UPCOMING

EVENTS:

- Monday: PBoC MLF, German IFO, US Durable Goods Orders.

- Tuesday: US Consumer Confidence.

- Wednesday: Australia Monthly CPI, Nvidia Earnings.

- Thursday: US Q2 GDP 2nd Estimate, US Jobless

Claims. - Friday: Tokyo CPI, Japan Retail Sales, Eurozone Flash

CPI and Unemployment Rate, Canada GDP, US PCE.

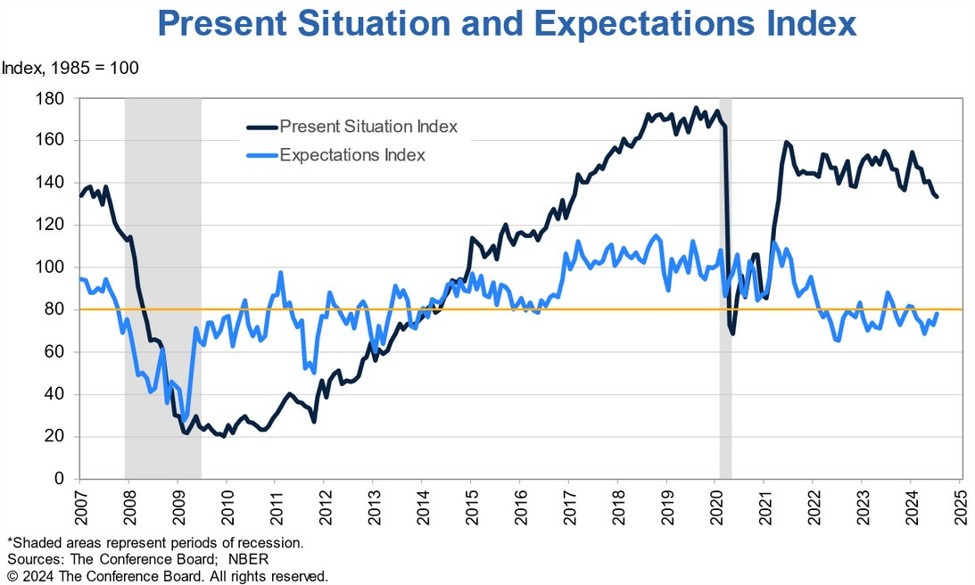

Tuesday

The US Consumer

Confidence is expected at 100.1 vs. 100.3 prior. The last report saw the present situation index, which is generally a

leading indicator for the unemployment rate, falling to a three-year

low.

Dana M. Peterson,

Chief Economist at The Conference Board said: “Confidence increased in July,

but not enough to break free of the narrow range that has prevailed over the

past two years. Compared to last month, consumers were somewhat less

pessimistic about the future.”

“Expectations for

future income improved slightly, but consumers remained generally negative

about business and employment conditions ahead. Meanwhile, consumers were a

bit less positive about current labour and business conditions.”

“Potentially,

smaller monthly job additions are weighing on consumers’ assessment of current

job availability: while still quite strong, consumers’ assessment of the

current labour market situation declined to its lowest level since March 2021”.

US Consumer Confidence

Wednesday

The Australian

Monthly CPI Y/Y is expected at 3.4% vs. 3.8% prior. The RBA continues to

maintain a hawkish stance, while the market keeps on expecting at least one

rate cut by the end of the year.

Australia Monthly CPI YoY

Thursday

The US Jobless

Claims continues to be one of the most important releases to follow every week

as it’s a timelier indicator on the state of the labour market.

Initial Claims

remain inside the 200K-260K range created since 2022, while Continuing Claims

have been on a sustained rise showing that layoffs are not accelerating and

remain at low levels while hiring is more subdued.

This week Initial

Claims are expected at 234K vs. 232K prior, while Continuing Claims are seen at

1870K vs. 1863K prior.

US Jobless Claims

Friday

The Tokyo Core CPI

Y/Y is expected at 2.2% vs. 2.2% prior. As a reminder, the economic indicators

the BoJ is focused on include wages, inflation, services prices and GDP gap.

The Tokyo CPI is seen as a leading indicator for National CPI, so it’s generally

more important for the market than the National figure.

Moreover, Governor

Ueda kept the door open for rate hikes as he said that the recent market moves

wouldn’t change their stance if the price outlook was to be achieved and added

that Japan’s short-term interest rate was still very low, so if the economy

were to be in good shape, BoJ would move rates up to levels deemed neutral to

the economy.

Tokyo Core CPI YoY

The Eurozone CPI

Y/Y is expected at 2.2% vs. 2.6% prior, while the Core CPI Y/Y is seen at 2.8%

vs. 2.9% prior. This report won’t change anything for the ECB as the central

bank is going to cut rates by 25 bps in September.

Eurozone Core CPI YoY

The US PCE Y/Y is

expected at 2.5% vs. 2.5% prior, while the M/M figure is seen at 0.2% vs. 0.1%

prior. The Core PCE Y/Y is expected at 2.7% vs. 2.6% prior, while the M/M

reading is seen at 0.2% vs. 0.2% prior. Forecasters can reliably estimate the

PCE once the CPI and PPI are out, so the market already knows what to expect.

This report won’t

change anything for the Fed as they will cut rates in September no matter what.

The Fed is now focused on the labour market and the next NFP report is going to

decide whether the FOMC will cut by 25 or 50 bps at the upcoming decision

on the 18th of September.

US Core PCE YoY