gsheldon

Funding Thesis

Preview

We initially covered Hershey (NYSE:HSY) within the article ” Hershey: Chocolate’s ‘Lipstick Effect” Will not Absolutely Translate Into Earnings Energy” in February this year with a sell rating. The focus of our thesis was to point out that although chocolate was a commodity is recession-resilient with the so-called “lipstick impact”, Hershey still has more weakness in its earnings and cash conversion in the near term. The stock has been down by 21.12% within the past nine months since then.

Previous Rating Record (Seeking Alpha)

Should we buy this holiday delight now?

Updates

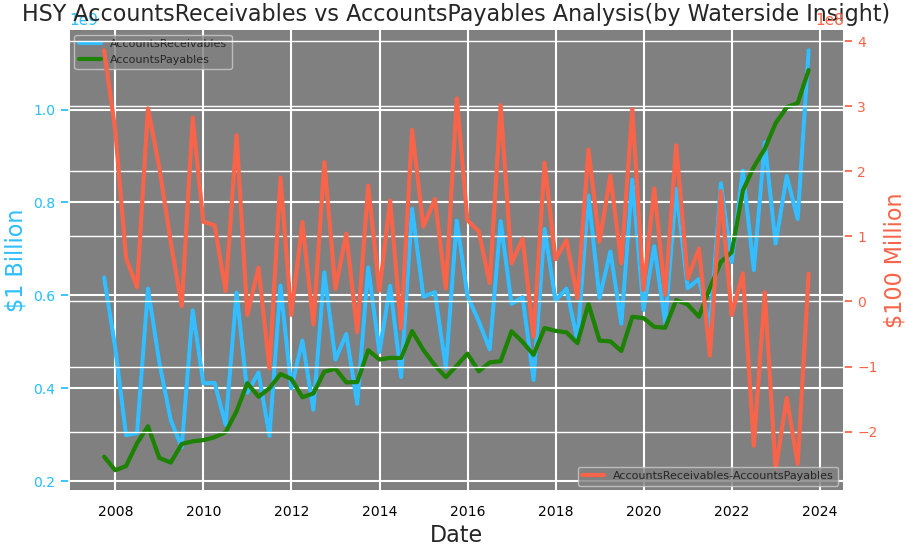

Since we last wrote about Hershey’s internet working capital dropped under to be deep within the pink, Hershey has pulled it again as much as break even stage. It means it has virtually the identical account receivables versus account payables, however largely attributable to a bounce within the receivables. Throughout its history as a public company since the 1980s, this high level of using credit to pay for vendors and suppliers is not a norm for the company. It has always not only had lower accounts payables than receivables, but it also maintained a relatively stable level of how many accounts payables it had. So the recent jump in the payables since 2022 is an outlier. The higher payables usage helped to shorten its cash conversion cycle that adversely impacted by its largest inventory level. It takes about 70 days to have one cycle of inventory turnover, which is more than 20 days longer than its five-year average pre-pandemic. We are not experts on how long the chocolate candies and snacks can keep fresh but would guess most would prefer a shorter period. In other words, it is using its credits with the suppliers to help keep its cash flow conversion within a normal range. This is risky as the suppliers could be facing difficulties themselves should any demand disruption occur.

Hershey: Accounts Receivables vs Accounts Payables (Calculated and Charted by Waterside Insight with data from the company)

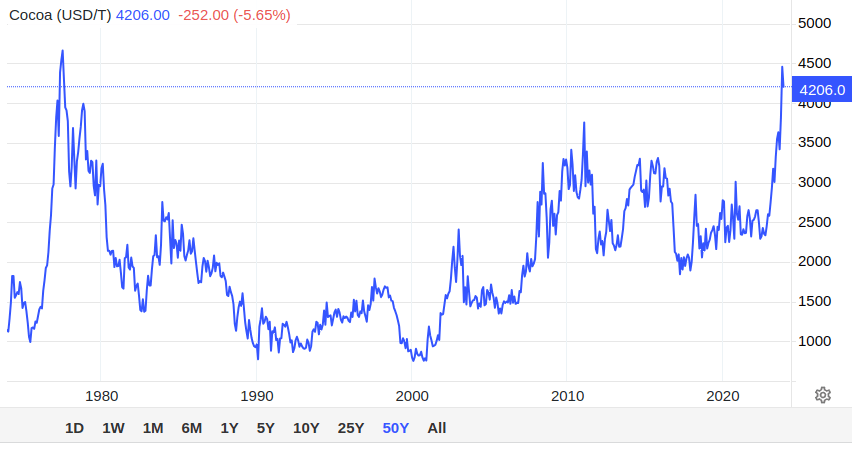

We posted the historical prices of the coca beans in the last article, and since then, there has been little relief. The prices have continued to climb to almost close to their all-time high recorded in 1977. By now, we can see Hershey is facing a squeeze from both the demand side and the supply side.

Cocoa Futures Price (Tradingeconomics)

Summarizing the latest developments, it has confirmed our previous thesis that

We think the recession-resilient power of sweet chocolates probably cannot fully translate into recession-resilient earnings power for Hersey.

On the other hand, should the supply side start to ease from such a high level, Hershey could find some relief. To wait for it, the company needs more cash on hand. Its current ratio has somehow recovered a bit from the low of .8x last year to 1.09x, but its cash-to-debt ratio is only about 9%. This ratio has been below 10% since last year while its average is about 15% in the five years before that. During the stressful period before and after ’08, this ratio dropped to as low as 3-5%, and we can see in absolute value its current cash and cash equivalents are much higher than then. So this put it in perspective that it still needs to strengthen its liquidity position in order to weather the squeeze.

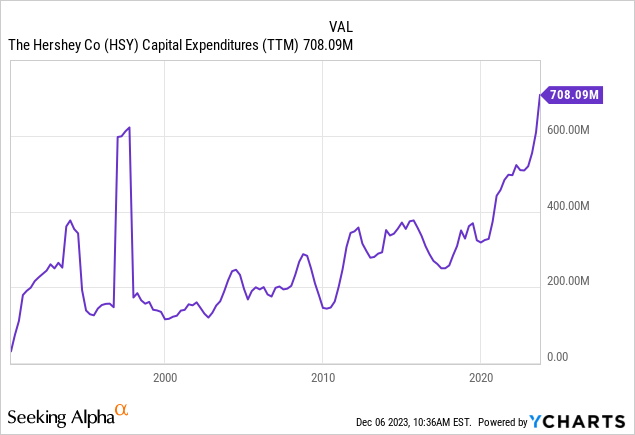

A stronger cash flow could help, but Hershey happened to have embarked on a large CapEx spending journey as of late. The largest capex spending came mostly in the past year or so, almost doubling since 2020. The company does not sectionize the CapEx, which is spent across all segments to support its global operations to maximize efficiency and productivity. Part of the CapEx spending was on the digital infrastructure such as Snack ERP system implementation, and capacity expansion across the enterprise. This spending may not be done yet, and we expect pressure from it on free cash flow to remain.

With the holiday season coming up, Hershey expected consumer spending on traditional holiday delights to be in line with the previous year. It is important since for certain segments, such as the North American Confectionery, holiday sales accounted for almost half of its full quarterly growth.

Monetary Overview & Valuation

Hershey: Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

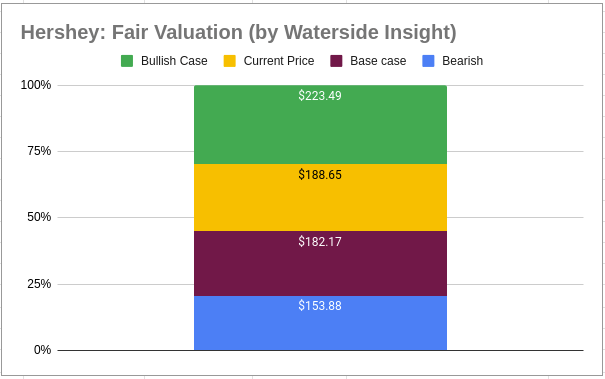

Our previous bearish estimate was $182.41, and Hershey’s current stock price has quickly approached that level. However, we have revised down the lower end of our estimate, mostly due to the cash conversion risks. The inventory has to come down much more than where it is to restore a historical norm to the situation. For the bullish and base case estimates, we slightly moved down both to reflect the expectation of a longer period to transition out of the current cycle than previously expected. This also indicates larger volatility could emerge for the stock going forward. The current stock price is just a tad higher than our base case estimate. The market has priced in the risks and brought down the stock to be fair valued but not yet cheap.

Hershey: Fair Valuation (Calculated and Charted by Waterside Insight with data from the company)

Conclusion

Hershey’s greater than 20% down since our last call to promote has confirmed the weak spot we noticed within the firm, together with in money conversion, provide facet squeeze, and upcoming softer demand. In reviewing the present state of affairs, we see the tight spot it’s going through provide and demand facet challenges to final for some extra time. It’s actively deploying capital to revamp its enterprise system for effectivity and productiveness upgrades. Until there’s a fast turnaround throughout this vacation season, the stress on free money move will persist for at the least the following few quarters. It’s now at our base case estimate. Despite the fact that it has been down by over 20% prior to now 9 months, we suggest a maintain as an alternative of purchase for now.