PM Images

Written by Nick Ackerman, co-produced by Stanford Chemist

Tortoise has been busy restructuring their business back into a traditional energy and power infrastructure investment firm. That came with the new CEO announcing that they will sell the Ecofin Advisors Limited business and its private credit business. That would be removing the part of the business that was more focused on sustainable infrastructure and renewable investments.

Alongside this restructuring, it’s come with a shake-up in their closed-end fund business as well. So far, the announcements have left out what exactly they intend to do with Ecofin Sustainable and Social Impact Term Fund (TEAF), which is geared toward investing in renewables with a significant focus on private investments as well. However, they haven’t forgotten about the fund, as they recently implied that changes could be on the horizon.

TEAF Basics

- 1-Year Z-score: 2.65

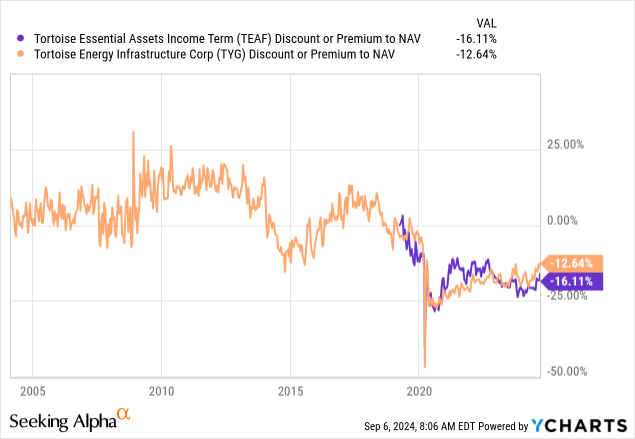

- Discount/Premium: -16.11%

- Distribution Yield: 8.67%

- Expense Ratio: 1.85%

- Leverage: 11.10%

- Managed Assets: $229 million

- Structure: Term (anticipated liquidation date around March 27, 2031)

TEAF was launched with the goal of “attractive total return potential with emphasis on current income and uncorrelated assets.” Additionally, “access to differentiated direct investments in essential assets” and “investments intangible, long-lived assets and services.” TEAF is also targeting a “positive social and economic impact.”

Weaker Results Could Prompt Strategy Shift

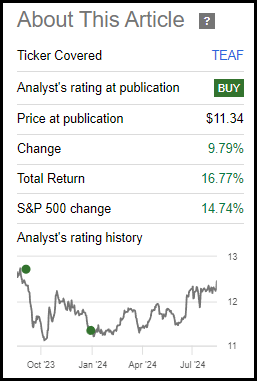

Since our last update, the fund has done rather well in terms of total returns. A large portion of this was thanks to the discount narrowing from the ~24% level to now narrowing to around a 16% discount.

TEAF Performance Since Prior Update (Seeking Alpha)

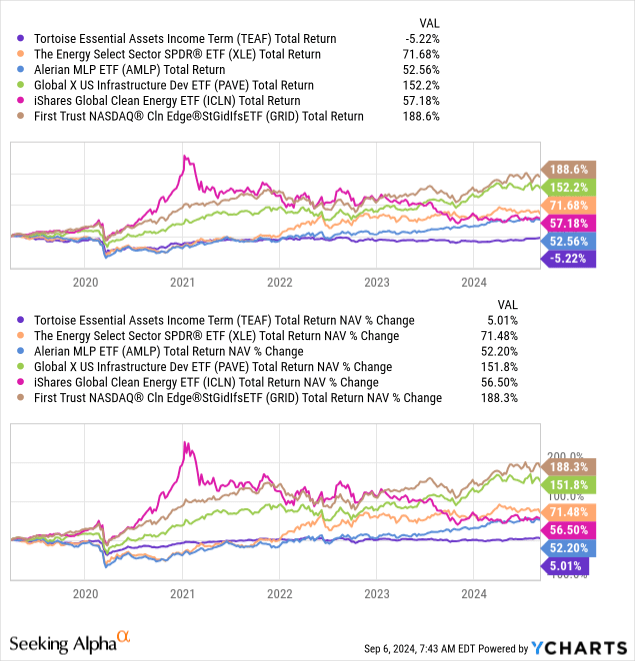

That said, that has not generally been the case as the longer term, the fund has had rather poor results. That’s whether you look at traditional energy/infrastructure ETF performance or clean energy ETF performance. Which TEAF is more a mixture of the two being blended together, then adding private investments. This also includes primarily debt investments and not equities, which is another difference between the ETFs that I’m using as a comparison here.

YCharts

Having exposure to private investments can produce the potential for greater rewards in the long run, but they just haven’t been able to seem to capitalize on that. That has generally meant the best reason to own TEAF was the sizeable discount that the fund frequently traded at. Being able to capitalize on that discount for greater potential potentially upside could possibly take place in the future as they’ve made a number of moves so far in their CEF lineup.

Last month, they announced that they would be looking to merge the Tortoise Power and Energy Infrastructure Fund (TPZ), Tortoise Pipeline & Energy Fund (TTP) and Tortoise Energy Independence Fund (NDP) into an ETF structure. We even noted that this could be something that NDP was going to have happened shortly before it was announced.

This would be similar to what we saw with First Trust doing to a number of their energy-focused CEFs as well. TPZ is going to be the surviving fund if the merger is approved.

Even more recently, we saw the announcement that Tortoise Midstream Energy Fund (NTG) and Tortoise Energy Infrastructure Corp (TYG) were also approved by the Board to merge but remain a closed-end fund structure. This deal will still require shareholder approval, as will the merger between TPZ, TTP and NDP to merge and convert to an ETF structure. If the NTG and TYG tie-up is approved, the fund will also switch to a monthly distribution schedule and increase its distribution by 40%.

That leaves only the black sheep of the family, TEAF, which they haven’t made a move on yet. However, it wasn’t forgotten about, as they did mention in the NTG and TYG announcements that they are still looking at their options for the fund.

In addition, Tortoise Capital intends to conduct a strategic review of the investment strategy of its closed-end fund Ecofin Sustainable and Social Impact Term Fund (NYSE: TEAF), including the impact of blending private and public investments in a closed-end fund. TEAF provides investors access to a combination of public and private investments in essential assets. TEAF had total assets, including leverage, of $229.0 million as of Aug. 31, 2024.

“As part of our product restructuring, we are evaluating our entire fund lineup and are making changes that are in the best interest of fund shareholders,” said Tom Florence, CEO of Tortoise Capital Advisors. “We have been disappointed with TEAF’s performance and its discount to NAV and aim to correct the issue.”

Not only does TEAF have the renewables focus in their business, which Tortoise is now divesting itself away from, but it comes with a term structure—that is, the fund is expected to liquidate in the future at whatever the NAV per share is at that time. The anticipated liquidation date, in this case, is March 27, 2031. There are always ways for the fund to extend this or become perpetual, but nonetheless, it is another consideration as these other funds are already perpetual.

With that said, the main line that caught my attention here is the “conduct a strategic review of the investment strategy…” That, to me, suggests that they are looking to change the investment policy to be more in line with the other sister funds, which are more invested in traditional infrastructure investments. At that point, with a sizeable portion of private investments, it would take the fund some time to convert over. However, just the idea of the fund changing strategy could garner more interest.

In the future, being that it is a smaller fund it could also look to be merged into presumably what would be a larger TYG. The combination of NTG and TYG, should it occur, would make a ~$900 million total managed asset fund. With TEAF at ~$229 million in total managed assets, reducing some private investments and shaving down its renewable exposure would ultimately make it a better fit for TYG.

At that time, it wouldn’t dramatically change the TYG fund either due to the meaningfully larger size of TYG—and TYG investment policy leaves the door open for private investments as well as renewable-specific infrastructure exposure.

In that potentially playing out in the future, investors would have to consider and approve removing the term structure of the fund as well. With a sizeable discount, and if TYG is able to narrow its discount more meaningfully on the back of the increased distribution and switch to monthly, then it could make sense for TEAF investors to take up the offer.

YCharts

Seeing TEAF change its investment policy wouldn’t be all that much of a shock, either. This is because Saba Capital Management, an activist group, is in this fund at an over 9% stake—it should also be noted that all of these changes in the CEFs have been presumably activist-driven.

Saba owns a nearly 10% stake in NTG. An increased distribution and monthly payout could see the discount narrow materially where they would benefit upon a merger. Saba also owned a 9.6% stake in NDP, along with other notable activist Bulldog Investors. Saba owns nearly 9% of TTP, TPZ is owned largely by Relative Value Partners Group at ~13%, and Bulldog Investors Holds a 6.19% stake.

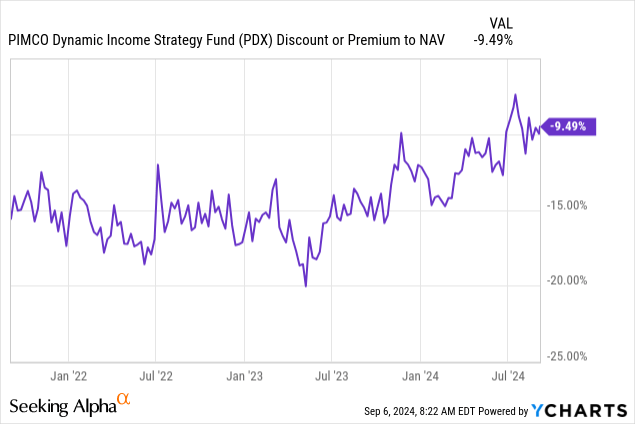

So Saba is looking to profit handsomely on all of these moves that are efforts to realize discounts in these funds. No doubt, they are in active discussion with getting TEAF to shake things up with the fund, as they had done previously with PIMCO. That saw the PIMCO Dynamic Income Strategy Fund (PDX) become what it is today, as it was formerly an energy-focused fund called PIMCO Energy and Tactical Credit Opportunities Fund under the ticker “NRGX.”

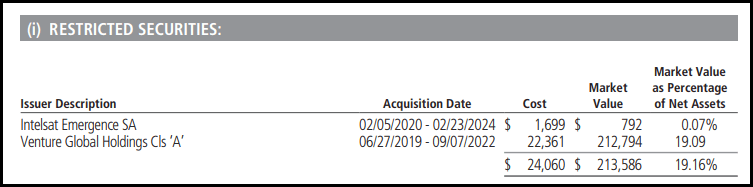

They announced a transition to the new name and investment policy that made PDX a fund similar to the rest of the PIMCO suite of multi-sector bond funds. That said, PDX has its own ‘issues,’ with its largest holding being a private and restricted equity position in Venture Global Holdings. That is the fund’s largest position at around 19%—which became such a large holding thanks to significant market value appreciation.

PDX Restricted Securities (PIMCO)

Even further, after announcing their transition, they took down their allocation to energy C-corp positions but have simply moved most of that to master limited partnership (“MLP”) positions. That’s left the fund largely still an energy-focused fund, which, admittedly, they left the door open to do just that. In their policy, they note that “normally invests at least 25% of its total assets in the energy industry.”

Regardless of whether it was just the optics of the policy and name change or the change in the distribution policy, the discount has been narrowing for PDX quite materially. Of course, I’m also a proponent of advocating for profiting from this move, as I’ve taken a position in the fund as well.

YCharts

In the case of TEAF, just a change in the investment policy is likely not enough. After all, the other Tortoise CEFs trade at fairly sizeable discounts as well. As of their last semi-annual report, ~40% of the fund was invested in restricted securities. So, trying to get approval to convert over to an ETF at this point simply is not an option. That means it could be interesting to see what they may be able to come up with in this scenario to entice investors.

Conclusion

TEAF finds itself in an odd position as its fund sponsor looks to shy away from the renewable business it had previously been trying to build up. The fund has produced mixed results historically, but with some activist pressure, the fund could look to get a shake-up soon. What that ultimately looks like for TEAF could be different from its sister funds due to its unique characteristics of sizeable private investments and its term structure. Whatever is announced, though, if it gets the Saba stamp of approval, it more than likely will result in the discount narrowing.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.