Basin to the Port of Corpus Christi are more than 90% full, and companies that operate some of these lines say the congestion is likely to get worse. By the second half of 2025, the pipes could be 94% or 95% full, estimates researcher East Daley Analytics.

Demand for the limited pipeline space comes at a time when the US is producing more crude oil than any other nation, with output set to hit a new record next year. The Permian region, one of the top producing shale basins in the world, accounts for nearly half of all US oil production. While output is set to keep growing, it will be difficult for that incremental output to reach international buyers without ample pipeline space.

Bloomberg

One of the key players in this area is Enbridge, as Bloomberg wrote that a plan to expand its Gray Oak pipeline system could likely reduce some bottlenecks to Corpus Christi (a key export city).

“Mission-Critical” And Poised For Long-Term Growth

Speaking of expanding, Enbridge has expanded quite aggressively in recent years.

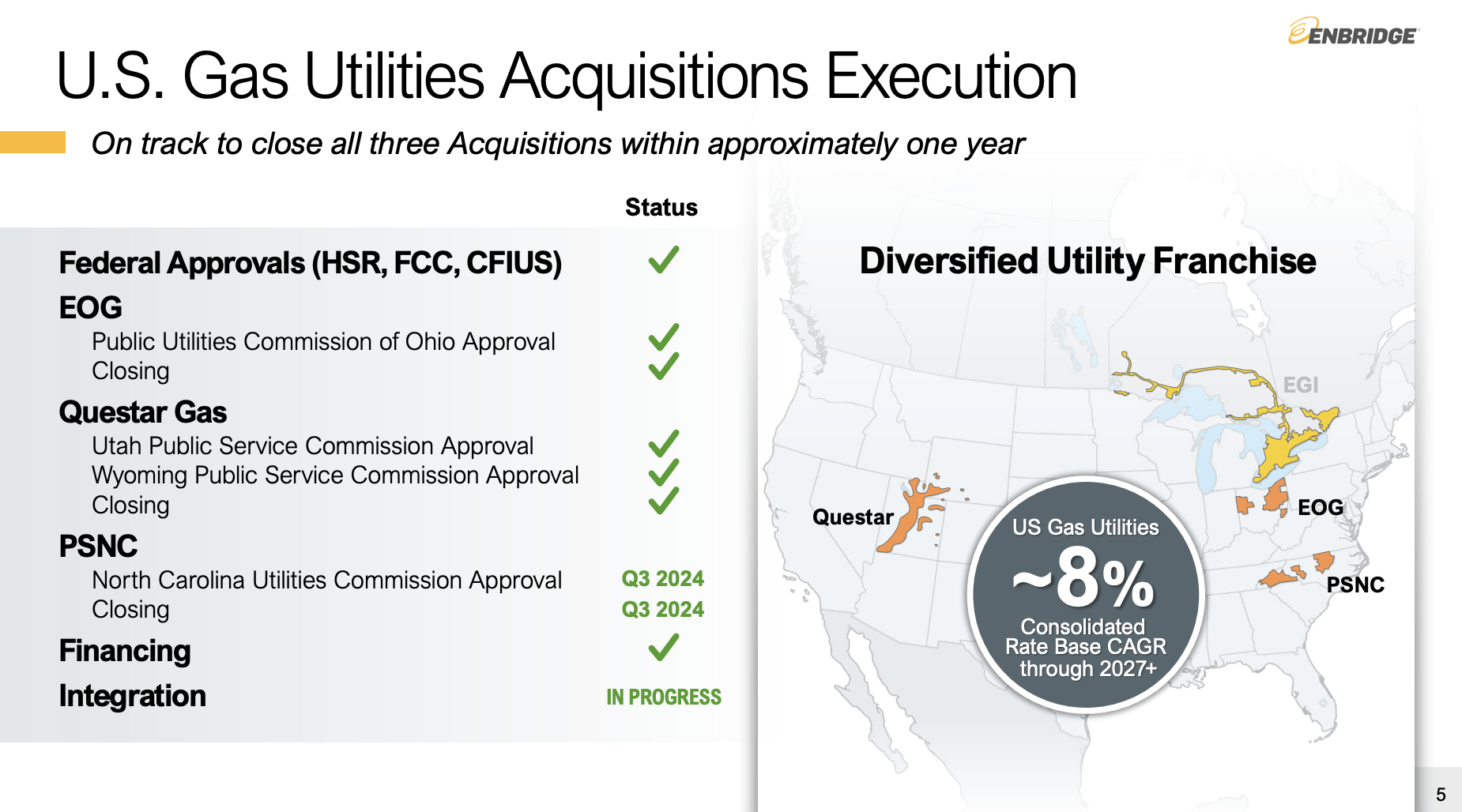

A standout acquisition is the company’s progress in acquiring U.S. gas utilities, a $19 billion investment that’s aimed at diversifying the company’s asset base and further improving “utility-like” cash flow stability.

In this case, the acquisition of East Ohio Gas, Questar, and Wexpro not only expands the company’s footprint but also integrates 1.2 million customers in Ohio and 1.2 million in Utah into the company’s gas utility network.

Even better, the company expects these assets to generate roughly 8% annual compounding rate base growth through 2027 and beyond.

Enbridge

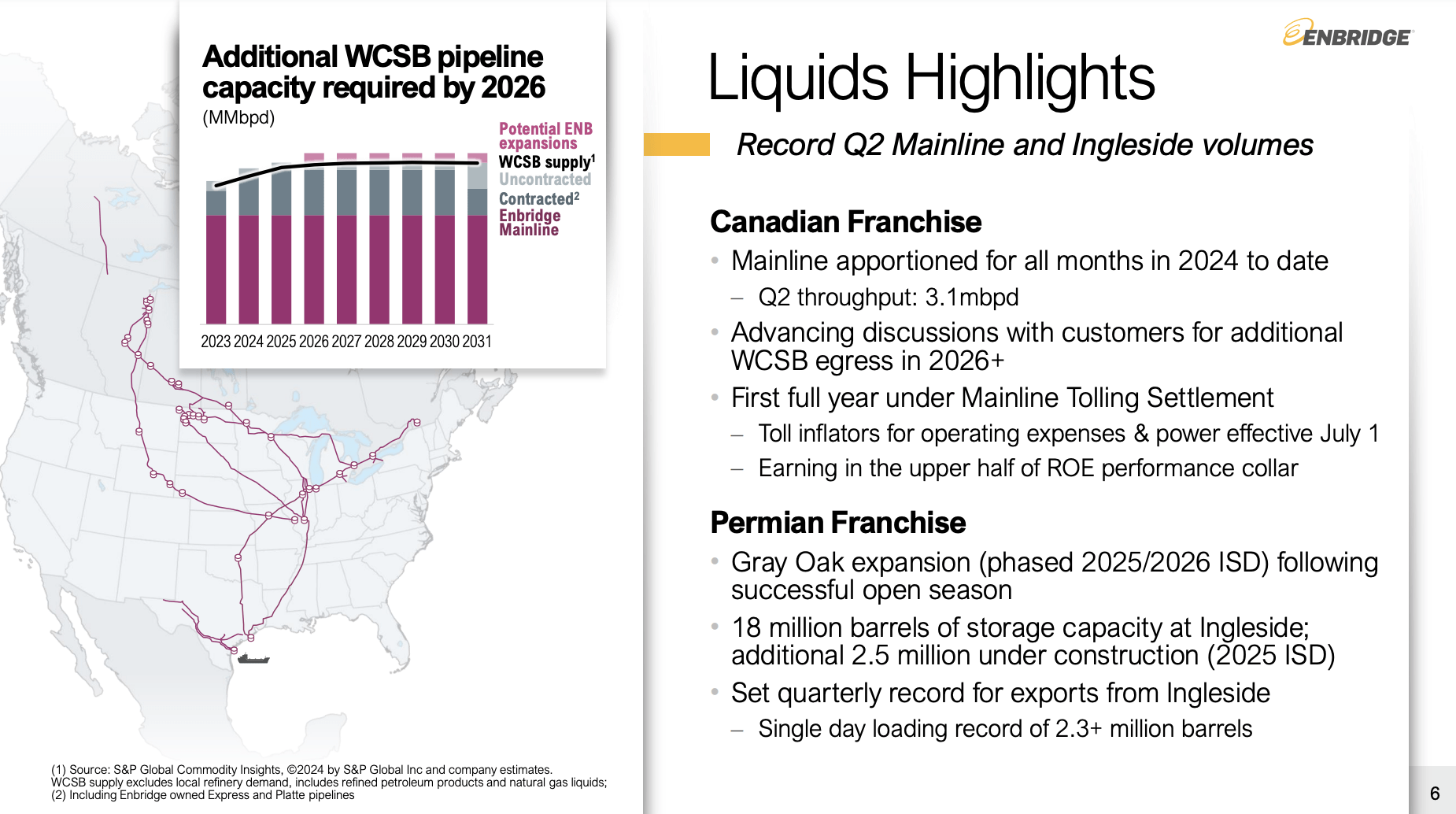

On top of that, the company benefits from the aforementioned volume tailwinds, as its Mainline system transported a record 3.1 million barrels per day in the second quarter. Its Ingleside export facility also saw record export volumes.

These elevated utilization rates are expected to continue, providing revenue and potential for sustainable expansion projects.

In the Permian, we sanctioned 120,000 barrel per day expansion of the Gray Oak Pipeline, following a successful open season this quarter, and expect this expansion will come fully online in 2026. The incremental volumes will serve growing demand at our Ingleside facility, and we expect the expansion to be capital efficient with an EBITDA multiple below 5x.

We now have 18 million barrels of storage capacity at Ingleside with an additional 2.5 million barrels under construction. Of note, Ingleside also set a quarterly record for exports and saw a single-day loading record of more than 2.3 million barrels. This again underscores our belief that cash flow from that asset will be sustainable and growing for many years to come. – ENB 2Q24 Earnings Call (emphasis added)

Enbridge

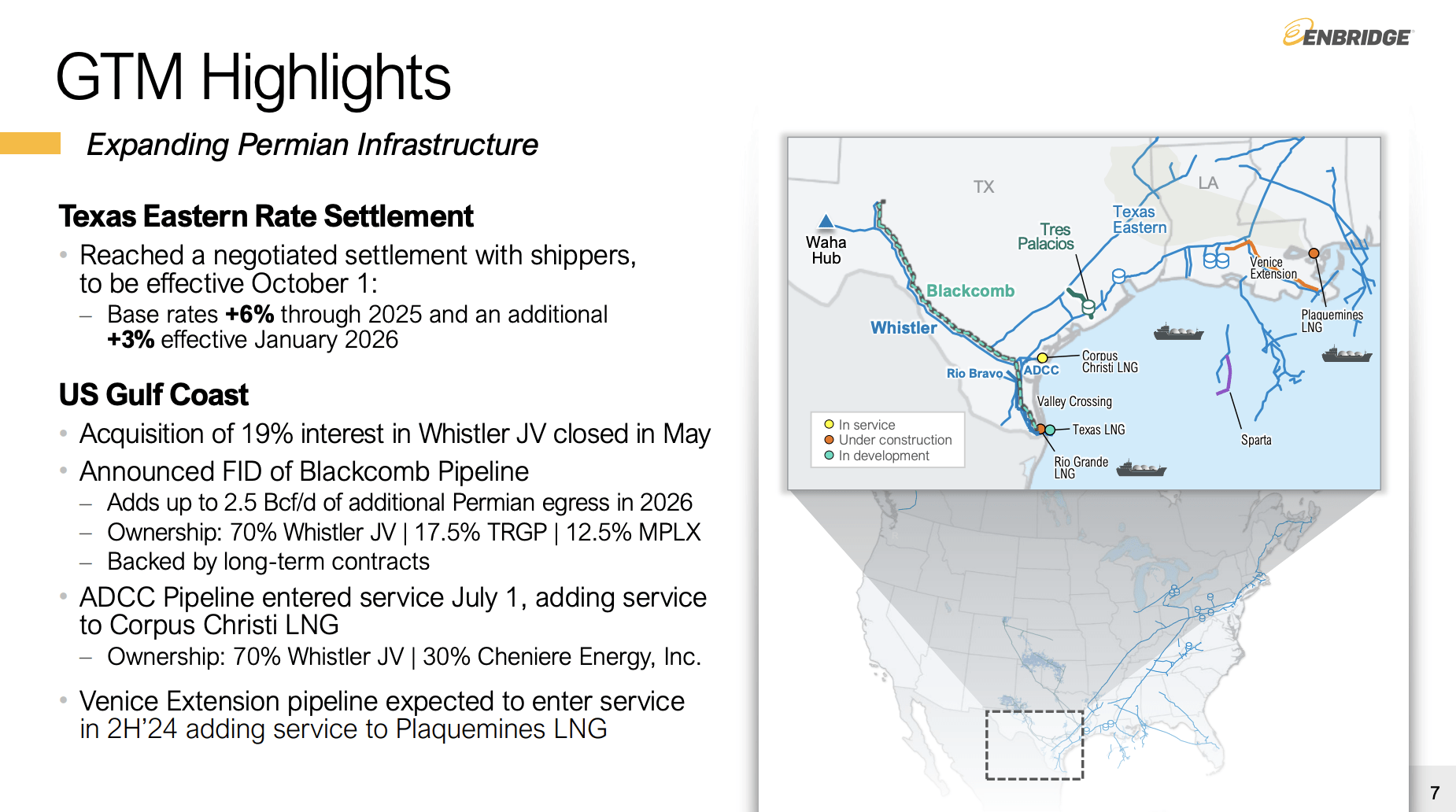

Additionally, the company’s involvement in the Whistler Joint Venture has led to the final investment decision for the Blackcomb Pipeline. This pipeline is expected to provide up to 2.5 billion cubic feet per day of critical natural gas takeaway (egress) for Permian shippers at a time when, in some areas, natural gas prices are negative due to elevated production and poor pipeline access.

Enbridge

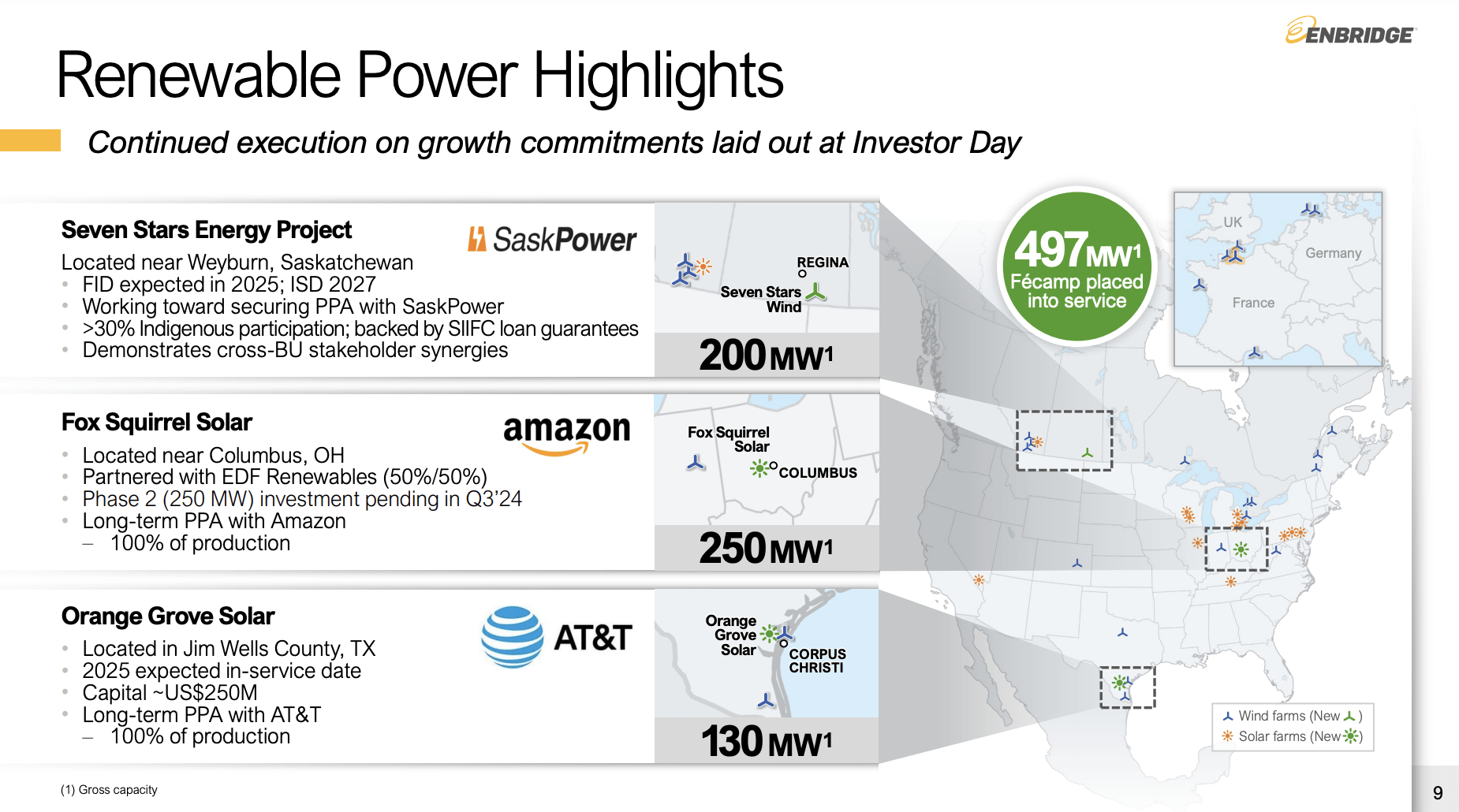

It’s also expanding its renewable energy footprint through projects like its 130-megawatt Orange Grove solar project in Texas and the Seven Stars wind project in Saskatchewan, Canada.

Enbridge

In other words, Enbridge isn’t just large, but also critical in serving North America’s rising oil and gas volumes.

This bodes well for shareholders.

Enbridge Is A Deep-Value Income Play

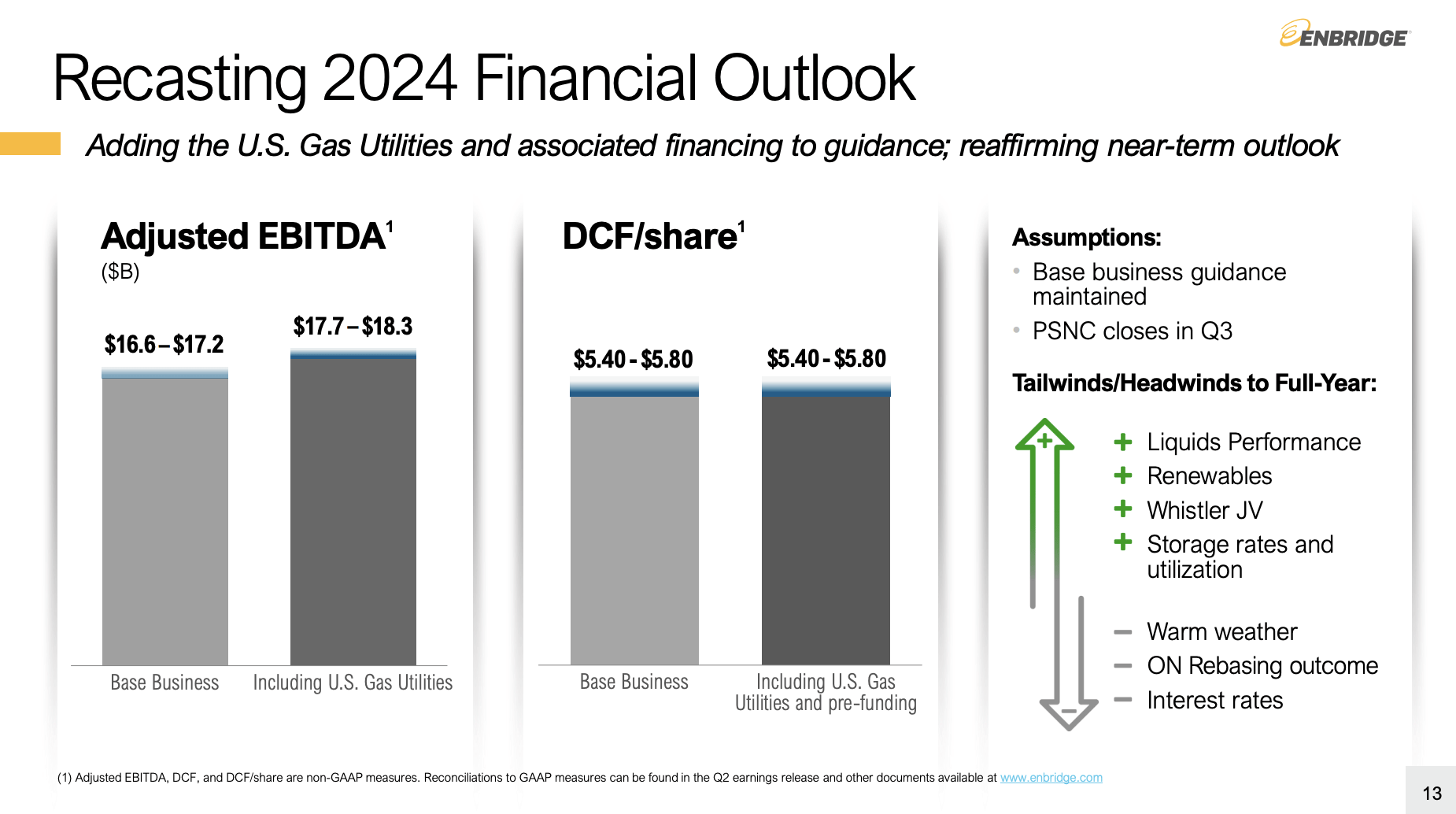

Based on everything said so far, the company is doing well, as it raised its full-year guidance, incorporating the closing of its natural gas utilities acquisitions.

It now expects full-year EBITDA to be in the range of $17.7 billion to $18.3 billion, with expected annual EBITDA growth of 7% to 9% through at least 2026.

Enbridge

This medium-term outlook includes 4-6% annual EPS growth and 3% distributable cash flow (“DCF”) per share growth.

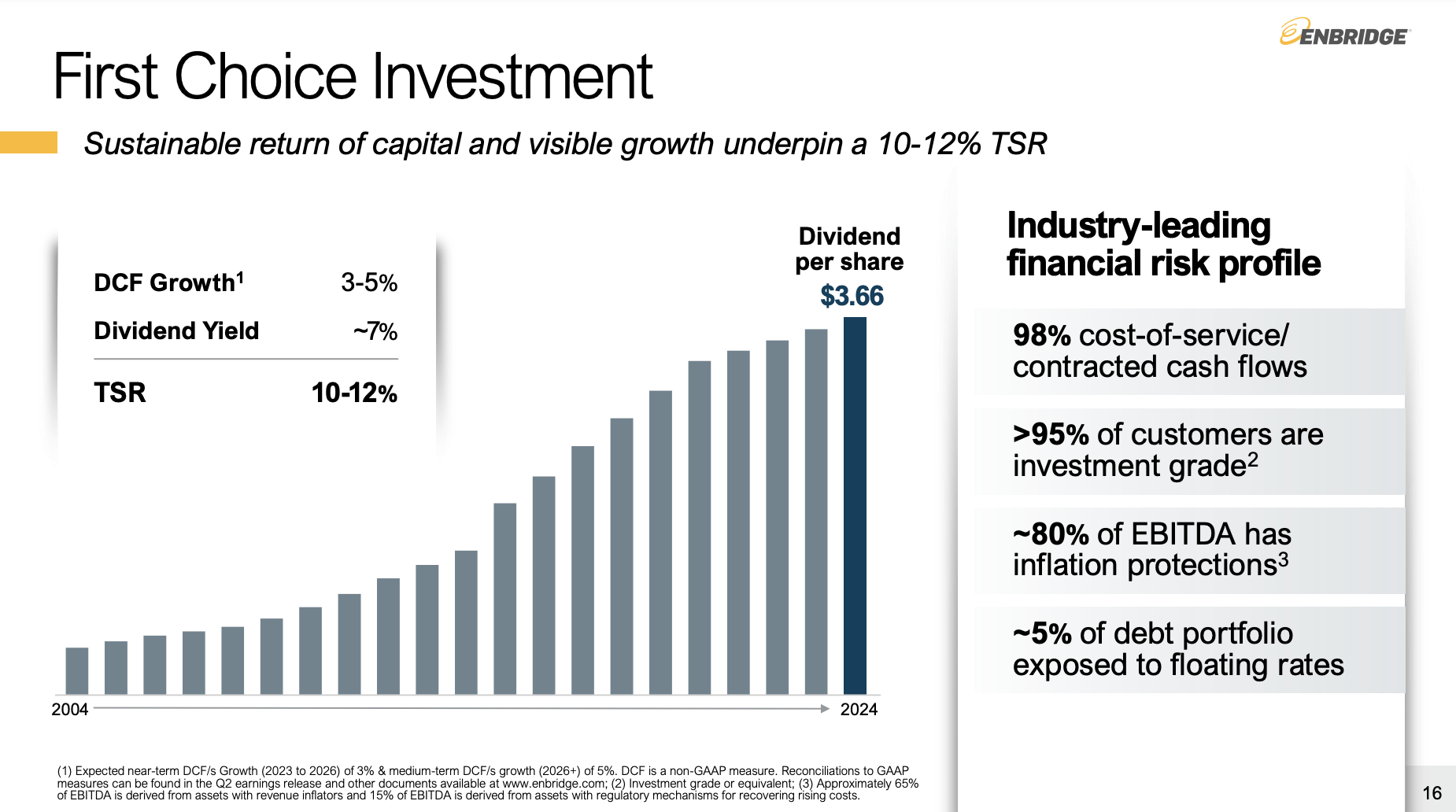

It also brings a lot of safety to the table. Not only are 98% of its earnings coming from cost-of-service or take-or-pay contracts, but it also enjoys built-in inflation protection in most of its contracts. In fact, Enbridge noted that 80% of its EBITDA is protected by inflation.

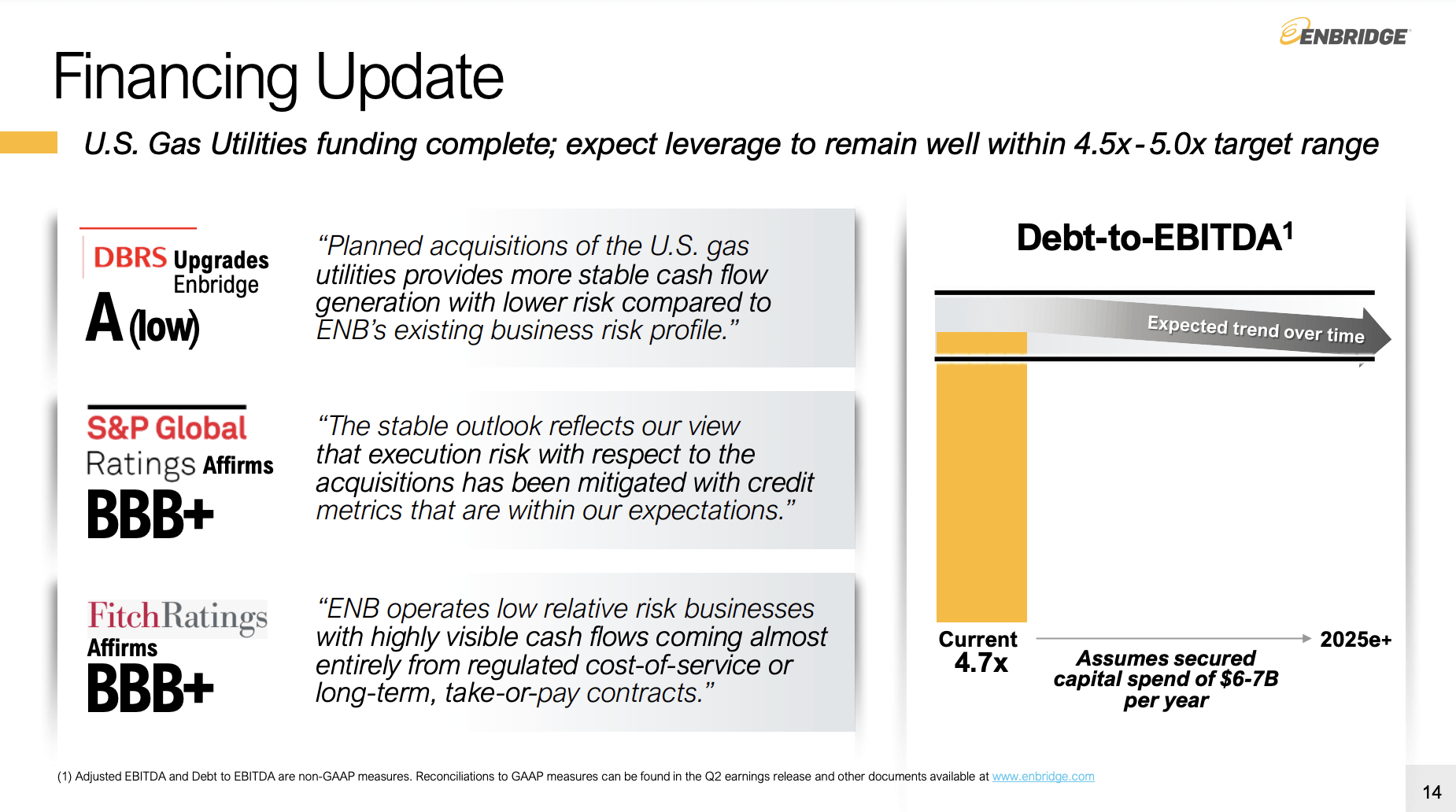

On top of that, it has a BBB+ credit rating from S&P Global and Fitch. Both affirmed these ratings, supported by healthy credit metrics and cash flow visibility. Currently, the net leverage ratio is 4.7x (EBITDA), well within the 4.5x-5.0x range. Only 5% of its debt has variable rates, which adds another layer of safety.

Enbridge

The mix of a fantastic business model, secular growth opportunities, and a healthy balance sheet are great for shareholders.

ENB has hiked its dividend for 29 consecutive years and remains committed to sustaining and growing its dividend, supported by healthy cash flow and prudent capital management. Currently, ENB pays $0.915 per share per quarter. This translates to a yield of 7.0%.

The five-year dividend CAGR is 5.1%, protected by a 2Q24 DCF payout ratio of 68%.

Enbridge

Even better, as we can see above, for the foreseeable future, Enbridge aims to deliver an annual total shareholder return of 10% to 12%, driven by a combination of cash flow growth, a growing dividend, and strategic capital allocation.

Essentially, a total return is the company’s dividend in addition to earnings or DCF growth.

If you receive a 7% annualized dividend, 3-5% annual DCF growth results in a total return of at least 11% *IF* the valuation multiple remains unchanged. After all, a stock trading at 10x DCF (I made that up) will see capital gains equal to per-share DCF growth if the valuation remains unchanged.

A higher valuation will lead to even higher gains. A lower valuation multiple will lead to lower gains. The company can influence the dividend and per-share DCF growth. It cannot influence the valuation multiple. That’s the market’s job.

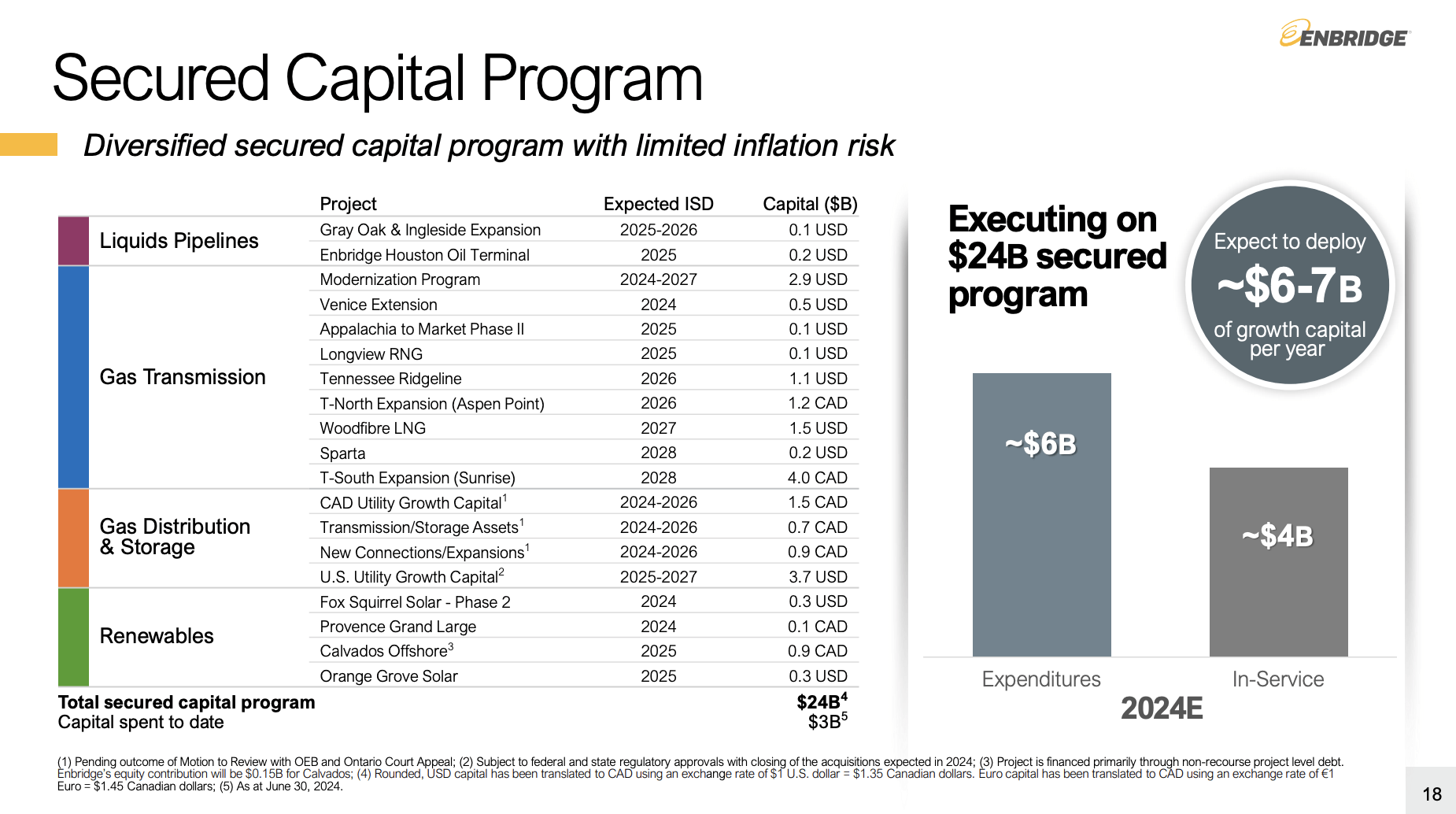

However, before we get to the valuation, I need to mention that the company has plans to invest between $6 billion and $7 billion per year in growth capital, with an additional $2 billion for strategic opportunities that include new projects, acquisitions, or debt reduction.

Enbridge

So, what about its valuation?

Valuation

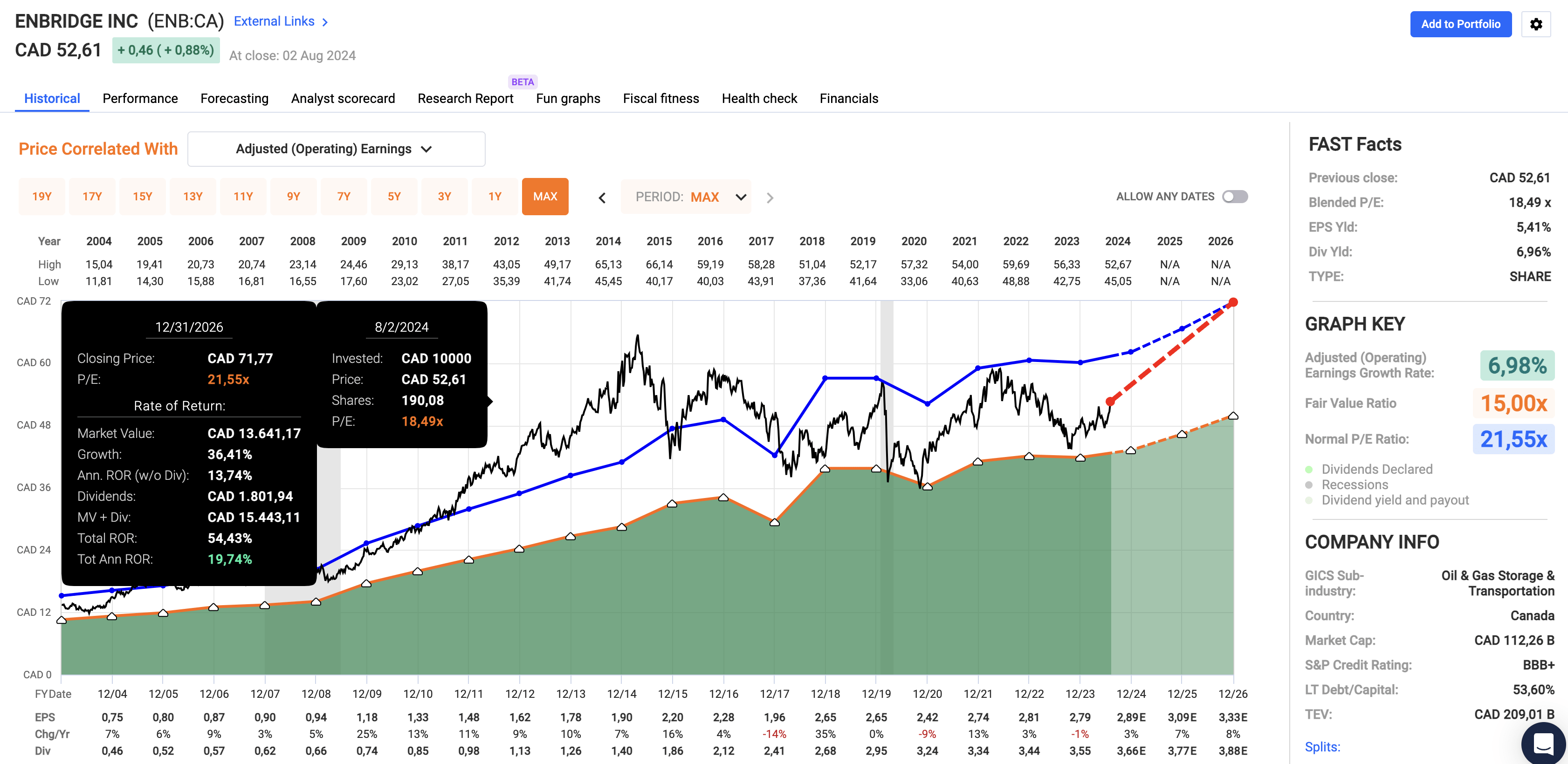

Since my May article, analyst estimates have improved. On May 13, expectations were for $3.25 in 2026 EPS. Now, that number is $3.33.

Moreover, the company trades at a blended P/E ratio of just 18.5x, below its normalized P/E multiple of 21.6x.

Assuming analysts are right (using FactSet data in the chart below), we could see an annual EPS growth acceleration from 3% in 2024 to 7% in 2025 and 8% in 2026. This paves the road for a fair stock price of C$72 in Toronto, 37% above the current price.

FAST Graphs

The same applies to New York-listed shares, with the addition of currency risks.

Hence, while I believe the company has the potential to deliver 10-12% annual total returns on a long-term basis, I expect the returns in the years ahead to be higher due to its favorable growth outlook and attractive valuation.

Needless to say, this means I maintain a Strong Buy rating.

Takeaway

Enbridge might have disappointed investors over the past decade, but recent developments paint a more promising picture.

Despite the lackluster past performance, I’m very bullish on Enbridge due to its fantastic pipeline assets, strategic acquisitions, and commitment to consistent dividend growth.

Moreover, I believe the company’s ability to capitalize on increasing oil and gas volumes, combined with a solid balance sheet and a very attractive valuation, sets it up for long-term growth and potentially elevated annual returns.

Pros & Cons

Pros:

Robust Infrastructure: Enbridge owns North America’s largest pipeline system, handling 30% of U.S. crude oil and 20% of natural gas.

Consistent Dividend: With a 7% yield and 29 consecutive years of dividend hikes, ENB offers reliable income.

Growth Potential: Strategic expansions in gas utilities and renewable energy, in addition to record pipeline volumes, put ENB in a great spot for long-term growth.

Valuation: ENB is trading at a very attractive multiple, supported by a good growth outlook and a juicy yield to enhance the total return.

Cons:

Past Performance Concerns: Despite recent improvements, ENB’s long-term performance has been lackluster, which may keep investors at bay – although it looks like this is changing now.

External Risks: As a midstream company, ENB is subject to market fluctuations, regulatory changes, and other industry-specific risks that could impact its performance.

Economic Weakness: While ENB benefits from a fee-based business with utility-like safety, potential economic weakness could cause growth rates to come in lower than expected.