Just_Super

All values are in USD except famous in any other case.

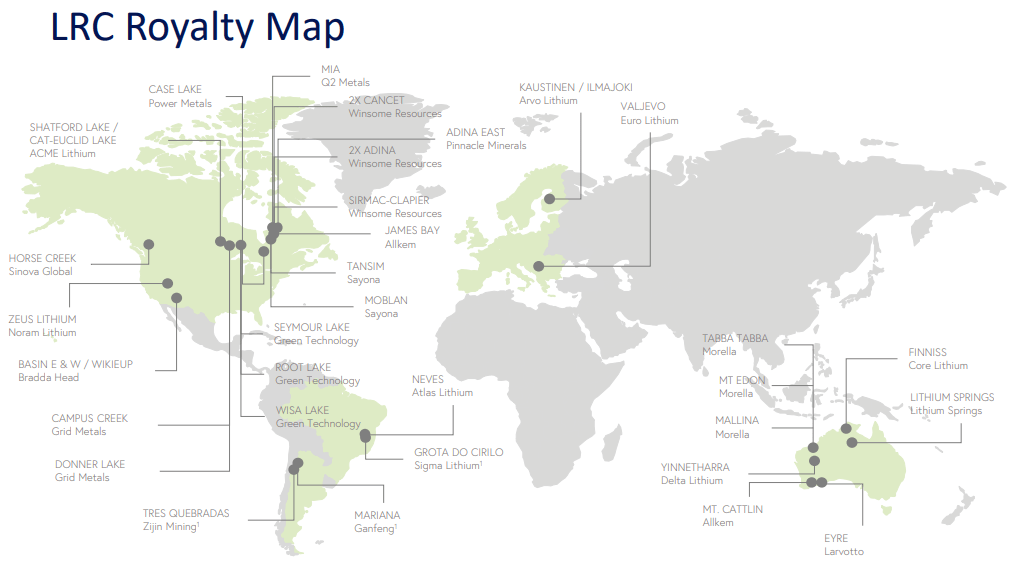

As its title suggests, the bread and butter of Lithium Royalty Corp. (OTCPK:LITRF, TSX:LIRC:CA) is royalty earnings. The LIRC portfolio includes 34 royalty pursuits in 32 mining properties situated within the Americas, Australia, and Europe.

Dec 2023 Presentation

This Canadian enterprise started operations in 2018 and has been including to its portfolio at a gentle charge over the past six years.

Dec 2023 Presentation

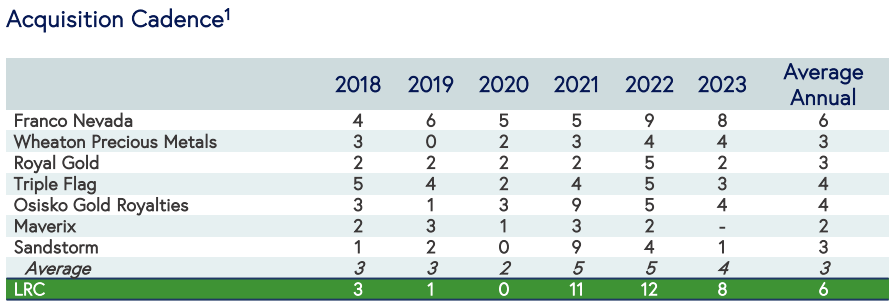

Whereas Lithium Royalty Corp. has been constructing its portfolio for over half a decade, it made its public debut solely earlier this 12 months, in March. LIRC IPO’d with an issuance of 8.8 million shares at a value of $12.35/share. The market has not shared within the firm’s perception vis-à-vis its worth and has pulled it down greater than a notch.

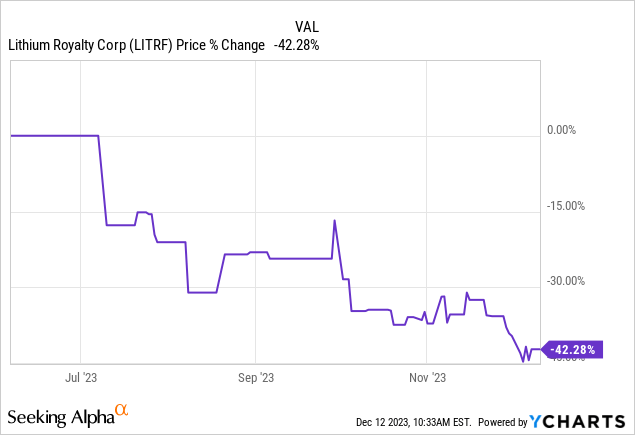

LIRC, nonetheless, stays undeterred by the market pricing, and the Q3 outcomes have it estimating the online asset worth, or NAV, to be round $15/share ($831 million / 55 million shares excellent).

Dec 2023 Presentation

Talking in regards to the firm’s portfolio (which types the predominant portion of its NAV), LIRC targets mining properties that produce lithium and different uncooked supplies for automotive batteries. The “overarching objective” as famous within the MD&A is:

to develop our portfolio and web asset worth via ongoing investments in royalties inside an electrification and decarbonization macroeconomic theme, with an emphasis on lithium.

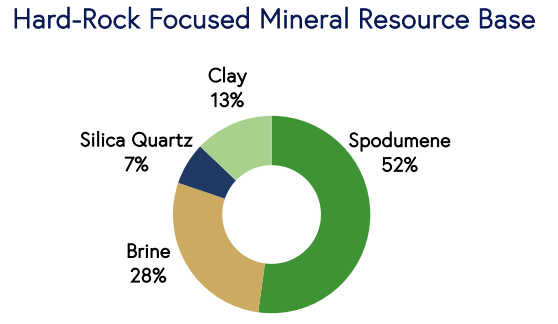

The corporate’s present portfolio base exhibits their dedication to the lithium trigger.

Dec 2023 Presentation

Three of the 32 properties within the LIRC portfolio are presently producing the products, with an equal quantity within the building stage. The steadiness of 26 are in numerous levels of improvement and exploration, the place no resolution has been made to start building. By way of the quantity invested by LIRC in these properties, 20% of its asset base is yielding royalties presently, with the perfect but to return.

Dec 2023 Presentation

LIRC expects the development section property to start manufacturing in 2024. Alternatively, the corporate doesn’t anticipate the 45% to provide till 2025. The LIRC earnings are a mixture of Gross Overriding Royalties [GOR], Web Smelter Return [NSR] and royalties primarily based on tonnage. Not like the tonnage-based charge, the previous two are impacted by the realized revenues of the miner.

In all circumstances, the market value of lithium dictates not solely the revenues, but in addition the speed at which the mining initiatives transfer alongside from improvement to manufacturing. One other all-pervasive issue impacting LIRC backside line is overseas alternate, for the reason that firm conducts its enterprise utilizing the USD, and it doesn’t essentially obtain royalties in the identical foreign money.

Q3 2023 Outcomes

LIRC has 3 out of 32 initiatives which might be producing presently, 2 of which solely started manufacturing in 2023. That is mirrored within the sixfold enhance in year-over-year royalty earnings. On the expense facet, the corporate was hit with bills associated to its public debut, leading to considerably greater basic and administrative outlays in comparison with the prior 12 months.

Q3-2023 MD&A

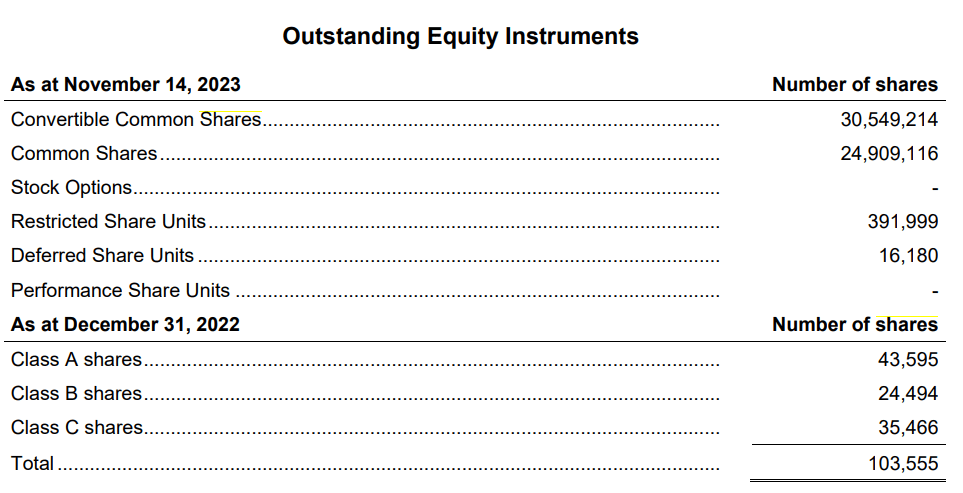

The 103,555 widespread shares pre-IPO had been transformed into 46,358,131 widespread shares in the course of the course of. Therefore the distinction within the respective interval ending shares shouldn’t be as steep because the under comparability would counsel.

Q3-2023 MD&A

LIRC’s money reserves declined from round $36 million at December 31, 2022, to $13.5 million on the finish of September. The 2023 acquisition exercise consumed most of this money. The administration indicated that remaining web proceeds from the IPO and the three producing mines had been ample to fulfill its working and dealing capital necessities for now. As well as, LIRC additionally has a $25 million credit score facility with Nationwide Financial institution of Canada, the funds of which may be utilized for working and funding functions. The phrases of the association are specified by the MD&A.

- Base charge mortgage with curiosity payable month-to-month on the Nationwide Financial institution base charge, plus between 2.00% and three.25% every year relying upon the Firm’s leverage ratio; or

- Time period loans for intervals of 1, 3 or 6 months with curiosity payable on the charge of term-based Secured In a single day Financing Price (“SOFR”), plus between 3.1% and 4.5% every year, relying on the Firm’s leverage ratio.

As of September 30, 2023, no quantities had been drawn on the power.

The Macro

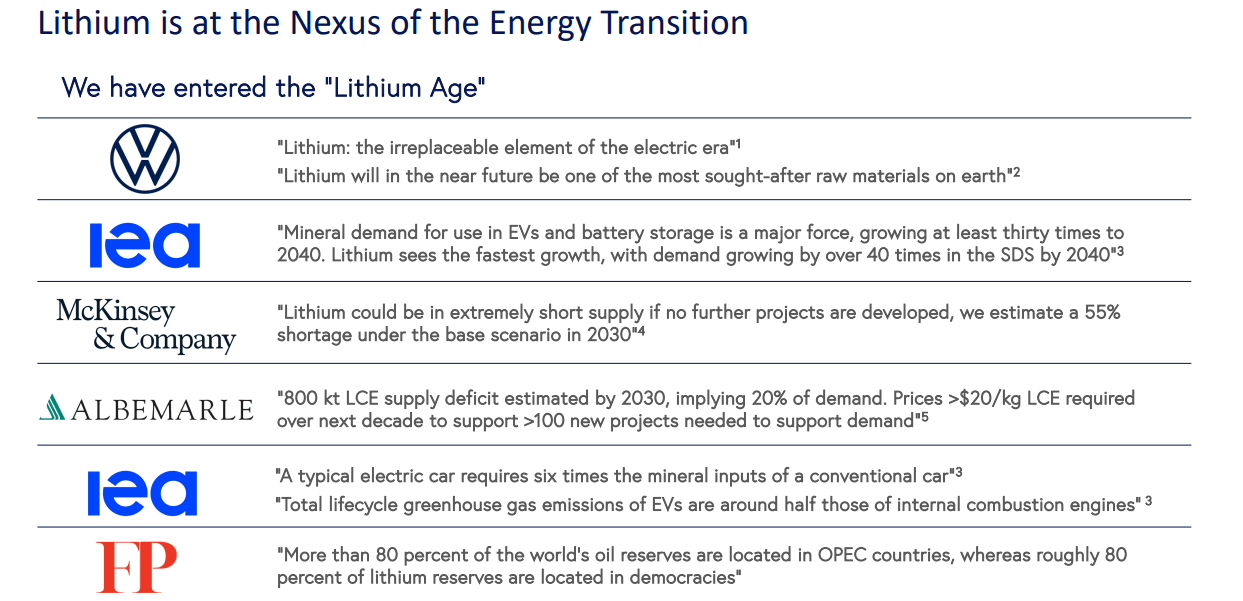

The lithium story has been getting loads of consideration over the past 3 years. Simply have a look at among the feedback being made by McKinsey, IEA, and Albemarle Company (ALB).

Dec 2023 Presentation

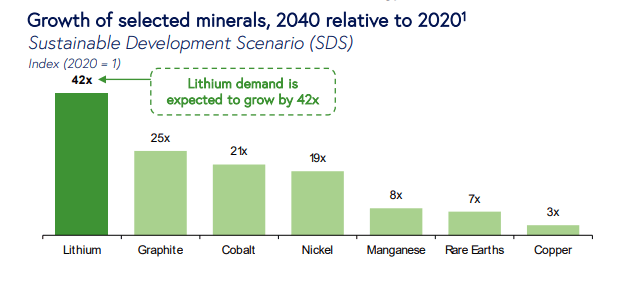

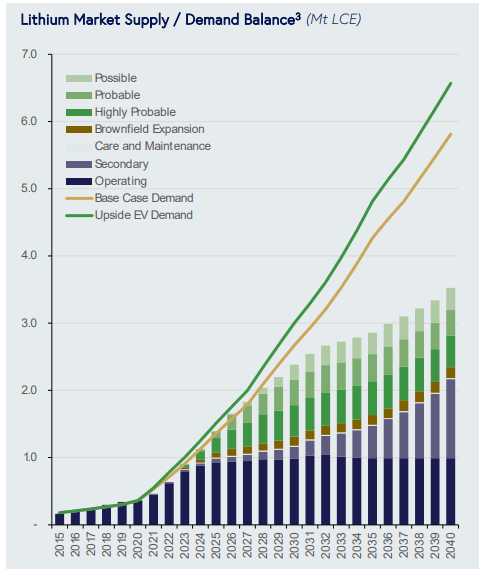

Estimates are that demand will go up 42-fold relative to the 2020 base by the 12 months 2040. It’s attention-grabbing that we see a number of tales that copper might be in brief provide by 2040, however lithium, which is meant to outpace that by 14-fold, will get much less consideration.

Dec 2023 Presentation

After all, if demand grows as anticipated, you may count on some extreme shortfalls by the point you get anyplace near that timeframe.

Dec 2023 Presentation

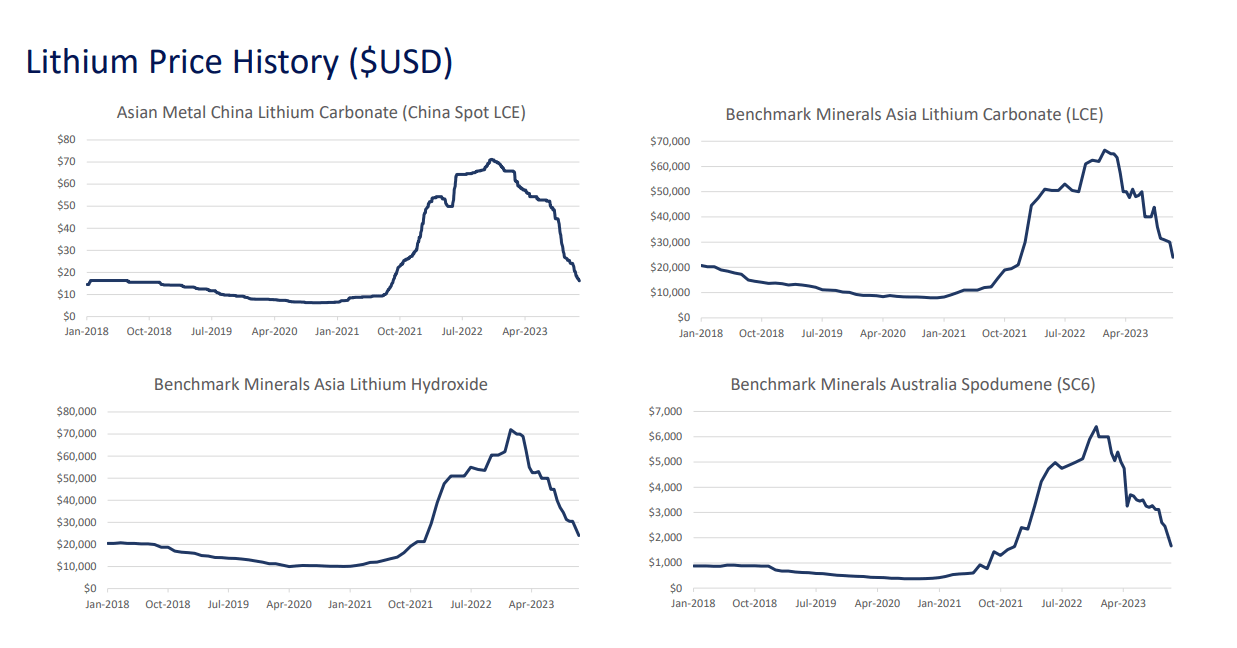

No person advised the lithium value that story, it seems. The value peaked in early 2023, and has been dropping like a stone since then.

Dec 2023 Presentation

Our take right here is that the story is, after all, as actual because it will get. However one should not utterly dismiss the counterarguments. From our perspective there are 3 main ones.

1) Lithium could also be ruling the roost at the moment, however various applied sciences might displace at the very least a portion of the overall demand. Right here is one which buyers ought to watch.

Toyota says it has made a technological breakthrough that can enable it to halve the load, dimension and value of batteries, in what might herald a serious advance for electrical automobiles.

The world’s second-largest carmaker was already pursuing a plan to roll out automobiles with superior solid-state batteries, which supply advantages in contrast with liquid-based batteries, by 2025.

Kaita mentioned the corporate had developed methods to make batteries extra sturdy and believed it might now make a solid-state battery with a spread of 1,200km (745 miles) that would cost in 10 minutes or much less.

The corporate expects to have the ability to manufacture solid-state batteries to be used in electrical automobiles as quickly as 2027, in line with the Monetary Instances, which first reported on Toyota’s claimed breakthrough.

Strong-state batteries have been extensively seen as a possible game-changer for electrical automobiles, promising to cut back charging occasions, enhance capability and cut back the fireplace threat related to lithium-ion batteries, which use a liquid electrolyte.

Nevertheless, solid-state batteries have sometimes been tougher and costlier to make, limiting their business utility.

Supply: The Guardian.

2) The second argument is that lots of these different components proven above (like uncommon earths, cobalt, and many others.) might develop into a limiting issue for whole lithium utilization. If the automotive can’t be manufactured because of a scarcity of any of these components, then, nicely, you will not use the lithium both.

3) The ultimate one is that one shouldn’t underestimate the provision response. Provide has been blistering and is poised to extend dramatically in 2024 and 2025. Ultimately, the overhang will cross, however it can take some painful years within the interim.

Verdict

Chalk it as much as actually poor timing. The IPO got here proper close to the worth peak for Lithium.

Lithium Royalty Corp. slipped 0.6 p.c in its Toronto Inventory Alternate buying and selling debut after elevating $150 million (US$109 million) in Canada’s greatest preliminary public providing in 10 months.

Shares of the Toronto-based firm fell to $16.90 at 9:30 a.m. begin of buying and selling Thursday on an “if, as and when issued basis,” barely under its IPO value. The inventory was down 1.8 p.c as of 9:45 a.m.

Lithium Royalty offered 8.82 million shares for $17 apiece in its IPO, inside its focused vary of $16 to $19. That makes it the largest IPO on a Canadian alternate since final Could, when Bausch + Lomb Corp. was spun off in a twin itemizing and Dream Residential Actual Property Funding Belief went public.

The sale, which confirms an earlier report by Bloomberg, brings one other lithium-based firm to the Toronto Inventory Alternate when the urge for food for battery metals is hovering on robust prospects for electrical automobiles. The corporate, which was based by Waratah Capital Advisors Ltd. in 2018, trades beneath the inventory image LIRC.

Supply: BNN Bloomberg.

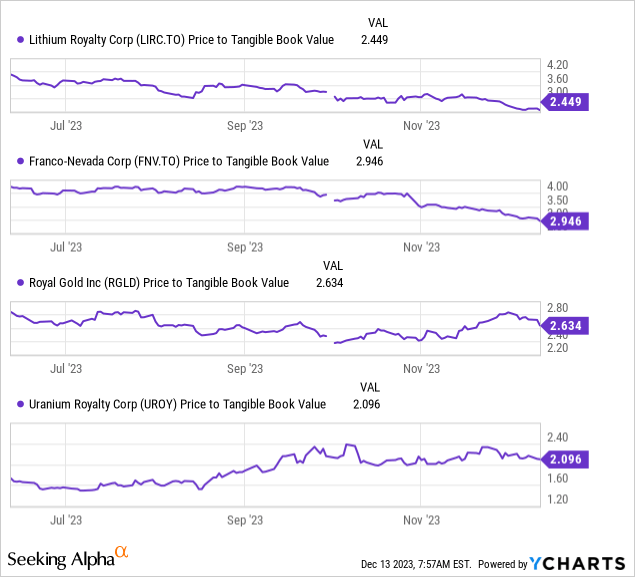

We might have really favored it extra at this level, if the corporate had raised much more money at that $16.90 value level. That will have boosted the tangible guide worth per share (the apparent facet impact of elevating capital nicely above tangible guide worth per share). Because it seems, it was a bit low. At present, regardless of the close to 50% drop, LIRC shouldn’t be resoundingly low cost on this metric while you run towards established royalty firms like Franco-Nevada Company (FNV), or Royal Gold, Inc. (RGLD), and even ones that aren’t displaying any revenues like Uranium Royalty Corp. (UROY).

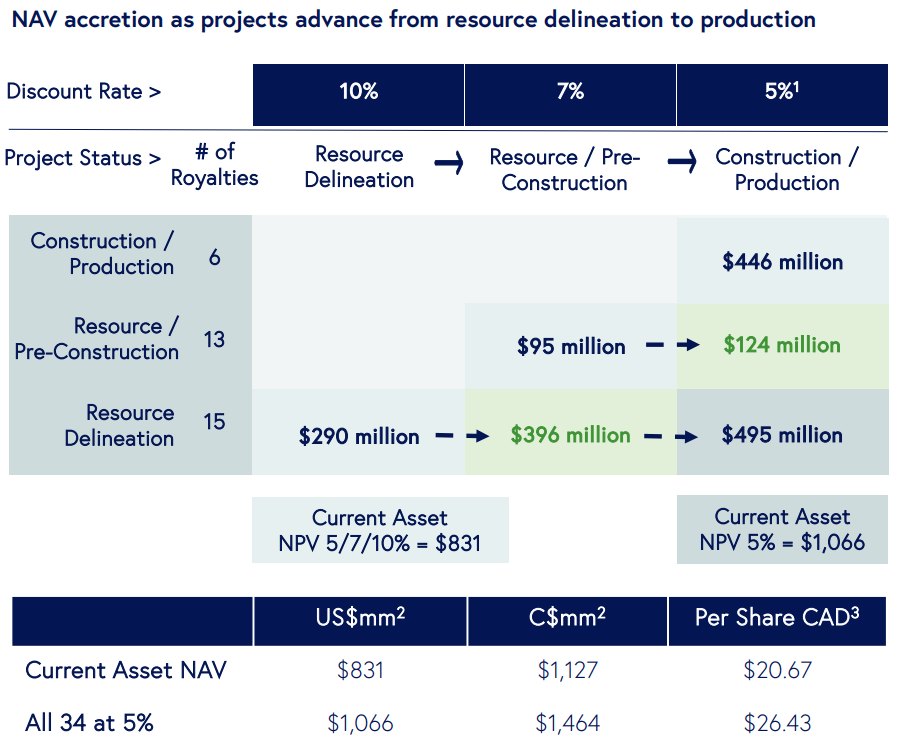

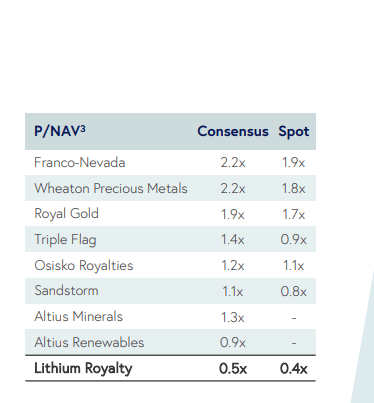

However value to tangible guide worth doesn’t all the time seize the potential in royalty performs. That is significantly true right here, as the corporate has been round since 2018 and loads of the offers had been struck over the past famine on this sector. The logic right here is that if LIRC strikes offers when the lithium value $10,000 per ton, it can earn more money in the long term versus in the event that they do it when lithium value is $60,000 per ton. Analysts have additionally established this of their fashions and have tried to determine what the actual worth of these royalty property is. In different phrases, determining a NAV.

Dec 2023 Presentation

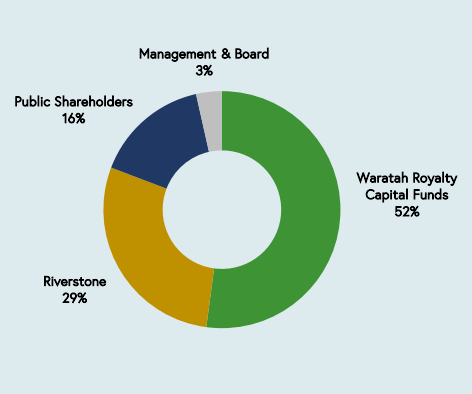

Everybody concurs that LIRC is radically undervalued primarily based on modeling that, and the numbers are just like what LIRC makes use of in its personal fashions. These NAV numbers above are from November 30, 2023, and LIRC is one other 10% decrease. So, it’s honest to say, you aren’t shopping for it with the FOMO crowd at this level. Administration is well-aligned right here, and Riverstone, which offered Hammerhead Vitality Inc. (HHRS) to Crescent Level Vitality Corp. (CPG), additionally owns an enormous chunk.

Dec 2023 Presentation

We expect Lithium Royalty Corp. inventory is an inexpensive wager right here for the lengthy haul, however tax loss promoting possible gives large headwinds for the subsequent 2 weeks.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.