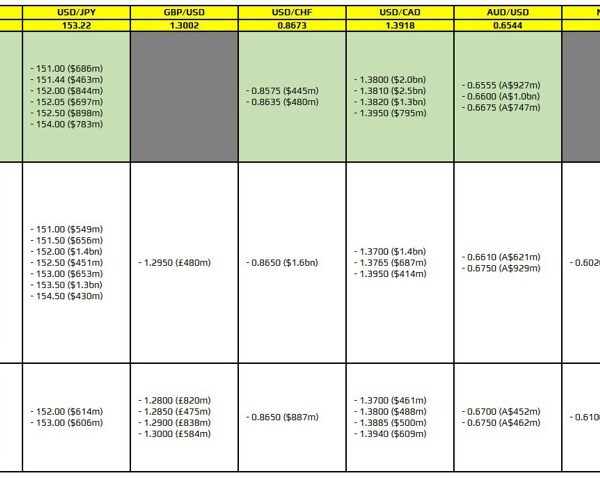

Today we might get another choppy day in the markets as the Thanksgiving holiday period tends to carry

through until the weekend even though the US markets are open today. The main highlight for today will be the Eurozone CPI data ahead of the ECB decision on the 12th of December. In the American session we have the Canadian GDP although it shouldn’t change much in terms of rate cuts expectations.

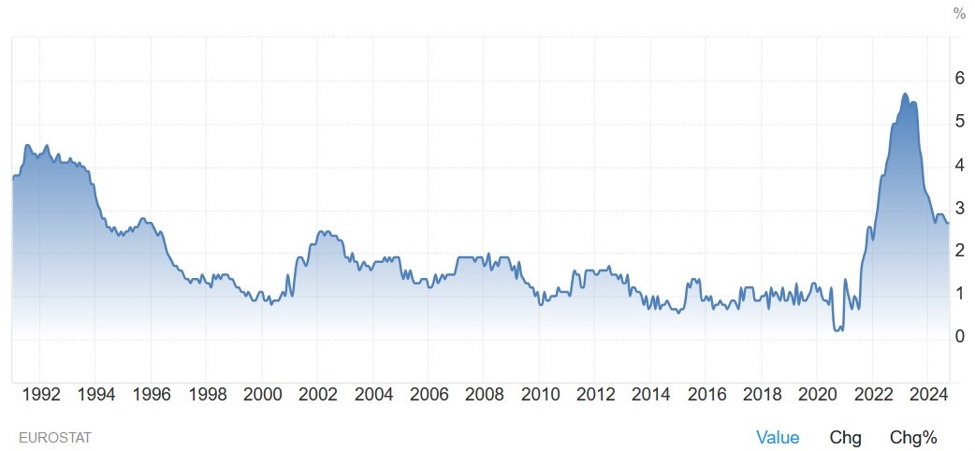

10:00 GMT – Eurozone November Flash CPI

The Eurozone CPI

Y/Y is expected at 2.4% vs. 2.0% prior, while the Core CPI Y/Y is seen at 2.9%

vs. 2.7% prior. The weak Eurozone PMIs last Friday led the market to raise the

chances of a 50 bps cut in December from 20% before the data to 60% after. That was an overreaction and this week the market pared back those bets with the 25 bps cut now being the favourite at roughly 80% probability.

A downside surprise in the Core CPI measures might get us to the ECB decision with basically a 50/50 chance, but the central bank will likely cut by 25 bps anyway. An upside surprise, on the other hand, should give the EUR a boost with the economy likely picking up next year and the aggressive rate cuts expectations being scaled back.

Eurozone Core CPI YoY