JHVEPhoto

Investment summary

My previous investment thought for ZoomInfo Technologies (NASDAQ:ZI) (published on 30th May) was a sell rating because valuation was relatively expensive compared to peers that are experiencing similar growth weakness. Indeed, ZI’s share price has fallen sharply since the end of May, from ~$12 to $9 today, with valuation multiple revised from 4.4x forward revenue to 3.6x. I am now hold-rated for ZI as I await more evidence of demand recovering that translates into revenue growth.

Poor 2Q24 performance due to SMB write-offs

Released a few days ago on the 5th of August, ZI saw a total revenue decline of 5.6% y/y, a deceleration from the 3.1% growth seen in 1Q24. Total revenue came in at $291.5 million. This drove adj EBIT margin down from ~40% in 2Q23 to 28% in 2Q24, which led to an adj EPS performance of $0.17, down from $0.26 in 2Q23. The main drag to the business was the poor performance in the SMB segment, which led to an elevated level of write-offs vs. 2Q23. The write-offs stemmed from an increased rate of nonpayment for credit ZI extended to customers over the past two years. After all the adjustments, ZI recognized a $33 million incremental charge in this quarter.

Signs of demand stabilization

The good news is that the demand environment seems to have stabilized. Customer growth metrics have finally turned positive after multiple quarters of negative growth. For instance, the total number of customers with more than $100k in annual contract value [ACV] grew 2.1% sequentially after five consecutive quarters of decline. The same trend was seen in customers with more than $1 million in ACV. While the actual figures were not disclosed, management indicated they saw the most sequential additions in six quarters, with ACV growth for this cohort accelerating to 17% y/y. Furthermore, in terms of new business deals, the comments given also painted a strong “turnaround” trend. Specifically, ZI signed its largest new business deal of $1.4 million in ACV (3-year commitment), and 2Q24 also set the record for being the best new business quarter in the mid-market and enterprise.

we again grew our million dollar plus customer cohort on a sequential basis with the most new million dollar plus customers since Q4 of 2022. 2Q24 earnings transcript

In terms of the existing customer base, 2Q24 also marked the first quarter that the dollar-based net retention rate [DBNRR] did not deteriorate, coming in at 85% (same as 1Q24). For reference, this is the first quarter of stabilization since 4Q21. Note that this is despite ZI still facing strong SMB headwinds. Which means, if we just zoom into the upmarket segment, ZI should be seeing very strong DBNRR trends (my assumption is that SMB DBNRR is still down, and if overall DBNRR is stable, it implies upmarket DBNRR is trending upwards). This dynamic makes sense given that large enterprises are generally the first to recover after a major macro slowdown. What this also means is that ZI should see SMB demand recover as the macroclimate gets better (Fed cutting rates is a near-term catalyst).

Putting macro drivers aside, it was certainly encouraging to see ZI’s Copilot performing ahead of management expectations. Notably, the product was adopted by the majority of ZI’s customers; they noted >1,000 logos contributed $18 million in ACV, which means more than half have used the product. Perhaps the more important point noted was that users are showing material improvements in engagement and utilization rates. The latter point is important because it shows that the product works, and this instills confidence that more adoption can take place. The financial impact of ZI Copilot should gradually become more prominent as adoption picks up, given that it is pricing accretive.

So Henry mentioned the monetization of Copilot. There are a number of opportunities where we’re beginning to see pricing uplift from that and that’s something that we’re focused on being able to continue as we move into Q3 and Q4. 2Q24 earnings transcript

Guidance seems conservative

Management FY24 guidance is likely to be conservative as it: (1) does not assume any upfront prepayment from riskier SMB customers and assumes a higher rate of write-offs for 2H24, despite the operational changes made; and (2) does not embed recent positive trends seen in its upmarket for the rest of the year. I can understand why the former point contributes to a conservative guide, since SMBs are still being pressured. However, for the latter point, it seems like management is just being overly conservative. In my opinion, this leaves plenty of room for upside surprises. For what it’s worth, ZI has beaten its own adj EPS guidance 15 out of the past 16 quarters by an average of 20% and 14 out of the past 16 quarters for its revenue guidance by 4%.

Valuation

Redfox Capital Ideas

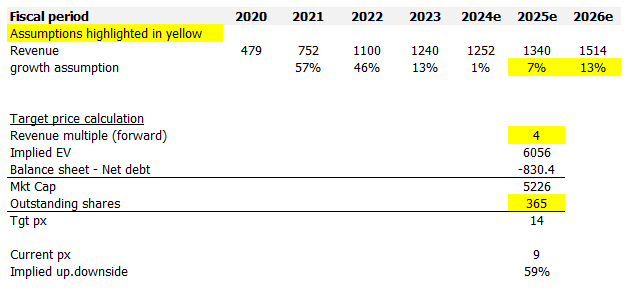

I am giving a hold rating to ZI despite the upside because I want to see more evidence of demand growth. However, assuming demand recovers nicely, and it translates to revenue growth back to FY23 levels of 13% starting from the 1% growth base in FY24, which I derived from assuming ZI beat FY24 revenue guidance by 400 bps (ZI historical track record), the upside could be huge as multiples could inflect upwards. I am using 4x as a starting point to think about ZI’s multiple, as this was the level that it traded at before the market priced in the relatively weak growth (refer to my previous post for more details). In an accelerating growth situation, I would expect the market to rerate ZI’s multiples upwards accordingly.

Risk

It is still unknown whether ZI has seen the worst of the SMB write-off situation. Although operational changes have been made, it does not guarantee that ZI can avoid further write-offs, as the underlying reason is largely related to SMBs going out of business or being unable to get funding. These are macro-related reasons that are outside of ZI’s control. If the underlying situation gets worse, ZI could see further headwinds that cause it to miss guidance.

Conclusion

My view for ZI is a hold rating as I await more signs of growth recovery. 2Q24 performance was mixed as it faced significant headwinds in the SMB segment, leading to write-offs and revenue declines, but also saw encouraging signs of stabilization. In particular, customer growth metrics, particularly in the upmarket, are showing positive momentum, and the Copilot product is gaining traction. However, given the ongoing uncertainties in the SMB market, I think it is safer to wait for more solid signs of growth recovery before turning bullish.