Scott Olson

Although the markets have rallied over the previous few months, it is troublesome to recall typically that this 12 months has been an particularly powerful local weather for many companies. We owe some due respect – and maybe funding consideration – within the corporations which have been in a position to make operational enhancements amid this powerful macroenvironment.

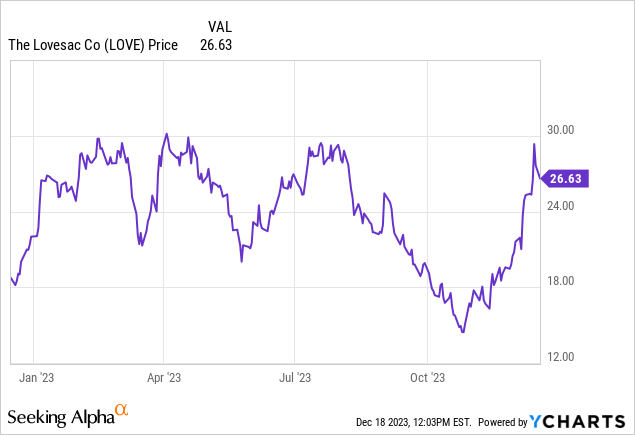

The Lovesac Firm (NASDAQ:LOVE), surprisingly, is a kind of names. The sectional furnishings maker has seen its share worth climb 20% this 12 months (roughly in step with the S&P 500), with a late-year rally making up for earlier losses.

I final wrote a bearish article on Lovesac in February, when the inventory was buying and selling nearer to ~$30. Quite a bit has occurred for Lovesac since then, together with a delayed Q2 earnings launch on the again of required accounting restatements. However in gentle of just lately launched Q3 results that I imagine exhibit energy within the enterprise, plus the decrease share worth since my final have a look at the inventory, I’m now extra sanguine on the corporate’s prospects and am ranking Lovesac at impartial.

I now see the corporate as a extra balanced bag of positives and negatives. On the intense aspect for Lovesac:

- Excessive gross margin merchandise. Lovesac generates wholesome >50% gross margins, which demonstrates each its positioning as an upper-middle tier residence decor product plus operational excellence. At scale, these excessive gross margins may also help Lovesac generate significant profitability.

- Modular product encourages cross-sell. Lovesac insists that its Sactionals product, which is roughly 90% of its income, is a “platform and not a product.” Whereas a bombastic assertion, the purpose is that clients can combine and match sectionals to create their desired furnishings structure, which inspires repeat gross sales of a number of merchandise.

- Omni-channel knowledgeable. Lovesac has a strong community of each company-owned retail shops in addition to pop-up places, most notably in Finest Purchase (BBY) shops. Having these third-party placements may also help the corporate scale back its opex footprint whereas nonetheless showcasing the model to consumers who will finally execute their purchases on-line.

On the identical time, nonetheless, we have now to be careful for the next:

- Residence items demand is down post-pandemic. The pandemic (and the transfer to the suburbs that it inspired) pulled ahead loads of demand for residence goods-related merchandise into 2020 and 2021. Now, amid more durable macro situations, shoppers’ willingness to spend on residence luxuries is dampened.

- Deep competitors. Furnishings is certainly not a simple market to compete in, and Lovesac has a lot deeper-pocketed rivals together with finances furnishings large IKEA and on-line market Wayfair (W), with its assortment of each decrease and higher-end manufacturers.

The underside line right here: I not essentially imagine there may be great draw back to go in Lovesac shares; however neither do I feel there are significant catalysts to get Lovesac to outperform in 2024. This inventory is now again on my watch record, nevertheless it’s not but a “rush to buy” identify both. Preserve monitoring this identify and investing elsewhere for now: look ahead to both the inventory to drop materially from right here, or for quarterly outcomes that materially speed up, earlier than shopping for again in.

Q3 recap

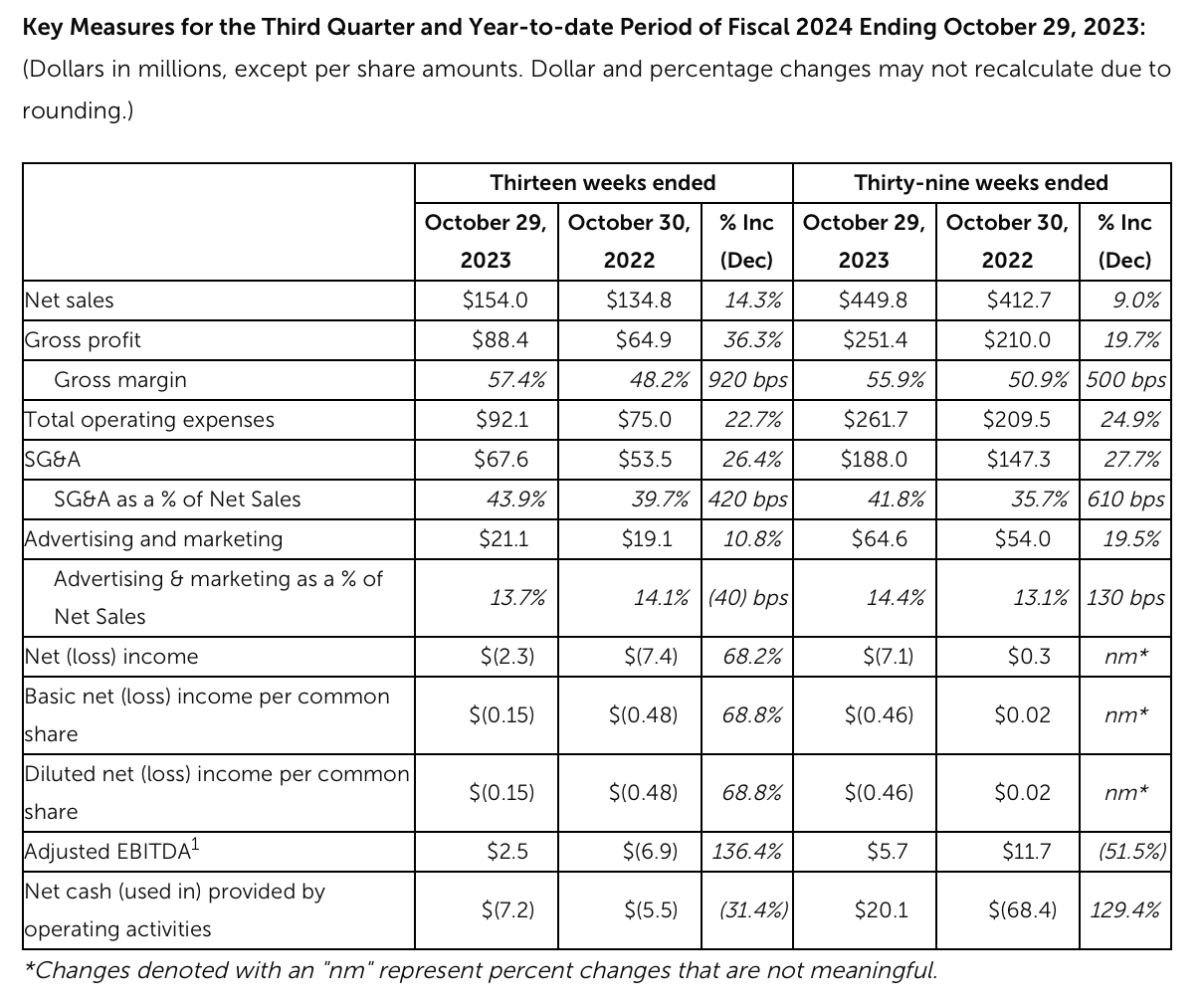

Let’s now undergo Lovesac’s newest quarterly leads to better element. The Q3 earnings abstract is proven under:

Lovesac Q3 outcomes (Lovesac Q3 earnings supplies)

Lovesac’s income grew 14% y/y to $154.0 million within the quarter, forward of Wall Avenue’s expectations of $153.8 million by a hair. Importantly, income progress accelerated relative to single-digit progress in Q1 (9% y/y) and Q2 (4% y/y).

It is price calling out as effectively that in contrast to different client merchandise corporations that rely closely on shipments to channel companions who maintain merchandise on their very own books, Lovesac does the majority of its enterprise via direct gross sales – which means there is no such thing as a stock cargo distortion on its income outcomes.

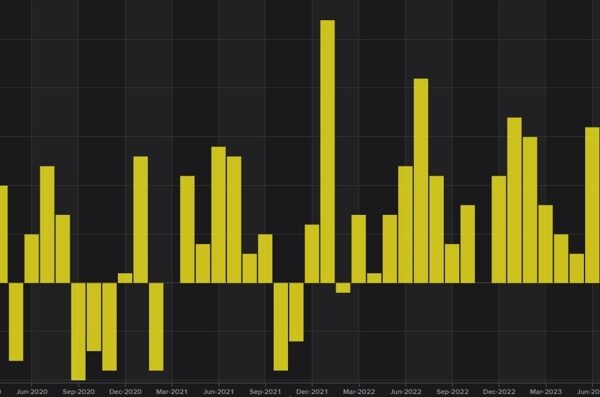

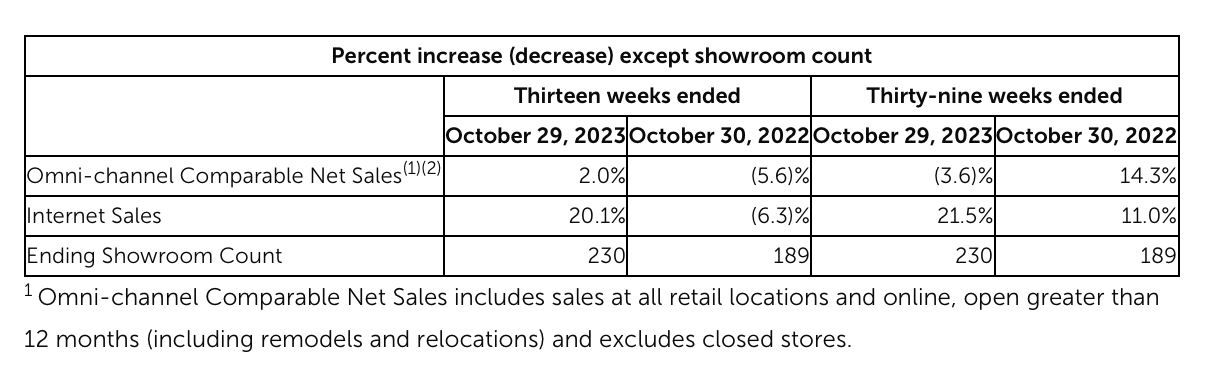

As proven within the chart under, the corporate’s Web gross sales soared to twenty% y/y progress in Q3. On the identical time, the corporate has additionally expanded its showroom depend to 230, up 22% y/y. On a comparable shops foundation, excluding the contribution from newly opened places, omni-channel gross sales had been up 2% y/y:

Lovesac showroom fleet (Lovesac Q3 earnings supplies)

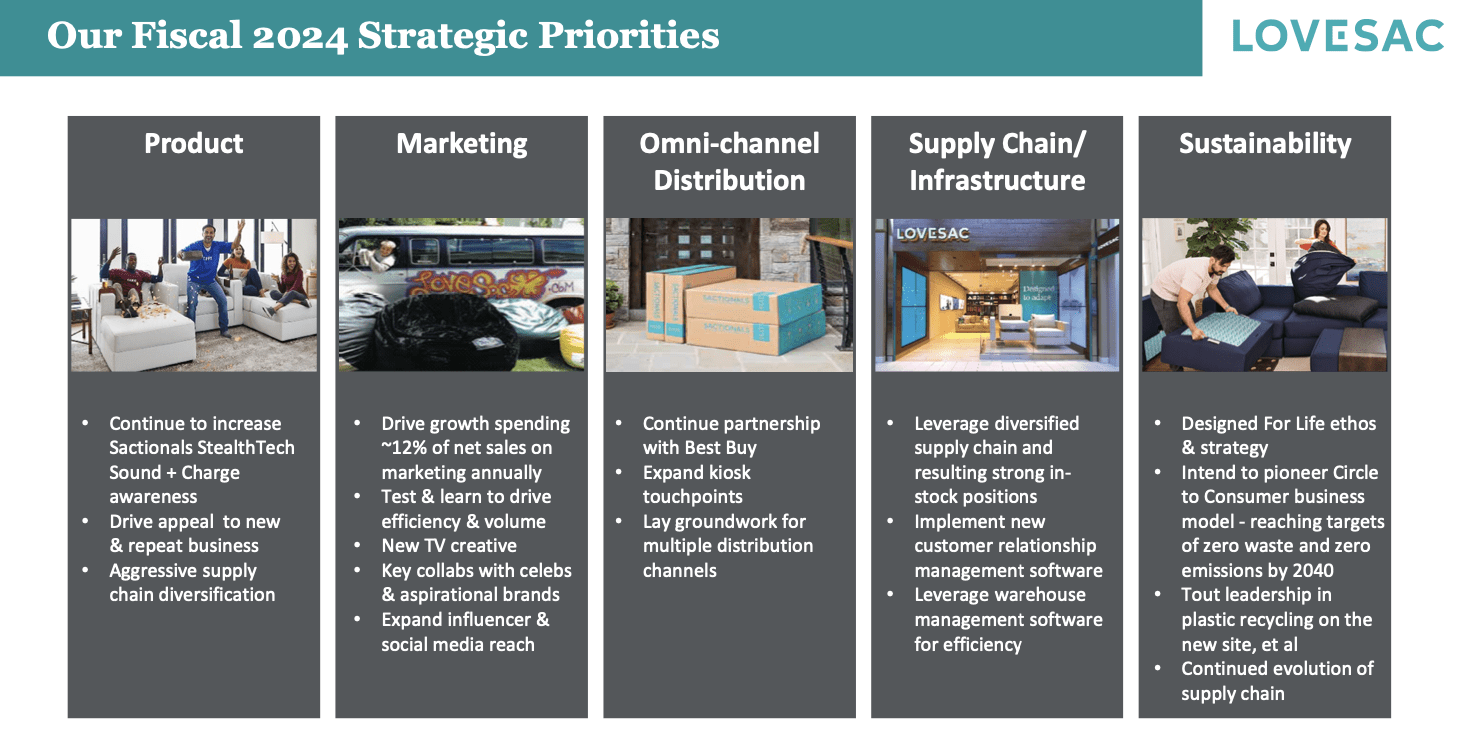

Increasing lower-touch storefronts has been a core precedence for Lovesac this 12 months, which has deepened its showroom partnership with Finest Purchase:

Lovesac strategic priorities (Lovesac Q3 earnings supplies)

The corporate has additionally continued to increase its footprint at Costco (COST) places as effectively. The long-term bull case for Lovesac can be to proceed deepening and diversifying its retail partnerships with these large-format, big-box shops. In doing so, the corporate will decrease its capex spend to open new shops in addition to restrict its opex in working these shops – overcoming its a lot smaller balance sheet in relation to its a lot bigger rivals.

Administration famous robust efficiency within the lead-up to the important vacation gross sales interval, which is a powerful main indicator for This autumn outcomes. Per COO Mary Fox’s ready remarks on the Q3 earnings call:

Class outperformance has continued this quarter with energy and demand versus final 12 months throughout Cyber 5, from Black Friday via Cyber Monday. And we’re very happy with our early outcomes. Some highlights from Cyber 5 embrace having our two largest gross sales days and the most important week in our historical past. We imagine this peak in gross sales that’s distinctive to our enterprise inside our class is due partly to our funding in constructing a model that’s unmatched within the furnishings class, coupled with supply to clients’ properties in just some days. Our clear technique for progress and the staff’s constant execution towards our progress methods permits us to proceed to gasoline our flywheel and drive operational excellence throughout the enterprise.”

From a profitability perspective, Lovesac’s gross margins jumped 920bps to 57.4%, which as previously noted is incredibly high for a consumer products maker. This was partially offset by higher opex spending, but overall, adjusted EBITDA clocked in at $2.5 million for the quarter, or a 1.6% margin – seven points higher than -5.1% in the year-ago quarter.

Key takeaways

Tendencies are shifting in the precise path for The Lovesac Firm, with accelerating gross sales outcomes and increasing gross margins. Add this inventory again to your watch record, however do not buy instantly.