MEDITERRANEAN/E+ through Getty Pictures

A Powerful Business

In his e-book Zero To One, Peter Thiel outlines two totally different ways in which industries can develop–monopolies and, effectively, non-monopolies. Non-monopolistic industries are full of merchandise which might be undifferentiated and extensively used (suppose: screws, bolts, and so on). Monopolistic corporations have extremely differentiated merchandise which might be very troublesome to interchange. Income for non-monopolistic corporations are sometimes competed away: should you begin being profitable promoting bolts, another person will ultimately are available and begin promoting bolts for much less, inflicting every of you to compete away your income.

The meals trade is decidedly a non-monopolistic enterprise. It’s an exceedingly troublesome house to reach, which makes the meteoric rise of Mama’s Creations (NASDAQ:MAMA) all of the extra fascinating.

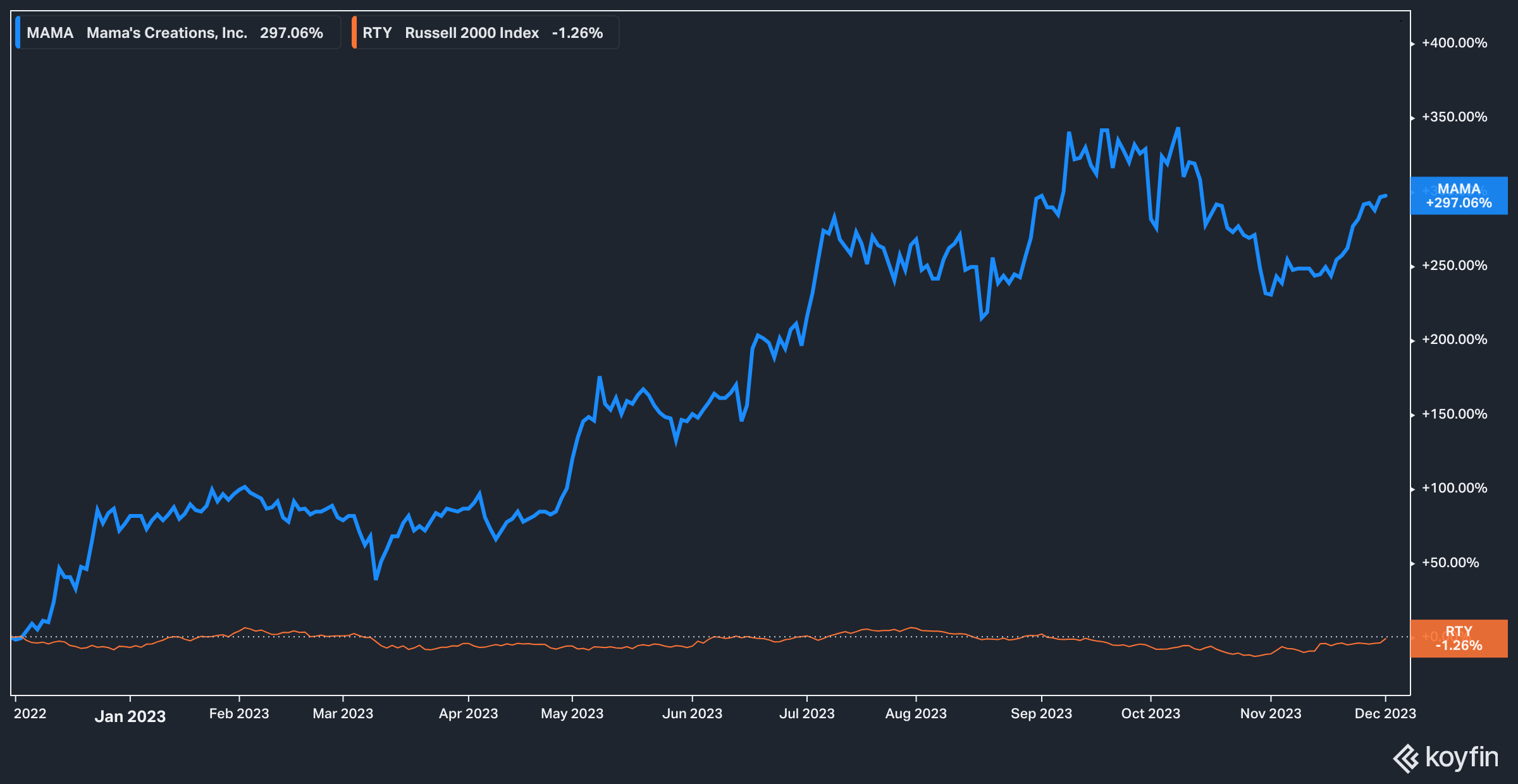

MAMA vs. RTY (Koyfin)

Within the final 12 months, Mama’s has surged virtually 300% whereas the Russell 2000 (RTY) has misplaced 1% in the identical interval.

This surge has come on the again of a monster 12 months for the corporate. In FY2022 (ending January thirty first, 2022), the corporate posted $47 million in gross sales. In FY2023, the corporate booked $93 million in income. The large query on investor’s minds, then, is whether or not or not the expansion can proceed.

Let’s dive in!

The Product

Mama’s Creations is the mum or dad firm of Mama Mancini’s, which is the most important model beneath which the corporate’s merchandise are bought.

MamaMancinis.com

Mama Mancini’s focuses on meatballs, deli merchandise, sausage, and different related objects.

There is a line from the Showtime present Billions the place Bobby Axelrod–the arch-villain hedge fund manager–advises a younger analyst engaged on a meals firm to “when you can, always put a company in your mouth.” In different phrases, attempt the product.

These unfamiliar (or unable) to attempt to product on account of availability might be forgiven if their default place is skepticism–after all, how good can these meatballs be?

Nicely, in accordance with buyer evaluations, fairly good. The corporate has an increasing partnership with Costco (COST), which is in and of itself an indication of top of the range (Costco is well-known for its rigorous product screening).

The partnership with Costco is increasing as effectively. CEO Adam Michael’s had this to say in regards to the relationship on the latest earnings call:

Most lately, we expanded our partnership with Costco, penetrating the Los Angeles area, marking the fourth out of 8 areas nationally. This progress contains our first-ever non-meatball product, a 3-pound sausage and pepper sleeve set for December rotation alongside MamaMancini’s beef meatballs. 2023 has seen us develop our relationship with Costco each by way of order quantity, which already has made 2023 a report 12 months with this buyer by way of order sizing, having lately obtained a report $1 million-plus order. This secures our triple play with Costco, having the most important orders in our historical past, with probably the most variety of areas within the 12 months and now having a number of objects in a 12 months. We look ahead to working intently with Costco to discover different thrilling merchandise for his or her extremely engaged buyer base.

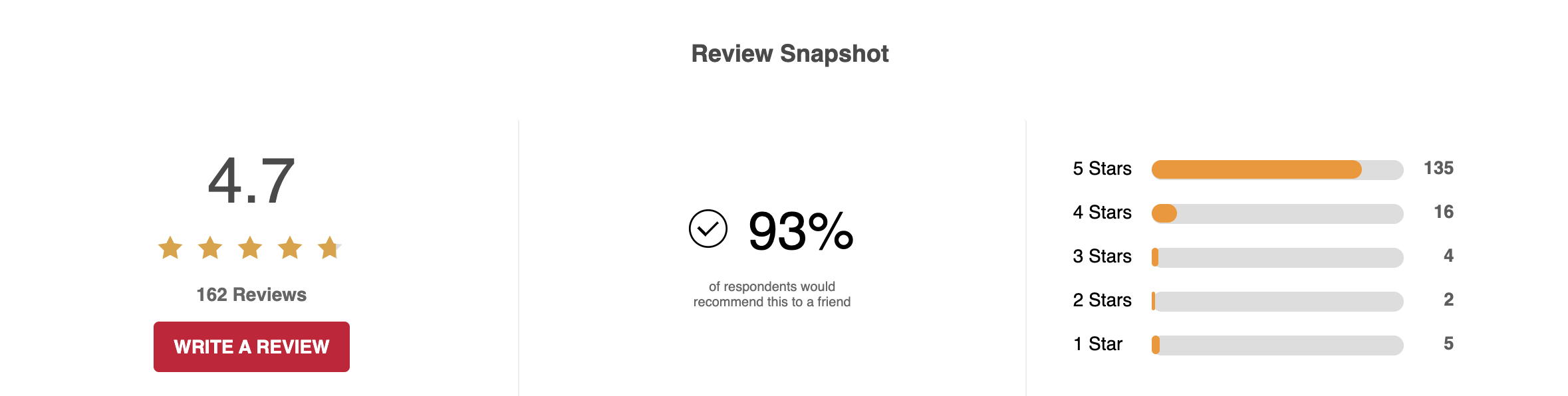

Evaluations from different retailers are stellar. 93% of BJ’s Wholesale (BJ) clients who’ve tried the product say they would recommend it to a friend.

Buyer Evaluations Overview (BJ’s Wholesale)

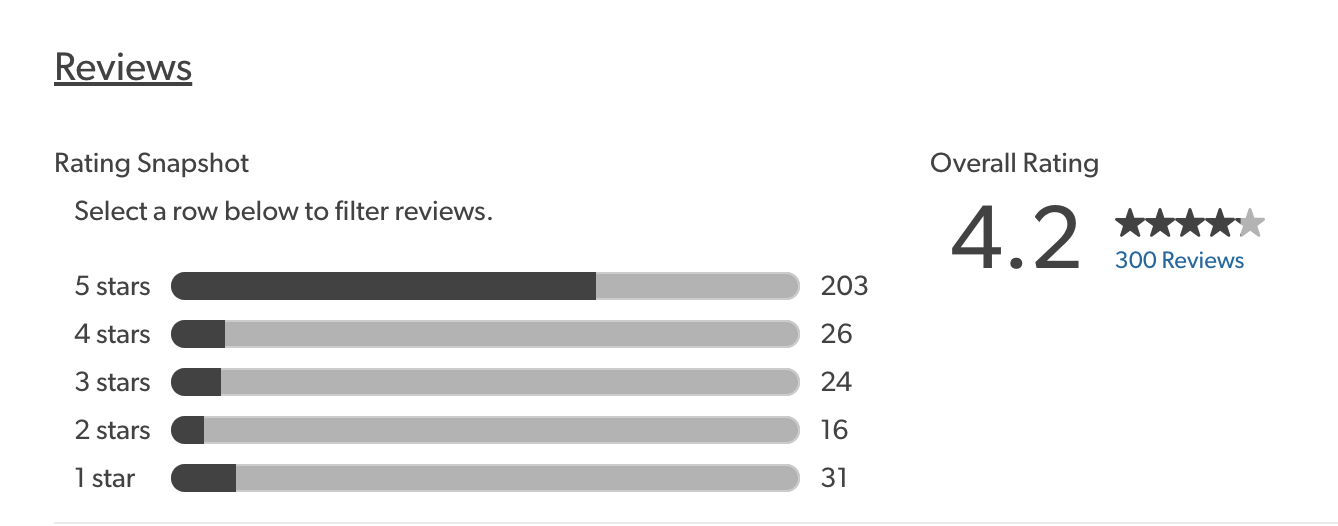

The corporate has the same review profile at Sam’s Club:

Buyer Evaluations Overview (Sam’s Membership)

Valuation & Development

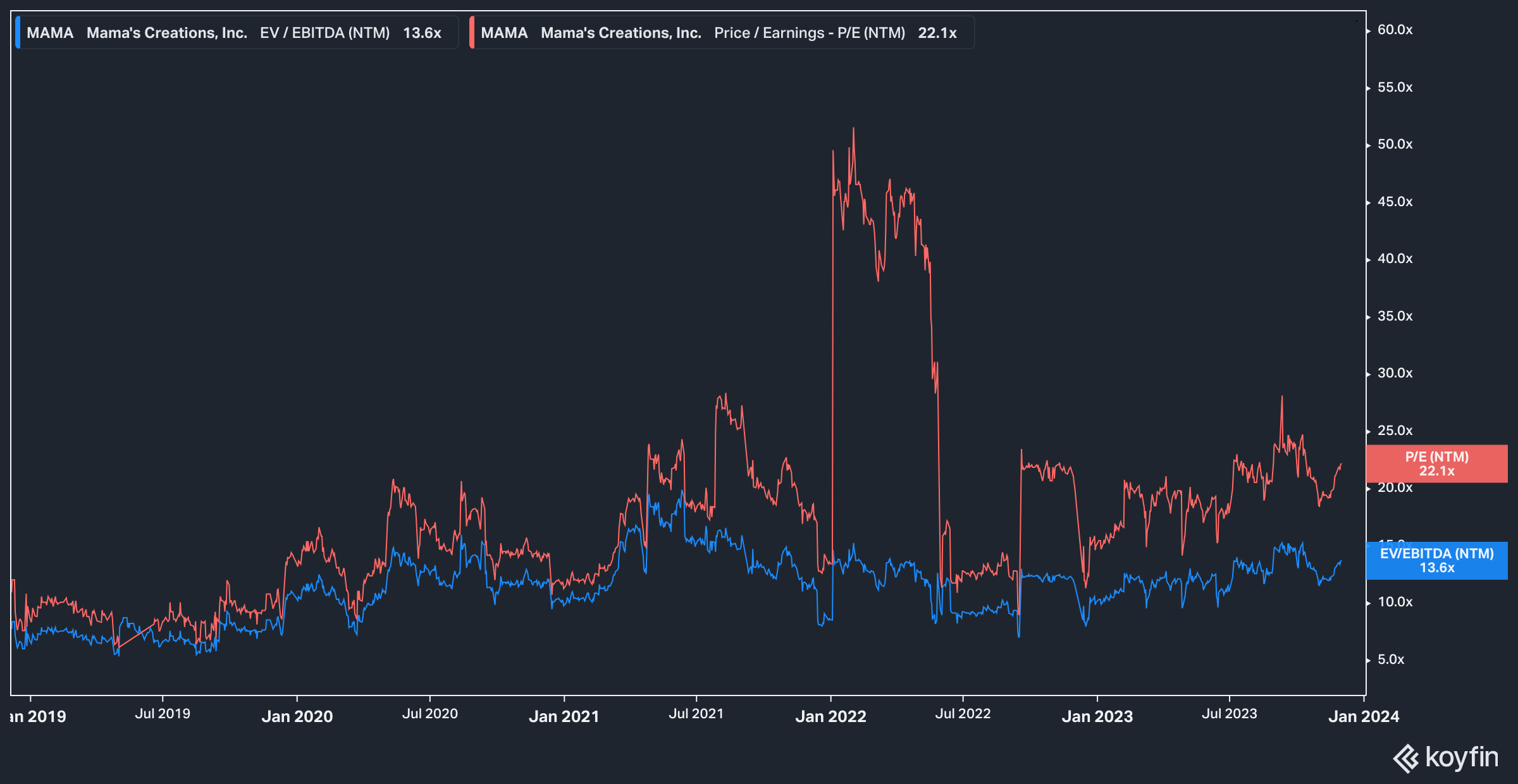

Mama’s Creations, then, is a really fascinating non-tech progress story. The corporate is worthwhile, and scaling quick. With its meteoric 12 months, it is not shocking then that valuations have turn into a bit stretched.

Koyfin

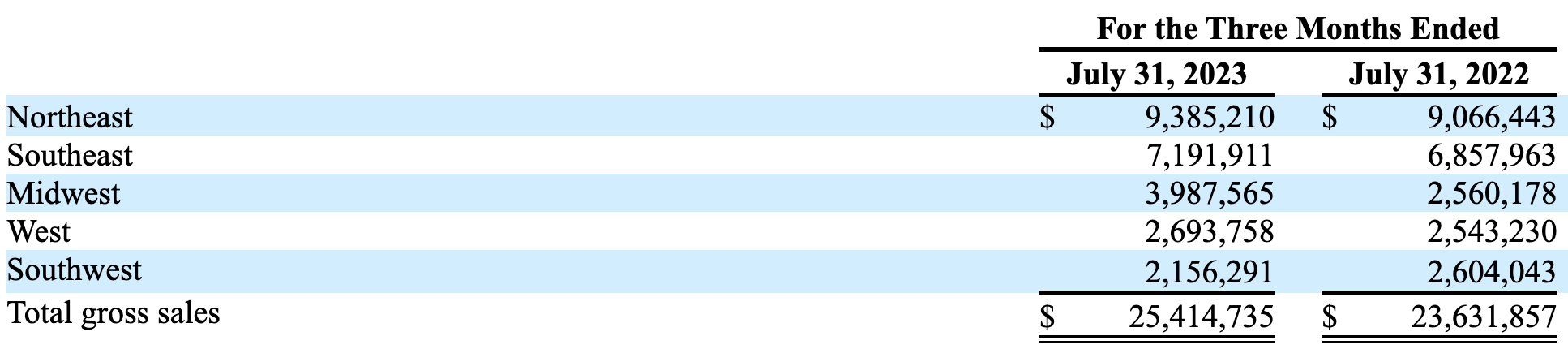

At present the inventory trades at 22x ahead earnings estimates and 13.6x occasions EV/EBITDA–so, not precisely low-cost. Nonetheless, the corporate has appreciable room for progress. Check out the corporate’s gross sales by geographic area from its latest quarterly filing:

MAMA SEC Filings

As an East Coast-based firm, it is not shocking to see that the Northeast and Southeast would boast the corporate’s largest gross sales. The remarks from Adam Michael, nevertheless, recommend that the corporate is aggressively working to develop its footprint and generate related gross sales profiles within the West, Southwest, and Midwest. On that entrance, the Midwest appears to be catching on to Mama Mancini’s–sales within the area grew by 56% 12 months over 12 months.

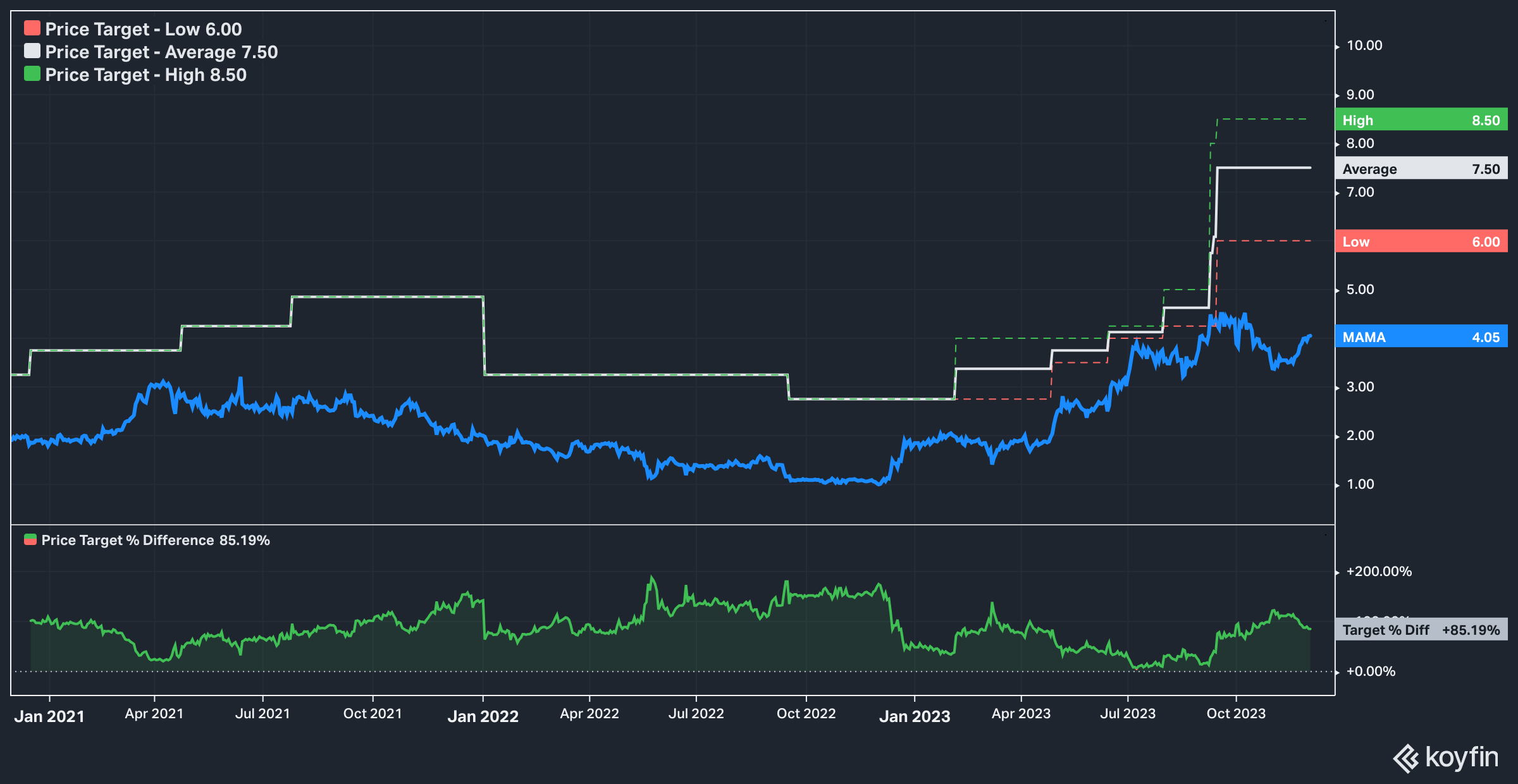

Wall Road analysts appear to agree that the runway for Mama’s Creations’ progress is sort of massive. Of the three analysts who cowl the inventory two price it a purchase, and one a powerful purchase.

Analyst Goal Worth (Koyfin)

The analysts have additionally lately raised their goal value. At present, the inventory trades 85% beneath the analyst consensus goal of $7.50 per share.

What Are The Dangers?

On the finish of the day, Mama’s is a micro-cap firm, and investing in corporations like this carries explicit dangers. Previously the corporate has issued most well-liked inventory with odd dividend payouts. In July 2023, the corporate transformed all excellent Sequence B most well-liked shares into frequent inventory, which is nice information for traders.

Mama’s additionally has buyer focus danger. Think about the next from the most recent quarterly submitting:

For the six months ended July 31, 2023, the Firm’s income was concentrated in three clients that accounted for about 22%, 13%, and 11% of gross income, respectively. For the six months ended July 31, 2022, the Firm’s income was concentrated in three clients that accounted for about 24%, 13%, and 12% respectively, of gross income.

Whereas we do not know the identification of those clients, we will assume primarily based on administration feedback that Costco is amongst them. Regardless of the identification, nevertheless, on the finish of the day 46% of whole gross sales might be attributed to solely three clients. Although this reliance has dropped 3% 12 months over 12 months, it’s not excellent.

The Backside Line

Mama’s Creations seems to be a uncommon bird–a non-tech progress (and worthwhile) progress story. Retaining in thoughts the dangers related to a micro-cap firm like this, we expect that the story for Mama’s is within the early innings and traders ought to pay shut consideration to this up-and-coming meatball maker.

Traders ought to maintain an eye fixed out — the corporate is about to report its Q3 earnings after the market shut on December thirteenth. High line expectations from Wall Road are $26.9 million and $2.22 million in working earnings. We predict the working earnings will likely be crucial quantity to look at, because the $2.22 million expectation is a 48% change from the prior 12 months and exhibits that the corporate is starting to attain working leverage.