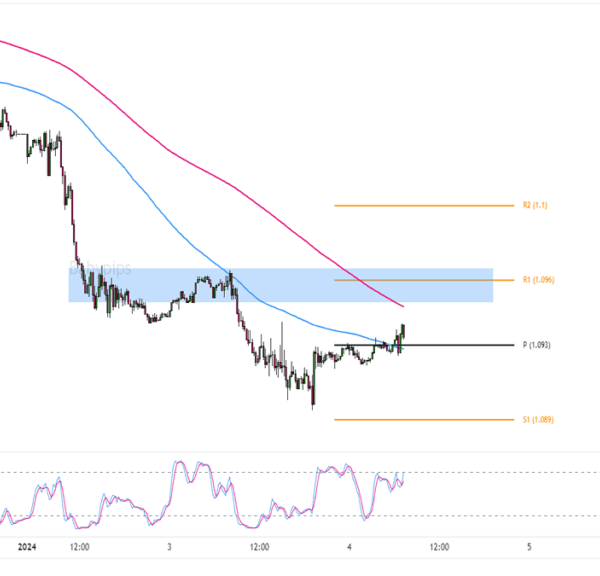

With so much scrutiny on the US labour market at the moment, it doesn’t come any bigger than jobs Friday. The non-farm payrolls data is going to be key in deciding how markets end the week. And it won’t be just the headline number, the details are going to matter too – especially the unemployment rate.

Yesterday, we got a bit of a taste of the mixture of key US data this week:

I would argue that the ADP was akin to the flop in poker and the ISM services PMI was like the turn. A quick Google will give you the gist of those terms but I’m sure it feels like you already know them. And that will make the non-farm payrolls data today the river i.e. final card dealt face up on the table.

The flop signaled further cooling in the US labour market. However, much like the ADP itself, it isn’t the be all, end all indicator for how the round is going to play out. The turn certainly kept things interesting as the ISM services PMI hinted that other parts of the economy is still doing fine.

So, there’s a balance to be struck there in weighing further downside risks to the dollar and a more dovish Fed.

And it will all come down to the river today with perhaps the most important piece of data in markets over the last three months. It’s no longer the US CPI report that is the ace in terms of economic releases. That mantle has now been taken by the US jobs report instead.

Traders are currently pricing in ~43% odds of a 50 bps rate cut for this month and ~110 bps for what’s left in 2024. It’s now a question of validation. And that is where market players will have to look to the river to decide if the odds are in their favour or not.

From yesterday: