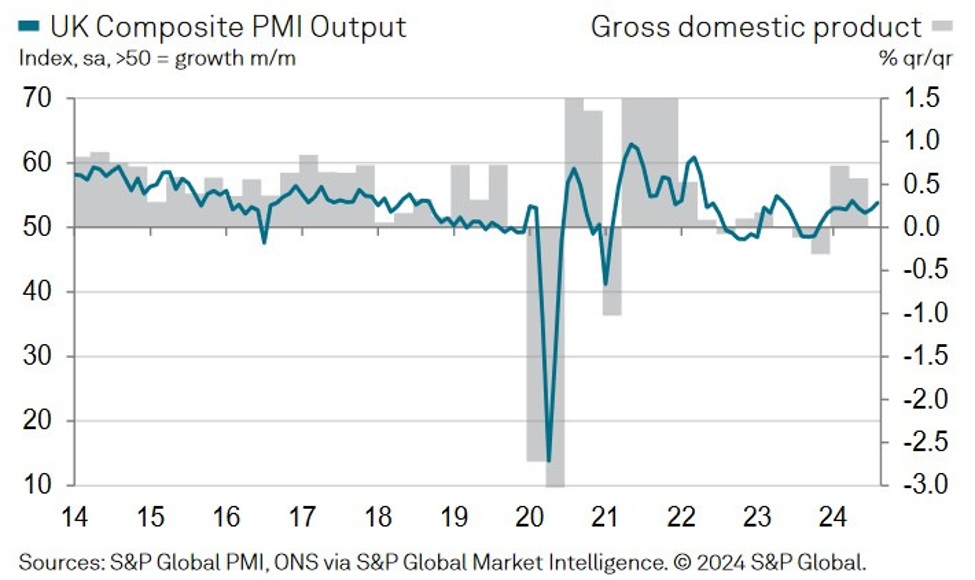

- Final Services PMI 53.7 vs. 53.3 expected and 52.5 prior.

- Final Composite PMI 53.8 vs. 53.4 expected and 52.8 prior.

Key findings:

- Business activity growth accelerates again.

- Robust rise in new work led by improving

domestic demand. - Slowest rate of prices charged inflation for three-

and-a-half years.

Comment:

Tim Moore, Economics Director at S&P Global Market

Intelligence

“August data highlighted a recovery in UK service sector

performance as improving economic conditions and

domestic political stability helped to bolster customer

demand. New business again increased at a robust pace

after a lull in decision-making earlier this summer.

This

fuelled the fastest upturn in service sector activity since

April and extended the current period of growth to ten

months.

Service providers responded to the upturn in business

conditions by hiring additional staff in August.

Job creation

remained faster than seen on average in the first half of

2024, despite headwinds from scarce candidate availability

and elevated wage pressures.

Higher salary payments resulted in another sharp rise

in cost burdens across the service economy.

However,

the overall rate of input price inflation resumed its recent

descent in August and reached its lowest since January

2021. Adding to meaningful signs of softer inflationary

pressures in the service sector, the latest survey indicated

that average prices charged increased at the weakest pace

for three-and-a-half years.

The modest post-election bounce in business activity

expectations faded, however, in August. Hopes of interest

rate cuts and steady improvements in broader economic

conditions helped to support confidence, but some firms

cited concerns about policy uncertainty in the run up to the

Autumn Budget.”

UK Composite PMI