MsLightBox/E+ through Getty Photographs

Central Puerto (NYSE:CEPU) is without doubt one of the most vital Argentinian electrical energy mills, with 16% of the nation’s whole capability.

I wrote articles in regards to the firm in April 2021 and January 2023. CEPU was my second article on the platform. For the reason that first article, the inventory has returned 350%, fairly a experience.

On this replace article, I assessment the current operational efficiency, the acquisition of Central Costanera, the corporate’s monetary situation, and speculate about potential profitability throughout Milei’s authorities.

Sadly, it’s time for me to get off the CEPU practice. It has been a incredible experience, however the firm’s share value already reductions a fantastic future forward.

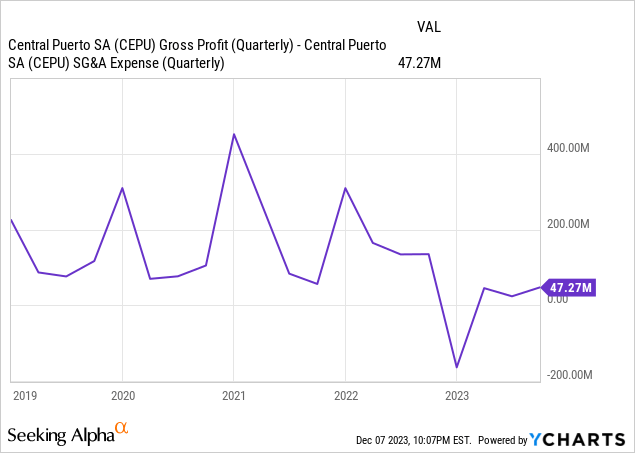

Tortoise and hare amongst CEPU’s generators

Below the present regulatory scheme, Argentina’s electrical energy technology business works just like the tortoise and the hare story. The federal government decides discretionarily when to replace the worth paid for electrical energy technology. Typically, the updates are above inflation, and generally not. With inflation working at greater than 150% yearly, a couple of delays could make the corporate’s earnings unstable.

Add to this that inflation performs its personal tortoise and hare sport with the peso trade price. This has made CEPU’s working earnings vary between $130 million and $400 million. Sadly, FY23 has been an election yr, and the salient authorities tried to maintain issues tight, which meant solely granting a 57% value enhance in November 2023, after an amassed 100% of inflation within the 9M23 interval.

You will have seen that I plotted gross revenue minus SG&A within the above chart, not working earnings. When studying Argentinian monetary statements, one should separate the results of inflation and depreciation on the earnings assertion. That is significantly so for CEPU, which has made the unusual determination to incorporate the FX impact of its dollar-denominated commerce receivables in working earnings as a substitute of placing it on the backside of the monetary earnings part.

What comes subsequent in vitality pricing

As talked about in a current article about Pampa, the brand new Argentinian authorities can determine on a distinct coverage on electrical energy pricing. Even when it determined to proceed with the present mounted value scheme, it ought to outline the profitability degree of the business, similar to the earlier authorities did (albeit haphazardly).

Two circumstances constrain the brand new authorities. First, any enhance in pricing and profitability will must be paid both by the folks or by the federal government (rising its deficit). The deficit is already important, and value will increase in electrical energy for shoppers are anticipated, so the federal government could determine to attend on value will increase for the mills, attempting to alleviate a few of the influence on shoppers and industries. Second, the federal government has already dedicated to buying pure gasoline as much as 2028, primarily for provision to electrical energy mills and gasoline distributors. Because of this an public sale system (extra regular in electrical energy markets) wouldn’t embody the worth of this important provide until the federal government determined to re-auction its gasoline contracts.

One factor, for my part, is fairly possible, although. The brand new authorities won’t put the mills right into a non-profitability scheme because it occurred earlier than 2015. I feel CEPU’s present profitability is a flooring, particularly contemplating that the corporate has a few of the most effective (and subsequently extra worthwhile in a contest scheme) mixed cycle generators out there.

This yr, CEPU generated $50 million from its renewable contracts (387 MW, dollar-denominated and fewer unstable) and solely $55 million from its typical property (greater than 10x extra at 4400MW). Annualized these segments would generate about $140 million in working earnings.

CEPU purchased property at knock-down costs

Originally of the yr, CEPU introduced that it had purchased the Central Costanera, a thermal generator, from the Italian electrical energy firm ENEL for $48 million. It was about to purchase participation in one other central from ENEL (Central Dock Sud), however the remaining shareholder, YPF (YPF), determined to make use of its refutal proper and buy ENEL’s participation.

Central Costanera added 2300 MW to CEPU (a 50% enhance in thermal capability) for simply $50 million. Central Costanera is the biggest thermal plant within the nation and was purchased by CEPU for (once more) $50 million. Certainly, 1100 of these MW belong to traditional cycle generators courting from the Sixties, and that, subsequently, aren’t employed by the market as a result of they don’t seem to be very environment friendly, though they might change into a closed cycle system. Nonetheless, the remaining 1200 MW are a part of two totally utilized mixed cycle generators. Though solely the 1200 MW mixed cycle generators have been purchased, $50 million may be very low cost.

CEPU generated a $55 million working revenue 9M22 from its typical manufacturing of 4400 MW at present costs. This suggests $16.5 thousand per MW per yr or $20 million for the 1200 MW mixed cycle at Central Costanera with out utilizing the opposite 1200 MW. That is an EV/EBIT shut beneath 3x with some spare property.

Monetary scenario

On the monetary facet, we have now to make extra changes, primarily due to the inflation impact on CEPU’s financial property (a non-cash expense). My method is to translate all money owed and curiosity to USD (straightforward within the case of CEPU, given that the majority debt is dollar-denominated) and ignore the impact of inflation on peso-denominated property (so long as we do not convert them to {dollars} in our calculations).

CEPU at present has $350 million in money owed and has introduced the cancelation of $50 million plus the issuance of one other $100 million, in phrases undisclosed. This may put the corporate at a $400 million debt degree by the tip of the yr. The corporate pays round 10% on that debt, and Pampa lately issued below related phrases for a similar maturities, so I feel 10% is an efficient method for the present debt construction. With that, we contemplate $40 million in annual curiosity bills.

On the asset facet, the corporate has $60 million in dollar-denominated money devices and $55 million in dollar-denominated bonds. That would go away a not-so-attractive $285 million in internet debt.

However, CEPU additionally has commerce receivables from the CVO thermal central which might be being serviced by the vitality authority for $300 million (dollar-denominated). These generate $50 million in yearly curiosity, which is being paid, greater than offsetting the curiosity expense. Lastly, AR$ 76 billion in authorities debt which is perhaps tied to inflation or depreciation ($76 million or $200 million relying on the speed used). With these monetary property, the corporate has a monetary surplus. I perceive that CEPU mustn’t run into issues to service its debt throughout its concentrated maturities in 2026 and 2030.

Conclusions

It’s tough to return to the drafting board to outline how a lot CEPU can extract from its 7 GW of energy-generating property. I consider that utilizing 2023 numbers is comparatively conservative, given the generalized value repression utilized by the salient authorities and the excessive inflation ranges.

From the technology property, including typical, the mixed cycle portion of Costanera, and renewables, we arrive at $160 million. Curiosity bills are offset by CVO receivable curiosity, and we aren’t including any curiosity from the $115 million and AR$ 76 billion in different monetary property.

Take away 35% earnings taxes, and we arrive at a $100 million internet earnings of what I contemplate a awful yr.

Lastly, we aren’t contemplating the 160 thousand hectares of forestry land that CEPU bought this yr, which generated between $2 and $5 million in working earnings plus some organic asset revaluation.

The issue is that CEPU trades at a $3 billion valuation already. The a number of is 30x utilizing the ground that I constructed. True, a couple of years in the past, CEPU was churning $400+ million in working earnings with the identical authorities however just a little higher monetary scenario, however that’s hypothesis. Plus, a couple of years in the past, CEPU was priced at solely $1 billion, not $3 billion.

I consider the scenario might be higher for the corporate right this moment, however the valuation hole is just too giant, and I choose to not speculate.