DamianKuzdak

We beforehand lined Pfizer (NYSE:NYSE:PFE) in September 2023, discussing its pessimistic efficiency because the decelerating COVID-19 portfolio and underperforming bolt-on acquisitions had contributed to its lowered FY2023 steering vary.

Mixed with the overly aggressive R&D efforts, costly acquisitions, and deteriorating stability sheet, we had most popular to cautiously charge the inventory as a Maintain then.

On this article, we will talk about why our downgraded ranking has confirmed to be proper, with the PFE inventory additional tumbling by -25.86% since then, attributed to the underwhelming FY2024 steering post-Seagen acquisition.

Whereas the pharmaceutical firm’s elementary efficiency stays considerably respectable, it’s obvious that bullish assist has fled for greener pastures, corresponding to generative-AI and weight reduction shares, with it remaining to be seen when a ground might materialize.

PFE’s Greatest Days Are Over For Now

With the closing of the Seagen deal, the PFE administration has reiterated their FY2023 revenue guidance of $59.5B (-40.6% YoY) and adj EPS steering of $1.55 (-76.4% YoY) on the midpoint.

Nonetheless, readers can also wish to notice that the quantity has been lowered from the earlier midpoint variety of $69B (-31.2% YoY) and $3.35 (-49% YoY) provided within the FQ4’22 earnings name.

It could be vital to know that the ultimate FY2023 income steering contains roughly $46.65B in non-COVID merchandise (+7% YoY) and $12.85B in COVID gross sales (-77.3% YoY).

Most significantly, regardless of the hefty $43B price ticket, Seagen is barely anticipated to contribute roughly $3.1B to PFE’s gross sales, bringing the latter’s general FY2024 income steering to $60B (+0.8% YoY) and adj EPS to $2.15 on the midpoint (+38.7% YoY).

Primarily based on the administration’s commentary, it seems that its non-COVID merchandise might generate as much as $50.84B in gross sales (+9% YoY) with an impacted COVID gross sales of $9.16B (-28.7% YoY).

There’s two methods to take a look at these numbers, to be trustworthy.

On the one hand, PFE’s non-COVID’s pipeline progress seems to be glorious certainly, in comparison with its historic progress development of +0.2% in FY2019. It’s obvious that the administration’s efforts to bolster its pipeline has been working as supposed, partly to offset the upcoming LOEs in 2026.

However, it’s obvious that Mr. Market expects the erosion in PFE’s COVID gross sales to be much less steep, primarily based on the earlier FY2024 consensus income estimates of $63.2B (+6.2% YoY) and adj EPS estimates of $3.17 (+104.5% YoY).

Its backside line prospects look like underwhelming as effectively, attributed to the FY2024 adj R&D expense steering of $11.5B (inline YoY/ +48.9% from FY2019 ranges of $7.72B) and the -$0.40 affect on its adj EPS attributed to the unprofitable Seagen.

Subsequently, whereas the administration has raised their annual internet value financial savings goal by $500M to not less than $4B by the top of 2024, it stays to be seen when sentiments might enhance, with market analysts doubtless pricing one other lowered COVID gross sales steering forward.

That is on prime of the pessimistic outlook for PFE’s weight loss pills, with two of its pipeline already failing to carry out as anticipated and just one awaiting early knowledge by H1’24.

This additional delays its reversal, with Eli Lilly (LLY) and Novo Nordisk (NVO) notably taking the lead on this area, with a supposed TAM of $77B by 2030, increasing at an accelerated CAGR of +54.27%.

PFE’s intermediate time period prospects aren’t helped by the deteriorating stability sheet as effectively, with the closing of $43B all-cash Seagen deal prone to drain its cash/ short-term investments of $44.17B within the newest quarter (-1.3% QoQ/ +22.2% YoY), whereas forsaking a bloated $61.04B in long-term money owed (-1% QoQ/ +85.2% YoY).

Mixed with its mixed FQ3’23 earnings result in October 2023, with revenues of $13.23B (+3.9% QoQ/ -41.5% YoY), adj EPS of -$0.17 (-125.3% QoQ/ -109.5% YoY), and $5.6B value of stock COVID write downs, it’s unsurprising that the just lately introduced FY2024 steering has triggered a steep plunge in its inventory worth.

The impacted profitability means that PFE might quickly make the most of its stability sheet and debt to service its annualized dividend obligations of $9.28B (inline QoQ/ +3.5% YoY) by the newest quarter.

The identical pessimism has additionally been urged by the Looking for Alpha Quant, attributed to its impacted TTM Curiosity Protection ratio of 4.28x and TTM Dividend Protection Ratio of 0.94x, in comparison with its historic common of 16.02x/ 2.45x and the sector median of seven.84x/ 3.68x, respectively.

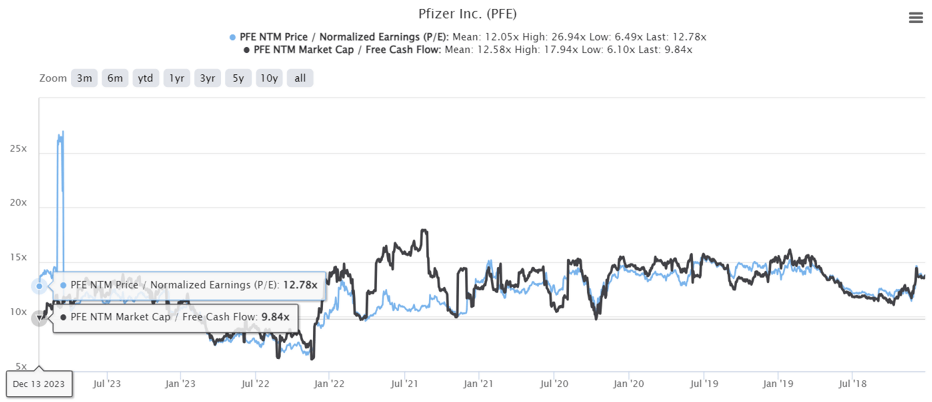

PFE Valuations

Tikr Terminal

Maybe that is additionally why PFE’s FWD P/E valuations of 12.78x and FWD Market Cap/ Free Money Circulate valuations of 9.84x have been considerably discounted, in comparison with its pre-pandemic imply of 14.23x/ 14.38x and the sector median of 10.97x/ 12.63x, respectively, although considerably inline to its 1Y imply of 12.46x/ 10.81x.

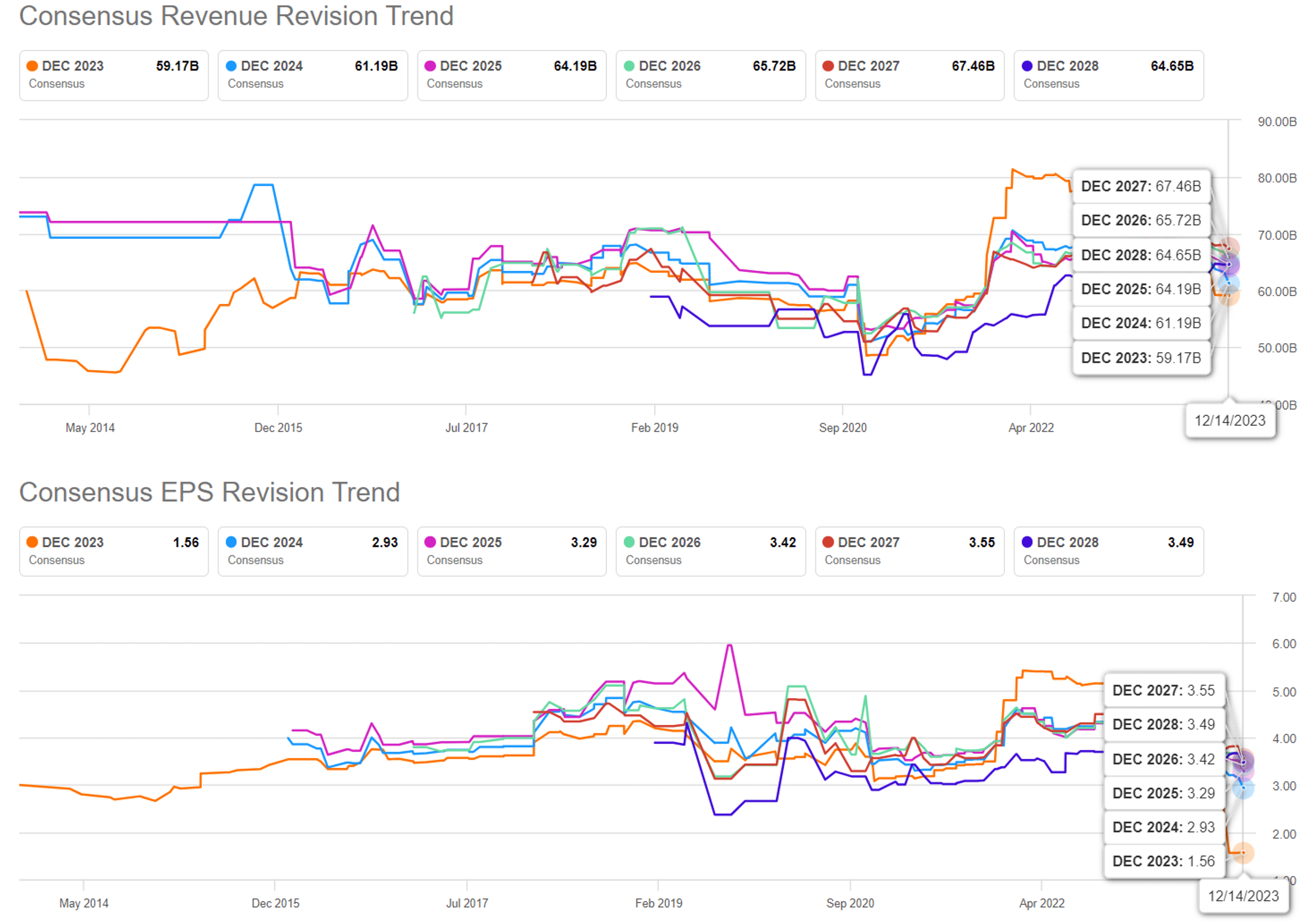

The Consensus Ahead Estimates

Tikr Terminal

The following downgrades in PFE’s ahead estimates aren’t stunning as effectively, with the pharmaceutical firm anticipated to generate a minimal prime and backside growth at a CAGR of +3.9% and +2.8% between FY2019 and FY2025, respectively.

That is in comparison with the earlier estimates of +4.4% and 5.9% over the identical timeframe, respectively.

The PFE inventory seems to be buying and selling above its honest worth of $19.80 as effectively, primarily based on the administration’s drastically lowered FY2023 adj EPS steering of $1.55 (down from the earlier steering of $3.35 and the annualized FQ2’23 adj EPS of $2.68) and its FWD P/E valuation of 12.78x (inline from earlier article).

Primarily based on the administration’s FY2024 adj EPS steering of $2.15, additionally it is evident that the inventory has pulled ahead a part of its upside potential to our NTM worth goal of $27.47.

Readers should additionally notice that PFE has been negotiating Medicare price revisions for 5 of its medicine since September 2023, with the brand new costs to enter impact from 2026 onwards.

We imagine that the affect could also be muted for now, with the blood thinner Fragmin solely comprising $228M of the pharmaceutical firm’s general top-line and Bicillin at $148M within the newest quarter, or the equal of 0.8% of its non-COVID portfolio, with the remainder not disclosed.

Then once more, the mix of underwhelming FY2024 steering, deteriorating stability sheet, and patent cliff/ Medicare headwinds from 2026 onwards doesn’t bode effectively to PFE’s intermediate time period prospects certainly.

We additionally imagine that its stock write-downs and goodwill amortization might speed up within the near-term, because of the impacted COVID demand and costly acquisitions, respectively.

So, Is PFE Inventory A Purchase, Promote, or Maintain?

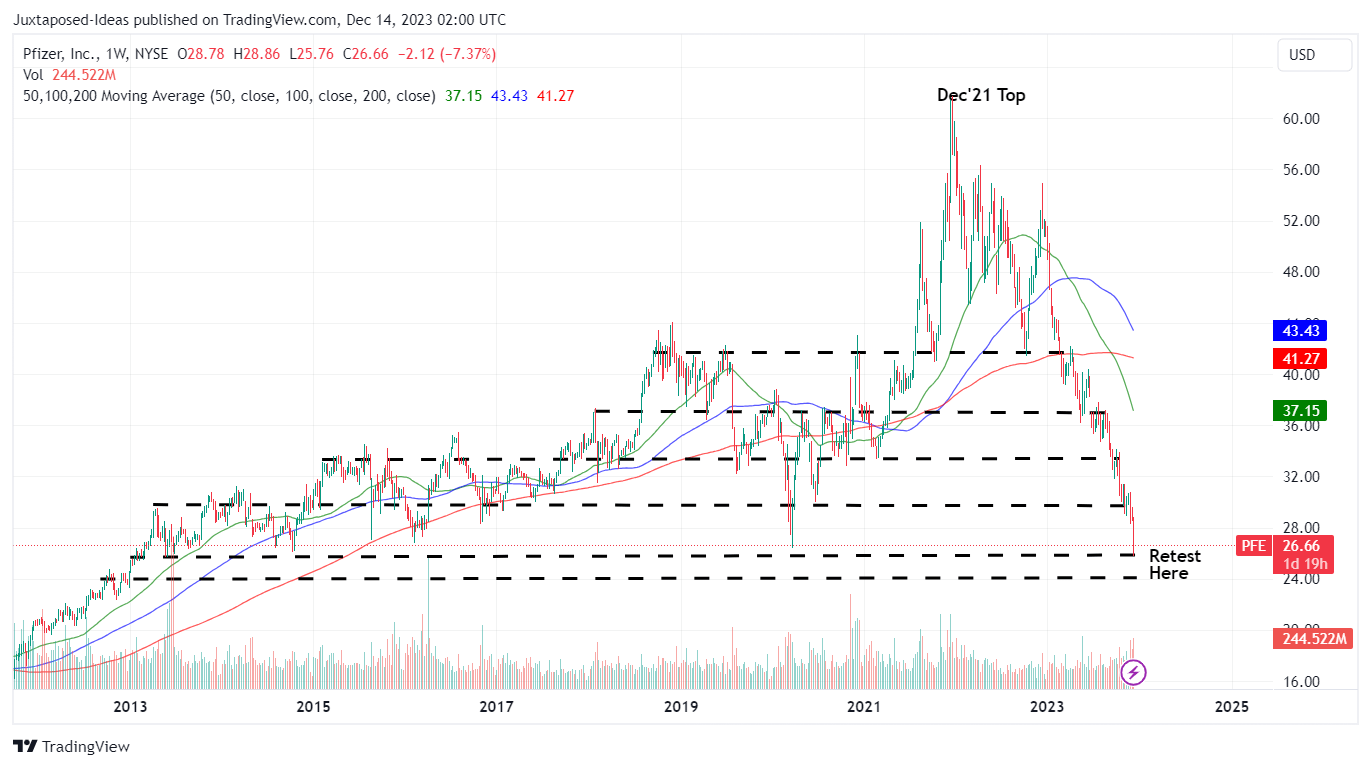

PFE 5Y Inventory Value

Buying and selling View

For now, PFE has already plunged drastically to retest its December 2012 ranges of $26s, with the dump closing the hole to its FQ3’23 e book worth of $17.54 (inline QoQ/ +6.2% YoY).

Whereas now we have no intention of recommending a Purchase at these ranges, it seems that everyone seems to be so bearish till the PFE inventory has been overly corrected, in our opinion.

Because of this.

The character of investing in pharmaceutical/ biotech shares have been speculative all alongside, since solely ~8% of clinical trials have been capable of obtain the coveted regulatory approval.

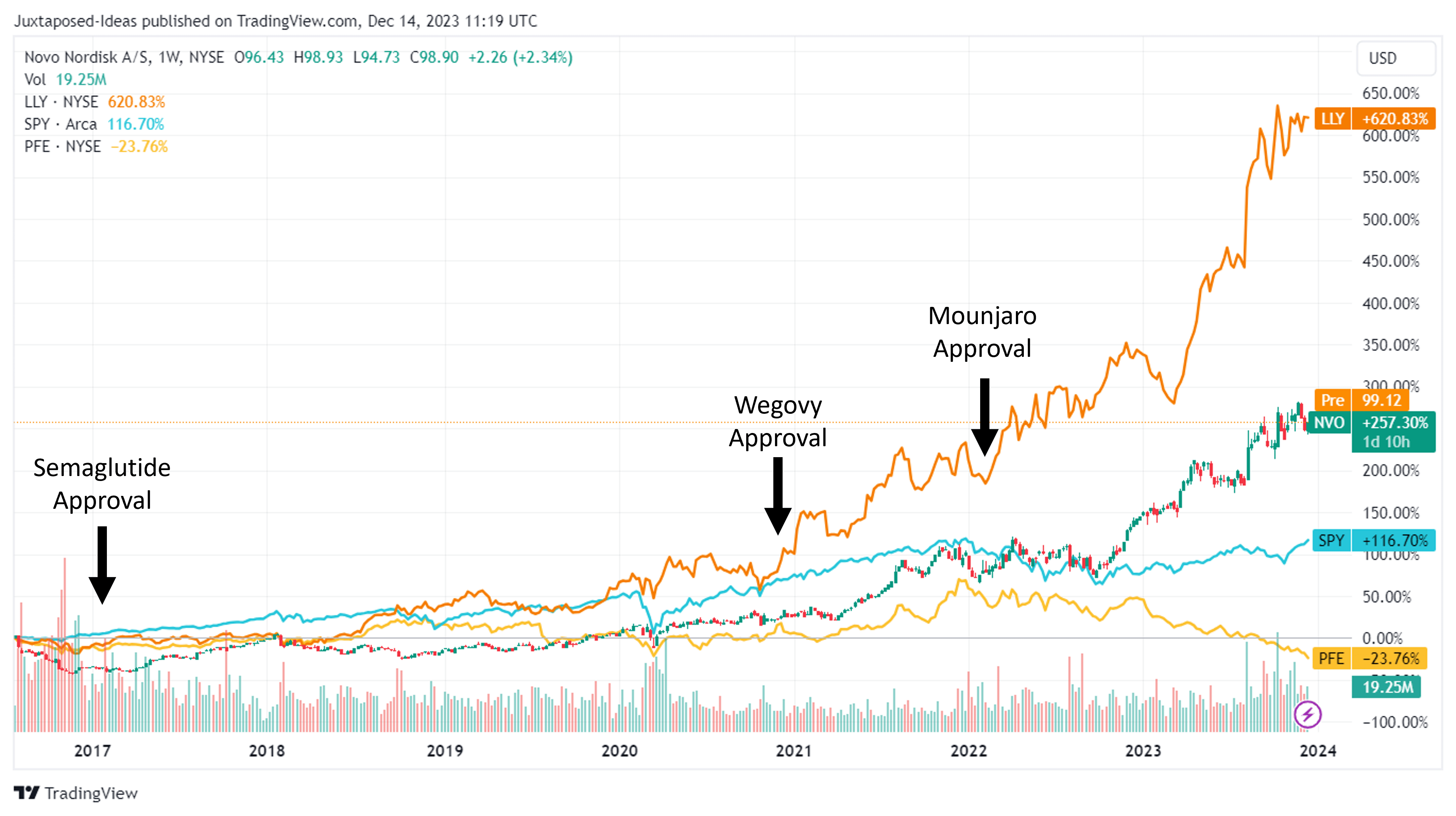

NVO & LLY Inventory Costs

Buying and selling View

For instance, Semaglutide was first accepted in 2017 for type-2 diabetes, with it solely gaining in recognition and hype after being accepted by the US FDA for weight reduction therapy in June 2021.

In any other case, it’s obvious that NVO, LLY, and PFE’s inventory actions have been considerably sluggish between 2016 and 2020, with minimal upside motion then.

Most significantly, valuations matter in any case. With PFE already drastically discounted at FWD P/E valuation of 12.78x, we imagine these ranges supply a extremely engaging threat/ reward ratio, as in comparison with LLY’s astronomical valuations at 88.11x and NVO at 36.63x.

Whereas the latter two’s funding theses could also be compelling, we keep our perception that there isn’t a level in chasing over valued shares with minimal margins of security, as equally highlighted by Peter Lynch:

There’s no disgrace in dropping cash on a inventory. Everyone does it. What’s shameful is to carry on to a inventory, or worse, to purchase extra of it when the basics are deteriorating.

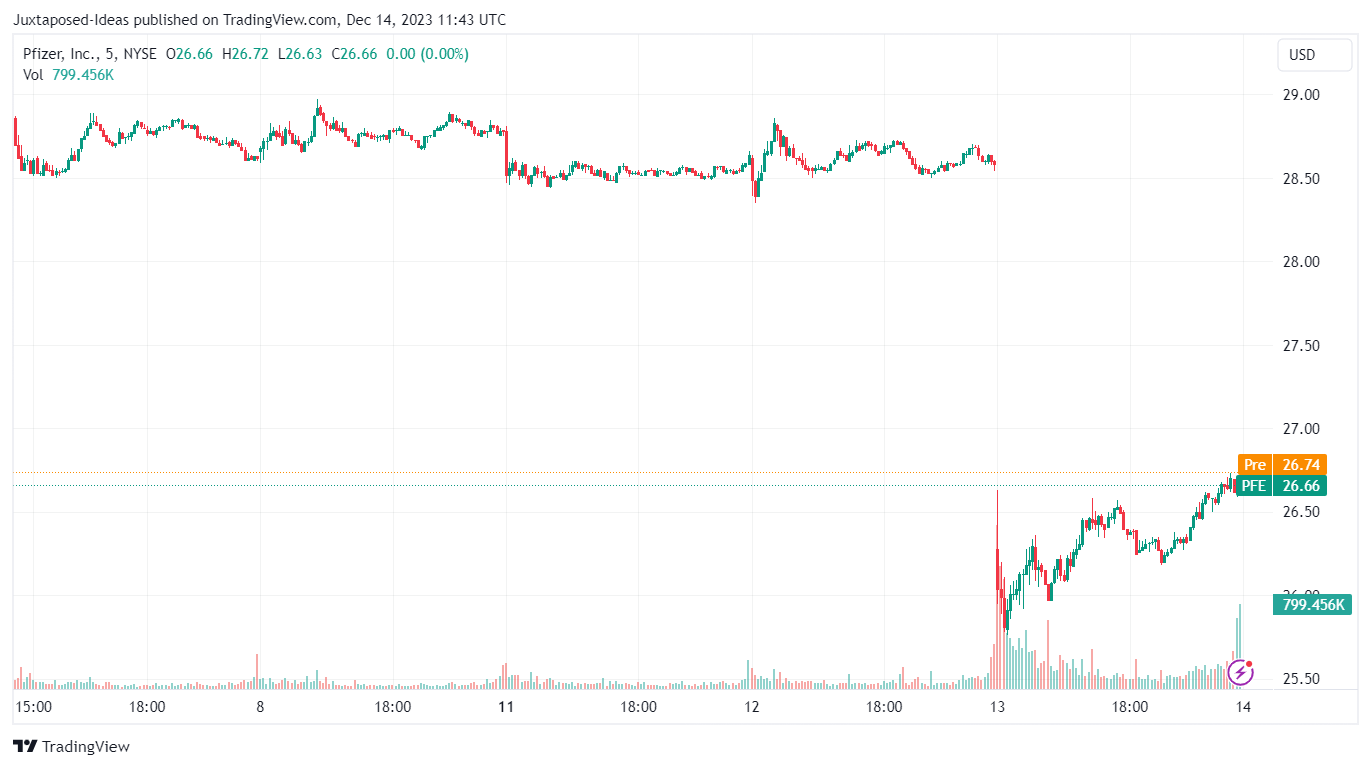

PFE 5D Inventory Costs

Buying and selling View

Whereas it stays to be seen how PFE might carry out transferring ahead, the inventory seems to have discovered bullish assist at $25.83 after the current freefall, with it already steadily climbing by +3.2% to $26.66 on the time of writing.

Whereas nobody can time the market, we imagine that the underside will materialize finally, particularly as a result of pharmaceutical firm’s expanded pipeline, aggressive R&D efforts, and COVID commercialization from H2’23 onwards.

Because of the overly steep correction, we imagine that Bob Farrell’s rule prone to run true right here:

Markets are inclined to return to the imply over time. Excesses in a single course will result in an reverse extra within the different course.

Because of the recently raised dividends, traders can also get pleasure from an expanded ahead yield of 6.28%, in comparison with the 4Y common of three.83% and sector median of 1.66%, particularly because the US Treasury Yields are already moderating to between 3.89% and 5.37%.

Regardless of so, we desire to cautiously keep our Maintain ranking for the PFE inventory, whereas recommending traders to watch its inventory trajectory earlier than shopping for, as soon as the inventory has established a sustainable backside. In any other case, traders might should undergo additional capital losses which is probably not lined by its dividend payouts.