Justin Sullivan

Funding Thesis

KB House (NYSE:KBH) faces near-term headwinds from a high-interest fee atmosphere, however some main indicators, like improved new orders and stabilizing backlog, point out that we’re close to the underside of the cycle and gross sales ought to enhance in FY24. Additional, a possible reversal within the rate of interest cycle and the corporate’s concentrate on rising neighborhood depend ought to contribute to the corporate’s gross sales within the medium to long run. The long-term housing fundamentals are additionally engaging with a decade-plus underproduction of latest properties for the reason that nice housing recession of 2008 which is leading to restricted resale house stock.

The corporate’s margins are anticipated to learn from wholesome ranges of pricing in new orders, value reductions, and productiveness enhancements. The corporate’s Constructed-to-Order enterprise mannequin additionally normally carries increased margins.

Whereas I like the corporate’s outlook, I am unable to say the identical about valuation. The inventory is already buying and selling close to its one-year ahead FY24 finish ebook worth, which I imagine is suitable within the present high-interest fee atmosphere. So, whereas I like the corporate’s outlook, I would like to attend for a greater entry level earlier than turning into extra constructive on the inventory. For now, I’ve a impartial ranking on KBH inventory.

Income Evaluation and Outlook

After experiencing sturdy development in FY21 and FY22, the corporate’s income development was negatively impacted in latest quarters attributable to excessive mortgage charges which led potential homebuyers to place their house purchases on maintain.

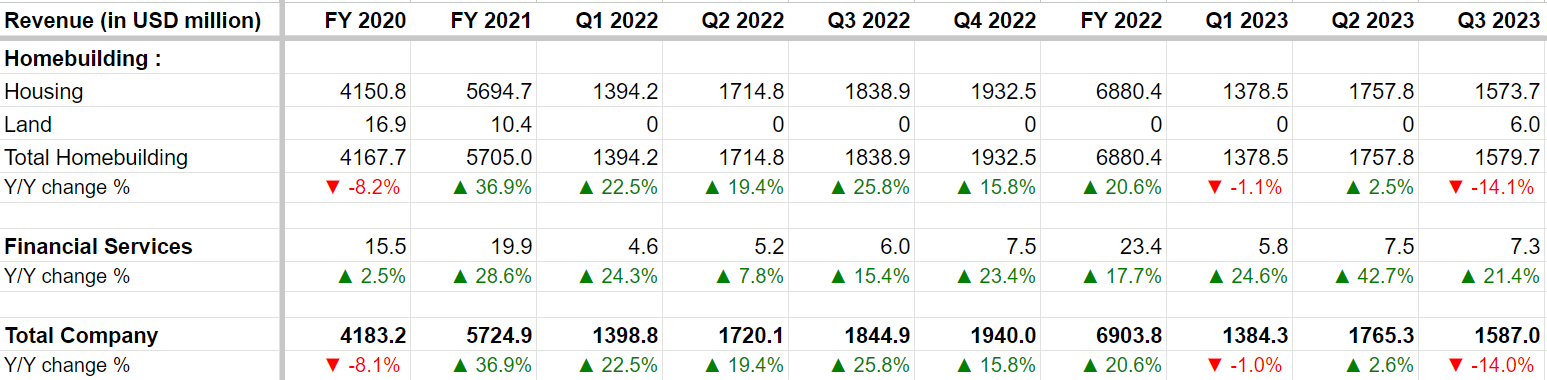

Within the third quarter of 2023, the corporate’s income declined 14% Y/Y to $1.587 billion, pushed by a 14.1% Y/Y decline within the core homebuilding revenues because the variety of properties the corporate delivered dropped by 6.6% Y/Y to 3375, with the typical promoting value falling 8.3% Y/Y to $466,300.

KBH’s Historic Income Development (Firm Knowledge, GS Analytics Analysis)

Trying ahead, whereas the fourth quarter and early 2024 revenues must be down Y/Y, there are indicators of potential stabilization in backlog and order fee which signifies a restoration within the second half of FY24.

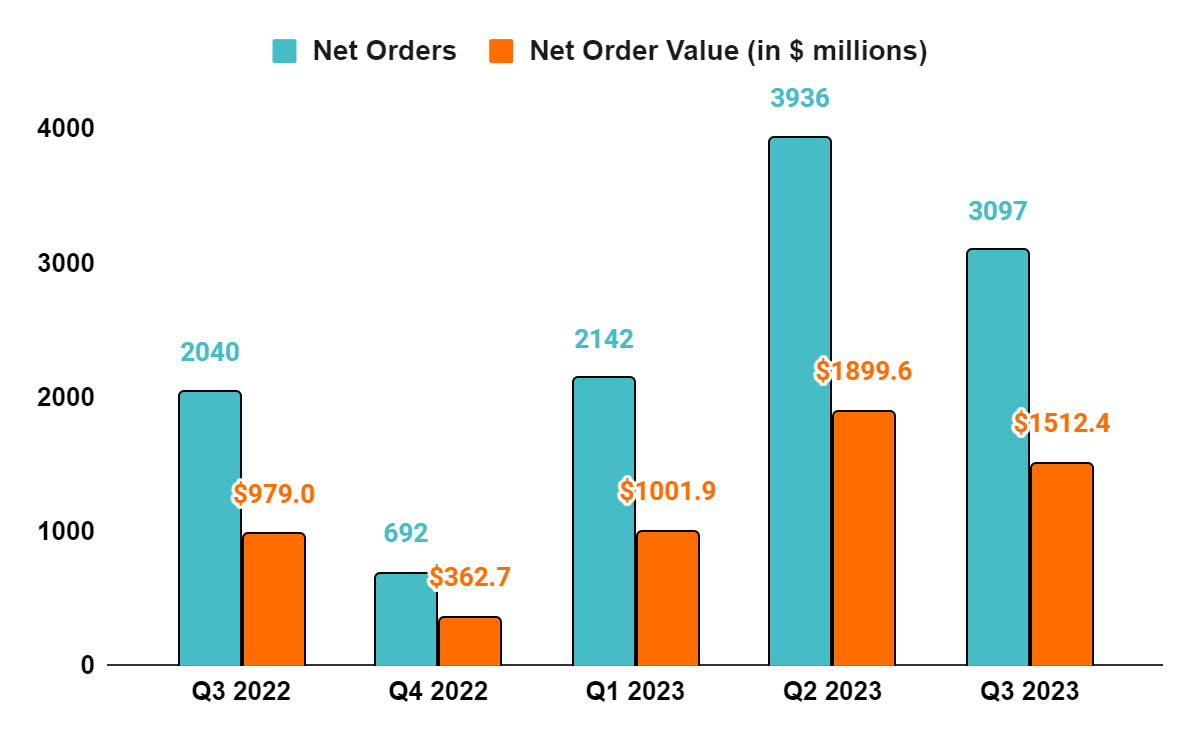

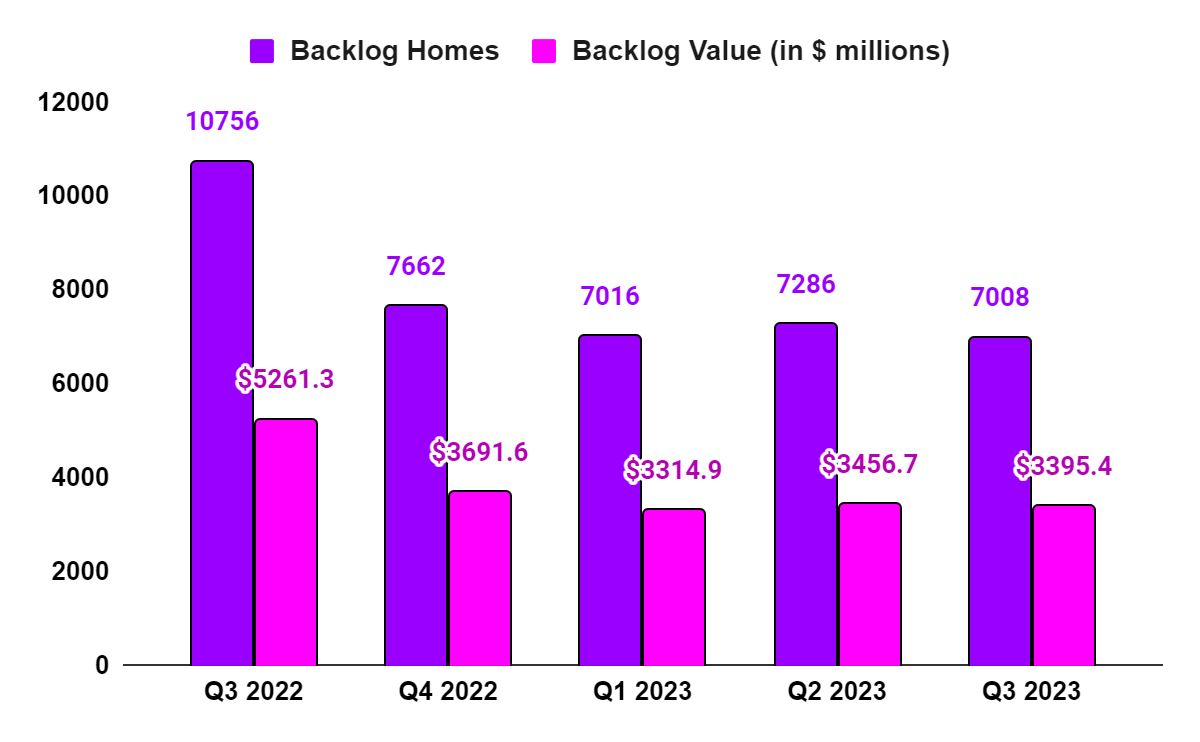

Regardless of excessive rates of interest, with 30-year mortgage charges over 7%, KBH reported regular buyer demand for brand new properties within the third quarter. The web orders grew 52% Y/Y to three,097 models within the third quarter, reflecting improved demand circumstances for brand new properties and a Y/Y decrease cancellation fee. The worth of web new orders was up 54% Y/Y to $1.51 billion and the corporate achieved an absorption (web orders per neighborhood per thirty days) of 4.3, which is above the corporate’s historic common third-quarter tempo earlier than pandemic-driven volatility. Whereas the backlog declined 34.8% Y/Y to 7,008 properties and its worth dropped by 35.5% Y/Y to $3.4 billion, the backlog worth has been stabilizing for the final 4 quarters. Since orders and backlog present good visibility on future revenues, I imagine income also needs to see some bottoming, particularly within the second half of FY24 (there’s a lag of a few quarters between the corporate receiving an order and it finishing gross sales by delivering the completed house to the homebuyer.)

KBH’s Internet Orders and Internet Order Worth (Firm Knowledge, GS Analytics Analysis)

KBH’s Backlog Properties and Backlog Worth (Firm Knowledge, GS Analytics Analysis)

Whereas some traders are frightened in regards to the firm’s build-to-order mannequin saying customization leads to increased house costs and will end in much less demand as consumers are at present specializing in affordability, this isn’t what is admittedly taking place when it comes to KBH gross sales as we will see from its sturdy web order development. KBH has elevated its concentrate on offering homebuyers with inexpensive housing choices and ~70% of its communities provide plans with sq. footage under 1,600 catering to the wants of budget-conscious homebuyers. So, I imagine the issues round order tendencies are usually not legitimate, and the corporate ought to proceed to see wholesome orders.

Additional, the corporate is planning to extend its neighborhood depend by ~15% by the top of FY24 from the present ranges. The corporate has invested a very good deal in land acquisitions in latest quarters and has over 57,000 tons owned or below contract that ought to help its plans of greater than 150 new neighborhood openings over the subsequent 5 quarters. The elevated neighborhood counts imply extra orders and may assist the corporate’s development in the long term.

Furthermore, the high-interest fee atmosphere that’s impacting the corporate’s gross sales is anticipated to reverse as there have been some constructive indicators, with inflation trending within the right route, which may result in the Federal Reserve slicing rates of interest within the coming yr. The analysts at Deutsche Financial institution just lately commented that they see a significant fee minimize beginning in June 2024. As soon as the Federal Reserve begins slicing charges, we should always see a very good restoration within the business. The undersupply of latest properties within the U.S., attributable to a significant underbuild since Nice Housing Recession, has resulted in a decent demand-supply atmosphere, which also needs to help restoration as soon as the rate of interest cycle reverses.

In abstract, whereas there are near-term headwinds, I imagine we’re near backside and might see income restoration ranging from 2HFY24.

Margin Evaluation and Outlook

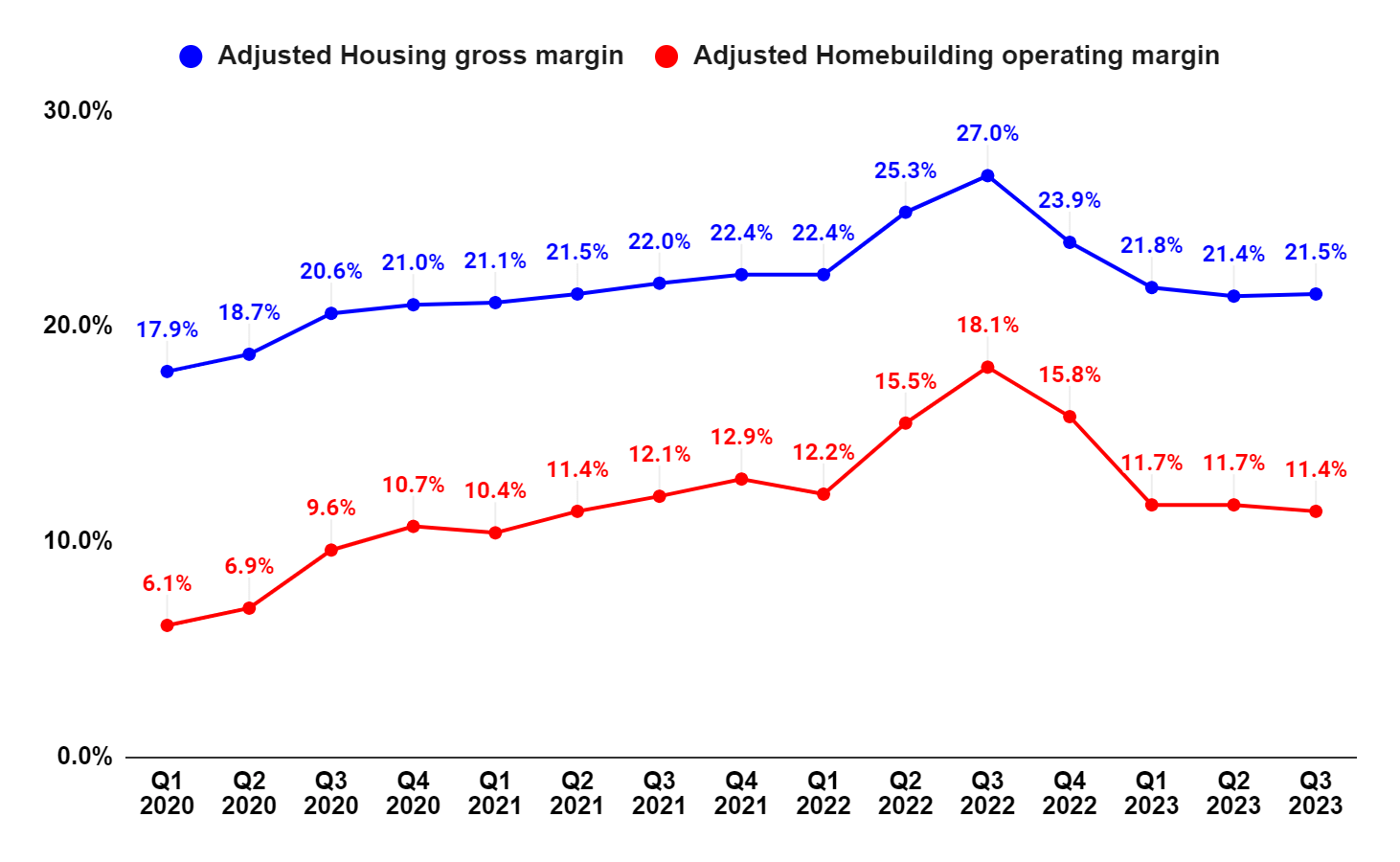

In Q3 2023, the corporate’s adjusted housing gross margin (which excludes inventory-related fees) contracted by 550 bps Y/Y to 21.5% attributable to decrease pricing and different homebuyer concessions for orders booked within the prior durations, elevated development prices, and a mixture shift away from the higher-priced West Coast area. SG&A as a share of housing revenues elevated 130 bps Y/Y attributable to diminished working leverage from decrease housing revenues and better gross sales commissions. Decrease adjusted housing gross margin and better SG&A expense as a share of housing revenues led to a 670 bps Y/Y decline in adjusted homebuilding working margin (excluding inventory-related fees) to 11.4%.

KBH’s Adjusted Housing Gross Margin and Adjusted Homebuilding Working Margin (Firm Knowledge, GS Analytics Analysis)

Trying ahead, I imagine the corporate’s margins are close to the underside of the present downcycle and may see some enchancment in FY24. In Q3, the wholesome demand pattern throughout the corporate’s finish markets enabled it to boost costs for brand new orders in ~65% of its communities, whereas lowering costs in solely ~10%. The power in pricing of the brand new orders that the corporate is reserving bodes effectively for the corporate’s margins within the coming durations.

Furthermore, the corporate is engaged on lowering homebuilding cycle time to its historic construct time of between 4 and 5 months. The corporate has executed effectively on this entrance thus far, with a 35-day sequential discount within the third quarter, and KB House is at present constructing properties in roughly six months. There must be an additional discount on this quantity, which ought to end in elevated productiveness for the corporate.

As well as, the corporate’s efforts on leveraging its extremely customer-centric Constructed-to-Order enterprise mannequin additionally bode effectively for the margins. In keeping with administration, Constructed-to-Order properties have a 300 bps increased margin than speculative properties (move-in prepared properties constructed earlier than a house purchaser makes a purchase order) as personalized properties permit the corporate to generate revenues from lot premiums in addition to a design studio and structural choices.

Total, the corporate’s margin also needs to backside round these ranges and may see some enchancment in the direction of the again half of FY24.

Valuation and Conclusion

The corporate ended the third quarter with a Ebook worth of $48.29 per share, and it’s at present buying and selling round $55.51 or ~1.15x final reported ebook worth. When it comes to ahead estimates, if we have a look at the present consensus EPS estimates, the corporate is anticipated to submit an EPS of $1.68 in This autumn 2023 and $7.31 in FY24. KBH has an annual dividend of $0.80 per share. So, the corporate’s ebook worth on a one-year ahead foundation or on the year-end FY24 must be near $56.48 (=$48.29+ $1.68+$7.31-$0.80). So, the inventory is buying and selling nearly close to its one-year ahead FY24 end-book worth.

Whereas I do not see a lot draw back from these ranges given the corporate’s revenues and margins are more likely to backside, I do not see a lot upside both given the inventory is already buying and selling close to its one-year ahead ebook worth. I’m not comfy assigning the inventory a premium valuation versus its one-year ahead ebook worth, given the place the rates of interest are. Therefore, I’ve a impartial ranking on the inventory for now.