The Daring Bureau/iStock through Getty Pictures

Introduction

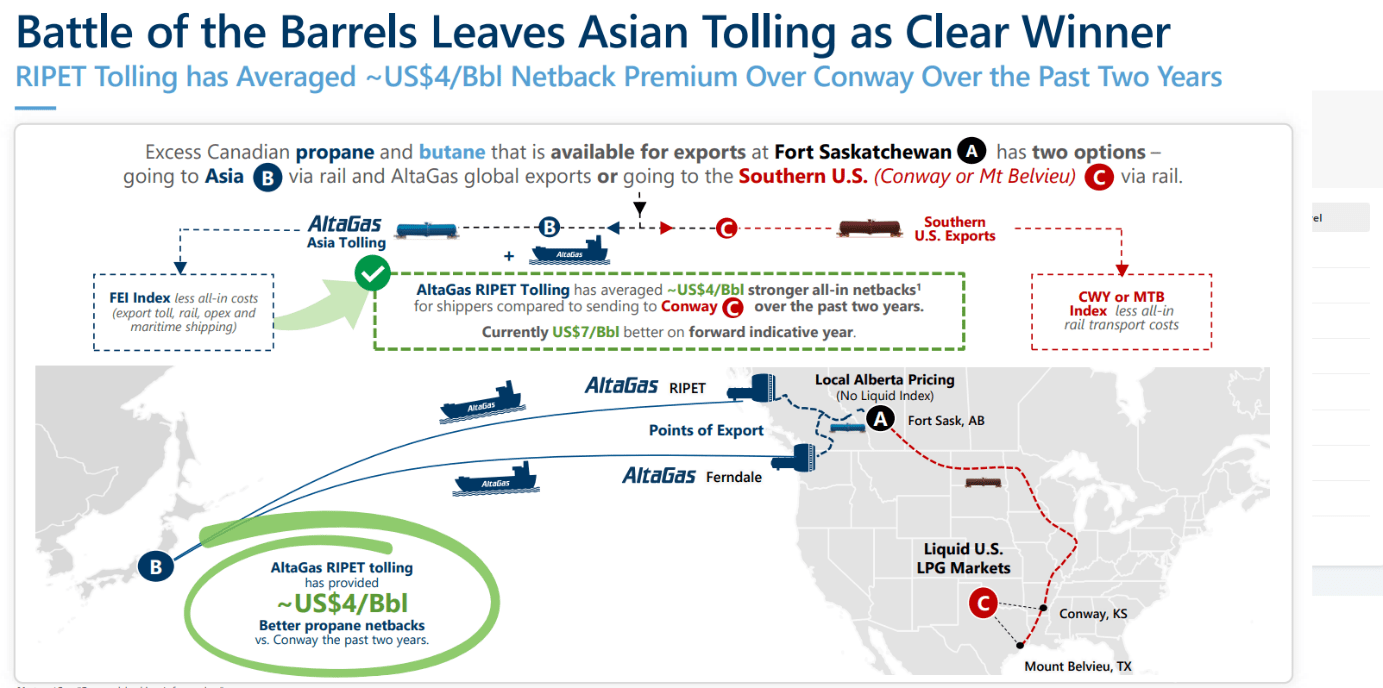

AltaGas (TSX:ALA:CA) (OTCPK:ATGFF) is a Canadian energy infrastructure company specializing in its utilities and midstream divisions. Within the midstream division, the corporate operates two LPG terminals which provide a aggressive benefit to serve Asian markets. Throughout the third quarter, AltaGas exported virtually 120,000 barrels of LPGs per day to Asia.

AltaGas Investor Relations

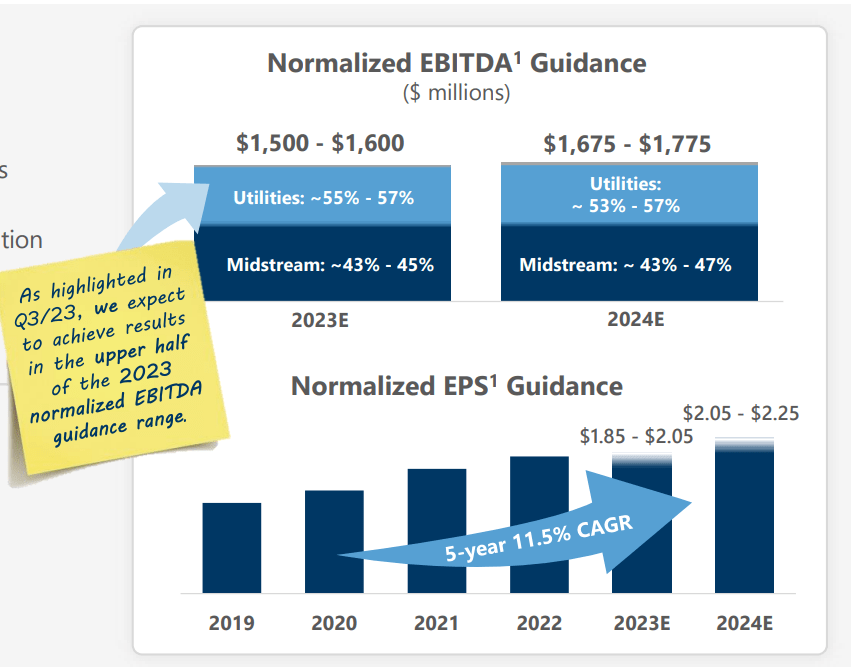

The utilities division consists of the rate-regulated pure fuel distribution belongings in Maryland and components Michigan, and primarily based on the expectations for 2023 and 2024, the utilities division will account for simply over half the EBITDA.

AltaGas Investor Relations

Whereas the corporate has a considerably decently liquid itemizing within the US, the corporate’s predominant itemizing is in Canada the place it is listed with ALA as its ticker symbol. The typical each day quantity in Canada exceeds 600,000 shares per day so traders with entry to the Canadian itemizing ought to positively commerce the place volumes are one of the best. As the corporate stories on its monetary ends in Canadian Greenback, I’ll use that foreign money as base foreign money all through this text, until indicated in any other case.

The just lately launched steerage for FY 2024 is interesting

The corporate just lately launched upbeat steerage for 2024, and I needed to have a better look to determine what this actually means for the corporate and its funding thesis.

The primary takeaway is AltaGas’ steerage to report a normalized EPS of C$2.05-2.25 per share, which might be a rise of roughly 10% on a YoY foundation utilizing the midpoints of the 2023 and the 2024 steerage. The corporate additionally expects to report a normalized EBITDA of C$1.675-1.775B Canadian Greenback which might be an 11% enhance on a YoY foundation, as soon as once more utilizing the midpoints of the respective steerage for each years. AltaGas expects to spend roughly C$1.2B on capital expenditures in 2024 with the bulk going towards the utilities division. Hardly a shock as that division additionally accounts for almost all of the EBITDA consequence.

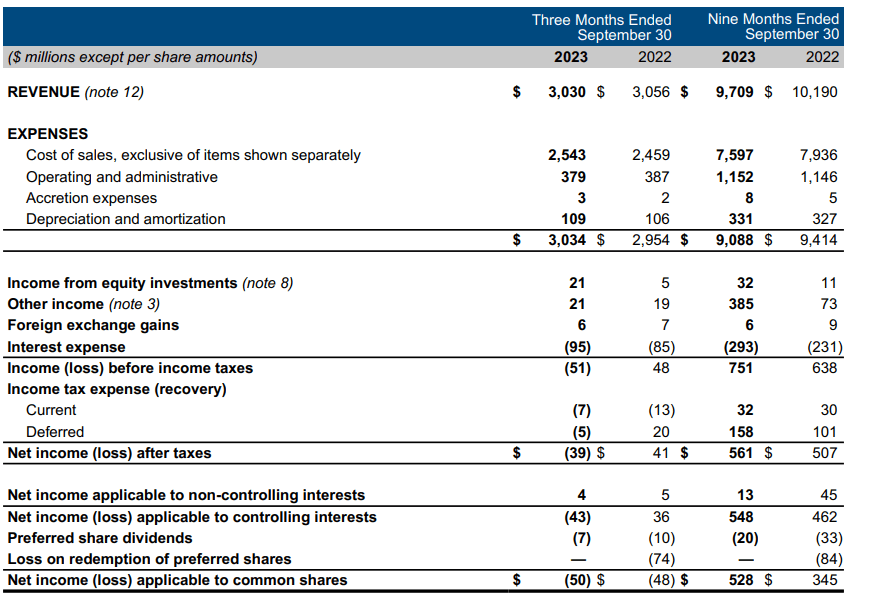

With a purpose to perceive the influence of the EBITDA steerage, we should always first take a look at how Transalta will carry out in 2023, and I believed it is smart to drag up the Q3 and 9M 2023 outcomes. And whereas the FFO is a vital metric for the corporate, I might first like to determine the anticipated sustaining free money movement.

Because the income statement below exhibits, the corporate reported roughly C$109M in depreciation and amortization bills within the third quarter whereas its curiosity bills got here in at C$95M.

AltaGas Investor Relations

That is vital to know as this permits us to use these numbers to the anticipated full-year EBITDA to find out the tax foundation and the full tax invoice. We all know the corporate goals for C$1.73B EBITDA (that is the midpoint of the FY 2024 steerage) and we all know the annualized depreciation and amortization costs shall be round C$450M. This ends in a C$1.28B EBIT, and after deducting roughly C$400M in curiosity bills, the pre-tax revenue shall be roughly C$880M whereas the online revenue ought to be round C$660M after making use of a mean tax fee of 25%.

From C$660M web revenue, we should always nonetheless deduct the anticipated C$25M in most popular dividend funds. That is decrease than what AltaGas shall be paying in 2023 (and the full quantity of most popular dividends might even drop to C$20M however I favor to err on the facet of being cautious right here) as the corporate just lately referred to as C$200M value of most popular shares.

This implies there shall be about C$635M in web revenue which, divided over the present share rely of 282M shares, the underside line consequence will present an EPS of roughly C$2.25. That is in keeping with the normalized EPS steerage, so the maths checks out.

Now we should always translate this right into a free money movement consequence. We all know the online working money movement ought to be roughly C$1.08B. Whereas this may not be enough to cowl the full anticipated capex invoice of C$1.2B, it is very important perceive the corporate plans to put money into further progress in 2024.

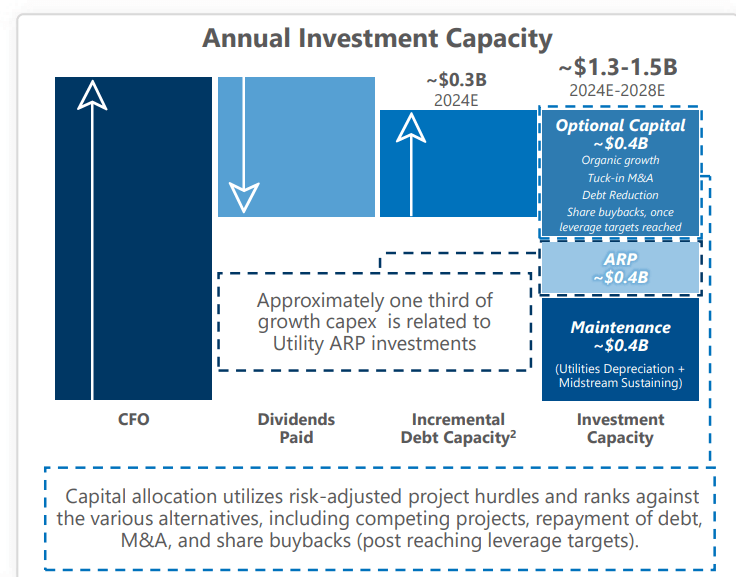

AltaGas Investor Relations

Because the picture above exhibits, the maintenance capex is just C$0.4B whereas the Accelerated pipeline Replacement Program will value a further C$0.4B per 12 months. You could possibly argue the ARP investments should not be thought of as a sustaining capex however these pipelines must get replaced over time anyway, however certainly not on the present tempo. In case you would come with the ARP investments within the free money movement calculation, you’d find yourself at a free money movement results of C$280M. for those who would exclude them, the underlying free money movement consequence can be C$680M or C$2.40 per share. I feel probably the most honest interpretation can be to incorporate a portion of the ARP within the sustaining capex wherein case the sustaining free money movement would come at a stage fairly near the adjusted EPS.

The corporate guarantees further dividend progress

After increasing the projected dividend by 6% to C$1.19 per share for 2024, AltaGas expects to be ready to proceed to extend its dividends within the foreseeable future. The official steerage requires an annual dividend CAGR of 5%-7% over the following 5 years. And AltaGas is clear sufficient to truly present a visualization of the anticipated dividend progress trajectory.

AltaGas Investor Relations

At a 5% CAGR, the dividend on the frequent shares would enhance to C$1.45 per share by FY 2028. At a 7% CAGR, this is able to leap to C$1.56 per share. And naturally the payout ratio of fifty%-60% of the adjusted EPS stays unchanged.

Funding thesis

Buying and selling at roughly 13 instances the mid-point of the anticipated earnings for 2024, AltaGas is not low-cost. That being mentioned, I am initiating a small lengthy place as I like the corporate’s aggressive place to ship NGL merchandise to Asia. The recently-announced acquisition of further infrastructure belongings will seemingly show to be a very good transfer whereas I like the corporate’s prudent capital allocation plans. Whereas 2024 shall be a capex-heavy 12 months, the underlying working and monetary efficiency ought to keep sturdy.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.