UPCOMING

EVENTS:

- Monday: China CPI.

- Tuesday: UK Labour Market report, US NFIB Business

Optimism Index. - Wednesday: UK GDP, US CPI.

- Thursday: Japan PPI, ECB Policy Decision, US PPI, US

Jobless Claims. - Friday: New Zealand Manufacturing PMI, US University of

Michigan Consumer Sentiment.

Monday

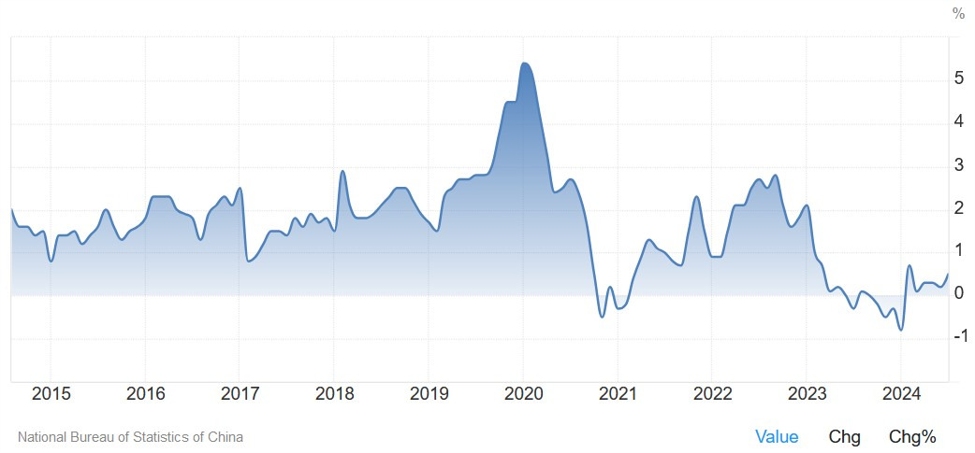

The Chinese CPI

Y/Y is expected at 0.7% vs. 0.5% prior, while the M/M measure is seen at 0.5%

vs. 0.5% prior. Real rates in China continue to be too high when there’s a

strong need for very low and even negative rates in such economic

circumstances. Chinese officials keep pledging more support but overall they’ve

been pretty slow in doing so.

China CPI YoY

Tuesday

The UK Labour

Market report is expected to show 114K jobs added in the three months to July

vs. 97K in June, and the Unemployment Rate to tick lower to 4.1% vs. 4.2% prior.

The Average Earnings including Bonus is expected at 4.1% vs. 4.5% prior, while

the Average Earnings excluding Bonus is seen at 5.1% vs. 5.4% prior. The market

sees an 83% probability of no change at the upcoming BoE meeting, and a total

of 43 bps of easing by year-end.

UK Unemployment Rate

The US NFIB Small

Business Optimism Index is expected at 93.6 vs. 93.7 prior. It’s a pretty empty

week on the data front and the market is very focused on growth, so this

release might be market moving. As a reminder, the NFIB index recently broke out from the range it’s been stuck since 2022 and jumped to a new cycle high at 93.6.

US NFIB Small Business Optimism Index

Wednesday

The US CPI Y/Y is

expected at 2.6% vs. 2.9% prior, while the M/M measure is seen at 0.2% vs. 0.2%

prior. The Core CPI Y/Y is expected at 3.2% vs. 3.2% prior, while the M/M

figure is seen at 0.2% vs. 0.2% prior.

The Fed is now

focused on the labour market, and they’ve even stated that upside surprises in

inflation won’t change their overall outlook. Therefore, inflation reports have

less significance at the moment although I’d say that a soft report will likely

push the expectations for a 50 bps cut back around 50% as the it would give the

Fed a stronger excuse to deliver a 50 bps insurance cut.

US Core CPI YoY

Thursday

The ECB is

expected to cut by 25 bps and bring the policy rate to 3.50%. This rate cut has

been strongly telegraphed since July. The market expects the central bank to

cut by 25 bps at each subsequent meeting until June 2025. Although President

Lagarde might not explicitly pre-commit to a back-to-back cut in October, it’s

likely that she will keep such an option on the table “depending on the data”.

ECB

The US Jobless

Claims continues to be one of the most important releases to follow every week

as it’s a timelier indicator on the state of the labour market.

Initial Claims

remain inside the 200K-260K range created since 2022, while Continuing Claims

have been on a sustained rise (although they’ve improved recently) showing that

layoffs are not accelerating and remain at low levels while hiring is more

subdued.

This week Initial

Claims are expected at 230K vs. 227K prior, while Continuing Claims are seen at

1850K vs. 1838K prior.

US Jobless Claims

Friday

The University of

Michigan Consumer Sentiment is expected at 68.0 vs. 67.9 prior. This indicator becomes

more important at turning points in the business cycle, so it will be something

the market will keep an eye on given the current focus on growth.

University of Michigan Consumer Sentiment