urbancow/E+ by way of Getty Pictures

We beforehand coated C3.ai (NYSE:NYSE:AI) in September 2023, discussing its blended prospects at a time of generative AI growth, with the administration electing to pivot to a decrease margin consumption-based pricing mannequin to seize market share and shopper base.

Mixed with its sustained money burn and deteriorating stability sheet, we had most popular to price the inventory as a Maintain then.

On this article, we can be highlighting C3.ai’s improved near-term prospects, attributed to the diminished gross sales friction with decrease common contract worth (lower cost factors) and shorter gross sales cycle.

Mixed with the rising ratio of subscription income and better projected conversion price, it seems that the administration’s new enterprise mannequin is working as meant.

Regardless of so, we preserve our Maintain score, since we imagine that there’s a minimal margin of security at these inflated ranges, with the inventory overly buoyed by the generative AI hype.

The Generative AI Funding Thesis Stays Overly Inflated Right here

For now, C3.ai has reported a backside line beat within the FQ2’24 earnings call, with revenues of $73.23M (+1.2% QoQ/ +17.3% YoY) and adj EPS of -$0.13 (+44.4% QoQ/ +18.1% YoY).

On the one hand, the transition to a consumption-based pricing mannequin has straight impacted its path in the direction of profitability, attributed to its declining adj gross margins of 69% (inline QoQ/ -8 factors YoY).

The identical has been noticed in C3.ai’s revised FY2024 steering, with revenues of $307.5M (+15.2% YoY) and adj loss from operations of -$125M on the midpoint (-83.6% YoY), as its losses speed up from the previous offered guidance of -$62.5M on the midpoint (+8.1% YoY).

Alternatively, the SaaS firm reviews rising subscription revenues of $66.4M (+8.1% QoQ/ +11.5% YoY) and 404 in buyer engagements (+81% YoY), additional underscoring its profitable buyer wins to this point because of the diminished gross sales friction.

The rising ratio of subscription revenues at 91% (+6 factors QoQ/ -4.3 YoY) is extremely encouraging as nicely, attributed to the improved predictability of its gross sales and expanded shopper base, more likely to additional contribute to its long-term prime/ backside line fly wheel.

Nonetheless, with nice demand, additionally comes nice competitors.

It stays to be seen how aggressive C3.ai’s choices can be in opposition to nicely funded Huge Tech corporations whom are providing related generative-AI primarily based analytic SaaS, reminiscent of Microsoft (MSFT) by means of OpenAI, Nvidia (NVDA), Palantir (PLTR), and Alphabet (GOOG).

Maybe this explains the brand new enterprise mannequin’s decrease common contract value of $0.8M (-20% QoQ/ -94.7% YoY) within the newest quarter. That is on prime of the shorter gross sales cycle of roughly 24 hours, with the applying anticipated to go reside inside 4 to eight weeks.

Based mostly on C3.ai’s accomplished contracts to this point, the administration has additionally confidently guided a relatively aggressive “pilot to production conversion rate of about 70%,” implying its rising alternative to monetize its AI choices at a a lot quicker price.

That is on prime of the deepened partnership with Amazon’s (AMZN) AWS, with the brand new C3 Generative AI utility permitting “users of all technical levels to begin using generative AI within minutes of signing up,” out there with a 14-day free trial.

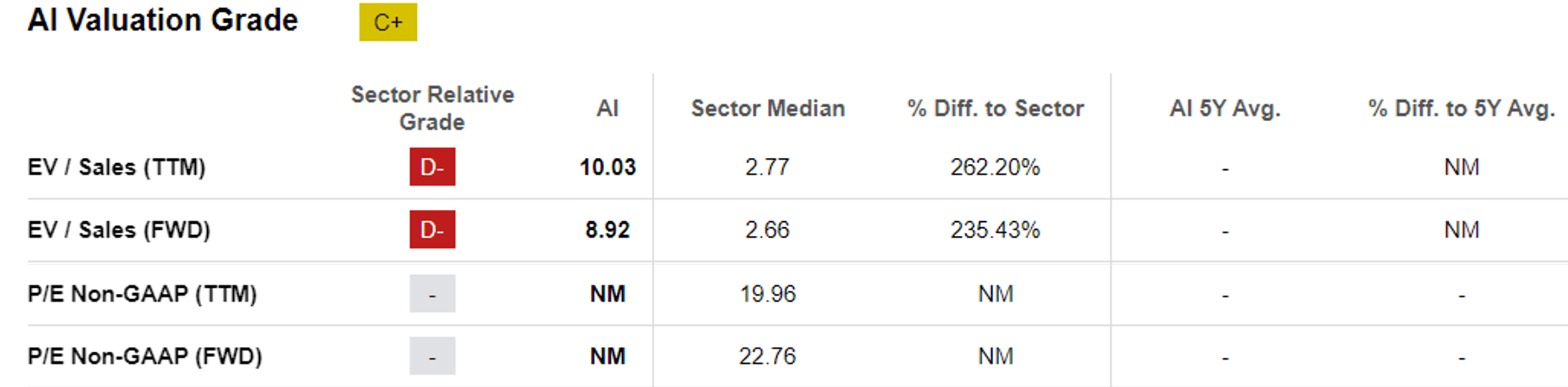

C3.ai Valuations

Looking for Alpha

Maybe for this reason Mr. Market has awarded the C3.ai inventory with the premium FWD EV/ Gross sales of 8.92x, nonetheless comparatively increased than its 1Y imply of seven.16x and the sector median of two.71x.

The identical premium has additionally been noticed in its SaaS supplier friends, reminiscent of CrowdStrike (CRWD) at 18.05x, MSFT at 11.24x, NVDA at 19.42x, and PLTR at 16.60x, implying their comparatively stretched valuations at a time of Generative AI hype.

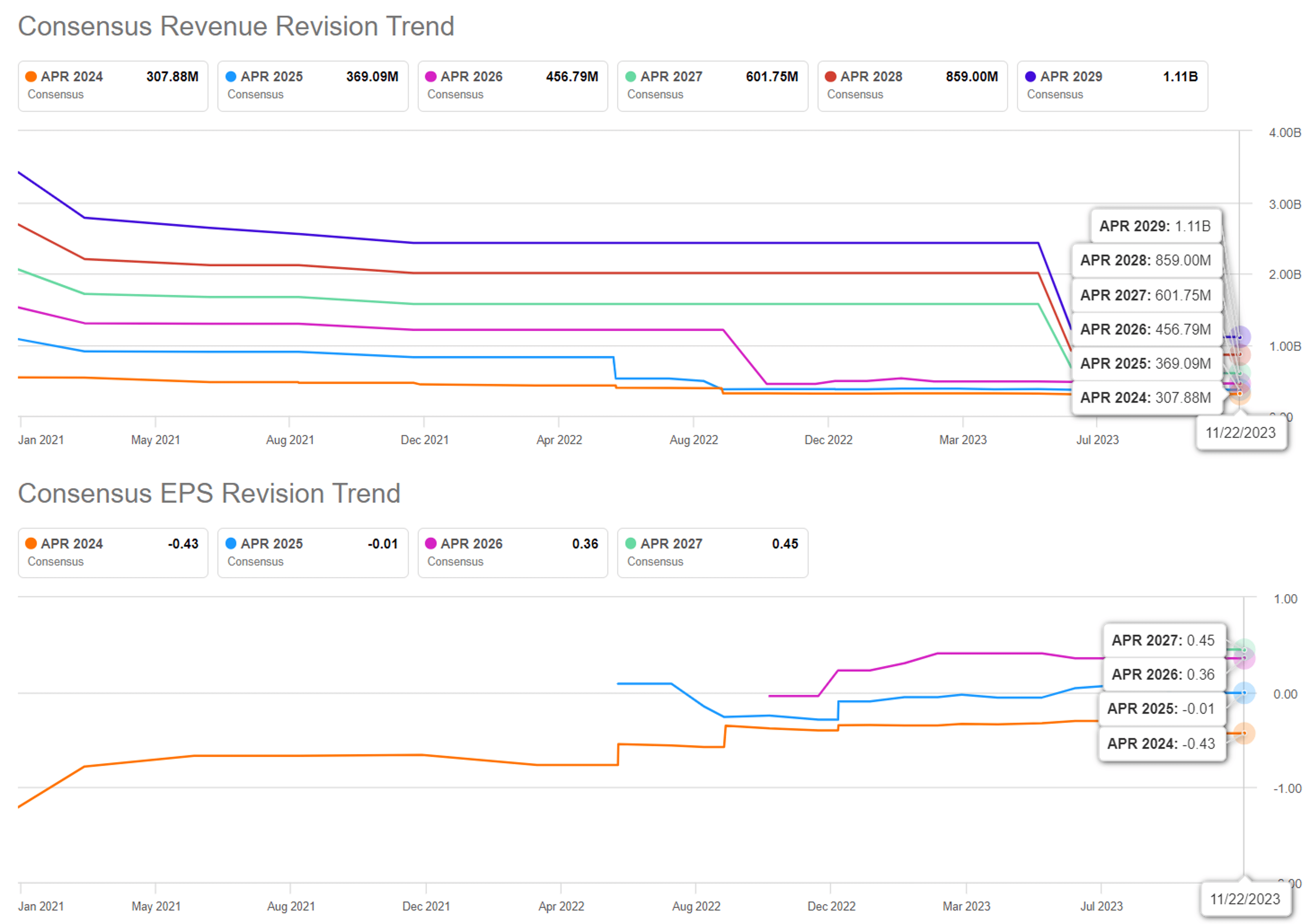

The Consensus Ahead Estimates

Looking for Alpha

Then once more, herein lies the dillemma.

C3.ai’s top-line prospects have been notably downgraded to a CAGR of +19.6% by means of FY2026, with a chronic adj EPS/ FCF profitability. That is in comparison with the earlier estimates of +22.1% and FY2025 adj EPS/ FCF profitability, respectively.

Given their efforts to restructure its world gross sales group principally composed of technical area specialists, it’s obvious that the administration has elected to seize market share and shopper base first, earlier than specializing in its backside line.

For now, the downgraded prime line estimates and extended profitability suggest that the C3.ai inventory could have pulled ahead most of its upside potential, with the premium valuations providing a minimal margin of security at present ranges.

This additionally implies that the SaaS firm’s reliance on stock-based compensation could stay elevated over the following few years, additional accelerating its share dilution from the 118.65M reported within the newest quarter (+2.97M QoQ/ +9.77M YoY).

Regardless of the supposedly giant generative AI TAM of as much as $1.3T by 2032, it additionally stays to be seen how a lot of it could fall on C3.ai’s lap, with its FQ4’23 income steering of $76M on the midpoint (+3.7% QoQ/ +13.9% YoY) showing to be underwhelming.

That is in comparison with PLTR’s accelerating QoQ/ YoY growth, with FQ3’23 revenues of $558.16M (+4.6% QoQ/ +16.8% YoY) and FQ4’23 steering of $601M (+7.6% QoQ/ +18.1% YoY).

Solely time could inform.

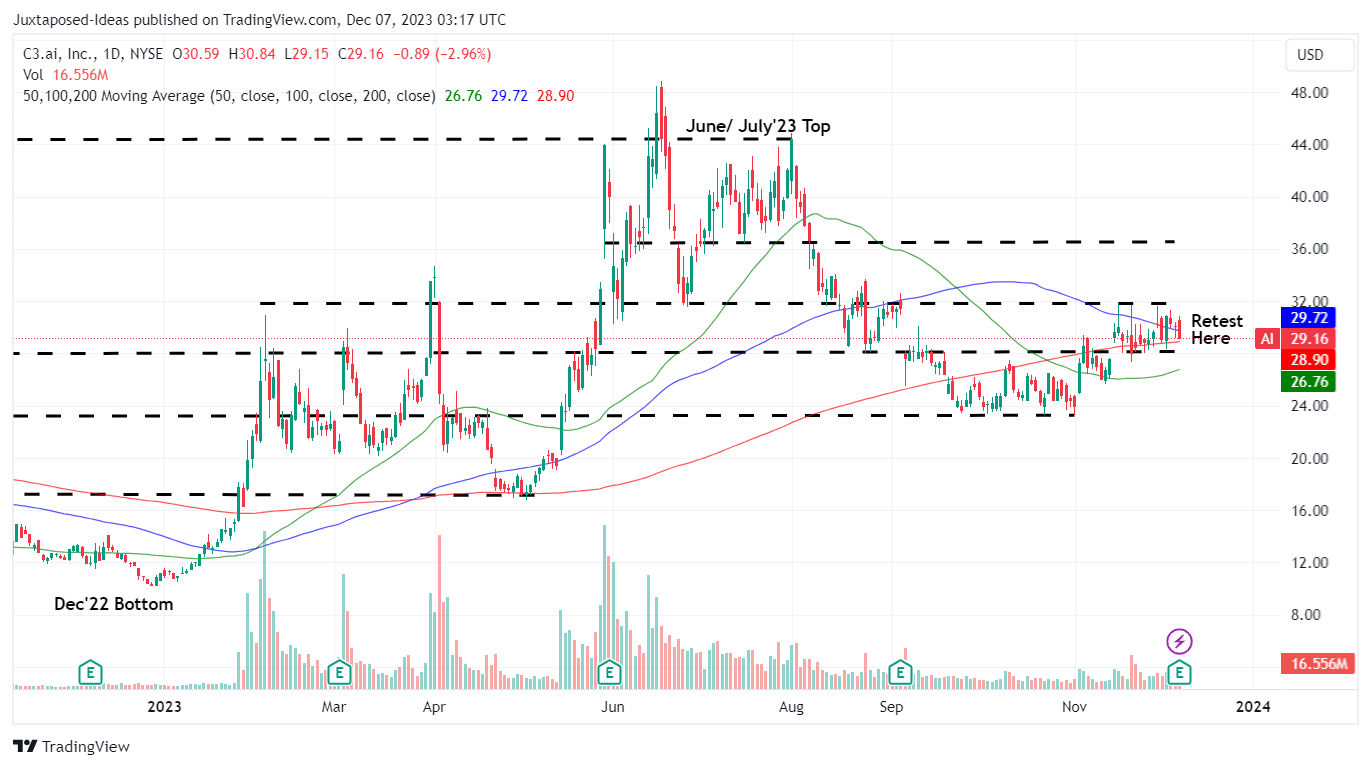

So, Is C3.ai Inventory A Purchase, Promote, or Maintain?

C3.ai 1Y Inventory Worth

Buying and selling View

For now, C3.ai has already rallied over optimistically by +21.6% from the November 2023 backside, with the inventory showing to be nicely supported at $28s whereas assembly immense resistance on the $30s.

Nonetheless, we’re not satisfied about its long-term upside potential, with the inventory buying and selling means above its ebook worth per share of $7.91 and the minimal reversal in its adj EPS profitability of $0.36/ FCF of $39.22M by FY2026.

Whereas C3.ai has reported accelerating pilot/ adoption, we imagine that the continuing consumption-based pricing mannequin could pose near-to-intermediate-term headwinds to its stability sheet, with a web money place of $762.3M (+1.5% QoQ/ -9.2% YoY), with it remaining to be seen if the earlier money burn could proceed.

Mixed with the potential volatility related to its immense quick curiosity of 34.35% on the time of writing, we want to proceed score the C3.ai inventory as a Maintain (Impartial) right here.