jetcityimage

Article Thesis

Whereas Eli Lilly and Firm (LLY) has had a superb run in recent times, Pfizer (NYSE:PFE) has been a disappointment. However right this moment, Pfizer looks like the extra engaging funding and has, I consider, fewer execution and valuation dangers in comparison with Eli Lilly. I consider that locking in features in very costly Eli Lilly and shifting into low-cost and high-yielding Pfizer may very well be a good suggestion.

A Story Of Two Pharma Corporations

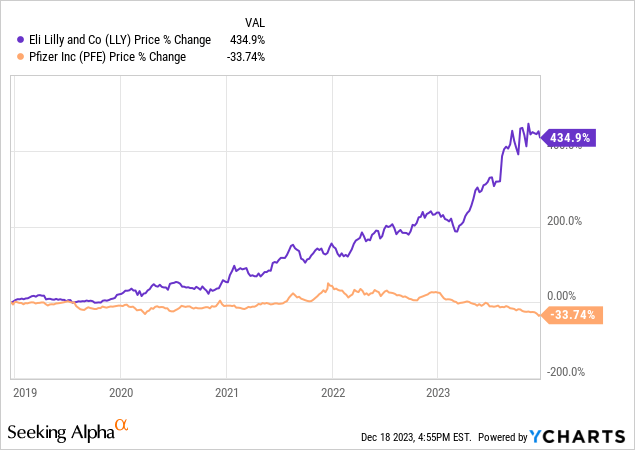

The charts of Eli Lilly and Firm and Pfizer Inc. during the last 5 years could not be rather more totally different than they’re now:

Eli Lilly soared by greater than 400%, greater than quintupling traders’ cash, even earlier than dividends. Pfizer, in the meantime, noticed its share value drop by round one-third during the last 5 years, regardless of an enormous bull run within the broad market. Much more surprisingly, Pfizer has massively underperformed regardless of producing gigantic income throughout the pandemic by way of the sale of its COVID vaccine (“Comirnaty”) and the sale of its COVID therapy (“Paxlovid”). It needs to be famous that Pfizer spun off some elements of its enterprise during the last couple of years, however nonetheless, the return distinction in comparison with Eli Lilly is dramatic. People who purchased Pfizer 5 years in the past will possible be fairly sad with their funding, whereas those that purchased Eli Lilly have possible been very glad, seeing their funding soar increased and better. However that does not imply that issues would be the identical going ahead.

Why Pfizer Might Be Higher Than Eli Lilly Going Ahead

After all, nobody is aware of for positive what the longer term will carry, however we are able to make estimates and take a look at possibilities. And I consider that there’s a good probability that Pfizer will considerably outperform Eli Lilly over the approaching years — though there is no such thing as a assure for that. I consider that that is possible because of the following causes:

1: (Lack of) Dependence on a single drug

All pharma corporations have smaller and bigger medication, and all pharma corporations are extra depending on some medication in comparison with others. However not all pharma corporations are equally depending on one drug or on one group of medication.

Pfizer is comparatively properly diversified throughout totally different areas, together with coronary heart ailments, oncology, vaccines, irritation, infectious ailments, and so forth. Its largest drug, or fairly group of medication, is the Prevnar household, which contributes round 14% of Pfizer’s revenues. If these revenues had been to fade in a single day, then Pfizer’s income would take a success, however the firm would possible nonetheless be fairly worthwhile, and its development outlook wouldn’t be harm dramatically.

In distinction, Eli Lilly appears extraordinarily depending on a single drug: Mounjaro/Zepbound. This drug was first accepted for sort 2 diabetes however has lately additionally acquired approval as an weight problems therapy. The overwhelming majority of the anticipated income development for the corporate over the approaching years depends on this single drug (tirzepatide) — truly, even on a single indication for this single drug, because the weight problems market is the place analysts and traders see Eli Lilly develop its revenues by quite a bit. Some analysts see Zepbound producing a number of dozens of billions of {dollars} in annual income in some unspecified time in the future sooner or later, which suggests Eli Lilly is extraordinarily depending on a single drug.

Which means if the drug is certainly as profitable as anticipated, it will likely be a hefty development driver. But when something goes incorrect, then that may very well be disastrous for the inventory, as the expansion outlook would take an infinite hit. Eli Lilly is anticipated to generate gross sales of $55 billion in 2026, trying on the present consensus estimate. If something had been to go incorrect with Zepbound, gross sales estimates would dwindle. And there are, in fact, some potential dangers — unknown long-term uncomfortable side effects may materialize over time, a competitor may carry a extra environment friendly drug to the market, and it is usually attainable (though not going) for patent points to come up. All in all, if a pharma firm may be very depending on a single drug, particularly on a single drug in a single indication, then that’s extremely dangerous. A extra diversified participant that advantages from development in numerous markets and that may steadiness out headwinds in a single space by way of its inside diversification appears much less dangerous.

2: Priced for perfection versus priced for catastrophe

There’s an previous and well-known saying about investing when there’s blood within the streets. Shopping for when sentiment is weak and when valuations are low makes for engaging entry costs whereas shopping for when there’s huge euphoria and when valuations are very excessive makes for unattractive entry costs.

Ideally, shopping for when valuations are low and locking in features when valuations are excessive is what traders ought to purpose for.

At present, Pfizer is priced for catastrophe and thus very low-cost, whereas Eli Lilly is priced for perfection and thus very costly.

Trying on the profit estimates for 2024, which is able to begin in lower than 2 weeks, Pfizer Inc. is at present valued at simply 12x internet income, which makes for an earnings yield of round 8%. Eli Lilly, in the meantime, is valued at 46x subsequent yr’s anticipated internet earnings, which makes for a valuation that’s round 4x as excessive as that of Pfizer.

For traders which are bullish on Eli Lilly as a result of its development potential over a couple of yr, we are able to additionally check out estimates for 2025: We see that Pfizer is anticipated to see its earnings per share develop by 31% in 2025, to $2.88, which makes for an earnings a number of of 9 primarily based on present costs. Eli Lilly is forecasted to see its income climb by 41% in 2025, which makes for an earnings a number of of 33. Once more, Eli Lilly is buying and selling at a valuation premium of a number of hundred proportion factors. Its anticipated development is increased, however the distinction between a 31% revenue development price and a 41% revenue development price is, I consider, not drastic sufficient to warrant a valuation that’s greater than 3 instances increased.

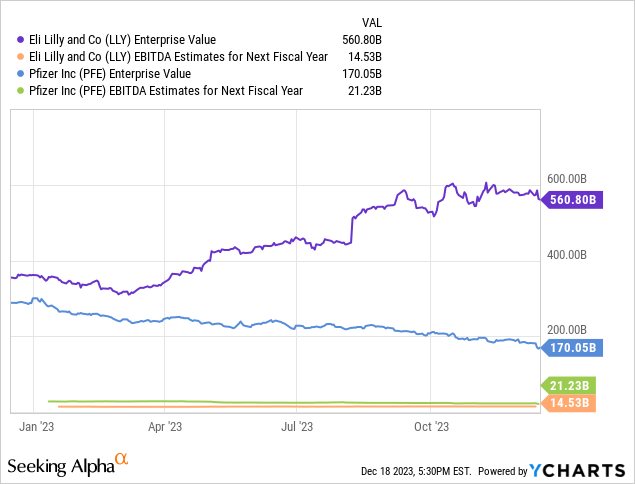

We are able to additionally take a look at totally different valuation metrics, and we are going to see the identical image. The next chart reveals Eli Lilly’s and Pfizer’s enterprise worth and EBITDA estimates for 2024:

Pfizer is at present buying and selling at 11.7x subsequent yr’s EBITDA, whereas Eli Lilly trades at 26.7x subsequent yr’s EBITDA. Once more, Pfizer is the way in which cheaper inventory, buying and selling at lower than half the valuation of Eli Lilly — even once we account for debt on the steadiness sheets of the 2 corporations. fairness valuations alone, Pfizer is even cheaper, relative to Eli Lilly, as we’ve got seen earlier when utilizing the price-to-earnings a number of.

3: Dividends as a complete return booster

Share value features are good, however dividends matter quite a bit as properly in terms of producing complete returns:

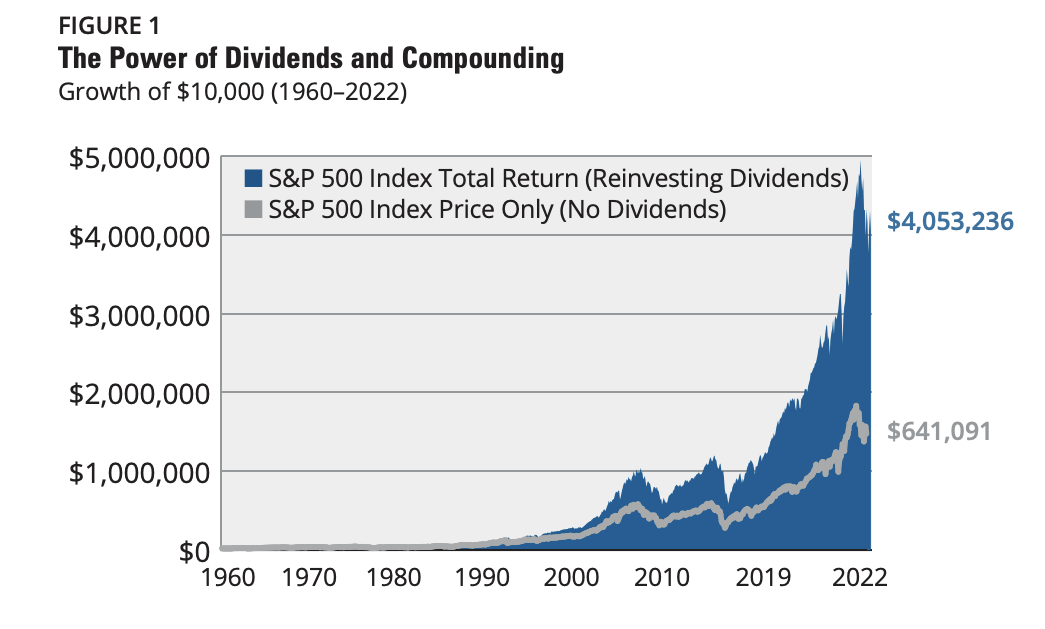

Dividend contribution to complete returns (hartfordfunds.com)

The above chart from a whitepaper from Hartford Funds reveals that the S&P 500’s complete returns during the last couple of many years drastically depend upon dividends and the reinvestment of those dividends. With out them, complete returns would have been simply 15% of what they’d been with all dividends reinvested.

At present, Pfizer’s dividend yield may be very totally different from that of Eli Lilly: Pfizer simply raised its dividend and is now providing a dividend yield of 6.2%, whereas Eli Lilly’s dividend yield is simply 0.9%. In different phrases, Pfizer supplies round 7x the revenue Eli Lilly supplies — one must make investments $70,000 in Eli Lilly to get the identical dividends as one can get from a $10,000 funding in Pfizer. Dividend yield is not all the pieces, however with the large significance of dividends for complete returns over a longer-term interval and with the dividend yield being so drastically totally different between Pfizer and Eli Lilly, I consider Pfizer’s means higher revenue technology potential is a crucial purpose to favor Pfizer over Eli Lilly at present costs.

Takeaway

Is Pfizer a greater firm than Eli Lilly? One can argue that PFE’s means higher diversification is a plus and that the current Seagen acquisition offers it extremely interesting oncology belongings, however I nonetheless would not say that Pfizer is a greater funding than Eli Lilly. Would I favor Pfizer over Eli Lilly if each had been valued at $300 billion? I would not, to be sincere, nor would I favor Pfizer over Eli Lilly if each traded at 20x, 30x, or 40x internet earnings.

However with well-diversified Pfizer buying and selling at simply 12x subsequent yr’s earnings, whereas Eli Lilly trades at a massively increased valuation, I consider Pfizer is extra engaging right this moment. If something goes incorrect at Eli Lilly with Zepbound, that may very well be dramatic for its share value — Pfizer doesn’t have the identical threat as a result of not being priced for notion and since it isn’t as depending on a single development asset. Add the hefty dividend yield of Pfizer and distinction it to the very low yield one can get from Eli Lilly, and the previous seems to be higher at present costs.

With one inventory being very low-cost and out of favor, and the opposite having run up massively and being in a state of euphoria, I consider the previous is the extra opportune funding. At totally different costs, the decision may very well be totally different, however right here it is sensible, I consider, to lock in features in very costly LLY and to shift them into Pfizer (or one other very cheap pharma firm).