Win McNamee/Getty Pictures Information

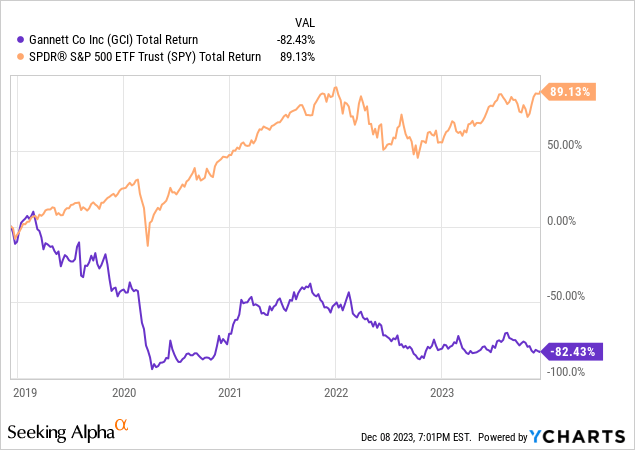

Gannett Co Inc (NYSE:GCI) has not proved an excellent funding over the previous few years as the corporate has struggled to adapt to a altering media panorama.

Whereas different Looking for Alpha analysts are present bullish on the inventory, there are 4 explanation why I’m presently cautious:

1. Q3 outcomes have been disappointing and the corporate lowered FY 2023 steering

2. The corporate has a extremely leveraged steadiness sheet and should wrestle to refinance its current debt

3. Print media enterprise continues to wrestle and nonetheless accounts majority of income

4. Lack of any near-term catalyst

1. Q3 outcomes have been disappointing and the corporate lowered FY 2023 steering

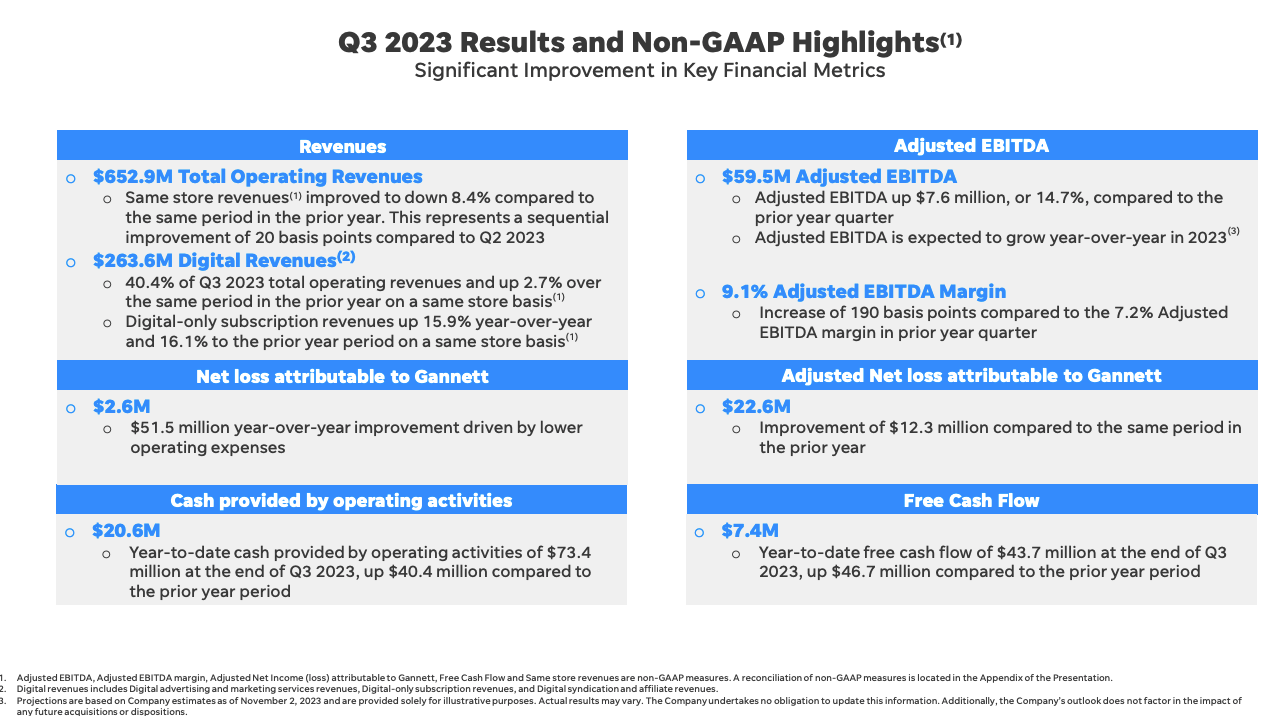

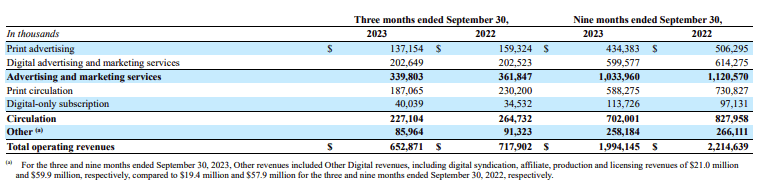

On November 2, 2023 GCI reported Q3 2023 outcomes that disenchanted traders. The corporate reported GAAP EPS of $0.02 per share which beat consensus estimates by $0.01 and evaluate favorably to a lack of $0.39 per share throughout the identical interval a yr in the past. GCI reported income of $652.9 million, missed consensus estimates by $7.53 million, and represents a 9.1% decline from the identical interval a yr in the past.

Probably the most disappointing a part of the Q3 report was the truth that GCI lowered its full yr outlook. The corporate lowered its income outlook to a variety of $2.65 – $2.67 billion down from a earlier vary of $2.75 – $2.8 billion. GCI additionally lowered its Adjusted EBITDA steering to a variety of $270 – $290 million down from a earlier vary of $290 – $310 million.

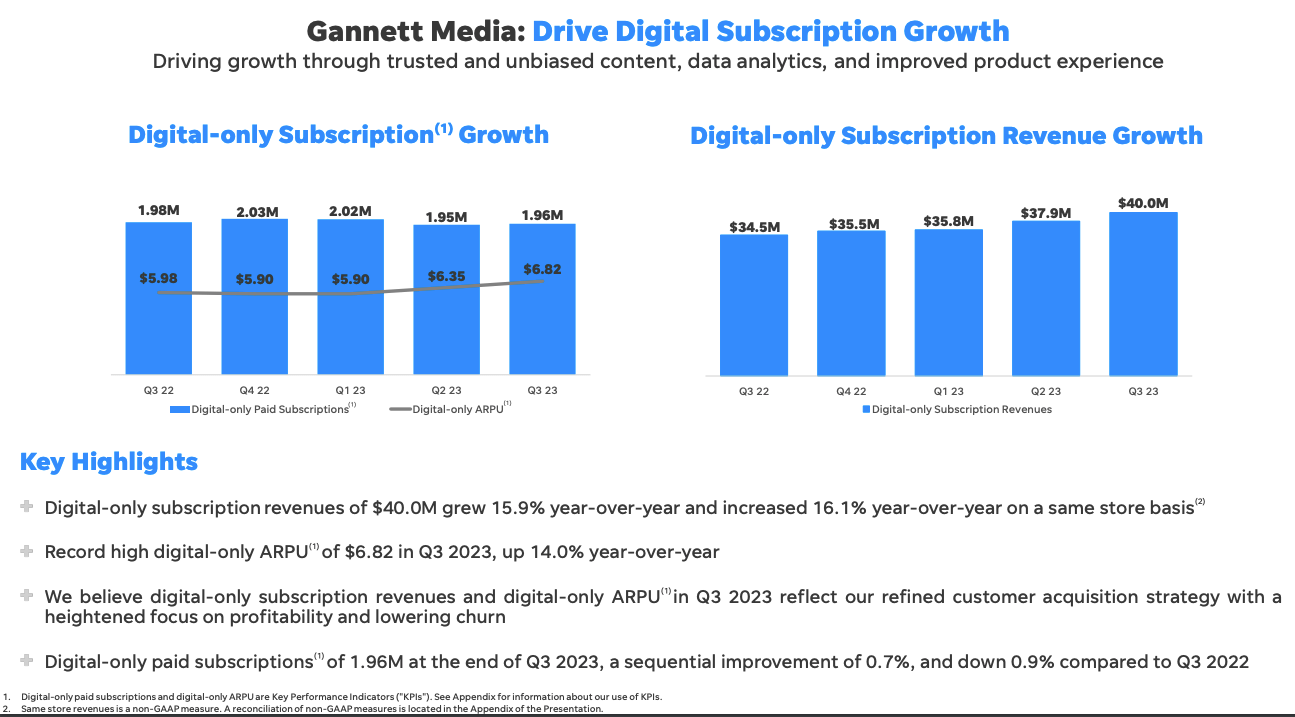

One other comparatively disappointing a part of the Q3 earnings launch was the truth that digital revenues elevated simply 2.7% in comparison with the identical interval a yr in the past on a similar retailer foundation. Digital paid subscriptions for the quarter got here in at 1.96 million representing a 0.7% enhance from Q2 2023 however down 0.9% in comparison with Q3 2023.

In response to this improvement, GCI shares plunged by 25%. Through the Q3 earnings name the corporate blamed the its steering lower on macroeconomic headwinds:

Whereas we made nice strides on our strategic priorities, we should acknowledge the complicated financial setting through which we’re working. We imagine there are indicators that buyers are starting to really feel the cumulative influence of upper rates of interest and continued inflation which has led to an total discount in shopper confidence. Consequently, the small and medium-sized companies we serve have grow to be extra cautious of their method to promoting expenditures than we had beforehand seen.

These outcomes are notably disappointing as friends have reported higher outcomes. For instance, The New York Instances (NYT) reported a 9.3% enhance in income, a 13.7% enhance in digital income, and a 9.5% enhance in digital subscribers all on a year-over-year foundation.

Given this, the distinction in comparatively trajectory I’m involved that GCI could also be experiencing firm particular points and never merely promoting softness on account of a weaker financial system.

GCI Investor Presentation GCI Investor Presentation

2. The corporate has a extremely leveraged steadiness sheet and should wrestle to refinance its current debt

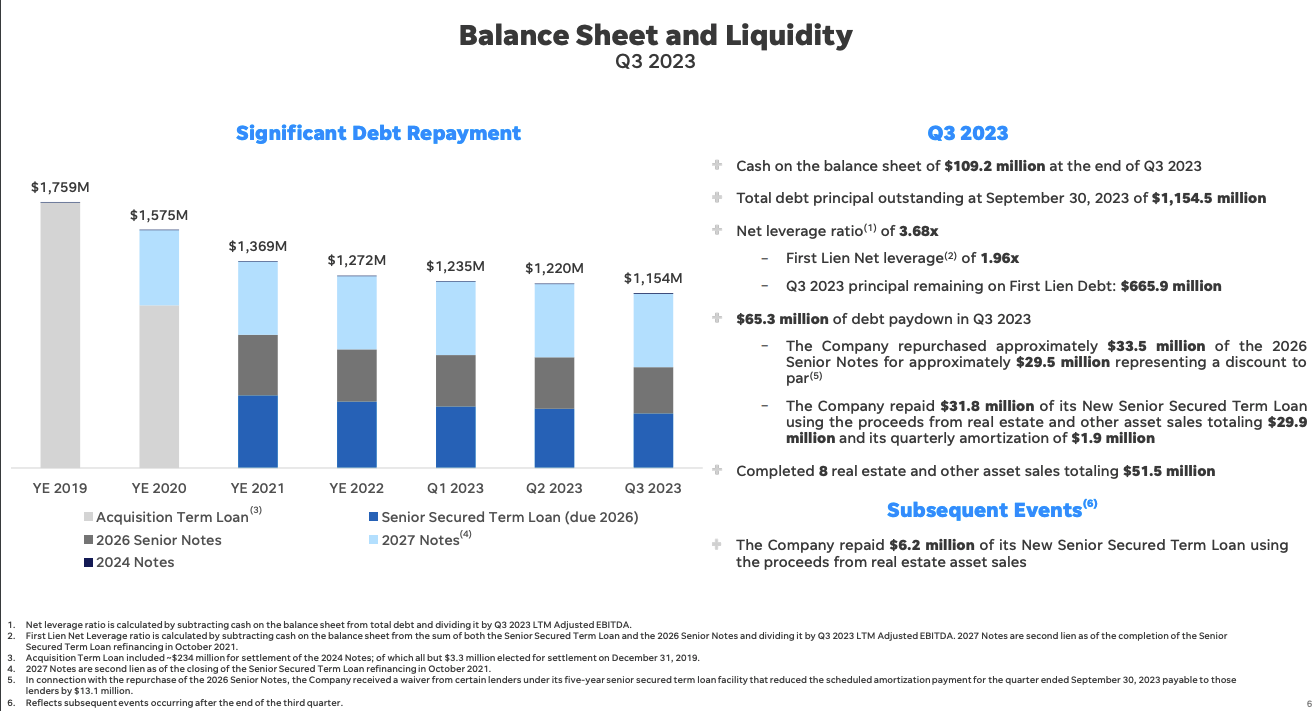

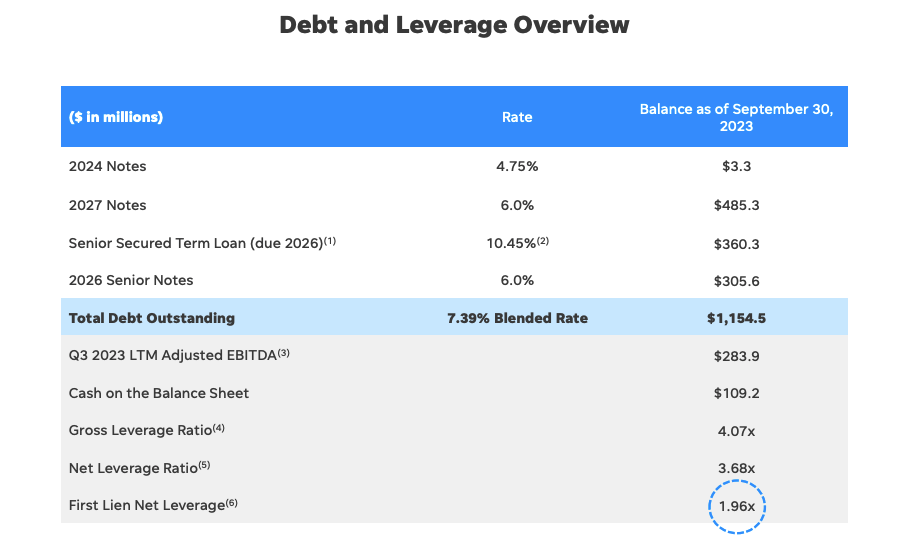

Whereas GCI has made appreciable progress bettering its steadiness sheet over the previous few years, the corporate stays extremely levered. As of Q3 2023, GCI had a complete web leverage ratio of three.68x and a gross leverage ratio of 4.07x. I view this as a reasonably excessive degree of leverage for any firm not to mention one which has struggled to attain profitability.

At present, GCI has a blended price of debt of seven.39%. Whereas this price may be very engaging given the present degree of rates of interest it’s probably that GCI will expertise a big enhance in its blended price of debt as soon as it’s pressured to refinance the $305.6 million in 2026 Notes and $485.3 million 2027 Notes.

Given the present degree of rates of interest and danger related to a extremely levered comparatively cyclical firm I imagine GCI can be pressured to pay at the least 12% to refinance these notes. The results of this could be a further ~$47.5 million in annual curiosity expense.

To place this quantity into context take into account the truth that GCI expects to generate free money move of $65 – $85 million for FY 2023.

In a greatest case situation, GCI might be able to generate sufficient money move over the subsequent two years to scale back the quantity of debt it must refinance. In a worst case situation, GCI might expertise money burn and EBITDA deterioration within the occasion of a recession which has the potential to make refinancing at any degree of charges difficult or unattainable.

GCI might be able to handle its steadiness sheet however there may be little or no margin of error.

GCI Investor Presentation GCI Investor Presentation

3. Print media enterprise continues to wrestle and nonetheless accounts majority of income

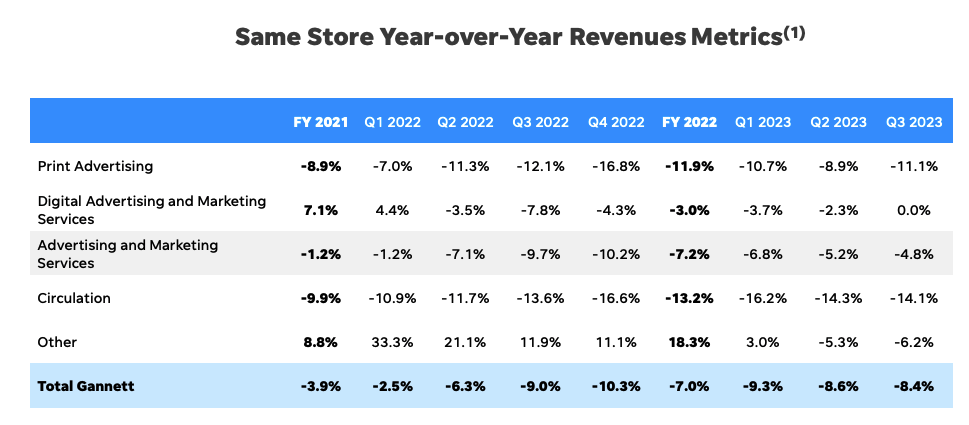

Digital income accounts for simply 40.4% of whole income and thus print associated income stays GCI’s major income driver. The print enterprise continues to expertise sharp declines on account of a secular shift in the direction of on-line media.

Throughout Q3 2023, GCI reported an 11.1% decline in print promoting income in comparison with the identical interval a yr in the past on a similar retailer foundation. Print circulation revenues, which account for 28.7% of the corporate’s whole income, fell by ~19% throughout Q3 2023 in comparison with the identical interval a yr in the past. These declines are staggering and symbolize a key headwind for GCI. Comparably, The New York Instances reported only a 1.8% decline in print subscription revenues for Q3 2023. Equally, New Corp (NWSA) reported that circulation income at Dow Jones, writer of The Wall Avenue Journal, fell by ~1% throughout Q3 2023 in comparison with the identical interval a yr in the past.

These outcomes means that the USA At present and different key print properties owned by GCI are performing significantly worse than different print publications. It is a main detrimental given the corporate’s continued reliance on the print media enterprise.

GCI Investor Presentation GCI Q3 2023 10Q

4. Lack of any near-term catalyst

Some may argue that GCI is an affordable inventory primarily based on the truth that it trades at ahead EV/ EBITDA of simply 5.3x in comparison with friends resembling NYT and NWSA which commerce at 18.5x and 10.4x ahead EV / EBITDA multiples. Whereas GCI is a weaker enterprise, it could possibly be argued that the valuation low cost must be smaller than is presently the case given GCI’s sturdy digital advertising and marketing companies enterprise.

Nonetheless, I don’t presently see any catalyst which means that GCI is about to shut this valuation hole anytime quickly. The corporate has a $96.9 million share repurchase authorization however it seems extremely unlikely that the corporate will repurchase any shares within the near-term given steadiness sheet challenges.

It additionally appears extremely unlikely that the corporate can be acquired by one other media firm given its excessive debt load.

The Bull Case

The bullish case for GCI facilities across the potential worth of its Digital Advertising Options (“DMS”) enterprise which provides a cloud-based platform of merchandise to allow small and medium-sized companies to perform advertising and marketing goals.

Throughout Q3 2023, DMS achieved LTM Revenues of $479 million and LTM Adjusted EBITDA of $57mm. Some have argued that DMS could also be conservatively price ~$800 million. Nonetheless, I don’t see a near-term path to monetization of that asset. That mentioned, the potential worth of this asset does hold me from score GCI as a promote.

The bulls additionally imagine that GCI will have the ability to expertise vital progress in its digital enterprise. Whereas this can be doable, latest outcomes have been extremely disappointing in comparison with different platforms which leads me to query the long-term earnings potential of GCI’s digital choices.

Conclusion

GCI has delivered weak outcomes for shareholders over the previous few years and is buying and selling at depressed ranges.

Different Looking for Alpha analysts are bullish on the inventory however I’m extra cautious. Weak Q3 outcomes in comparison with friends recommend the corporate could also be going through firm particular points associated to its print and digital media publication choices.

GCI has improved its steadiness sheet over the previous few years however stays extremely levered. The corporate is more likely to expertise a big enhance in curiosity expense over the subsequent few years as current fastened price debt will must be refinanced at a lot greater charges. Nonetheless, I imagine GCI may handle to refinance its debt at an affordable price if it is ready to pay down a good portion of its debt utilizing free money move over the subsequent two years. That mentioned, the steadiness sheet will show tough to handle via even a average financial decline.

The corporate’s near-term revenues stay primarily pushed by print promoting and circulation income. GCI’s print enterprise has carried out very poorly each on an absolute foundation and vs friends suggesting firm particular points have performed a job within the sharp decline of the enterprise.

GCI trades at a really low-cost valuation vs friends however lacks any near-term catalyst. One potential catalyst can be some type of monetization of GCI’s DMS enterprise.

I’m initiating GCI with a maintain score however would take into account upgrading the inventory to purchase if a monetization catalyst emerged surrounding its DMS enterprise or if the corporate have been to considerably enhance its steadiness sheet.