Robert Manner/iStock Editorial through Getty Pictures

Abstract

Readers might discover my earlier protection through this link. My earlier score (printed in mid-October 2023) was a purchase, as I believed Fox Company (NASDAQ:FOXA) had potential for continued progress, pushed by its digital technique and content material management. Moreover, relative valuation towards friends recommended that FOXA was low cost. I’m reiterating my purchase score as FOXA’s digital technique is progressing rather well, with vital seen room forward to proceed rising. Whereas there are seen headwinds, I consider these headwinds are usually not structural and won’t be current in FY25.

Financials / Valuation

FOXA reported an alright 1Q24 with consolidated income totaling $3.21 billion (flat y/y), pushed by Affiliate income of $1.74 billion and Promoting income of $1.2 billion. Consolidated adjusted EBITDA got here in at $869 million. By phase, Tv income got here in at $1.78 billion, pushed by Promoting revenues of $910 million, pushed by sturdy Tubi efficiency (extra under). Tv additionally reported an EBITDA of $351. For Cable Networks, income got here in at $1.37 billion and EBITDA at $607 million.

How the 1Q24 outcomes match into FOXA efficiency during the last yr: whole income grew 0.5% over 1Q23 and 6% sequentially. On EBITDA efficiency, the $869 million in EBITDA carried out poorly vs. final yr, down 20.4% however improved sequentially from 4Q23.

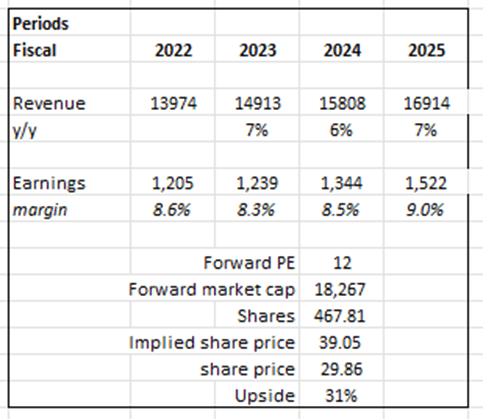

Based mostly on creator’s personal math

Based mostly on my view of the enterprise, FOXA ought to enhancements within the subsequent few quarter’s progress to fulfill my FY24 expectations. Nevertheless, the cadence of progress is hard to estimate given the combined of tail and headwinds between Tubi and y/y comps impact.

Nonetheless, I consider the present share worth stays engaging. Given the seen headwinds forward, I’m revising my FY24 progress outlook downwards modestly, however anticipate progress to get well in FY25 because the headwinds (as talked about under) are all a matter of timing. FY25 will likely be a yr when progress will face a normalized comp in FY24. However, I’ve revised my margin expectations upwards to 9% in FY25 as I acquire extra confidence that FOXA’s digital technique (Tubi) is progressing very nicely, with vital room to additional penetrate. For the reason that underlying infrastructure ({dollars} spent on sustaining Tubi) is basically mounted, further promoting income ought to see a excessive incremental margin, thus driving margins upward.

My relative valuation technique stays the identical, which is to match towards Paramount World (PARA). I proceed to consider that FOXA deserves to commerce at an identical ahead earnings a number of to PARA, which can also be FOXA historic 10-year common, as I anticipate FOXA to develop sooner than PARA (consensus expects PARA to develop 4% over the subsequent 12 months) and that FOXA has a better margin than PARA.

The important thing metrics I’ll observe are Tubi’s progress (income progress vs whole view time, and variety of customers) and consolidated promoting progress tempo.

Feedback

The 1Q24 outcomes proved that FOXA is discovering success in its digital technique. The important thing spotlight was sturdy progress in Tubi. After reaching 64 million customers in February, Tubi noticed a surge of 10 million customers since then, and in September surpassed 74 million month-to-month lively customers [MAUs]. At first look, it seems like a nasty factor that the overall view time progress fee of 65% remains to be outpacing the income progress fee of 30% for Tubi. For my part, this reveals that FOXA has a big alternative to enhance its advert income in the long term. As I stated in my earlier put up, there’s nonetheless a whole lot of room for enchancment in relation to promoting monetization as a result of the service is not utilizing all of its advert stock (as evident by the unfold between income progress and whole view time). Yet one more factor to remember is that each metrics present that Tubi remains to be rising at a really quick clip, albeit income was up 47% and TVT up 65% from the earlier quarter.

Apart from Tubi momentum, FOXA’s consolidated promoting income continues to carry out very strongly. FOXA reported consolidated promoting income of $1.2 billion ($910 million from Tv and $290 million from Cable Networks), regardless of the robust competitors confronted from final yr’s political promoting tailwinds. The important thing level from administration’s remarks is that promoting revenues are working barely forward of final yr, excluding the political impression of final yr. Driving this progress are monetary companies, cars, and retail sectors, whereas being offset by the betting, wagering, and leisure sector. The best way I see it, if we take a look at the weather driving promoting income, the important thing drivers are all main components of the economic system, and the truth that promoting income can develop signifies that underlying enterprise well being stays wholesome.

That stated, I’m additionally cognizant of the bearish narrative that promoting income may see deceleration within the near-term (2Q24). The narrative is that FOX community and stations are going to face robust comps as a result of political cycle, the Males’s World Cup in 2Q23, and softness in direct response pricing. Additionally, this yr’s World Sequence was brief and attracted a smaller nationwide viewers, which ought to have a adverse impression on promoting revenues. For my part, these are usually not structural weak point as they’re a matter of timing. As soon as we get into FY25, all these headwinds is not going to be current anymore. Particularly with the softness in direct response pricing, it should lap subsequent month, so the impression will not be going to be enormous for 2H24. As such, I believe buyers ought to use this to measurement/time their buy, however shouldn’t impression the long-term outlook of the enterprise.

Threat & conclusion

The upcoming headwinds could be worse than I anticipated, particularly if FOXA sees worse-than-expected twine reducing. Additionally, the retail spending setting is consistently on the mercy of the fed additional growing charges. Given the discretionary nature of FOXA’s merchandise, a recession will likely be unhealthy for FOXA. To finish off, I’m reiterating my purchase score for FOXA as a result of progress of its digital technique, notably with Tubi’s substantial person progress. I’ve adjusted my FY24 progress expectations barely downward as a result of foreseeable headwinds, however nonetheless anticipate a rebound in FY25. I additionally adjusted my margin assumption upwards to mirror the energy and progress of FOXA’s digital technique.