jonya

My previous and first article on Agree Realty (NYSE:ADC) was issued this Summer with a title of “Agree Realty: Great Way To Diversify From Realty Income“. As the title implies, in my opinion, ADC offered a great alternative to Realty Income (O) or at least a decent optionality for investors to invest in defensive yield-generating asset in a sector, which is underpinned by stable and sound business dynamics.

In the article, I did not recommend to dump Realty Income and shift the proceeds to ADC. Instead, I made a case that slight difference in the multiples (ADC being more expensive) is fully justified as the ADC had stronger underlying fundamentals than O. For example, it had (and still has) less leveraged balance sheet and higher quality mix of tenants, where more than half is explained by investment grade tenants.

Namely, I had both names recommended as clear buys for long-term investors, who value stable and predictable current income streams.

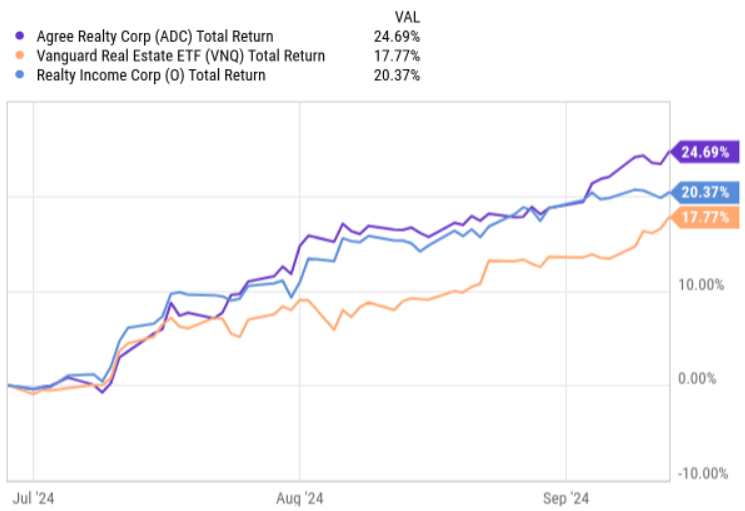

In the chart below, we can see how ADC has performed since the moment when I published the previous piece.

Ycharts

During this time, ADC has managed to register a total return performance of ~ 25%, slightly outperforming Realty Income and delivering alpha of ~ 7% relative to the broader real estate index.

As a result of this, the dividend yield has declined to 3.9% and the FWD P/FFO multiple has expanded to 18.7x. These metrics start to become relatively stretched and less favorable.

With this in mind, let’s dissect the recent earnings report to understand whether the investment case is still there.

Thesis review

If we look at one of the most important metrics measuring REIT cash generation results – the FFO or AFFO per share – we will notice a fairly positive picture. For the Q2, 2024 the core FFO per share landed at $1.03, which marks a healthy increase of 5.7% compared to the same period last year. The AFFO per share ticked higher by 6.4%, which is even greater result and not that common in retail-based segment. Typically, such growth rates could be observed within higher multiple segments such as data centers and industrials.

Now, if we peel back the onion a bit, we will notice several drivers behind the increased core FFO or AFFO generation, but the two most critical ones are related to the embedded rent escalators and, more importantly, the M&A effects, where ADC has been extremely active.

For example, in H1, 2024 period ADC has deployed ~ $345 million into new properties – some of this has already percolated through the books and started to contribute to the underlying cash generation. In Q2, 2024 specifically, the total invested capital through M&A amounted to $203 million at a weighted-average cap rate of 7.7% and a weighted-average lease term of over nine years. These are truly attractive cap rates, which as I will describe a bit later in the article are directly accretive to ADC’s business.

Since the M&A markets have started to exhibit some signs of recovery and considering the acquisition progress so far this year, the Management increased the acquisition guidance to ~ $700 million from $600 million. This means that we will see a continued spread capture by ADC in a fairly notable fashion that should help maintain the approximately 5% FFO per share growth alive. Apart from these transactions, we have to also factor in the internal or organic growth CapEx, which as of Q2 consisted of 25 projects (some were already finished in Q2), which have roughly $101 million of committed capital outstanding.

Speaking of the growth ambition and ADC’s ability to accommodate all of this, it is worth taking a look at the current capital structure. Yet, before we dissect the balance sheet, there are two important sources of capital that should allow the Management to fund the growth without assuming too much of an incremental financial risk:

- Conservative FFO payout ratio, which enables ~ 26% retention of quarterly FFO generation that could be directed towards new acquisitions.

- Consistent and targeted asset recycling program, where the Management divests non-core buildings usually at lower cap rates than what it can source from the M&A markets. For example, during Q2, the amount of proceeds stemming from the disposition activity landed at almost $37 million with a weighted average cap rate of 6.4%.

Looking at the balance sheet specifically, the key metric – net debt to recurring EBITDA – stood at 4.1x and excluding the effects from unsettled forward equity, the metrics is 4.9x. These levels are clearly indicative of robust financial profile, well within the range that is necessary to safely maintain the investment grade rating. Moreover, the underlying structure of this leverage is very sound with the weighted-average debt maturity of almost 7 years.

Finally, turning to the cost of capital front, there are again two vital aspects I would like to underscore.

The first one relates to the cost of debt component. Here, the recent public bond issuance of $450 million by ADC resulted in a 5.625% yield with a maturity date in 2034. This is very solid level and supportive for accretive spread capture given the aforementioned cap rate dynamics.

The second one related to the cost of equity. As the P/FFO multiple has increased, funding new acquisitions through fresh equity issuances becomes increasingly relevant. This means that ADC can access equity financing at levels, which in combination with ~ 5.5% debt component would render ~ 7.5 – 8% cap rate transaction inherently accretive to the existing shareholders. On top of this positive mathematical difference, by acquiring more properties, ADC could enjoy the additional benefits that stem from being a larger enterprise (e.g., reduced cost of capital, diversification). Plus, the embedded rent escalators could introduce an additional positive in this equation.

In fact, during Q2, we could already notice some maneuvers by the Management of trying to capitalize on this clear opportunity. Namely, in Q2, 3.2 million shares of forward equity were sold, receiving in return circa $195 million of fresh liquidity.

The bottom line

As one might imply from the analysis outlined above, ADC, in my opinion, remains a fundamentally sound and attractive business. The only thing that could argue against investing in ADC now is the current P/FFO multiple, which has increased by 20 – 25% compared to the moment when I issued my initial bull case back in June 2024. As a result of the multiple expansion, the dividend yield has decreased to below 4%, which is another negative for investors, who invest for stable and attractive current income streams. While the former component is obviously there, the latter has become less pronounced.

Having said that, the increase in multiple has also its benefit on ADC’s prospects to grow the business and thus justify the valuation. Since the cost of equity is lower, it now makes increasingly sense for the REIT to tap into the secondary equity issuances to use that capital in conjunction with relatively cheap debt with an aim to expand the portfolio and capture enticing spreads.

All in all, I would say that the investment case has weakened but not to a level, where a rating downgrade to hold could be justified.