Maryana Serdynska/iStock by way of Getty Photographs

Independence Realty Belief, Inc. (NYSE:IRT) is a REIT primarily concerned in buying, managing, and bettering multi-family condominium communities inside secondary markets.

Past its numerous portfolio in enticing markets, the quick working progress, and the conservative use of leverage, Independence Realty’s shares commerce at an enormous low cost to NAV, making the inventory a becoming selection for a price portfolio. On this submit, I’ll give you the thesis that helps these statements.

Diversified Portfolio in Enticing Markets

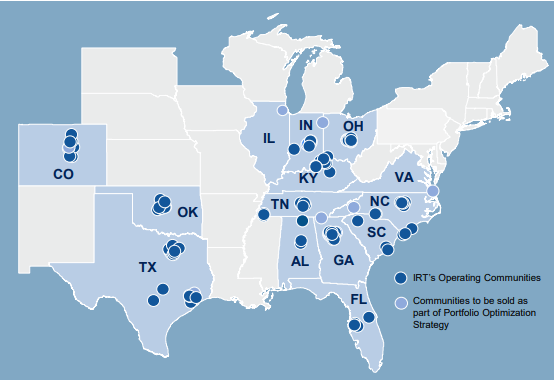

As of September 30, 2023, Independence Realty owned 120 multi-family condominium properties, consisting of 35,427 items throughout Virginia, Alabama, Colorado, Florida, Georgia, Illinois, Indiana, Kentucky, North Carolina, Ohio, Oklahoma, South Carolina, Tennessee, and Texas.

Investor Presentation

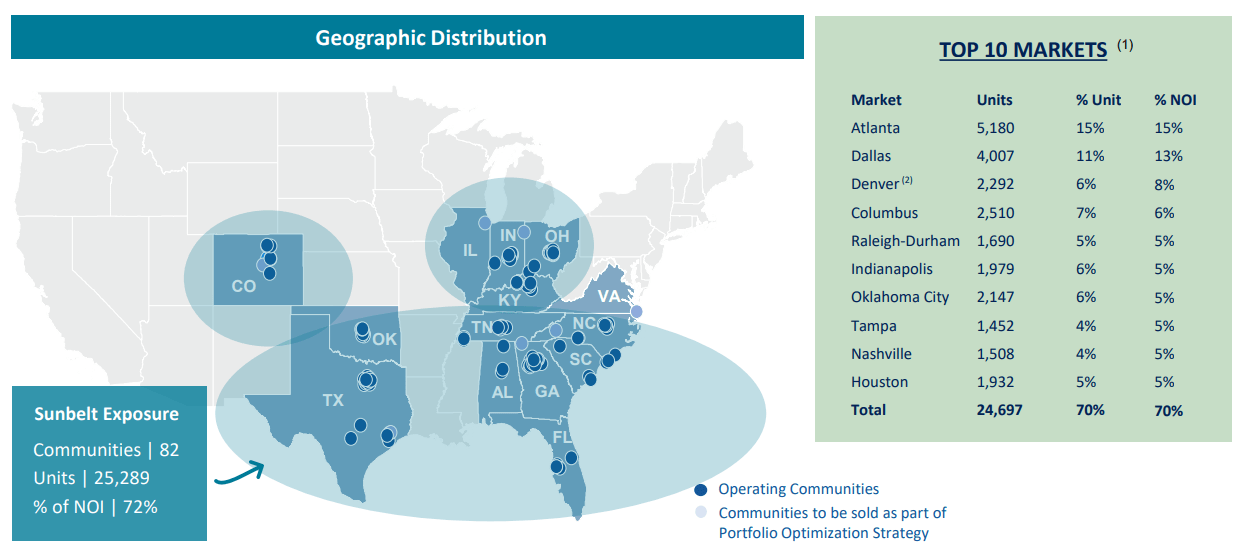

In addition to the truth that the portfolio is nicely diversified, we even have to understand that 72% is concentrated in Sunbelt states. That is an excellent space to have residential publicity to because it has skilled distinctive demand within the past 3 years and year-to-date.

Investor Presentation

Rising at an Unreasonable Tempo

In relation to occupancy, it stood at 94.6% for the same-store portfolio as of September 30; simply 0.4% increased than the speed reported for a similar interval the earlier yr. In my view, that is glorious. It depicts environment friendly administration of the property and leaves some room for progress.

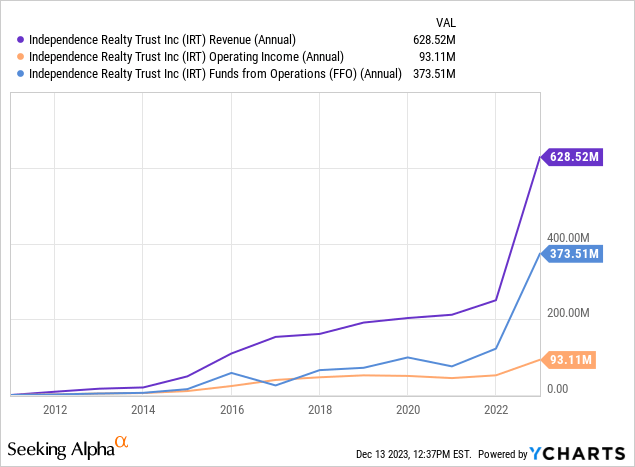

Additional, the REIT’s working efficiency has skilled outstanding progress up to now:

Income and working earnings have been restlessly making new highs, whereas FFO progress has been extra modest lately. Regardless, all of them made a giant bounce just lately.

The newest quarterly outcomes signify this current progress nicely. Beneath I am presenting the modifications between the latest annualized figures and the typical annual ones reported within the REIT’s final three fiscal years:

| Rental Income Development | 85.70% |

| NOI Development | 107.09% |

| AFFO Development | 107.01% |

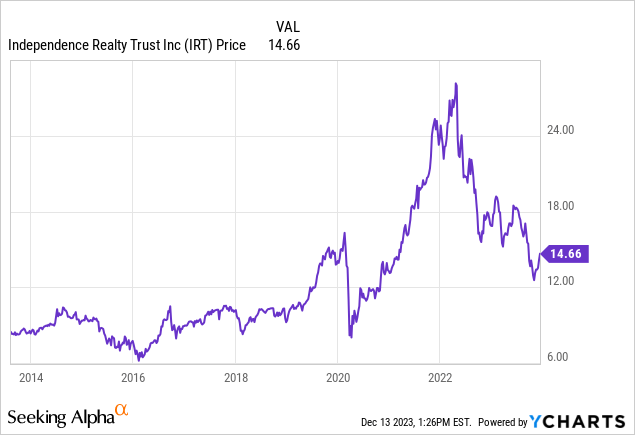

Now, I imagine that the market has appreciated the REIT’s previous operational efficiency. After the 2020 drawdown, it is evident that the market has responded nicely to its exponential progress:

All the identical, REITs could not keep away from the overall risk-off perspective of traders this yr and Independence Realty was no completely different. Because of this, I can’t attribute such YTD poor value efficiency to fundamentals; I’m positive that it’s going to find yourself being a hiccup looking back.

Low Leverage, Excessive Liquidity, No Important Maturities Till 2026

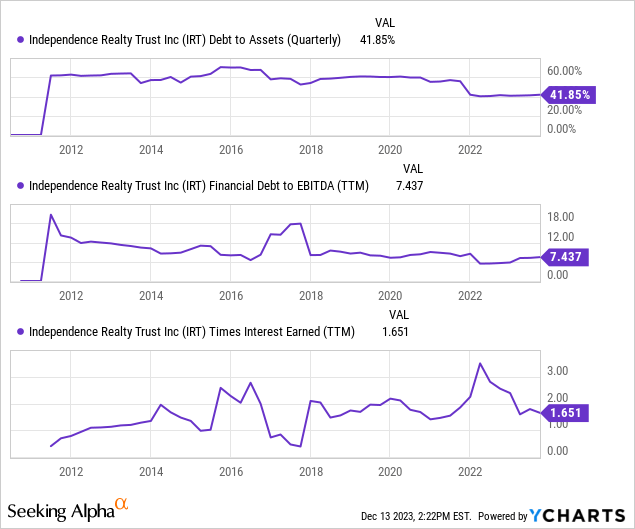

As for its leverage, the REIT is conservatively financed with debt accounting for 41.85% of its property; the ratio has additionally been pushed down lately from a ~60% degree. Furthermore, the debt-to-EBITDA ratio sits at 7.43 and curiosity protection is at 1.6, representing sufficient liquidity.

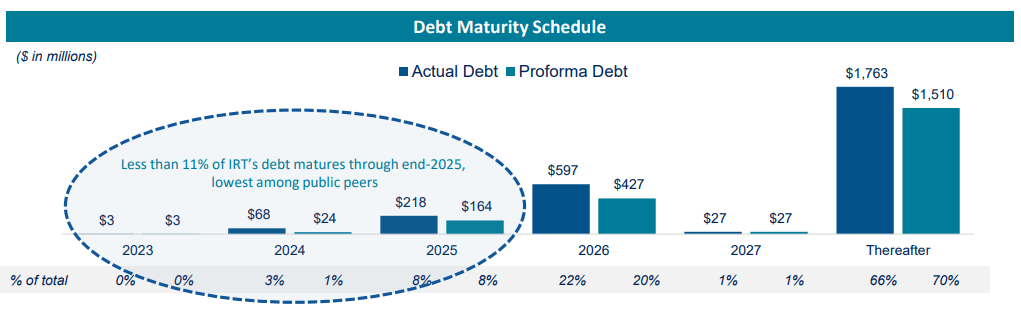

Additionally, upcoming maturities do not replicate any main hazard to increased financing prices, given the small quantities coming due in 2024/2025 and that the yr 2026, when about 20% of the REIT’s debt will mature, is sufficiently far-off from now for the present excessive interest-rate setting to have materially improved.

Investor Presentation

Low Yield however Excessive Low cost

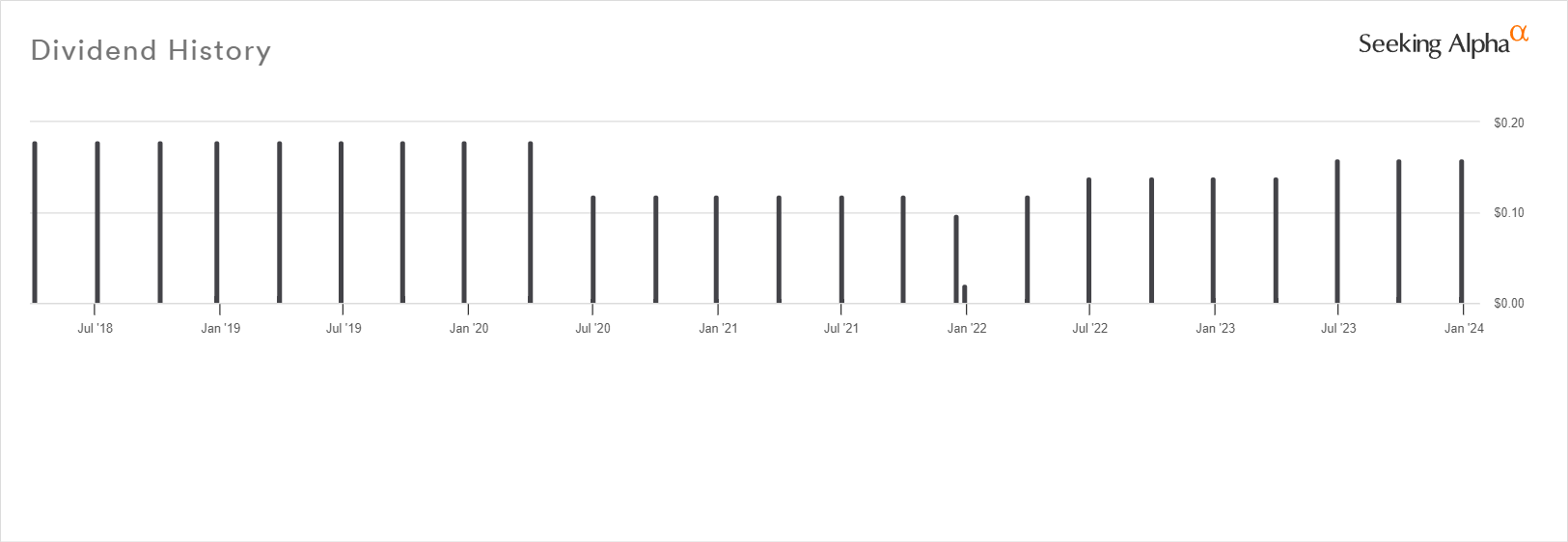

The REIT at present pays a $0.16 dividend per share which ends up in a ahead yield of 4.09%. Whereas the payout ratio primarily based on AFFO (final quarterly determine annualized) is low at 57.53%, the dividend declaration report has been erratic within the final 5 years:

Searching for Alpha

Due to that, I would not name the present distribution secure below adversarial circumstances.

Regardless, the inventory is undervalued at an implied cap fee of 6.52%. For residential properties within the Sunbelt area, a 5% cap fee could also be extra acceptable; which might lead to a $23.74 per share NAV and a 51.7% low cost primarily based on present ranges.

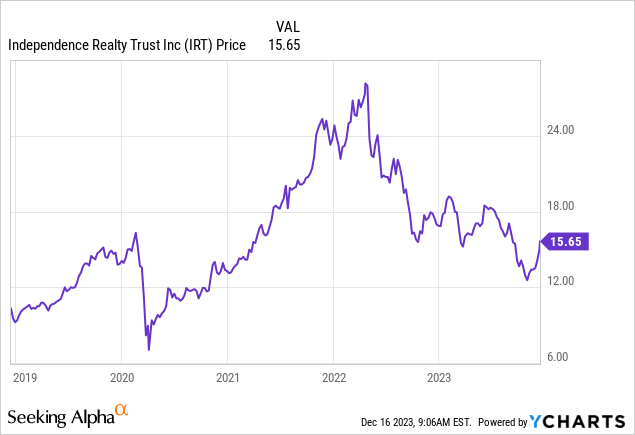

By the best way, only one yr in the past the inventory’s value had elevated increased than the present NAV:

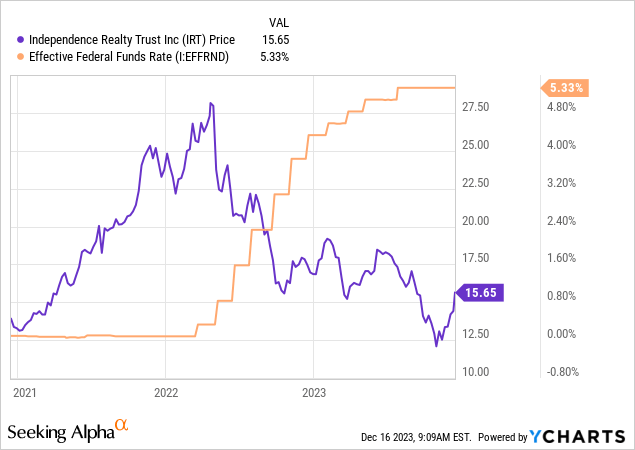

Then the Fed began elevating charges:

The market looks as if it has already reacted positively within the absence of any fee hikes currently; not simply with IRT in fact. I think about that the potential creation of a few fee cuts in 2024 will lead to a way more enthusiastic response and probably a repricing of IRT. If it is not throughout 2024, nevertheless, shareholders will must be affected person if they’re to appreciate the potential upside.

Dangers

Which brings me to the first danger right here. The low cost could also be big, however the upside a possible correction might understand will not be realized quick sufficient. An investor might incur a possibility price that the low yield of 4% won’t considerably offset.

One other danger that try to be conscious of is said to cap charges. Unlikely as I believe it’s, in the event that they develop for residential properties, the estimated NAV above won’t apply and the margin of security might slim. Do not forget that NAV calculation is just not a precise science and although the excessive predictability of a REIT’s profitability is a nice situation, cap charges are way more versatile; and so is NAV because of this.

Final, as I already stated, the dividend doesn’t seem secure due to the report. A dividend minimize is feasible, so traders should not base an funding resolution on the present yield alone.

Verdict

All in all, the steep low cost is sufficient for me to fee IRT as a BUY and I imagine that buying shares as much as $20 would offer a really enticing common margin of security.

What’s your take? Do you personal IRT or intend to? Why or why not? Be happy to share your ideas with me under and I will get again to you as quickly as I can. Thanks for studying!