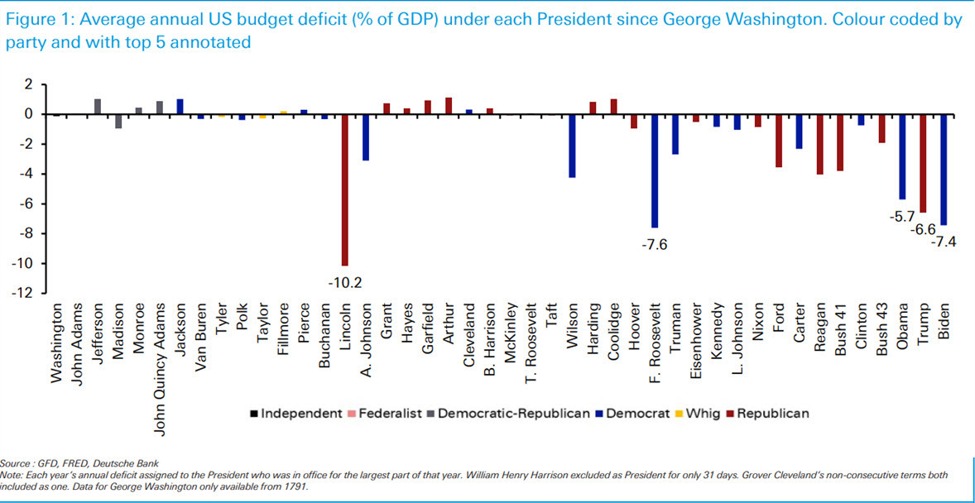

Deutche Bank is out with a critical reminder today that the US government is spending far more than it takes in annually.

In 2023:

- Total Outlays (Spending): $6.13 trillion

- Total Receipts (Revenue): $4.44 trillion

- Deficit: $1.69 trillion

To get that back into balance, you need to either 1) raise taxes very much or 2) cut spending drastically. Given that about $900 billion is now interest on debt, the options are perilously limited.

What’s very likely to happen is that this problem is going to be kicked down the road another 4 years. Fourteen years ago, Republican Tea Party members started to take power in the House based almost solely on the idea that deficits need to be cut. Those politicians have only gained power since and yet here we are.

Coming out of the election, there is a very likely scenario where old Tea Party politicians hold the balance of power (I’d argue it’s a near-certainty). The question is: Will they do anything about deficits?

Hedge fund legend Paul Tudor-Jones on CNBC this week said that Trump’s original tax cuts have to expire but I just can’t see that happening. My strong suspicion is that the recent trend in deficits extends beyond the next administration and that’s good news for Obama, who will be pushed out of the top-5.

What does it mean for equity markets, Deutsche Bank lays it out:

“You could argue that it’s taken progressively larger deficits over the last 90

years to keep strong stable equity returns and EPS growth, not to mention

maintaining economic growth”

I would certainly make that argument, particularly lately. And I think forward equity returns very much depend on where this is headed next.

Today’s market darling is Tesla, which had surprisingly large earnings $2.5 billion but $739 million of that was regulatory credits, also known as government subsidies. What does the stock price look like when you take away the source of 30% of its earnings?

That’s a direct example but so much of the velocity of money in the economy is held up by Americans and American companies receiving more from the government than they pay.

So what happens with the election? I think the most-hawkish scenario is one where Harris is President but Republicans win the House and Senate. That’s very unlikely but even holding the Senate might be enough to make some Republican fiscal hawks dig in.

Those would be the most-negative scenarios for equities. Another interesting one is if Trump wins the Presidency and Republicans win the Senate but Democrats control the House. That’s a realistic outcome and I wonder if it doesn’t result in Democrats suddenly putting on the fiscal hawk mask, particularly with the aforementioned Trump tax cuts expiring at the end of 2025.