Millionaires and million-dollar homes, they’re on the rise. Almost one in 10 homes in the country are valued at $1 million dollars or more. It’s the greatest share on record in history, higher than last year, and more than double than before the pandemic, according to an analysis from Redfin.

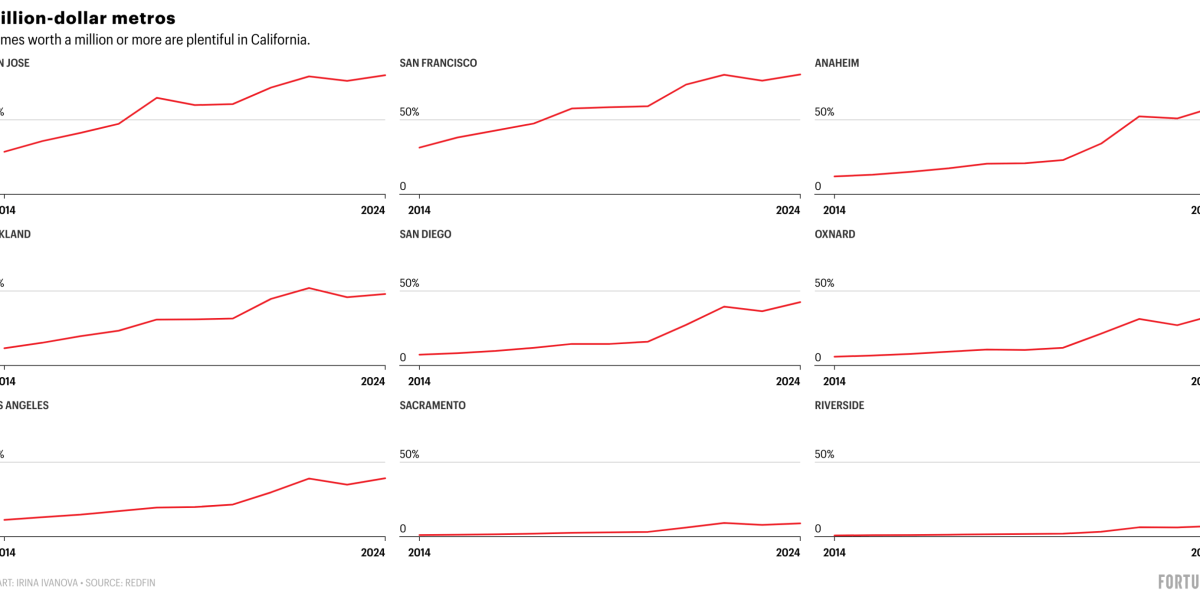

So which state holds the most million dollar homes? None other than California. And “pricey California metros are gaining million-dollar homes faster than anywhere else in the U.S.,” the analysis states. So not only does California already have more seven-figure homes than anywhere else in the country, it’s seeing them expand faster, too. They rose the most in Anaheim, San Diego, and Los Angeles, where the share of homes worth $1 million or more, are roughly 59%, 43%, and 39%, respectively. “Those places are gaining seven-figure homes fast because the median home price in each of those metros is around $1 million, meaning there were a lot of homes poised to jump over the million-dollar mark,” Redfin said.

In San Francisco and San Jose, around 80% of their homes are worth at least a million. Let that sit. Redfin doesn’t necessarily concentrate on why that is, apart from pointing to their median sale prices—but we know these opulent, stunning coastal cities struggle to build more homes; they are prime examples of California’s housing crisis, and it’s shutting typical people out. “The people who are buying without hesitating are in tech and work at Google, Apple, Facebook or a similar company,” a Bay Area-based Redfin agent said in the analysis.

And it isn’t only California either. Million dollar plus homes are everywhere; some 47 out of 50 of the most populous metropolitan areas saw the share of million-dollar homes swell in the past year. The three that didn’t were Austin, Indianapolis, and Houston—and in the former, they actually fell, whereas in the latter two, they remained unchanged. The two Texas cities are known for building more homes to meet demand, and that’s pushing home prices down, or in the very least, keeping them from continuing to soar.

Home prices rose substantially throughout the pandemic, and in the last year, they’ve continued to rise, albeit slower. All the while, prices for luxury homes are increasing even faster. “Prices of luxury homes rising has an outsized impact on the share of homes worth at least $1 million because a major portion of them have long been on the cusp of hitting the million-dollar mark, and just did,” the analysis read.

In typical housing cycles, when mortgage rates shoot up (as they have in the aftermath of the pandemic) and demand softens and sales weaken, home prices fall. Redfin’s chief executive Glenn Kelman said it himself, in a prior interview with Fortune, that he’s never seen anything like this. “I was the CEO during the Great Financial Crisis,” he said. “Sales volume went down but prices did, too.” But we have a supply problem: there aren’t enough homes, and a lot of people who have below-market mortgage rates don’t want to sell. Inventory has improved, but it hasn’t caught up to pre-pandemic levels. It’s a killer combination that happens to be rough for anyone who wants to buy a home and kind of fantastic for anyone who already owns a home.

Still, as Redfin points out, there are metros where million dollar homes are close to none, such as Detroit, Cleveland, Pittsburgh, and Kansas City. But because that’s only four metropolitan areas out of 50, where less than 1% of homes have a seven-figure tag, I don’t know how much comfort that’ll bring. Not to mention starter homes are on the decline.